collection call won't tell you creditor is, that is a serious red flag and possibly a federal law violation. A legitimate debt collector must give you the creditor's name either during the first call or within five days of that first contact. No exceptions.

At my credit repair company, this is one of the most common situations clients bring to us. A client once came in shaking because a caller demanded $800 and refused to name the original creditor. She almost paid. That call was a scam.

The numbers back this up. Debt collection generates more fraud reports to the Federal Trade Commission than any other industry, with consumers losing $2.95 billion to imposter scams in 2024 alone and more than 100,000 fraud claims filed in just the first quarter of 2025. Many of those cases started exactly the same way: a call with no creditor name.

What a Debt Collector Must Tell You by Law

The Fair Debt Collection Practices Act (FDCPA) sets the rules here. Any debt collector who contacts you for payment must share certain information about the debt. If collectors don't give you this information when they first contact you, then they must submit the information to you in writing within five days of the initial contact.

That required information includes:

The name of the creditor.

The amount owed.

Your right to dispute the debt in writing within 30 days.

A collector must also include your right to get information about the original creditor if you ask for it within 30 days of receiving validation information.

So if a collector calls you today and refuses to name the creditor, they are breaking federal law. Full stop.

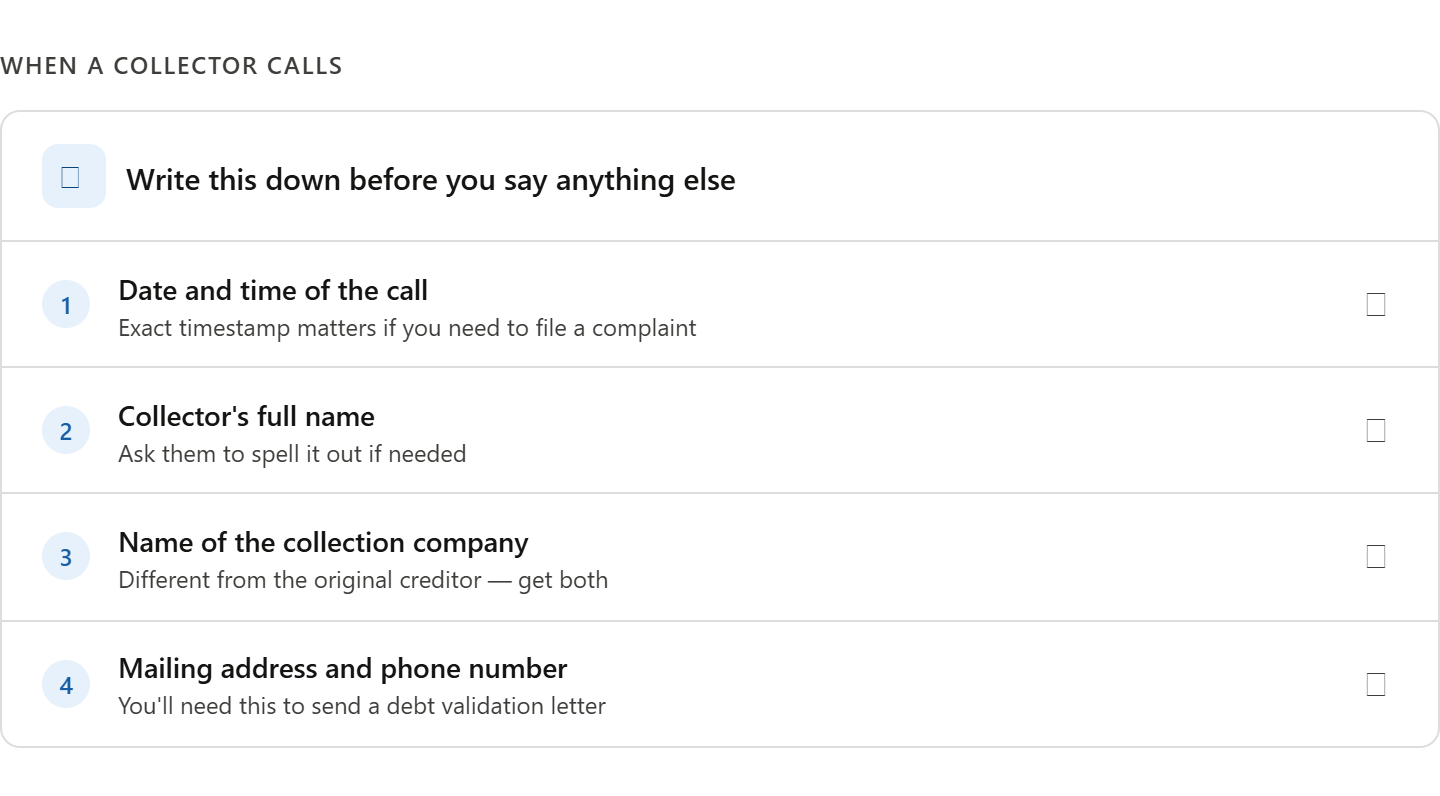

What to Do When a Debt Collector Calls You

The FTC recommends talking to the collector at least once, even if you are unsure the debt is yours. That one conversation can help you gather critical details.

