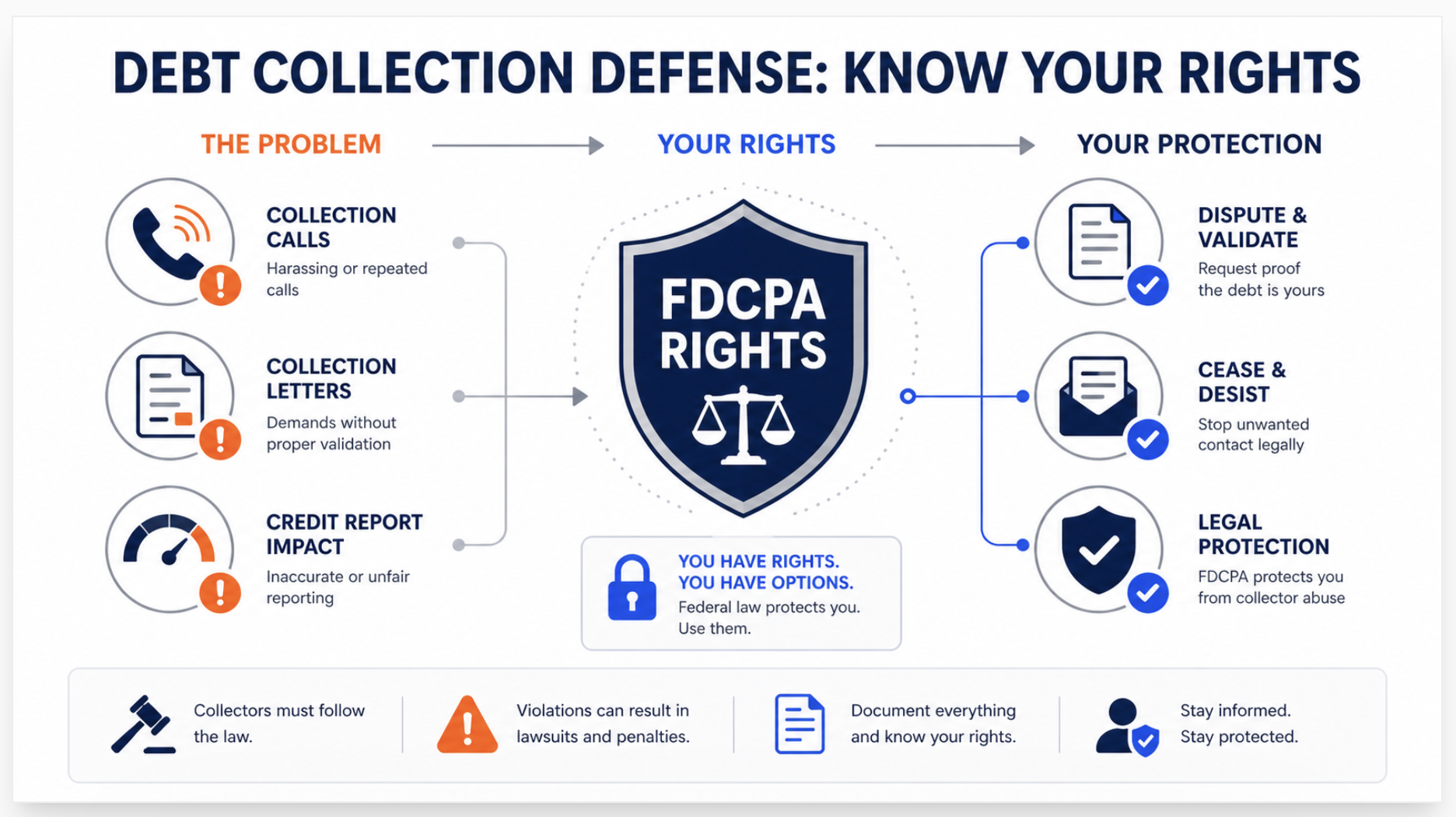

I want to share a proven debt collection defense. If a debt collector is calling you, sending you letters, or appearing on your credit report, you have more legal power than you probably realize.

The Fair Debt Collection Practices Act (FDCPA) gives you the right to stop collector contact, demand proof that a debt is yours, and dispute any errors. All in writing, without paying a lawyer.

This guide covers exactly what those rights are, how to use them, and what to do when a collector crosses the line.

What Is the FDCPA and Who Does It Protect?

The Fair Debt Collection Practices Act is a federal law passed in 1977 and enforced by the Consumer Financial Protection Bureau (CFPB). It was created specifically because debt collection abuses like harassment, threats, and deception had become widespread enough to cause serious harm to American consumers.

