Applying for your first credit card or choosing a new one requires understanding how credit cards actually work. Most people focus only on reward rates and annual fees while missing fundamental mechanics that affect approval odds and long-term costs.

According to a CNBC report and Federal Reserve data, Americans made over 171 billion credit card transactions in the past year, yet many cardholders don't understand basic credit card operations. This knowledge gap leads to declined applications, unnecessary fees, and missed opportunities for better card matches.

Understanding credit card history, numbering systems, expiration dates, and industry structures helps you make smarter application decisions. These insights reveal why certain practices exist and how to navigate the credit system more strategically for better approval rates and card selection.

Looking for the right credit card?

Understanding how they work is the first step.

After learning these essential facts, you'll be better equipped to compare cards, avoid common mistakes, and choose options that match your credit profile and spending habits.

Do Credit Card Expiration Dates Actually Matter?

Every credit card displays an expiration date on the front. But this date doesn't work the way most people assume.

Your credit card doesn't actually expire on that date. The plastic doesn't stop working. The magnetic stripe doesn't deactivate. The chip doesn't shut down at midnight on the expiration month.

Why Expiration Dates Exist

Credit card expiration dates serve two specific purposes unrelated to the card "expiring."

Purpose 1: Physical card replacement timing.

Credit cards wear out from daily use. The magnetic stripe degrades. Numbers fade. Plastic cracks or warps. The expiration date gives issuers a timeframe to send replacement cards before your current one becomes physically unusable.

Most issuers mail replacement cards 30 to 60 days before the expiration date. This ensures you never experience a gap in card availability.

Purpose 2: Security verification for card-not-present transactions.

When making online purchases or phone orders, merchants can't physically see your card. The expiration date provides one verification layer confirming you possess the physical card.

Someone who stole just your card number probably won't know the expiration date. This creates a basic security barrier, though it's weak by modern standards compared to CVV codes and two-factor authentication.

What This Means for Card Applications

When applying for new credit cards, understand that:

- Replacement cards maintain your existing account and credit history

- Your credit limit and APR remain unchanged with replacement cards

- Expiration doesn't trigger credit report inquiries or affect your score

- You can request early replacement if your card is damaged

Pro tip: If you're applying for a new credit card and your current card expires soon, apply before the expiration date. Some issuers view account age from the card issue date, and a replacement technically creates a new issue date even though it's the same account.

How Many Credit Cards Should You Have?

The credit card market is massive. As of 2017, over 1.65 billion credit cards existed globally just from three major networks. Visa accounted for 827 million cards. Mastercard had 718 million. American Express contributed 109 million.

That number has grown substantially since 2017, likely exceeding 2 billion cards worldwide by this year and beyond.

Optimal Number of Credit Cards for Your Credit Score

Credit scoring models like FICO and VantageScore consider your total number of accounts when calculating scores. But there's no perfect number that maximizes your score.

According to Experian data:

- People with FICO scores above 800 average 7 credit cards

- Those with scores in the 700s average 4-5 cards

- Consumers with scores below 600 often have 1-2 cards

Why multiple cards can help your score:

Lower credit utilization ratio. If you have three cards with $5,000 limits each, your total available credit is $15,000. Spending $3,000 monthly creates 20% utilization. With only one $5,000-limit card, that same $3,000 spending creates 60% utilization, which hurts your score.

Diversified credit mix. Credit scoring models reward account variety. Having multiple credit cards plus installment loans shows you can manage different credit types.

Extended average account age. More cards mean more accounts aging simultaneously. This extends your credit history length faster than having just one card.

Best Practices for Multiple Cards

Start with 2-3 cards if you're building credit. This provides utilization benefits without overwhelming complexity.

Space applications 3-6 months apart. Multiple applications in short periods trigger hard inquiries that temporarily lower scores.

Keep old cards open even if unused. Closing accounts reduces available credit and potentially shortens credit history.

Focus on cards matching your spending. Having seven cards doesn't help if they're all the wrong type for your purchases.

What Your Credit Card Number Reveals About Your Account

Credit card numbers aren't random. The digits follow a specific system identifying crucial information about your card and issuer.

Understanding this system helps you spot fake cards, identify card types instantly, and understand payment processing.

The Major Industry Identifier (First Digit)

The first digit on your credit card is called the Major Industry Identifier (MII). It instantly reveals the card issuer's industry.

Cards starting with 1 or 2: Airline companies. These are airline-branded cards or cards issued by airline financial divisions.

Cards starting with 3: Travel and entertainment. All American Express cards start with 3. All Diners Club cards start with 3.

Cards starting with 4 or 5: Banking and financial institutions. Cards starting with 4 are Visa. Cards starting with 5 are Mastercard. These represent the vast majority of credit cards since banks issue most consumer credit.

Cards starting with 6: Merchandising and banking. Discover cards start with 6. Many store credit cards start with 6.

Cards starting with 7: Petroleum companies. Gas credit cards typically use this identifier.

Cards starting with 8: Telecommunications companies.

Cards starting with 9: Reserved for national assignments and government purposes.

