The Austin Mortgage Market Is Unforgiving. Your Application Needs to Be Ready.

You have been renting in South Austin for three years, watching home prices climb. Perhaps, have been watching listings in Mueller disappear in days. You have friends who just closed in Cedar Park, and you are wondering if you missed your window.

You have not. So that means the way you approach your Austin mortgage application will determine whether you get into a home on terms that build wealth or drain it.

Austin is one of the most competitive housing markets in the country. As a result, the median home prices in Travis County have remained significantly above the national average. This is even as the broader market has cooled. Buyers in West Lake Hills, Round Rock, and Pflugerville are competing against well-prepared applicants who have strong credit profiles and pre-approvals already in hand.

Entering the market without understanding how lenders evaluate you can be costly. Your credit profile affects your mortgage rate, monthly payment, and the total price paid for your home. Not knowing how to strengthen your credit before applying could cost you tens of thousands over the life of your loan.

This guide exists to change that. Let’s walk through key milestones that will help you secure the best mortgage in Austin.

How Austin Mortgage Approval Works

It Is Not Just About Your Credit Score. Most buyers assume that mortgage approval starts and ends with their credit score. Moreover, lenders look at a much broader picture than that single number.

Your debt-to-income ratio is often the first filter. Most conventional lenders want your total monthly debt to stay below 43% to 45% of your gross income. This includes your new mortgage payment, along with other debts such as credit cards, car loans, and student loans.

FHA loans allow slightly higher ratios in some cases, but the threshold exists across all loan types.

Employment history and income stability matter big-time. Lenders want to see two years of consistent employment in the same field. Self-employed buyers, freelancers, and gig workers are usually reviewed more carefully by lenders. Most lenders also want to see two years of tax returns that show stable or growing income.

Payment consistency on existing accounts tells lenders how you behave as a borrower. A single 30-day late payment in the past 12 months can trigger overlays that increase your rate or require additional documentation. Two late payments in that window can disqualify you from certain loan programs entirely.

Reserves are the final piece most buyers overlook. Many lenders require 2 to 6 months of mortgage payments to be in your account after closing. Depleting your savings entirely to cover the down payment raises flags.

Loan Types Available to Austin Buyers

FHA loans are backed by the Federal Housing Administration and are usually the most accessible entry point for first-time home buyers in Austin. They allow down payments as low as 3.5% for buyers with scores of 580 or higher, and buyers with scores between 500 and 579 may qualify with a 10% down payment. FHA loans also require mortgage insurance premiums, which add to your monthly cost, regardless of your down payment amount.

Conventional loans differ from other options in that they require stronger credit profiles, typically a minimum of 620, though most lenders prefer 680 or higher for the best terms. Down payments start at 3% for qualifying buyers. Private mortgage insurance applies until you reach 20% equity.

VA loans are available exclusively to eligible veterans and active-duty service members. These loans are backed by the Department of Veterans Affairs, require no down payment, and do not require private mortgage insurance. VA loans usually offer competitive interest rates, which can be equal to or lower than conventional loan rates.

Jumbo loans are particularly relevant in the Austin market, given local home prices. In Travis County, loans above the conforming loan limit require jumbo financing. Unlike conforming loans, jumbo products have stricter credit requirements, including typical credit scores of 700 or higher, larger down payments, and reserve requirements that can reach 12 months of mortgage payments.