The FDCPA applies to third-party debt collectors. That means collection agencies, debt buyers, and attorneys who collect debts on behalf of someone else. It does not apply to original creditors collecting their own debts. Meaning if your credit card company calls you directly, the FDCPA technically does not govern that call. However, most states have their own laws that extend similar protections to original creditors.

What kinds of debts does the FDCPA cover?

The FDCPA covers personal, family, and household debts. This includes:

Credit card balances

Medical bills

Auto loans

Student loans (private)

Utility bills sent to collections

Mortgage debt

It does not cover business debts. If a collector is contacting you about a personal debt, the FDCPA almost certainly applies.

What Debt Collectors Cannot Do by Law

This is the section most people never read, and collectors count on that. The FDCPA places strict limits on when, how, and what collectors can communicate to you. Violating these rules is not just unethical. It is illegal, and it gives you grounds to sue.

Time and place restrictions

Collectors cannot call you before 8 a.m. or after 9 p.m. in your local time zone. They cannot call you at work if they know or have reason to know your employer does not allow personal calls. They cannot call you repeatedly with the intent to annoy or harass. Courts have found that multiple calls per day to the same person can constitute harassment.

Prohibited conduct are these below:

Threatening violence or harm

Using obscene or profane language

Misrepresenting who they are or how much you owe

Claiming to be attorneys or government representatives when they are not

Threatening to sue you if they have no intention of doing so

Telling you that you will be arrested for not paying a debt (debt is civil, not criminal)

Contacting third parties like your family, employer, or neighbors. Except to locate you

Written communication rules

Any written communication from a collector must include a validation notice - a statement that tells you the amount of the debt, the name of the creditor, and your right to dispute the debt within 30 days. If you do not see this in the first letter you receive, the collector may already be in violation.

How to Validate a Debt: Your Most Powerful Right

Debt validation is the single most important tool you have. Under the FDCPA, within five days of first contact, a collector must send you a written notice containing the debt amount and the original creditor's name. Within 30 days of receiving that notice, you have the right to send a written dispute requesting that the collector verify the debt.

Once you send a debt validation letter, the collector must stop all collection activity until they provide verification. If they cannot verify it - and many debt buyers cannot, because they purchase debts in bulk with incomplete records - the debt cannot be collected and should be removed from your credit report.

What happens if a collector cannot validate?

If a collector fails to respond to your validation request or if they continue collecting without verifying, they violate the FDCPA. At that point, you can file a complaint with the CFPB, sue in federal court for up to $1,000 in statutory damages plus attorney's fees, and dispute the account with the credit bureaus using the collector's non-response as evidence.

How to Stop Debt Collector Contact Legally

You have the right to tell a debt collector to stop contacting you. This is not the same as making the debt go away. The debt still exists and still affects your credit. But it does end the phone calls and letters. Here is how to do it correctly.

Send a written cease and desist letter via certified mail with a return receipt. Once they receive it, the FDCPA allows them to contact you only one more time. This is to confirm they are stopping contact or to notify you of a specific action they intend to take, such as filing a lawsuit.

When stopping contact is and is not a good idea

Stopping contact makes sense when a debt is past the statute of limitations, when a debt buyer cannot validate the debt, or when collector behavior has been abusive and you are documenting for a lawsuit. It is generally not a good idea if the debt is valid and within the collection window, because it closes off negotiation, including pay-for-delete agreements that could remove the account from your credit report.

Are debt collectors affecting your credit score?

Collection accounts can drop your score by 50 to 100 points or more - and they stay on your report for up to seven years. ASAP Credit Repair has helped over 70,000 clients dispute collections, remove errors, and rebuild their credit. Get your free credit report review and find out exactly what can be removed.

How Debt Collections Affect Your Credit Report

When a debt goes to collections, whether you know about it or not, the collection agency reports it to the three major credit bureaus: Equifax, Experian, and TransUnion. It appears as a collection account in the derogatory marks section of your credit report.

How much does a collection hurt your credit score?

The impact depends on your overall credit profile, but a single collection account can drop your score by 50 to 110 points. Newer accounts hurt more than older ones. Higher balances hurt more than lower ones. And the drop is sharpest when the collection first appears - it diminishes over time but stays on your report for seven years from the date of first delinquency with the original creditor.

Paid vs. unpaid collections: Does it matter?

Under older FICO scoring models (FICO 8 and below), paying a collection does not automatically improve your score - the account still appears as a derogatory mark. Under FICO 9 and VantageScore 3.0 and 4.0, paid collections are weighted less heavily. However, the most important thing is accurate reporting. If a collection is inaccurate, belongs to someone else, or cannot be validated by the collector, it can be disputed and removed entirely. This does improve your score.

What about medical debt?

