Bad credit car dealerships in Chicago are not hard to find. What is hard is walking into one without feeling embarrassed, anxious, or completely at the mercy of whatever number a finance manager comes back with.

Maybe you have been turned down already. Maybe you have not applied yet because you already know your score, and you are dreading the conversation. You need a car to get to work, get your kids to school, and hold your life together. But every time you get close to a solution, the credit issue gets in the way.

You are not alone in this. Chicago has one of the highest concentrations of subprime auto dealerships in the Midwest because the demand is that large. Lenders and dealers have built entire business models around buyers exactly like you.

But here is what most of those dealerships will never tell you. The way you approach this market determines whether you get a workable deal or spend the next five years paying thousands more than you should have.

This article gives you the full picture before you step into any showroom on the South Side, the West Loop, or Lincoln Park.

How Bad Credit Car Dealerships in Chicago Actually Work

Subprime Lending Is a Business, Not a Favor

Bad credit car dealerships in Chicago serve buyers with credit scores typically below 620. They make their money by connecting those buyers with subprime lenders who charge significantly higher interest rates than traditional banks and credit unions offer.

The lender takes on greater risk by approving buyers with damaged credit histories. That risk gets priced directly into your loan through elevated APR rates, larger required down payments, and stricter repayment terms.

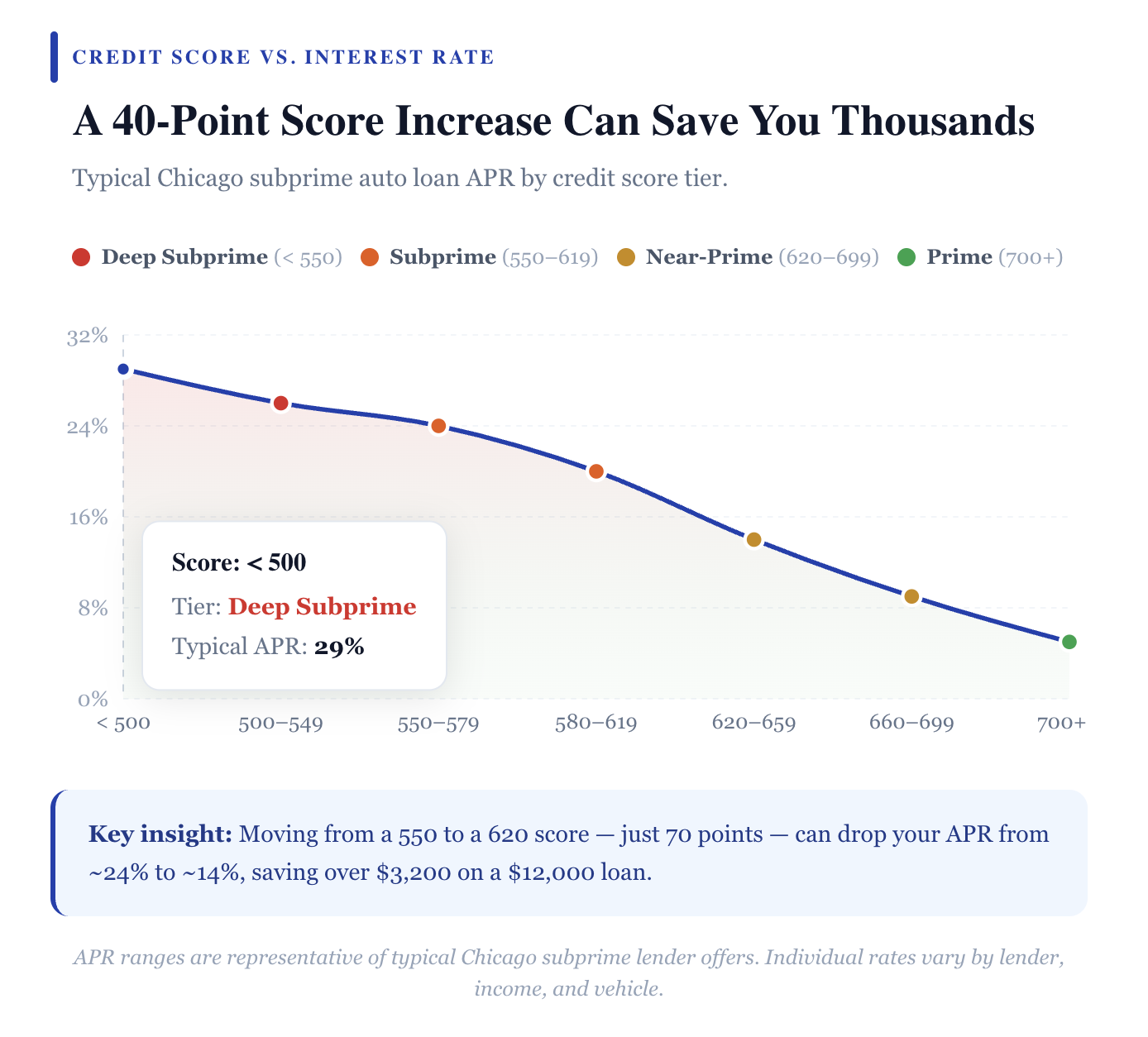

In Chicago, subprime auto loan APRs typically range from 18% to 29%, depending on your score, income, the lender, and the vehicle you are financing. Buyers with scores below 500 sometimes see rates higher than that.

How the Buy Here Pay Here Model Works

Buy here, pay here dealerships, commonly called BHPH lots, act as both the seller and the lender. You buy the vehicle from them and make your payments directly to them, often weekly or bi-weekly, sometimes in person and sometimes through an app.

Most BHPH dealers do not report your payment history to the major credit bureaus. That means even if you pay perfectly for three years, your credit score may see little to no improvement from the loan. For someone trying to rebuild, that is a significant cost that never appears on the sticker.

BHPH inventory also tends to skew toward older, higher-mileage vehicles. You may end up paying an above-market price for a car that needs repairs sooner than expected.

Larger Networks That Work With Subprime Buyers

Larger dealership networks like DriveTime specialize in subprime buyers and work with third-party lenders to structure approvals across a range of credit profiles. CarMax works with a broader credit range and may approve buyers in the low-to-mid subprime range depending on income and down payment strength.

