Most people in San Antonio think they need good credit to get a credit card.

That is the wrong way to think about it.

The real question is not whether you can get a credit card. Almost anyone can. The real question is what kind of card you qualify for right now, and what that card will cost you if you pick the wrong one.

I have seen San Antonio residents with a 490 credit score get approved for a credit card the same week they applied. I have also seen people with that same score walk out of a bank with a card that charged them a $75 annual fee, a $10 monthly maintenance fee, and a 36 percent APR. They had a card. But that card was quietly draining them.

Knowing your score and matching it to the right product makes all the difference.

Here is the full breakdown.

First: There Is No Universal Minimum Score

Let's clear this up right away.

There is no single credit score that unlocks credit cards for everyone. Every card issuer sets its own standards. A score that gets you denied at Chase might get you approved at River City Federal Credit Union in San Antonio. A score that qualifies you for a secured card at Discover might not qualify you for an unsecured card anywhere else.

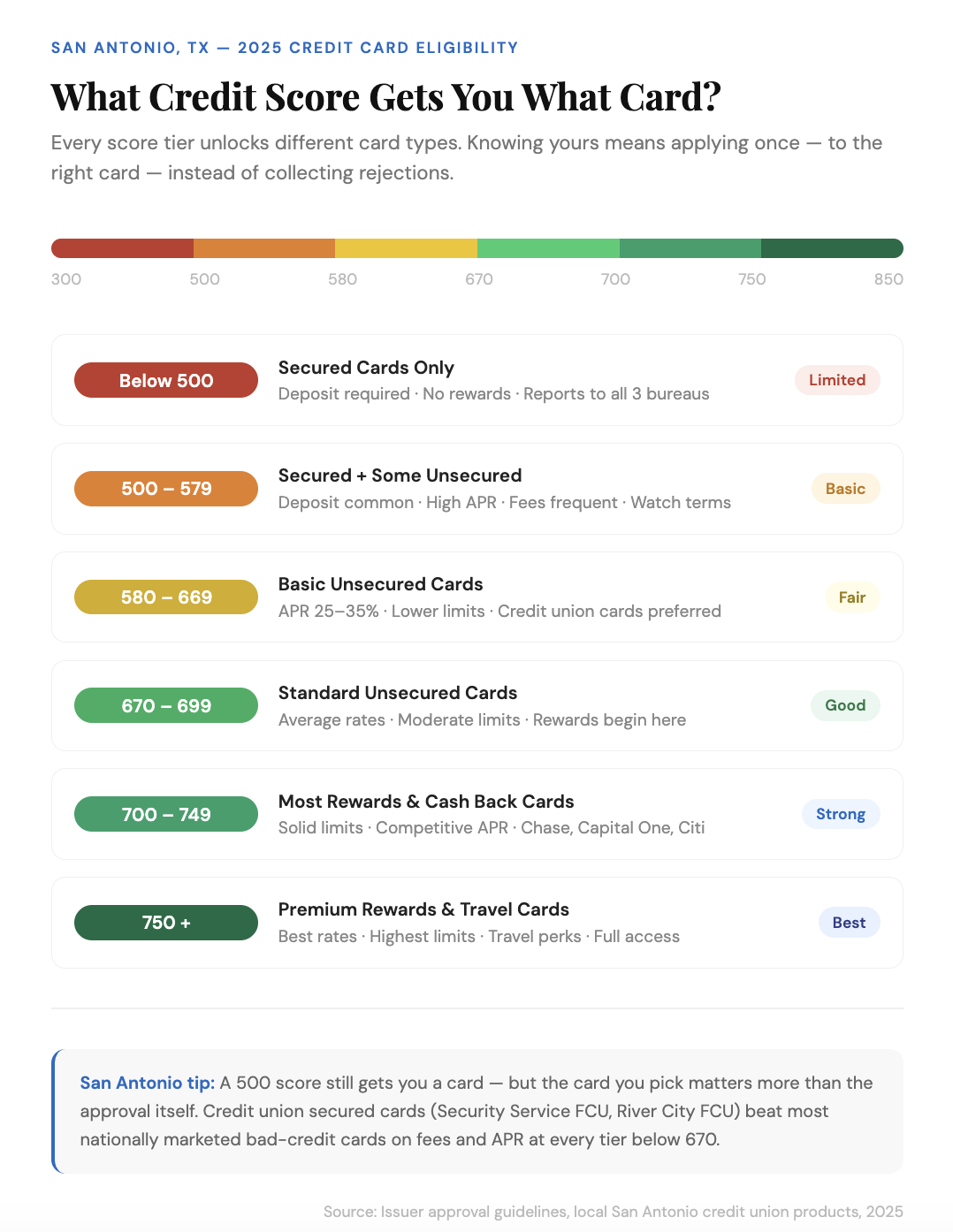

What actually matters is which tier your score falls into.

