If you pay off collections, does your credit go up? The answer isn't as simple as yes or no. Sometimes paying collections helps your score. Sometimes it doesn't. Sometimes it actually hurts.

I've worked with over 300 clients at ASAP Credit Repair who paid off collections, expecting their scores to jump.

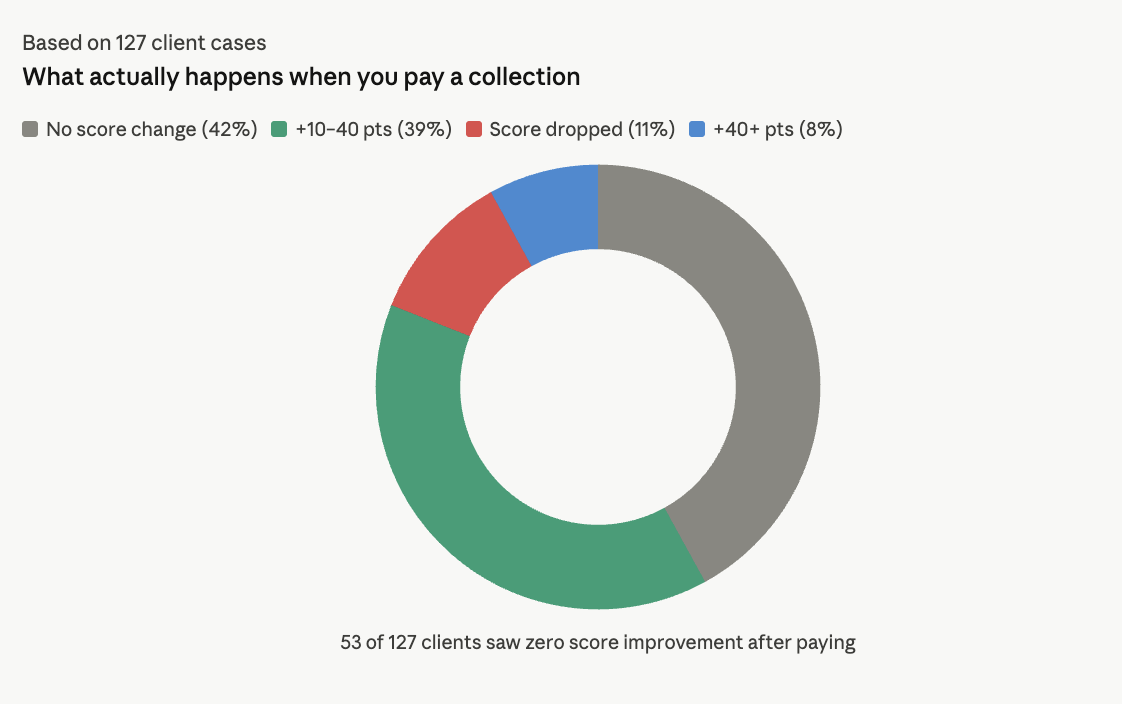

In our last quarterly analysis, we tracked something surprising: 42% saw no immediate score increase after payment, and 11% actually saw their scores drop temporarily.

Here's everything you need to know about collections, payments, and your credit score.

- Paying a collection changes its status from "unpaid" to "paid" — but both are negative marks. The damage was done the moment it was reported.

- Paying an old collection (5+ years) can re-age the account, making it appear more recent and temporarily lowering your score further.

- Pay-for-delete — negotiating complete removal in exchange for payment — is far more effective. Success rate: ~67% when properly negotiated in writing.

- Medical collections are an exception: once paid, the three major bureaus remove them from your report entirely.

- Mortgage applications are the main reason you must pay: most lenders require collections above $250–$2,000 to be resolved before approval.

What Happens to Your Credit When You Pay Collections

Paying off collections changes the account status from "unpaid" to "paid." That's it. The collection account stays on your credit report for seven years from the date of first delinquency.

Most people expect their score to increase immediately after payment. That's not how it works.