Texas-Specific Factors Every Austin Buyer Must Understand

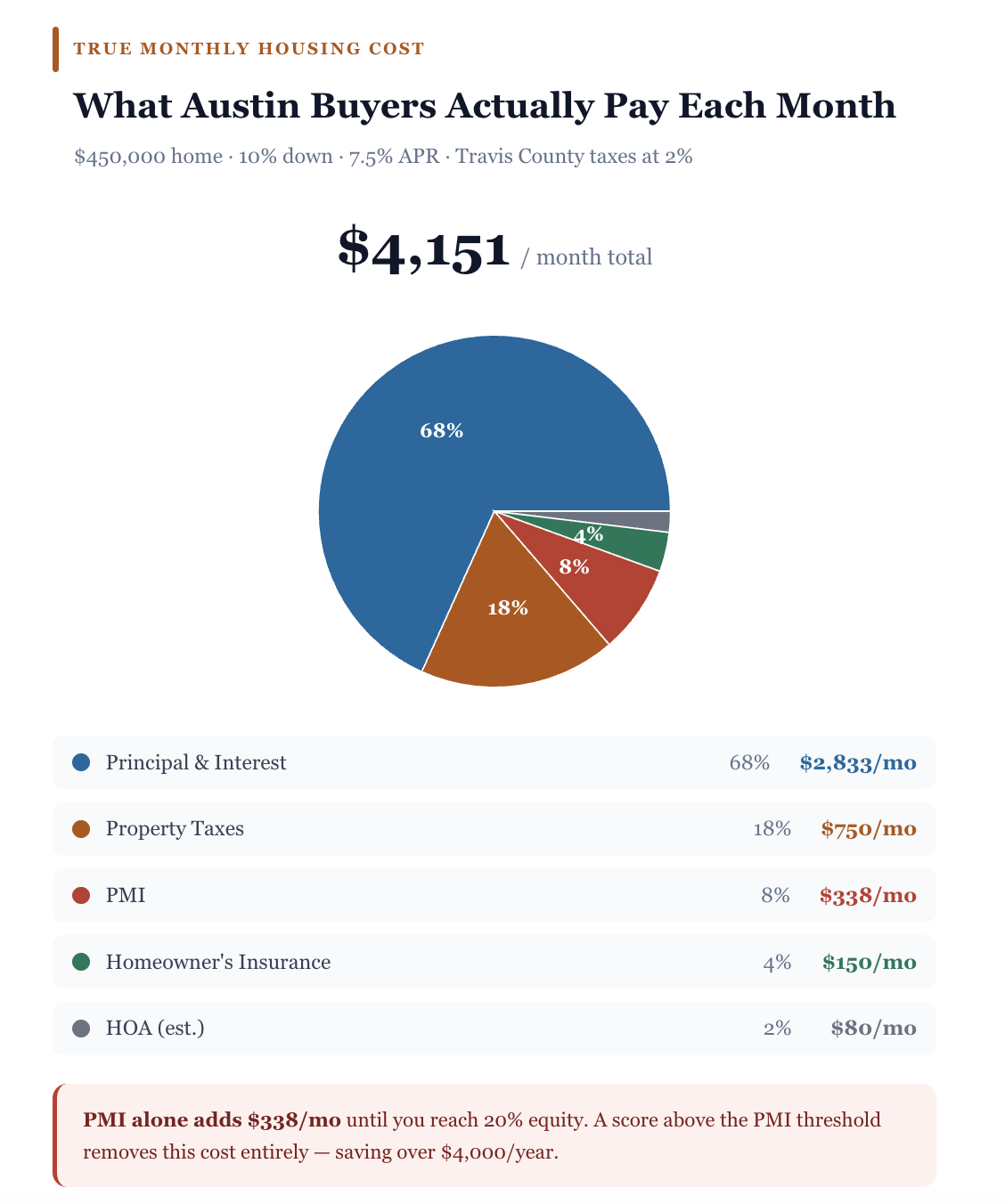

Travis County property taxes are among the highest in Texas and significantly affect your total monthly housing cost. Property taxes in Travis County average between 1.7% and 2.2% of assessed value annually. On a $450,000 home, that represents $7,650 to $9,900 per year added to your cost of ownership, factored directly into your debt-to-income calculation by lenders.

The Texas homestead exemption reduces the taxable value of your primary residence for school district taxes. Filing for the exemption after closing reduces your annual property tax burden and is a step every Austin homeowner should complete immediately after purchase.

Texas is a non-judicial foreclosure state. If a borrower defaults on a mortgage, the lender can foreclose without going to court. Foreclosures can move quickly in Texas, sometimes completing within 60 days of the first notice. It’s important to understand this before you take out a loan.

In Texas, choosing a mortgage payment you can afford in the long term is especially important. If your finances change, a payment that’s too high can quickly become a problem.