Here is how that breaks down for San Antonio residents in 2025.

Score Range | Card Type Available | What to Expect |

| 750 and above | Premium rewards cards | Low APR, high limits, travel perks |

| 700 to 749 | Most rewards and cash back cards | Good rates, solid limits |

| 670 to 699 | Standard unsecured cards | Average rates, moderate limits |

| 580 to 669 | Basic unsecured or secured cards | Higher APR, lower limits |

| 500 to 579 | Secured cards, some unsecured | Deposit required, fees common |

| Below 500 | Secured cards only | Deposit required, no rewards |

The key takeaway? Even a 500 credit score gets you a card in San Antonio.

The difference is the terms attached to it.

Recommended Read: Apartments for Rent in San Antonio With a Low Credit Score: What You Need to Know

Secured vs. Unsecured: The Distinction That Changes Everything

Here is where most people get confused.

A secured credit card requires you to put down a cash deposit. That deposit becomes your credit limit. Put down $300, and your limit is $300. The card works like a regular credit card. You spend, you pay, you build credit history. The deposit stays safe in an account and comes back to you when you upgrade or close the card.

An unsecured credit card requires no deposit. The lender extends you credit based on your score alone. No money held upfront. But they take on more risk, so they charge more for it through higher APRs and fees.

Here is the practical reality for San Antonio residents.

If your score sits below 580, a secured card is almost always the smarter starting point. You know you are getting approved. You control the limit. And the card reports to all three bureaus, which means every on-time payment builds your score, whether the card is secured or not.

If your score sits above 580, unsecured options open up. But read the terms carefully before you apply. Some unsecured cards for fair credit charge $75 to $100 in annual fees and APRs above 29 percent. In those cases, a secured card from a credit union in San Antonio often beats the fee-heavy unsecured alternative on every dimension.