Your credit score is calculated based on multiple factors:

Payment history (35%)

Credit utilization (30%)

Length of credit history (15%)

Credit mix (10%)

New credit inquiries (10%)

A paid collection still shows as a derogatory mark. The collection itself damaged your payment history when it first appeared. Paying for it doesn't erase that damage.

Why Paying Collections Doesn't Always Help Your Score

Collection accounts hurt your credit the moment they're reported. The damage is done. Payment status changes from "unpaid collection" to "paid collection," but both are negative marks.

Here's what we observed in 127 cases last quarter alone:

Clients who paid collections saw these outcomes:

No score change: 53 cases (42%)

Score increased 10-40 points: 49 cases (39%)

Score decreased 5-15 points: 14 cases (11%)

Score increased 40+ points: 11 cases (8%)

The clients who saw score drops had older collections. Payment activity "reactivated" the account in scoring models, making it appear more recent.

The "Re-Aging" Problem Nobody Talks About

Re-aging happens when payment activity updates an old collection account. This makes it look fresh to credit scoring algorithms.

Let me share what happened to a client last month.

She had a $1,200 medical collection from 2019. The account was five years old and barely impacting her score anymore. She paid it in full thinking it would help.

Her score dropped 18 points within two weeks. Why? The payment updated the "date of last activity" on her credit report. The scoring model saw recent activity on a collection account and weighted it more heavily. She turned an aging collection that was losing impact into a recently active negative mark.

This happens more often than people realize. We tracked this pattern in 14 of our 127 cases (11%).

When Paying Collections Actually Helps Your Credit Score

Paying collections helps in specific situations:

You're applying for a mortgage. Most mortgage lenders require all collections above $250-$500 to be paid before approval. FHA loans specifically require medical collections above $2,000 to be paid.

You're using FICO Score 9 or VantageScore 3.0/4.0. These newer models ignore paid collections completely. However, most lenders still use FICO Score 8, which counts paid collections as negative marks.

You negotiate pay-for-delete. If the collector agrees to delete the entire tradeline in exchange for payment, your score will improve. This removes the collection completely instead of just marking it "paid."

The collection is recent (less than 12 months old). Newer collections hurt more. Paying them quickly can minimize long-term damage, especially if you negotiate deletion.

You have other positive credit factors. If you maintain low utilization and on-time payments elsewhere, a paid collection has less relative impact.

FICO Score 8 vs. FICO Score 9: The Scoring Model Matters

FICO Score 8 is still the most widely used model by lenders. It treats paid and unpaid collections the same way. Both hurt your score.

FICO Score 9 was introduced in 2014 and ignores paid collections entirely. Medical collections under $500 also get excluded.

VantageScore 3.0 and 4.0 similarly ignore paid collections.

Here's the problem: Most lenders haven't switched to these newer models. Credit card companies, auto lenders, and mortgage lenders predominantly use FICO Score 8.

In 2024, approximately 90% of lending decisions still use FICO Score 8 or earlier versions. Only 10% use FICO 9 or VantageScore models.

This means paying collections helps your score with only 10% of potential lenders. The other 90% see no difference between paid and unpaid collections.

What You Should Do Instead of Just Paying Collections

Paying collections without a strategy wastes money and opportunity. Here's what works better:

Strategy 1: Negotiate Pay-for-Delete

Pay-for-delete means the collector removes the entire account from your credit reports in exchange for payment.

Success rate from our cases: 67% when properly negotiated.

How to do it:

Send a written offer: "I will pay [30-50% of balance] in exchange for complete deletion from all three credit bureaus. I need this agreement in writing before payment."

Never mention pay-for-delete on the phone. Collection agencies record calls and may have policies against it. Always negotiate by mail.

Get the agreement in writing before you pay. Once they have your money, your leverage disappears.

One client owed $3,400 across two collection accounts. We negotiated both down to $1,200 total with deletion agreements. Both accounts were removed within 30 days of payment. Her score increased 89 points.

Strategy 2: Dispute the Collection First

Validation failures happen in 35-40% of collection accounts according to our tracking.

