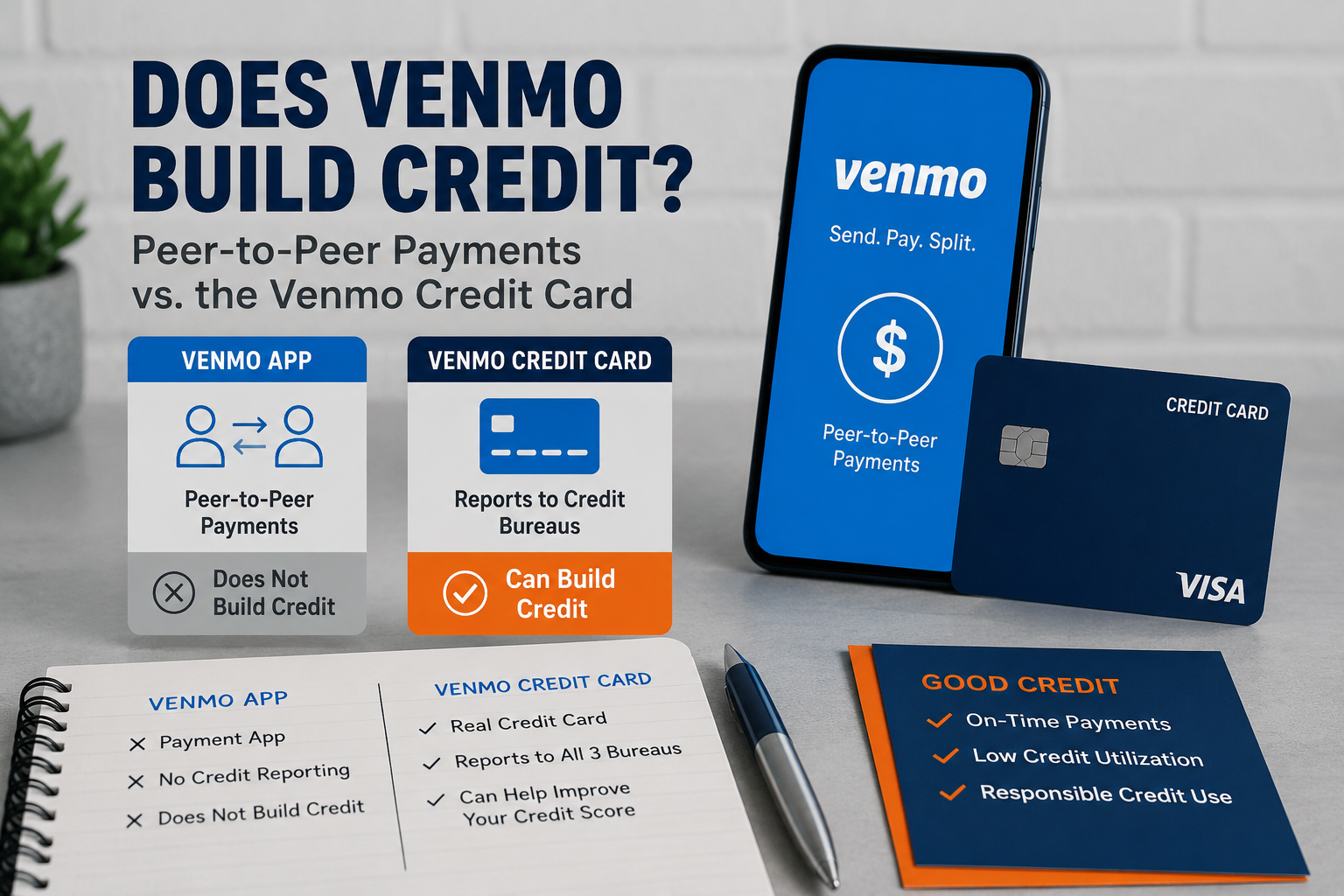

Does Venmo build credit? No. The Venmo app is a peer-to-peer payment tool. It never reports your payment activity to Equifax, Experian, or TransUnion. No matter how often you pay friends back on time, those transactions stay invisible to every major credit bureau. The only Venmo product that can build credit is the Venmo Credit Card, which is a completely different product from the app itself.