Current Mortgage Rates in Austin

What Austin Mortgage Rates Actually Mean for Your Budget

Current mortgage rates in Austin follow national trends but are influenced by local factors, including loan type, credit tier, loan-to-value ratio, and lender. What most buyers focus on is the rate itself. What they should focus on is the difference between the rate they qualify for today and the rate they could qualify for with 60 to 90 days of preparation.

Here is what that difference looks like on a real Austin transaction.

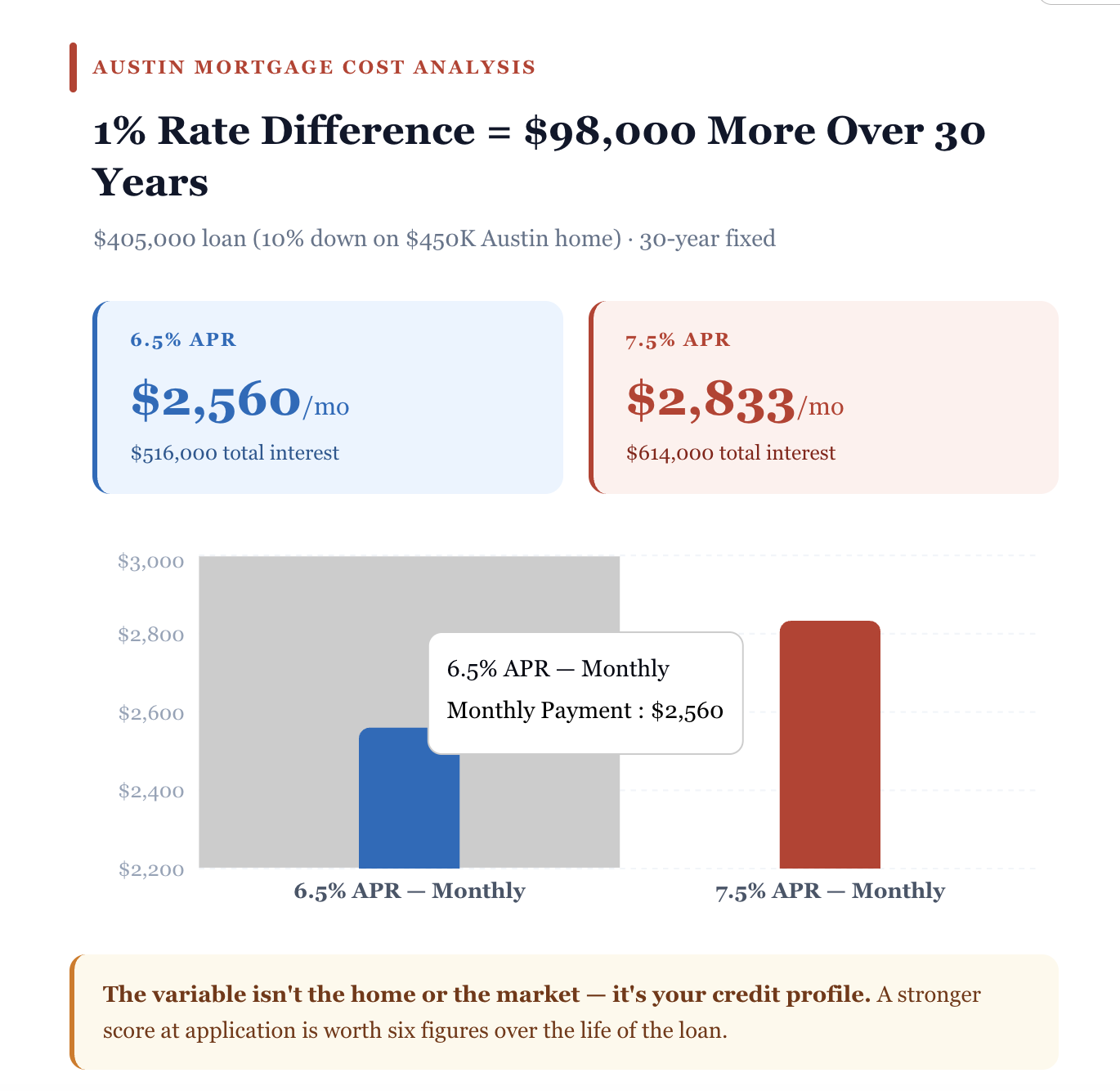

You are purchasing a $450,000 home with 10% down, financing $405,000 over 30 years.