These options tend to be more transparent than independent BHPH lots and are more likely to report your payment history to credit bureaus. Interest rates are still significantly higher than what a prime buyer receives, but the structure is more predictable.

What Chicago Dealers Look at Beyond Your Score

Used car dealerships with bad credit programs in Chicago look at more than just your three-digit number. They evaluate income stability, employment history, length of time at your current address, and the size of your down payment.

Bad credit car dealerships in Chicago with $500 down do exist, and some advertise this as the entry point. However, a larger down payment lowers your loan balance, reduces total interest paid, and in some cases moves you into a better rate tier with the lender.

Recommended Read: 10 Things You Must Know Before Getting a Car Loan

The Real Cost of Buying a Car With Bad Credit in Chicago

The Numbers Most Dealerships Do Not Show You

Here is what subprime financing actually costs on a real transaction.

You are financing a $12,000 used vehicle. At 6% APR over 60 months, your total interest paid is approximately $1,900 and your monthly payment is around $232.

Run the same loan at 24% APR, which is common for used car dealerships with bad credit in Chicago. Your monthly payment climbs to $346. Your total interest paid over 60 months is approximately $8,760.

That is nearly $7,000 in additional interest on the exact same $12,000 car. A vehicle that may already be five or six years old when you buy it.

What Illinois Law Says About Auto Lending

Illinois does not cap interest rates on most private auto loans, which means dealerships and their lending partners can legally charge rates that feel extreme. The Illinois Motor Vehicle Retail Installment Sales Act governs the structure of purchase contracts in the state, but does not limit APR on used vehicle financing arranged through dealers.

Illinois does regulate repossession. Lenders are generally required to provide written notice before repossessing a vehicle, and the state imposes a five-year statute of limitations on auto loan deficiency judgments. If your car is repossessed and sold for less than you owe, the lender has five years to pursue you for the remaining balance.

Knowing this before you sign matters.

The Real Problem With Bad Credit Car Dealerships in Chicago With $500 Down

Low down payment advertising gets buyers in the door. What it does not show is that a minimal down payment creates a larger loan balance, more interest, and higher monthly payments across the full loan term.

Some lenders require buyers with very low scores to put down 15% to 20% of the vehicle price regardless of what the advertisement says. Always confirm the actual down payment requirement before you make a trip.