I run a credit repair company, and this question comes up more than people expect. Just last month, a client told me she had been using Venmo to pay rent and splitting every bill for two years. She thought it helped her score. It had done nothing. That story is not rare. A thread on r/personalfinance (source) echoes this constantly: users assume payment apps count, and they don't. A Quora answer on the same topic confirmed it directly: "Venmo doesn't provide debt nor report about that debt to the traditional credit rating agencies" (source).

Venmo has over 64 million monthly active U.S. accounts, according to a 2025 PayPal press release. Most of those users have no idea their payment history on the app is completely invisible to lenders.

Why Standard Venmo Payments Do Not Build Credit

Venmo classifies as a payment app, not a credit product. Credit bureaus only track formal credit accounts, such as credit cards, personal loans, auto loans, and student loans. Venmo payments move money between bank accounts or Venmo balances. No lender is involved. No credit is extended. So nothing gets reported.

Think of it this way: paying back a friend through Venmo is no different to a credit bureau than handing them cash. The transaction does not exist in the credit system.

Payment apps like Zelle, Cash App, and PayPal P2P all work the same way. None of them reports standard transfers to the three major bureaus. The payment history you build inside these apps means nothing to a mortgage lender or a landlord running a credit check.

Does the Venmo Credit Card Build Credit?

Yes. The Venmo Credit Card is a real credit card issued by Synchrony Bank on the Visa network. Synchrony reports your account activity to Experian, Equifax, and TransUnion every month, according to WalletHub (source).

Each monthly report includes your payment history, current balance, credit limit, and account status. When you pay on time, those positive marks build your credit file. When you miss a payment, that damage shows up too.

This card works like any traditional credit card. The Venmo branding is marketing. Under the hood, it follows the same credit reporting rules as any Visa card you carry in your wallet.

Does Venmo Build Credit? What Actually Affects Your Score?

Yes, in two ways.

When you apply, Synchrony Bank runs a hard inquiry on your credit report. Hard inquiries typically drop your score by a few points temporarily. Synchrony primarily pulls TransUnion, though it may use Equifax or Experian depending on risk factors, per MyBankTracker (source).

After you're approved: Your score shifts based on how you manage the card. On-time payments raise your score. High balances relative to your credit limit lower it. A missed payment hurts it fast.

Payment history makes up 35% of your FICO score. Credit utilization makes up 30%. Managing the Venmo Credit Card well can move both of those factors in a positive direction.

In our credit repair practice, we've seen clients add 40 to 60 points within six months of opening a new card and keeping utilization below 30%. The Venmo Credit Card can deliver that same result if you use it correctly.

What Credit Score Do You Need for the Venmo Credit Card?

The Venmo Credit Card requires good credit. WalletHub reports that applicants need a 700 or higher FICO score for strong approval odds (source). Synchrony may approve some applicants with scores in the 640 to 699 range, but approval at that level is not guaranteed.

If your score sits below 640, do not apply yet. A denied application still leaves a hard inquiry on your report, which costs you points with nothing to show for it.

Build your score first with a secured card or a credit builder account. Once you reach the 680 to 700 range, your odds with Synchrony improve significantly.

Does the Venmo Debit Card Build Credit?

No. The Venmo Debit Card is a Mastercard-branded debit card tied to your Venmo balance. Debit cards pull directly from your existing funds. No credit is extended, so nothing gets reported to any bureau.

Using the Venmo Debit Card is identical to using your bank debit card. It has zero effect on your credit score, positive or negative.