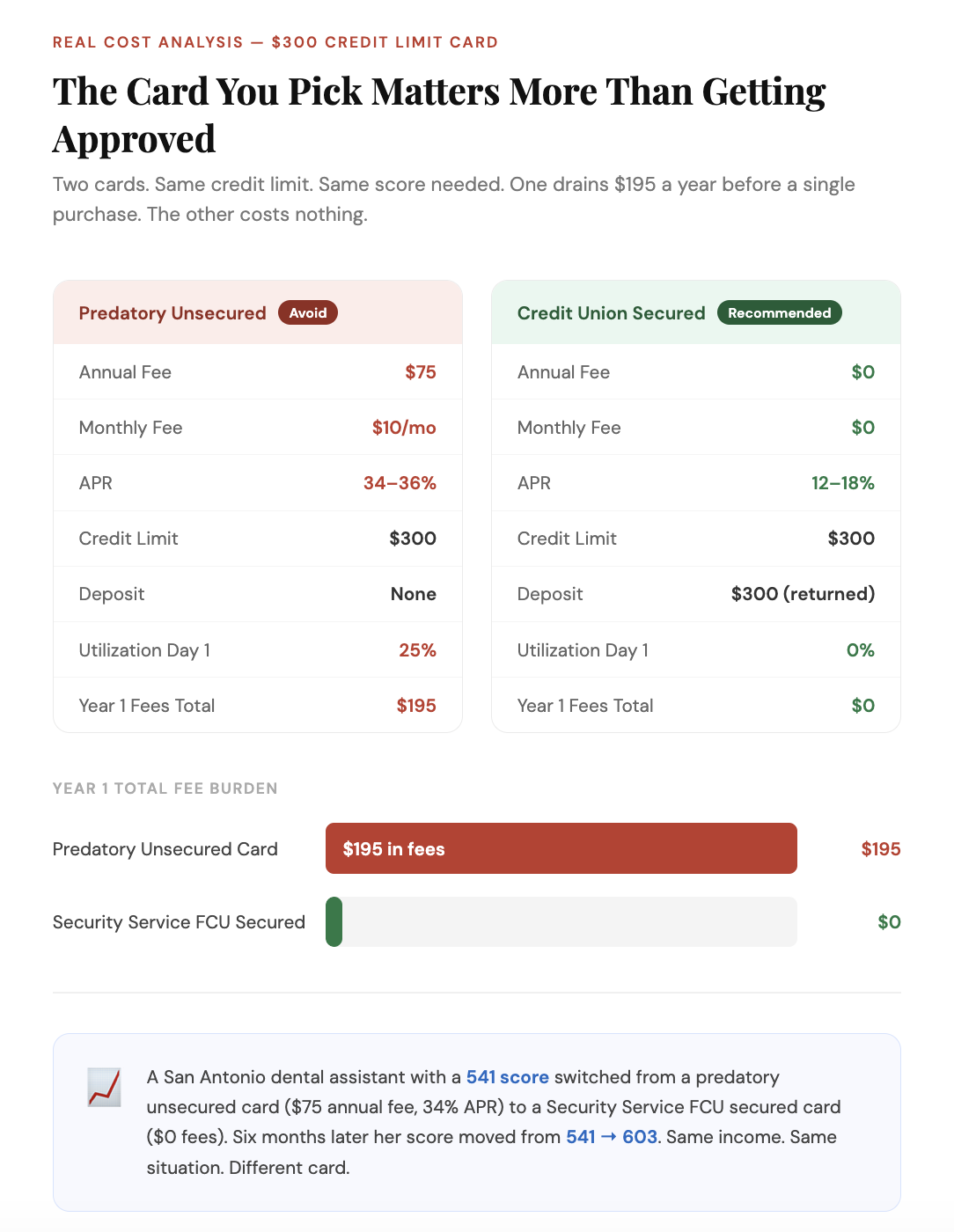

What Reyna Learned the Hard Way

Reyna worked as a dental assistant in the Medical Center area. She had a 541 credit score and no open credit accounts.

A mailer showed up in her mailbox for an unsecured card marketed to people rebuilding credit. She applied. She got approved instantly. The card came with a $300 limit, a $75 annual fee charged on day one, and a 34 percent APR.

By the time she activated the card, she already owed $75 on a $300 limit. Her utilization was 25 percent before she made a single purchase.

She called me four months later. Her score had not moved. The reason was that the card was reporting a consistent balance of $75 to $100 on a $300 limit, keeping her utilization in a range that was not helping her score climb.

We closed the card. We opened a secured card through Security Service Federal Credit Union instead. The deposit was $300, the annual fee was zero, and the APR was capped well below the predatory card she had started with.

Six months later her score had moved from 541 to 603.

Same situation. Completely different outcome. The only thing that changed was the card she chose.

The Best Credit Card Options in San Antonio by Score Tier

Now let's get specific.

If your score is below 580:

Your best first move is a secured card from a local San Antonio credit union or a major issuer with no annual fee.

Security Service Federal Credit Union offers a secured Visa card to members. The card reports to all three bureaus and has no annual fee. Membership is open to anyone who lives or works in the San Antonio area.

River City Federal Credit Union also offers a secured credit card product. Their member contact number is (210) 225-6866. For San Antonio residents starting from scratch or rebuilding after a setback, the credit union secured card route costs you less and builds you faster than most nationally marketed alternatives.

For a national option, the Discover it Secured Card requires no minimum credit score to apply, charges no annual fee, and begins automatic monthly account reviews after seven months to see if you qualify to upgrade to an unsecured card and get your deposit back.

The Capital One Platinum Secured Card approves borrowers with scores as low as 500. It requires a deposit as low as $49 for a $200 limit, depending on your credit profile.

If your score is 580 to 669:

You now have access to basic unsecured cards. But proceed carefully.

The Chase Freedom Rise is worth looking at if you have at least $250 in a Chase checking or savings account. It is one of the most rewarding cards available to borrowers new to credit or rebuilding, and it does not carry the predatory fee structure of most cards marketed to fair credit borrowers.