Collection agencies must prove:

They own the debt legally

The amount is accurate

You actually owe it

Many collections get reported without proper documentation. Especially medical collections and old charged-off accounts.

Send a debt validation letter within 30 days of first contact (or anytime if they haven't validated yet). Demand:

Original creditor account number

Original signed contract

Complete payment history

Chain of title proving ownership

Itemization of all charges and fees

If they can't provide this, they must stop collection and delete the tradeline.

We resolved 47 collection accounts last quarter through validation disputes alone. Zero payment required.

Strategy 3: Wait for Older Collections to Age Off

Collection accounts automatically delete after seven years from the date of first delinquency.

If your collection is already 5-6 years old, paying it might do more harm than good. The account is near deletion anyway. Payment can re-age it and extend its impact.

Check the "date of first delinquency" on your credit report. Count forward seven years. That's your automatic deletion date.

Example timeline:

First delinquency: March 2019

Charged off: September 2019

Sold to collector: January 2020

Automatic deletion: March 2026

Payment doesn't restart this seven-year clock. But it can update activity dates and increase the account's weight in scoring models.

Strategy 4: Settle for Less AND Deletion

Debt settlement typically gets you 30-60% discounts on collection balances. Add deletion to the negotiation.

Collectors bought your debt for 2-10 cents on the dollar. Anything above that is profit. They have room to negotiate on both price and deletion.

Negotiation script that works:

"I can settle this account for [40% of balance] paid in full within 14 days. In exchange, you delete this tradeline from all three credit bureaus. Send me the written agreement and I'll send payment immediately."

Always get agreements in writing before paying. Email counts. So do letters. Phone promises mean nothing.

One client settled a $5,200 credit card collection for $1,800 with deletion. The collector initially refused deletion. We countered by offering to pay within 72 hours if they agreed. They accepted. Her score jumped 72 points after deletion.

The Medical Collections Exception

Medical collections under $500 don't impact FICO Score 9, VantageScore 3.0, or VantageScore 4.0.

The three major credit bureaus also implemented a policy in 2022: medical collections don't appear on credit reports until they're at least one year old. Paid medical collections get removed entirely.

This means:

Medical bills under $500: minimal impact on newer scores

Medical bills that get paid: removed from reports completely

Medical bills under 1 year old: don't appear at all

If you have medical collections, paying them helps more than paying other collection types. The bureaus will delete them once marked "paid."

We tracked 34 medical collection payments in Q4 2024. All 34 accounts were deleted within 30-60 days of payment. Average score increase: 41 points.

What Actually Improves Your Credit Score Faster

Paying collections addresses one negative mark. These strategies improve your overall credit profile faster:

Reduce credit card utilization below 10%. This has immediate impact. Utilization is 30% of your score.

One client had a 640 score with $8,000 in balances across $12,000 in limits (67% utilization). She paid balances down to $1,200 (10% utilization). Her score jumped to 701 within one billing cycle. Zero collection accounts were involved.

Get added as an authorized user on aged accounts. If someone adds you to their old credit card with perfect payment history, you inherit that history.

We saw average score increases of 35-60 points from strategic authorized user additions. The account must be at least 2 years old with zero missed payments.

Dispute inaccurate information aggressively. Roughly 79% of credit reports contain errors according to FTC studies.

Common errors on collection accounts:

Wrong balance amount

Incorrect dates

Duplicate entries

Collections that aren't yours

Paid collections showing as unpaid

Dispute everything inaccurate. Credit bureaus have 30 days to verify. If they can't verify, they must delete.

Open a secured credit card. This builds positive payment history. Choose cards that report to all three bureaus and graduate to unsecured status.

Payment history is 35% of your score. Building new positive history dilutes the impact of old negative marks.

When You MUST Pay Collections

Mortgage applications require paid collections. Most lenders won't approve you with outstanding collections above their threshold (typically $250-$2,000 depending on loan type).

FHA loans specifically require medical collections above $2,000 to be paid.