Then ask the debt collector how much you owe, who you owe the money to, and what to do if you don't think you owe the money. The law says they have to tell you these things.

If they refuse to answer any of these, hang up. Do not give your Social Security number, bank account details, or any payment before you confirm the debt is real.

At our firm, in the first three months of 2025 alone, we logged 47 new cases where clients made partial payments to collectors who never named a creditor. Every one of those cases required a full dispute process to recover.

Is It a Scam? How to Tell

Refusing to name the creditor is the biggest red flag on the list. If someone calls you about a debt and doesn't identify themselves, asks for payment via wire transfer, demands personal information, or calls at odd hours, these are red flags that indicate the caller is a scammer.

Watch for these signs on any debt collection call:

They push you to pay immediately using a wire transfer or prepaid card.

They threaten arrest, license suspension, or contacting your employer.

They refuse to give you a mailing address.

They do not send a written validation notice within five days.

A legitimate debt collector should be able to provide the name of the company you originally owed without hesitation when asked. If they hesitate, deflect, or get aggressive, treat it as a scam until proven otherwise.

Can a Debt Collector Ask for a Payment?

Yes, a debt collector can ask for payment. That part is legal. But they cannot demand payment before giving you validation information, and they cannot pressure you into paying a debt you have not confirmed.

The law limits how and when a debt collector can contact you about covered debts. They cannot call before 8 a.m. or after 9 p.m. They cannot call your workplace if they know your employer prohibits it.

Asking for payment is fine. Demanding payment while hiding the creditor's name is not.

To recap: a collector can request payment, but only after you receive proper debt validation. Never pay before you see the creditor's name, the amount, and the dispute instructions in writing.

Can a Debt Collector Contact You If You Disputed the Debt?

No. Once you send a written dispute within 30 days of first contact, debt collectors are forbidden from calling, writing, or otherwise contacting a debtor if the debtor disputes or refuses to pay the debt. If the debtor requests validation of the debt, the debt collector must provide this proof before further contact is made.

Send your dispute letter by certified mail with a return receipt. Keep a copy. That paper trail protects you if they violate the rule and keep calling anyway.

What Happens If You Stop Calling a Debt Collector Back?

Ignoring the calls does not make the debt go away. If the debt collector is collecting a valid debt, avoiding or ignoring their call usually won't make them go away. They may instead find other ways to collect the money from you, including by filing a lawsuit.

Here is what can happen when you go silent:

The collector may report the debt to the three major credit bureaus.

Your credit score drops when a collection account appears on your report.

The collector can file a civil lawsuit and potentially win a judgment against you.

A court judgment may allow wage garnishment in some states.

Silence is not a strategy. Verify the debt, send a written dispute if needed, and deal with it directly.

How to Send a Debt Validation Letter

If a collector contacts you and will not name the creditor, your first move is a debt validation letter. Send it within 30 days of the first contact.

Your letter should include:

Your name and address.

A statement that you are requesting verification of the debt under the FDCPA.

A request for the name and address of the original creditor.

A request for the amount owed and how it was calculated.

The CFPB provides free sample letters at consumerfinance.gov. Use them. Once the collector receives your validation letter, they can only contact you to confirm they will stop contacting you, or to tell you a specific action, like filing a lawsuit, will be taken.

Debt Collector Refusing to Name the Creditor?

Do Not Pay Until the Debt Is Verified

If a collection call will not tell you who the creditor is, your rights may have been violated. ASAP Credit Repair can help review your credit report, identify suspicious collection accounts, and guide you through the dispute process.

Get Your Credit Report ReviewedNo pressure. No upfront payment advice. Just a clear review of what is in your report.

How to Report a Debt Collector Who Breaks the Rules

If a collector refused to name the creditor, keep every record of that interaction and file a complaint immediately.

You have three places to report:

The Consumer Financial Protection Bureau at consumerfinance.gov/complaint

The Federal Trade Commission at ReportFraud.ftc.gov

Your state attorney general's office

The CFPB fields complaints about FDCPA violations and helps consumers resolve issues with debt collectors who violate the law. Filing a complaint creates an official record and can trigger an investigation.

You may also have the right to sue the collector directly. The FDCPA allows consumers to seek up to $1,000 in statutory damages plus actual damages and attorney's fees if a collector violates the law.

Your Rights Under the FDCPA: A Quick Reference

Under the FDCPA, a collector cannot harass or abuse a debtor, using violence, threats, or obscene language. It also cannot call you repeatedly or threaten to tell the general public that you do not pay your bills.

Rights you hold on every collection call:

The right to receive the creditor's name within five days of first contact.

The right to dispute the debt within 30 days in writing.

The right to request the original creditor's name and address.

The right to send a cease-contact letter and have the collector stop reaching out.

The right to sue for damages if the collector violates the FDCPA.

Knowing these rights is your best protection. A collector who refuses to tell you the creditor's name is not just being difficult. They are breaking the law.

If you received a call from a collector who refuses to identify the creditor, do not pay a single dollar. Write down what they said, send a debt validation letter by certified mail, and file a complaint with the CFPB. If you want help reviewing your credit report for unauthorized collection accounts, a credit repair professional can walk you through every dispute step.