Greater Texas Federal Credit Union, which operates in San Antonio, offers Visa credit cards to members with fair credit. Credit union cards in this range typically charge lower APRs than national issuers offering cards to the same score tier.

If your score is 670 and above:

You qualify for most standard rewards cards. USAA, which is headquartered in San Antonio and serves the military community broadly, offers competitive Visa and rewards cards to qualifying members with good credit. If you are eligible for USAA membership, their cards are consistently among the best available to San Antonio residents at this tier.

At 700 and above, Capital One, Chase, and Citi all open up with stronger rewards, lower APRs, and higher credit limits.

The Three Mistakes San Antonio Residents Make When Applying

These mistakes come up over and over in conversations with my clients.

Mistake one: Applying to multiple cards without a strategy.

Every credit card application triggers a hard inquiry. A hard inquiry drops your score by two to five points. Apply to five cards in a single month and you have added five separate inquiries. That pattern tells lenders you are desperate for credit, and it pushes your score lower at the exact moment you are trying to use it.

Pick one card that matches your score tier. Apply to that one. Wait for the decision before applying anywhere else.

Mistake two: Choosing a card based on approval odds instead of terms.

Being approved feels like a win. But a $75 annual fee plus a $10 monthly maintenance fee on a $300 limit card costs you $195 per year before you make a single purchase. That is 65 percent of your credit limit in fees. Read the full terms before you apply. Focus on annual fee and APR before anything else.

Mistake three: Carrying a balance on a card meant for building credit.

A secured card is a building tool. It is not extra spending power. Every dollar of balance on a $300 limit card raises your utilization ratio. Keep the balance below $90, which is 30 percent of a $300 limit, and pay it in full every month. The card builds your credit. You pay zero interest. That is the entire point.

Related Content: Fix Your Credit Score in San Antonio: A Complete Local Guidec

How a Credit Card Improves Your Score in San Antonio

Here is why getting the right card matters beyond just having access to credit.

Payment history makes up 35 percent of your FICO score. Every on-time payment on a credit card goes on your record. After 12 months of on-time payments, you have built a track record that other lenders can see and trust.

Credit mix makes up 10 percent of your score. Adding a revolving credit account, which is what a credit card is, improves your mix if you only have installment accounts like a car loan or student loan.

Length of credit history makes up 15 percent of your score. Opening a card now starts that clock. The card you open today becomes your oldest card if you keep it open. That history compounds over time and works in your favor on every future application.

A secured card opened today with a $300 deposit, used once a month for a small purchase and paid in full, can move a 540 score to 620 within six to nine months. That 80-point improvement changes what loans are available to you, what rates you pay, and what apartments, car financing, and even insurance costs you face in San Antonio.

The right card is not just a card. It is the tool that opens the next door.

More Info About Applying for a Credit Card in San Antonio TX

Which credit unions in San Antonio offer credit cards for bad credit?

Security Service Federal Credit Union and River City Federal Credit Union both offer secured credit card products to members. Membership is open to San Antonio area residents. Greater Texas Federal Credit Union also serves the San Antonio area with Visa card products for members with fair credit. Credit union cards consistently carry lower APRs and fees compared to nationally marketed bad credit cards.

How long does it take to go from a secured card to an unsecured card in San Antonio?

Most credit card issuers begin automatic reviews after six to twelve months of on-time payments and responsible use. Discover begins monthly reviews at the seven-month mark. Capital One reviews accounts for upgrades periodically. Some credit unions in San Antonio upgrade members after consistent on-time performance. The fastest path is paying the full balance every month and keeping utilization below 30 percent.

Does applying for a credit card hurt my score in San Antonio?

Yes, but minimally. Each application triggers a hard inquiry that typically reduces your score by two to five points. That impact fades within a few months and disappears from score calculations after one year. The key is applying strategically. Choose one card that matches your score tier. Avoid spreading applications across multiple issuers in the same window unless you can confirm which issuers use a soft pull for pre-approval.

Should I get a credit card or a credit builder loan first?

Both build your credit, but they build different parts of it. A credit card adds revolving credit history and affects your credit utilization ratio. A credit builder loan adds installment credit history and improves your credit mix. If you can manage both responsibly, having one of each produces faster overall score improvement than either alone. If you can only manage one, start with the secured credit card because it costs less upfront than a credit builder loan requires in monthly payments.