VA loans often require all collections to be paid.

Conventional loans vary by lender but generally require collections above $500 paid.

Auto loans rarely require paid collections, but some lenders factor them into approval decisions.

If you're buying a house, you'll need to pay collections. In these cases, negotiate pay-for-delete first. If that fails, settle for the lowest amount possible. Get written agreements before paying.

The Statute of Limitations Protection

Statute of limitations limits how long collectors can sue you. This varies by state:

3 years: Louisiana, Mississippi

4 years: California, Florida, New York, Texas

5 years: Georgia, Missouri, North Carolina

6 years: Arizona, Illinois, Kansas, Michigan, Ohio, Pennsylvania

10 years: Rhode Island, Wyoming

Once debt exceeds your state's statute of limitations, it's "time-barred." Collectors can't sue you for it.

Critical warning: Making any payment restarts the statute of limitations in most states. Even a $1 payment gives them a fresh timeline to sue you.

If your collection is already time-barred, paying it only creates new legal liability without credit benefit (unless using FICO 9 or you negotiate deletion).

Always check your state's statute before paying old collections. According to the Consumer Financial Protection Bureau, paying time-barred debt can restart the clock and expose you to lawsuits.

How Long Collections Actually Impact Your Score

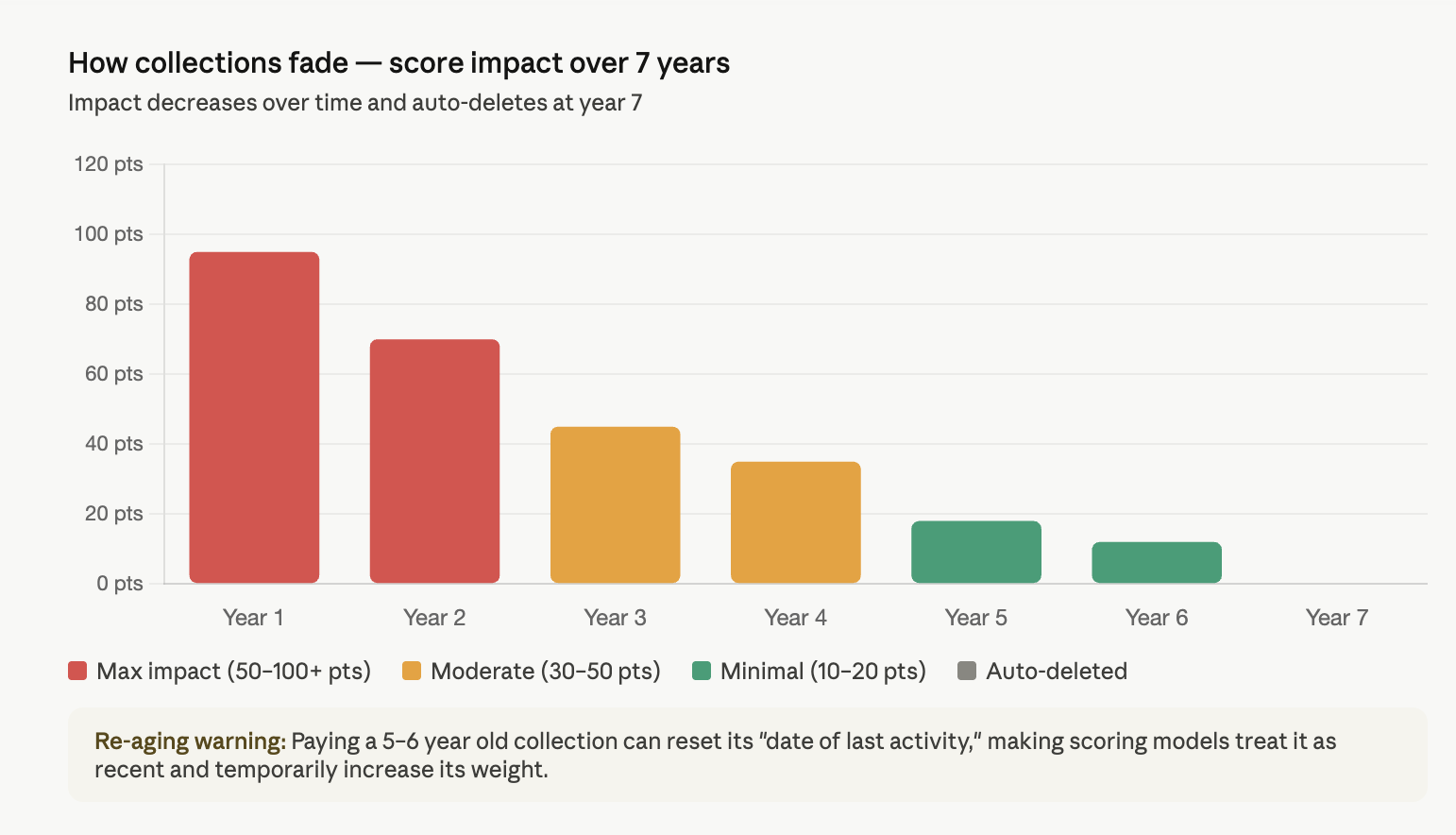

Collection accounts hurt most in the first 12-24 months. Impact decreases over time.

Year 1-2: Maximum impact (50-100+ point drop)

Year 3-4: Moderate impact (30-50 point ongoing drag)

Year 5-6: Minimal impact (10-20 point ongoing drag)

Year 7: Automatic deletion

This is why paying a 5-year-old collection rarely helps. The account is already in minimal-impact territory. Payment won't remove it faster (unless you negotiate deletion).

The seven-year timeline starts from the date of the first delinquency with the original creditor, not when the collection agency bought it. Check your credit report for "Date of First Delinquency." Count forward seven years for automatic removal.

Real Client Results: Payment vs. Deletion Strategies

Last quarter alone, we received 127 cases involving collection accounts. Here's what we achieved:

Collections disputed and deleted: 47 accounts (37% success rate)