How to Improve Your Approval Odds Before You Apply

Your Score Is Not Fixed

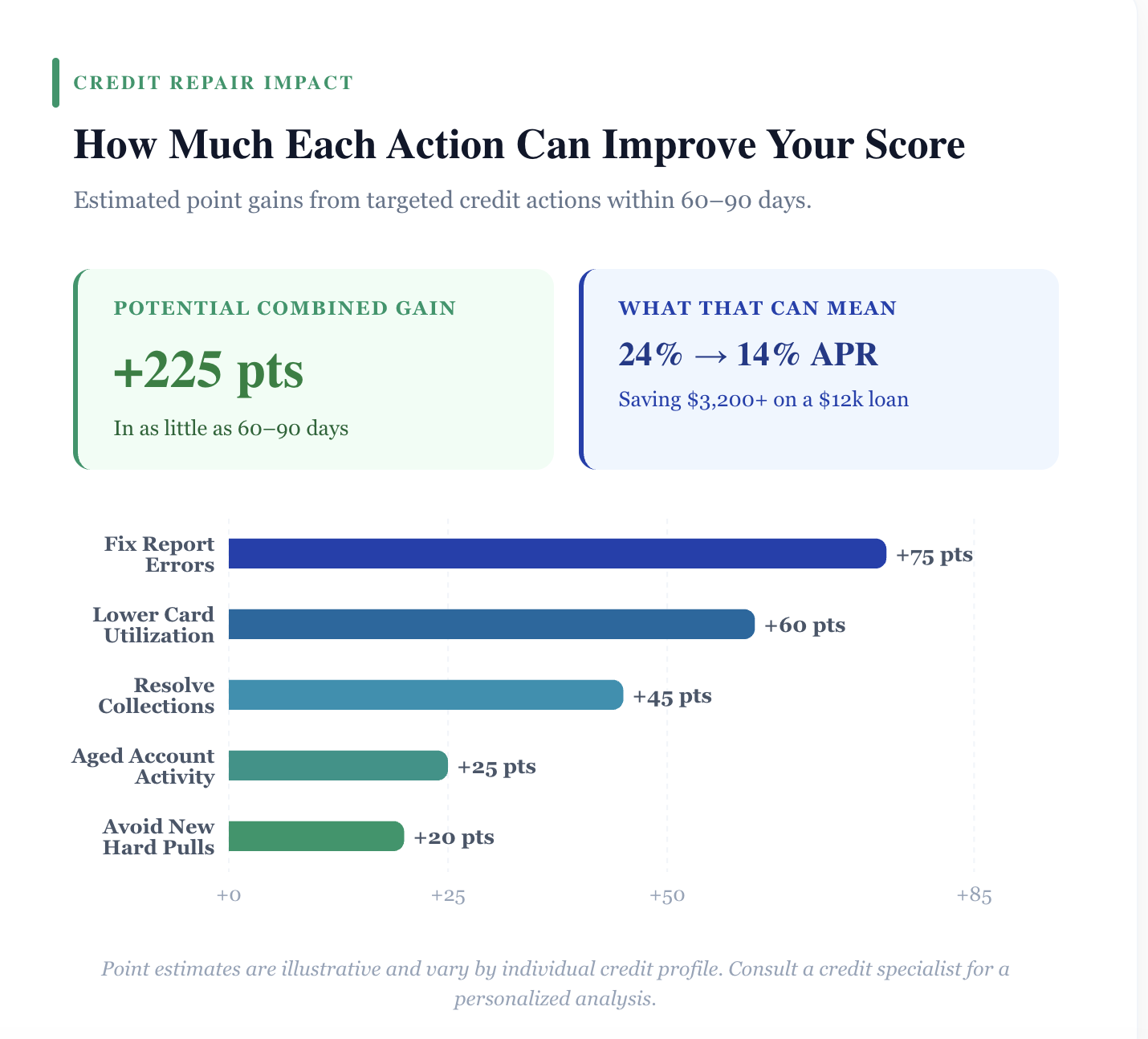

Most buyers assume their credit score is permanent. It is not. Credit scores are calculated from current data, and that data changes as you take targeted action. Many buyers can add 40 to 80 points to their score within 60 to 90 days by addressing the right issues in the right order.