As of 2023, the three major credit bureaus removed paid medical collections from credit reports and stopped reporting medical debts under $500. Medical debt under $500 no longer appears on consumer credit reports regardless of payment status. Unpaid medical debt over $500 still appears after a 12-month grace period.

How to Negotiate With Debt Collectors

If a debt is valid and within the statute of limitations, negotiation is often more effective than avoidance. Debt buyers typically purchase debts for a fraction of the face value - often 3 to 15 cents on the dollar. Which means they have significant room to settle for less than the full amount.

Pay-for-delete agreements

A pay-for-delete agreement is a negotiation where you agree to pay the debt in exchange for the collector removing the account from your credit report entirely. This is not guaranteed. Not all collectors will agree, and it is not explicitly sanctioned by the credit bureaus - but it works often enough that it is worth attempting before paying without conditions.

The key: always get the pay-for-delete agreement in writing before making any payment. A verbal agreement is unenforceable.

Settling for less than the full amount

Collectors will frequently accept 40 to 60 cents on the dollar to close an account, especially on older debts. If you settle, get the settlement terms in writing, confirm what the collector will report to the bureaus (settled in full vs. paid in full), and understand that forgiven debt over $600 may be reported to the IRS as income on a 1099-C form.

How to File an FDCPA Complaint

If a collector has violated your rights under the FDCPA, you have three enforcement options. You can use all three simultaneously.

File a complaint with the CFPB at consumerfinance.gov/complaint. The CFPB forwards your complaint to the collector, who is required to respond. The CFPB publishes complaints in a public database, which affects the collector's regulatory standing.

File a complaint with the Federal Trade Commission at reportfraud.ftc.gov. The FTC does not resolve individual complaints but uses them to identify patterns and build enforcement cases.

Sue the collector in federal district court or small claims court. Under the FDCPA, you can sue for actual damages, statutory damages up to $1,000, and attorney's fees and court costs. Many consumer protection attorneys take FDCPA cases on contingency. Meaning you pay nothing unless you win.

The FDCPA has a one-year statute of limitations, meaning you must file a lawsuit within one year of the violation.

Joe's Take: What 20 Years in Credit Repair Actually Teaches You About Debt Collectors

Joe Mahlow - Founder, ASAP Credit Repair

The biggest mistake I see clients make is paying a collection account without asking for anything in return. They see the balance, they panic, they pay. But the collection stays on their report for seven years regardless. Paying does not erase it under most scoring models. What actually moves the needle is the debt validation process. In my experience, a significant number of debt buyers - especially on older accounts. Genuinely cannot produce the original agreement, the full payment history, or a proper chain of ownership. When they cannot validate, that account has to come off your report. I have seen clients remove four and five accounts this way without paying a single dollar, purely because the collector could not do their paperwork. That is the conversation I wish every client had before they wrote a check.

Debt Collection Defense: Frequently Asked Questions

Can a debt collector sue me?

Yes - if the debt is valid and within the statute of limitations in your state, a collector can file a civil lawsuit. If they win a judgment, they may be able to garnish your wages or place a lien on your property. This is why ignoring collector contact entirely is risky. Responding with a debt validation letter is a better starting point than silence.

What is the statute of limitations on debt?

The statute of limitations is the period during which a collector can legally sue you to collect a debt. It varies by state (3 to 10 years) and by debt type. After the statute of limitations expires, the debt becomes 'time-barred' - a collector can still attempt to collect it, but they cannot sue you. Making a payment or acknowledging the debt in writing can restart the clock in some states.

How long does a collection account stay on my credit report?

Seven years from the date of first delinquency with the original creditor, not the date the debt was sold to a collection agency. After seven years, the account must be removed from your credit report automatically under the FCRA. If it is not, you can dispute it with the credit bureaus directly.

Can I remove a legitimate collection from my credit report?

You cannot remove accurate, verifiable collection information before the seven-year mark through standard dispute processes. However, if the collector cannot validate the debt, if the reporting contains errors (wrong balance, wrong dates, wrong creditor name), or if you negotiate a pay-for-delete agreement, removal before seven years is possible.

Do I have to respond to a debt collector?

You are not legally required to respond. However, ignoring a collector does not make the debt disappear and does not prevent a lawsuit. The most strategic first move is always a debt validation letter. It pauses collection activity, tests whether the collector can actually substantiate the debt, and creates a paper trail that protects you if the matter escalates.

Is a debt collection account hurting your credit score right now?

Collection accounts damage your score every day they stay on your report. ASAP Credit Repair has helped over 70,000 clients remove collections, dispute inaccurate items, and rebuild their credit history. Legally and permanently. We will pull your credit report, identify every negative item, and show you exactly what can be disputed.

Ready to improve your credit?

Get Started →