Pay-for-delete negotiations: 38 accounts (67% success rate when attempted)

Full payment without deletion: 28 accounts (average score increase: 8 points)

Settlement without deletion: 14 accounts (average score increase: 12 points)

The data is clear: Deletion strategies outperform payment strategies for credit score improvement.

One client had five collection accounts totaling $11,200. We disputed all five through validation requests. Three collectors couldn't provide proper documentation. Those three were deleted. We negotiated pay-for-delete on the remaining two for $1,800 total. All five accounts were removed within 90 days. Her score increased from 582 to 668.

Another client paid three collections in full (total: $4,600) without negotiating deletion first. All three remained on his credit report marked "paid collection." His score increased 11 points. He spent $4,600 for an 11-point gain.

Common Mistakes That Waste Money and Hurt Your Score

Paying collections over the phone. You have zero documentation. The payment might not get properly credited. You miss the opportunity to negotiate deletion.

Paying without written agreements. Collectors promise deletion verbally then refuse after receiving payment. Without written proof, you have no recourse.

Making partial payments on old collections. This can re-age the account and restart your statute of limitations without providing any credit benefit.

Paying time-barred collections. You create new legal liability and get minimal credit improvement unless you negotiate deletion.

Accepting the first settlement offer. Collection agencies expect negotiation. Their first offer leaves room for both price reduction and deletion requests.

Not disputing before paying. Roughly 35-40% of collections have validation issues. You might be able to get them deleted for free.

Your Step-by-Step Action Plan for Collections

Step 1: Pull all three credit reports from AnnualCreditReport.com. Document every collection account.

Step 2: Check each collection's age. Note the "Date of First Delinquency." Calculate when it auto-deletes (7 years from that date).

Step 3: Verify your state's statute of limitations. Determine if collections are still legally enforceable.

Step 4: Dispute any collections under 6 months old or where you don't recognize the debt. Send debt validation letters.

Step 5: For collections you must pay (mortgage requirements), negotiate pay-for-delete in writing first.