At 6.5% APR, your principal and interest payment is approximately $2,560 per month. Your total interest paid over the life of the loan is approximately $516,000.

At 7.5% APR, your principal and interest payment rises to approximately $2,833 per month. Your total interest paid over the life of the loan climbs to approximately $614,000.

That one percentage point difference costs you $273 per month. So that’s approximately $98,000 over the full loan term. In the same house. With the same down payment.

The variable is not the home, nor is it the market. The variable is your credit profile.

How Your Credit Score Affects Your Austin Mortgage Rate

Mortgage lenders use a tri-merge credit report that pulls from all three bureaus and uses the middle score for qualification. The rate tier assigned to you is directly tied to where that middle score lands on the day your application is submitted.

A buyer with a 760 score applying for a conventional loan on a $450,000 Austin home may receive a rate offer meaningfully lower than a buyer with a 680 score applying for the same product at the same lender on the same day. The difference in qualification tier can also affect whether private mortgage insurance is required and at what premium level.

PMI on a conventional loan typically costs between 0.5% and 1.5% of the loan amount annually. On a $405,000 loan, that is $2,025 to $6,075 per year, or $169 to $506 per month, added to your payment until you reach 20% equity.

A credit score that eliminates PMI or drops you into a lower rate tier is not a minor detail. It is thousands of dollars per year.