So, to recap on Venmo's products: the app and the debit card do nothing for credit. The credit card is the only product in Venmo's lineup that touches your credit file.

Is There a Venmo Credit Card Without the Venmo App?

No. The Venmo Credit Card requires an active Venmo account. You apply through the Venmo app or through Synchrony Bank's website, but the card stays connected to your Venmo profile. You manage payments, track spending, and redeem cash back directly inside the Venmo app.

If you do not have a Venmo account, you need to create one before applying. There is no standalone version of the card that operates outside the Venmo ecosystem.

How Do You Use the Venmo Credit Card?

The Venmo Credit Card works like any Visa card. You use it anywhere Visa is accepted, online or in-store. Here is how it works in practice:

Spend on the card across any of the eight eligible categories: groceries, dining, gas, travel, entertainment, transportation, health and beauty, and bills and utilities.

The app tracks your spending each month and identifies your top two categories automatically.

You earn 3% cash back on your top category, 2% on the second, and 1% on all other purchases. Categories rotate monthly based on where you actually spend.

Your cash back lands in your Venmo balance. From there, you can apply it as a statement credit, send it to friends, or transfer it to your bank.

Pay your statement balance through the Venmo app by the due date each month.

The card requires no category enrollment or manual tracking. The rewards system adjusts itself based on your spending behavior.

Does the Venmo Credit Card Have an Annual Fee?

No. The Venmo Credit Card carries no annual fee. NerdWallet confirms the fee structure: $0 annual fee, $0 foreign transaction fee (source).

The current APR range is 19.49% to 31.49% variable, depending on your creditworthiness. Carrying a balance month to month costs you in interest, which cancels out the cash back rewards quickly. Paying in full each month is the only way to get real value from the card.

How the Venmo Credit Card Compares to Other Credit-Building Cards

The Venmo Credit Card is not a credit-building card by design. It targets people with established credit who want cash back rewards. The no-annual-fee structure and automated reward categories make it competitive against cards like the Citi Double Cash and the Chase Freedom Unlimited.

For someone building credit from scratch, the Venmo card is the wrong starting point. Secured cards and credit builder accounts exist specifically for that purpose. They accept thin files, report to all three bureaus, and give you a track record before you apply for a card like Venmo's.

Last year alone, a significant portion of the cases we handled at our credit repair company involved people who applied for rewards cards too early, collected hard inquiries, and came to us after repeated denials. Sequencing matters. Build first, then reward.

Other Payment Apps and Credit: The Full Picture

Venmo is not an outlier. Cash App, Zelle, PayPal standard transfers, and Apple Pay do not report to credit bureaus. PayPal Credit, which is a buy-now-pay-later credit line, does report. Apple Card, Google Pay credit products, and store-branded cards through fintech platforms are also reported. The rule is simple: if a product extends credit and a bank or lender issues it, it reports. If a product just moves your own money, it does not.

Not Sure If Venmo Is Helping Your Credit?

Venmo payments do not build credit, but the right credit strategy can. If your score is holding you back from better cards, loans, or approvals, start by reviewing what is really affecting your report.

Check Your Credit Report TodayNo pressure. Just a simple first step toward understanding your credit.

What Actually Builds Credit in 2026

Credit builds through four main paths.

Credit cards with on-time payments and low utilization. Even a secured card with a $200 limit works.

Credit builder loans, where a lender holds the funds and you pay monthly installments reported to the bureaus.

Becoming an authorized user on someone else's card with a long, clean history.

Reporting rent and utility payments through third-party services like Experian Boost or RentTrack, which add non-traditional data to your file.

Venmo P2P payments fit none of these categories. The Venmo Credit Card fits the first one, but only if you qualify and manage it properly.

If you use Venmo daily and want to turn that habit into credit progress, apply for the Venmo Credit Card when your score crosses 700. Before that point, use a secured card for purchases and pay it in full every month. That combination builds the file you need to qualify for rewards cards like Venmo's.