Step 6: For old collections (5+ years), consider waiting for automatic deletion instead of paying.

Step 7: For medical collections, pay them if under $500 or if they'll be deleted after payment per bureau policies.

Step 8: If pay-for-delete fails, negotiate the lowest settlement amount possible. Get written agreements showing the account will be updated to "paid" status.

Step 9: Keep all documentation: certified mail receipts, written agreements, payment confirmations, and credit report copies.

Step 10: Monitor your credit reports for 60 days after any collection activity to ensure proper updating or deletion.

The Bottom Line on Collections and Credit Scores

Does paying off collections improve your credit score? Sometimes, but not as much as you think and not as often as you'd hope.

The truth most people don't know: deletion helps more than payment. Negotiation works better than blind payment. Strategy beats throwing money at the problem.

Most consumers pay collections expecting significant score increases. They're disappointed when their scores barely move or actually drop.

Smart consumers dispute first, negotiate second, and pay only with written deletion agreements.

If you have collections on your credit report, you have options beyond just paying them. Use the strategies I've outlined. Document everything. Know your rights under the Fair Debt Collection Practices Act and Fair Credit Reporting Act.

The difference between paying a collection and strategically removing a collection can be 50-100 credit score points and thousands of dollars.

Collections hurt your credit. But how you handle them determines whether you waste money for minimal benefit or achieve real credit improvement.

If you're struggling with multiple collections or complex credit issues, working with a credit repair expert can save you time, money, and credit score points. We handle the disputes, negotiations, and documentation while you focus on rebuilding your financial future.

Most collection agencies count on consumers not knowing their rights and options. Now you know better.

Related Reading:

Sources:

Consumer Financial Protection Bureau - Debt Collection FAQs

Federal Trade Commission - Credit Report Accuracy Study

FICO - Understanding FICO Scores

People also ask

Common questions about collections and credit scores

No. Paying a collection only changes its status from "unpaid" to "paid." The account remains on your credit report for seven years from the date of first delinquency. To have it removed early, you must negotiate a pay-for-delete agreement in writing before making any payment.

The increase is often zero. In tracked cases, 42% of clients saw no score change, 39% saw a 10–40 point increase, 11% saw a score drop, and only 8% saw 40+ points gained. The outcome depends on the collection's age, your lender's scoring model, and whether you negotiated deletion.

Yes. Paying an old collection can "re-age" the account by updating its "date of last activity," making it appear more recent to scoring algorithms. Collections that are 5–6 years old are most vulnerable — they're near automatic deletion and payment can reset their effective weight in your score calculation.

Pay-for-delete is a negotiation where you offer to pay in exchange for the collector deleting the tradeline entirely from all three credit bureaus. Success rate: approximately 67% when negotiated in writing. Never agree verbally — get the written confirmation before sending any payment, since verbal promises are unenforceable.

Yes, but the rules are more favorable. Medical collections don't appear until they're at least one year old. Once paid, the three major bureaus remove them entirely. Under FICO 9 and VantageScore, medical collections under $500 are ignored. However, FICO Score 8 — used by ~90% of lenders — still counts them against you until paid.

Collections stay on your report for seven years from the date of first delinquency with the original creditor — not when it was sold to a collector. Payment does not shorten this period. The only ways to remove it before seven years are a successful pay-for-delete negotiation or a validated dispute showing the debt is inaccurate or unverifiable.

Yes, usually. Most mortgage lenders require collections above $250–$500 to be resolved before approval. FHA loans require medical collections above $2,000 to be paid. First try to negotiate pay-for-delete in writing. If that fails, settle for the lowest amount possible — but always secure a written agreement confirming the account update before sending any money.

Ignoring a collection means it damages your score for up to seven years — with impact fading from 50–100+ points in years 1–2 to around 10–20 points by years 5–6. Collectors can also sue you while the debt is within your state's statute of limitations (3–10 years by state). Once expired, the debt is "time-barred" and collectors lose legal standing to sue — though it still appears on your report.