That improvement can shift you from a 24% APR to a 14% APR. On a five-year loan, that gap is thousands of dollars.

Dispute Inaccurate Items on Your Report

The Fair Credit Reporting Act gives you the right to dispute any item that is inaccurate, incomplete, or unverifiable. A significant percentage of credit reports contain errors that are suppressing scores unnecessarily.

Pull your reports from all three bureaus at AnnualCreditReport.com and review every account, every late payment marker, and every collection entry. If anything is reported incorrectly, dispute it in writing with documentation. Removing inaccuracies can produce fast score improvement without paying off any debt.

Handle Collections Strategically

Not all collections affect your score equally. Newer collections carry more weight than older ones. Medical collections are now treated differently under updated FICO scoring models.

Before paying off any collection, understand exactly how it is affecting your current score. Paying a collection does not always improve your score and sometimes changes its status in ways that have no positive impact. A Chicago-based credit specialist can walk you through this before you make any payments.

Lower Your Credit Utilization

Credit utilization, the ratio of your balances to your available credit limits on revolving accounts, accounts for 30% of your FICO score. Maxed-out or near-maxed credit cards are suppressing your score every single month.

Paying balances below 30% of each card limit produces a measurable score increase within a single billing cycle. Getting below 10% on each card produces an even stronger result.

Should You Fix Your Credit Before Visiting a Chicago Dealership?

What a 40-Point Increase Actually Does for You

Even a modest credit score improvement produces real financial results for a Chicago car buyer.

A 40-point increase can move you from a deep subprime rate of 24% to a standard subprime rate around 16%. On a $12,000 loan over 60 months, that difference saves you roughly $3,200 in total interest. It can reduce the down payment requirement that some lenders impose. It can open access to financing programs that are simply unavailable below a certain score threshold.

An 80-point improvement can move you out of subprime entirely and into near-prime lending, where rates at some lenders drop into single digits.

Best Bad Credit Car Dealerships in Chicago: What to Look for Instead of Where to Go

Rather than chasing a list of the best bad credit car dealerships in Chicago, the smarter approach is to identify which lender networks align with your specific credit profile before you walk in anywhere.

Dealerships on the South Side often cater to deeper subprime buyers and price their financing accordingly. The West Loop has a wider mix of dealerships working with both franchise lenders and independent financing sources. Lincoln Park and the North Side generally serve buyers with stronger credit, though exceptions exist within every neighborhood.

Knowing which dealerships work with which lending networks, and what credit profile each network accepts, lets you target your applications strategically rather than walking in blind.

The Hidden Cost of Applying at Multiple Dealerships

Every time a dealership pulls your credit, it generates a hard inquiry. Multiple hard inquiries in a short window signal risk to lenders and reduce your score. Applying at five dealerships across one weekend can cost you 15 to 25 points before you have signed anything.

If you are looking at bad credit no credit check car dealerships in Chicago as a way to avoid this, understand the tradeoff. No-credit-check dealers typically charge higher prices, higher rates, and offer limited inventory. Those loans rarely help you rebuild credit, which means you stay in the same situation for the next loan.

Get a Free Credit Analysis Before You Step Into a Dealership

The single smartest move a Chicago car buyer with damaged credit can make right now is to understand exactly what is suppressing their score and what can realistically be fixed before applying.

A free credit analysis identifies the specific items holding your score down, gives you a realistic picture of how much improvement is possible in your timeframe, and helps you walk into any dealership from a position of knowledge rather than desperation.

Get a free credit analysis before you step into a dealership. It takes less than 20 minutes and gives you information that could save you thousands.

The Bottom Line: Apply Smarter, Not Faster

The bad credit car dealerships in Chicago will still be there in 60 days. What changes in those 60 days is your credit score, your negotiating position, and the total amount of money you spend over the full life of your loan.

Buyers who pay the most are the ones who walked in the most desperate. Buyers who pay the least are the ones who took a few weeks to understand their credit, fixed what could be fixed quickly, and showed up knowing exactly what they qualified for.

You do not have to choose between getting a car and protecting your finances. You need a plan.

Get a free credit analysis before you step into a dealership. Start there before you start shopping.

Have questions about your credit or your options as a Chicago car buyer? Leave a comment below or reach out directly for a no-obligation credit consultation.