How to Improve Your Approval Odds Before Using a Mortgage Lender in Austin, TX

The Preparation Window Most Buyers Skip

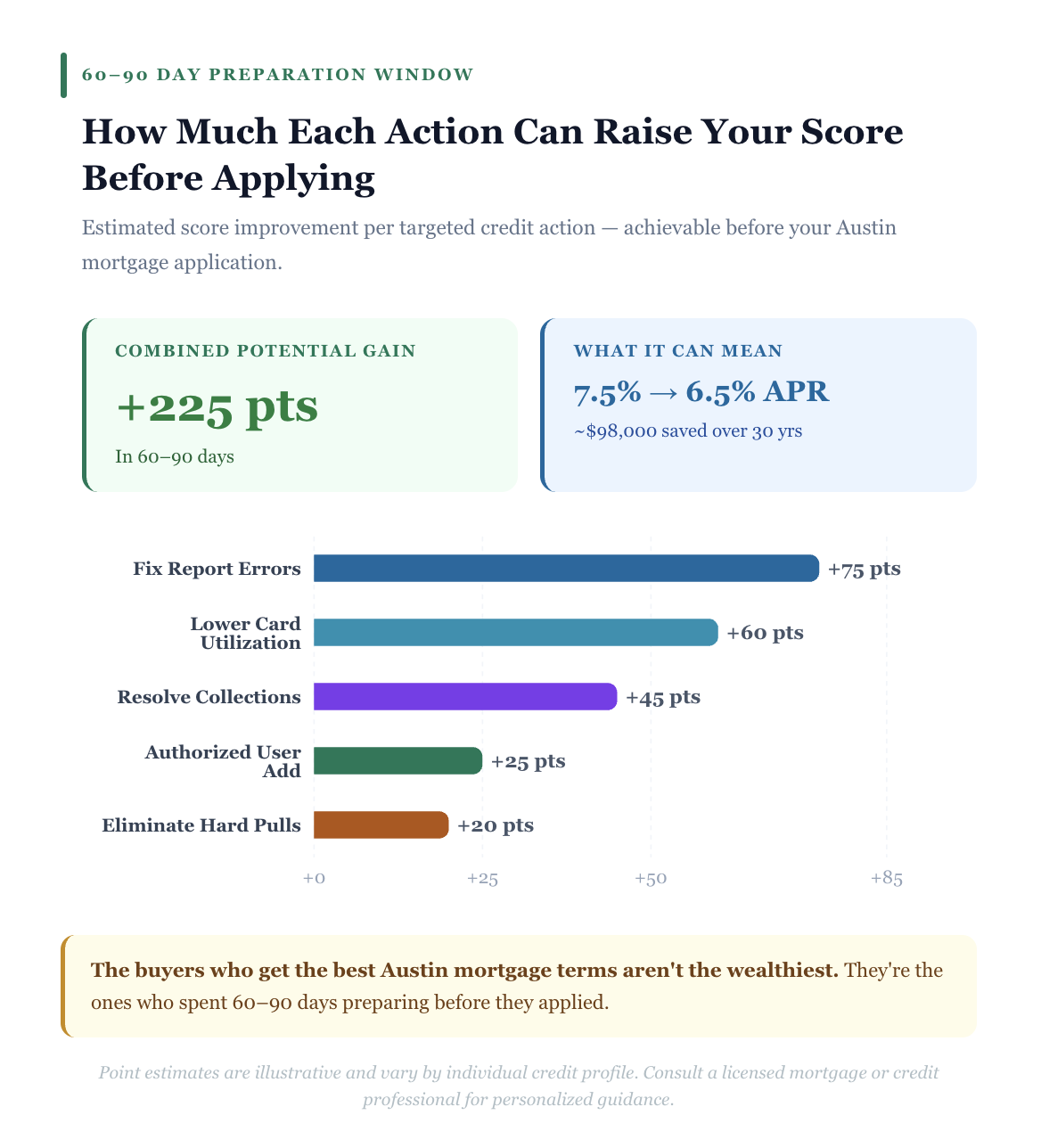

The buyers who get the best Austin mortgage terms are not necessarily the wealthiest or the most financially sophisticated. They are the ones who started preparing 60 to 90 days before they applied.

That preparation window is where credit work happens. It is where utilization ratios get corrected, where inaccurate items get removed, and where the score moves from one rate tier to the next.

Remove Inaccurate Negative Items

Pull your credit reports from all three bureaus at AnnualCreditReport.com and review every account for accuracy. Incorrect late payment markers, accounts that do not belong to you, balances reported higher than they actually are, and collection accounts past the reporting period are all disputable under the Fair Credit Reporting Act.

Removing a single inaccurate 30-day late payment from a mortgage lender's perspective can be the difference between qualification and denial on certain loan products. This step costs nothing and can produce results within 30 to 45 days.

Reduce Credit Utilization Below 30 Percent

Credit utilization, the ratio of your current balances to your total credit limits on revolving accounts, accounts for 30% of your FICO score. High utilization suppresses your score every single month, regardless of your payment history.

Paying balances below 30% of each card's limit produces a measurable score increase within one billing cycle. Getting below 10% on each card produces the strongest result. For buyers applying for a mortgage in North Austin, Round Rock, or Pflugerville, this single step frequently moves scores 20 to 40 points in a short window.

Stabilize Your Income Documentation

Lenders evaluating Austin home loan rates and your qualification will request the most recent 30 days of pay stubs, two years of W-2s, and two months of bank statements at a minimum. Inconsistencies between these documents, unexplained large deposits, or gaps in employment history create underwriting conditions that delay approval or result in denial.

Avoid changing jobs, going from salaried to self-employed, or making large, undocumented transfers during the 60 to 90 days before you apply.

Avoid New Credit Inquiries

Every hard inquiry from a new credit application reduces your score temporarily. In the months before applying for an Austin mortgage, do not open new credit cards, finance a vehicle, or apply for any new credit product.

If you are rate shopping among mortgage lenders in Austin, TX, multiple mortgage inquiries within a 14-day window are treated as a single inquiry by most scoring models. Rate shopping is smart. Applying for new consumer credit during this window is not.

Recommended Article: What Is a Soft Pull on Your Credit? Expert Answers

Should You Fix Your Credit Before Applying for an Austin Mortgage?

The Question Every Serious Buyer Should Ask

The answer depends on where your score sits today and what loan product you are targeting. If you are already above 740, the incremental benefit of additional credit work before applying is limited. On the other hand, if your credit score is between 620 and 700, consider taking 60 to 90 days to improve your credit before applying for a mortgage in Austin.

A higher score could help you get a lower rate.

Here is what a 40-point score improvement can realistically produce for an Austin buyer.

It can move you from a 7.5% rate tier to one closer to 6.5% on a conventional loan. On a $405,000 loan, that is approximately $273 per month and close to $98,000 over 30 years. It can eliminate the PMI requirement entirely if you cross the threshold that removes it under your lender's guidelines. It can expand your lender options, including access to portfolio lenders and credit unions offering competitive Austin home loan rates that are not available to buyers in lower score tiers.

An 80-point improvement can shift you from an FHA-only qualification into conventional loan eligibility, removing mortgage insurance premiums from your payment structure entirely.

The Smarter Path Into the Austin Market

The Austin housing market rewards buyers who are prepared. Competition in neighborhoods like Mueller, Cedar Park, and West Lake Hills means sellers frequently have multiple offers. A buyer with a strong pre-approval letter from a well-regarded lender, backed by a clean credit file and documented financial stability, presents a fundamentally more attractive offer than a buyer whose pre-approval is conditional and carries credit caution.

Preparation is not just about your rate. It is about your competitive position in one of the country's most active real estate markets.

Before you apply with a lender, consider a free credit review to see if you can qualify for better terms. That conversation takes less than 20 minutes and can identify specific actions that move your score before your application is submitted.

Austin Mortgages Frequently Asked Questions

What credit score do you need for an Austin mortgage?

FHA loans in Austin allow scores as low as 580 with 3.5% down. Conventional loans generally require 620 minimum, though most lenders prefer 680 and above for standard terms. Jumbo loans, common in higher-cost Austin areas, typically require a 700 or higher. The higher your score, the better your rate and the broader your lender options.

How much income do you need to buy a home in Austin?

At a $450,000 purchase price with 10% down and a 7% rate, your principal, interest, taxes, and insurance payment will likely range from $3,200 to $3,600 per month. Most lenders cap total debt obligations at 43% to 45% of gross monthly income, meaning you would generally need a gross household income of approximately $85,000 to $95,000 annually at a minimum for this price point.

Do Austin mortgage lenders check all three credit bureaus?

Yes. Most mortgage lenders use a tri-merge credit report that pulls from Equifax, Experian, and TransUnion simultaneously. The middle score of the three is used for qualification and rate determination. If two borrowers are on the application, the lender typically uses the lower of the two middle scores as the qualifying score.

Is Texas a judicial foreclosure state?

No. Texas is a non-judicial foreclosure state. Lenders can foreclose on a defaulted mortgage without going through the court system. Texas foreclosures can move significantly faster than in judicial states, sometimes completing within 60 days of the initial notice of default. Understanding this timeline reinforces the importance of choosing a payment that remains manageable under financial stress.

Can I use an Austin mortgage calculator to estimate my payment?

Yes, and you should. An Austin mortgage calculator gives you a baseline principal and interest figure. For accuracy, add Travis County property taxes averaging 1.7% to 2.2% of the purchase price annually, homeowner's insurance, and PMI if applicable. The combined figure is what lenders use to calculate your debt-to-income ratio, not the principal and interest figure alone.

What is the difference between a mortgage broker and a direct lender in Austin?

A mortgage broker in Austin works with multiple lenders and can shop your application across several institutions to find the best available rate for your profile. A direct lender originates and funds loans in-house. Brokers offer broader rate comparison but add a layer of processing. Direct lenders may move faster on approvals. For buyers with credit challenges, a broker with experience in subprime and near-prime mortgage products can be particularly valuable.

What are the current mortgage rates in Austin?

Mortgage rates in Austin follow national benchmarks but vary based on loan type, credit score tier, down payment size, and lender. Rates fluctuate daily. The most accurate way to determine your rate is to obtain a pre-approval from at least two to three lenders. Rate comparison within a 14-day window protects your credit score while giving you real market data.

The Bottom Line: Prepare First, Apply Second

The Austin mortgage market does not reward the fastest applicant. It rewards the most prepared one.

A buyer who spends 60 days improving their credit profile before applying may qualify for a rate that saves them $200 to $300 per month over the life of their loan. Over 30 years, that preparation is worth six figures. In the same house. In the same neighborhood. With the same down payment.

You do not need a perfect credit score to buy a home in Austin. You need the best credit profile you can build before you submit your application.

Start with a free credit review before you talk to a lender. Know your score, understand what is affecting it, and find out how much improvement is realistic in your timeframe. That conversation is the foundation of every smart Austin mortgage decision.