Why This Matters for Applications

When applying for credit cards, knowing issuer types helps:

Visa and Mastercard aren't card issuers. They're payment networks. Banks like Chase, Citi, and Capital One issue Visa and Mastercard-branded cards. When you apply for a "Visa card," you're actually applying to a bank that uses the Visa network.

American Express issues its own cards. Amex is both the network and the issuer. Your application goes directly to American Express, not through a bank.

Store cards often come from banks. That Target credit card or Amazon card? Issued by banks like Synchrony or TD Bank. The retailer is just the brand partner.

Different issuers have different approval criteria. Chase typically requires good credit (670+). Capital One approves wider credit ranges. Knowing who actually issues the card helps you target appropriate applications.

The Rest of Your Card Number

After the first digit, the structure continues systematically:

Digits 2-6: Bank Identification Number (BIN) or Issuer Identification Number (IIN). These five digits identify the specific financial institution that issued your card.

Digits 7-15: Your unique account identifier. These digits are specific to your account.

Final digit: A checksum calculated using the Luhn algorithm. This validates the entire card number mathematically. Payment systems use this to instantly spot typos or fake numbers.

This systematic structure enables the payment network to instantly identify cards and route transactions to the correct processor during the authorization split-second.

Good Read: Discovering Soft Credit Checks: Your Guide to Credit Check Basics

How Credit Cards Evolved: History That Affects Your Applications Today

Understanding credit card history reveals why certain application practices exist and how approval criteria developed.

The First Universal Credit Card (1950)

Frank McNamara founded the Diners Club Card in 1950 after forgetting his wallet at a business dinner. He realized how useful a card accepted at multiple locations would be.

Diners Club launched with just 28 New York restaurants and two hotels accepting the card. Within one year, membership hit 10,000 cardholders among New York's business elite.

The card was made of cardboard. No magnetic stripes. No chips. Merchants manually recorded transactions. The entire system ran on paper and trust.

Why this matters for applications today: The trust-based system still underlies modern credit. Issuers approve applications based on predicted trustworthiness measured through credit scores, income verification, and history. The fundamentals haven't changed despite technological advances.

The First Mass Credit Card Distribution Disaster (1958-1959)

Bank of America employee Joseph P. Williams had an idea that sounds insane today. He mailed 60,000 actual working credit cards with $300 pre-approved limits to random people in Fresno, California.

These weren't applications. They were real functioning cards made of paper. Recipients opened their mail and suddenly had credit whether they wanted it or not.

Williams called this the "Fresno Drop" and distributed 2 million cards across California by October 1959.

The results were catastrophic. Twenty percent of accounts became delinquent. Bank of America lost $8.8 million (equivalent to $80+ million today). Williams lost his job.

Congress made unsolicited credit card mailings illegal in 1970. However, mailing pre-approved applications remains completely legal.

Why this matters for applications today:

Pre-approved offers in your mailbox descend from this disaster. The difference is you must opt in by completing the application rather than receiving an active card.

The 20% delinquency rate shaped modern approval criteria. Issuers learned they couldn't give credit to random people and hope for repayment. This led to the development of credit scoring, income verification, and the entire approval infrastructure that exists today.

Delinquency risk still dominates issuer decisions. Every application gets evaluated for likelihood of repayment. This is why credit scores matter so much and why issuers decline applications from people they consider risky.

Must Read: How Ignoring a Credit Card Lawsuit Can Wreck Your Finances

Why Sears Credit Cards Matter

Sears created the first retail store credit card in 1911. Customers could charge purchases and pay later instead of needing cash.

This wasn't a modern credit card, but it established buy-now-pay-later credit extended by retailers. The Sears card operated for 92 years until Citigroup purchased it in 2003.

Sears also launched the Discover Card during the 1986 Super Bowl, one year before American Express entered the credit card market. At that time Visa and Mastercard completely dominated. Discover became the fourth major U.S. credit card network.

Why this matters for applications today:

Store cards often have easier approval. Retail credit cards typically accept lower credit scores than bank-issued cards. They use approval as a customer acquisition tool rather than a primary profit center.

Store cards can help build credit. If you're rebuilding credit or starting out, store cards might approve you when bank cards won't. Responsible use builds history that qualifies you for better cards later.

Network matters for acceptance. Cards on major networks (Visa, Mastercard, Discover, Amex) work almost everywhere. Store cards often only work at that retailer, limiting usefulness.

Choosing the Right Credit Card Based on How They Actually Work

Understanding credit card mechanics leads to smarter application decisions and better card matches.

Match Cards to Your Credit Score Range

Excellent Credit (750+):

- Premium rewards cards with best earning rates

- Cards with high annual fees but valuable perks

- 0% intro APR offers with longest periods

- Best approval odds for any card

Good Credit (670-749):

- Most rewards cards with decent rates

- Many 0% intro APR offers

- Mid-tier travel cards

- Solid approval odds for mainstream cards

Fair Credit (580-669):

- Secured cards that build credit

- Starter rewards cards with modest benefits

- Cards specifically marketed to fair credit

- Lower approval odds for premium cards

Poor/Building Credit (Below 580):

- Secured cards requiring deposits

- Credit-builder loans

- Authorized user positions on others' accounts

- Focus on building history before applying

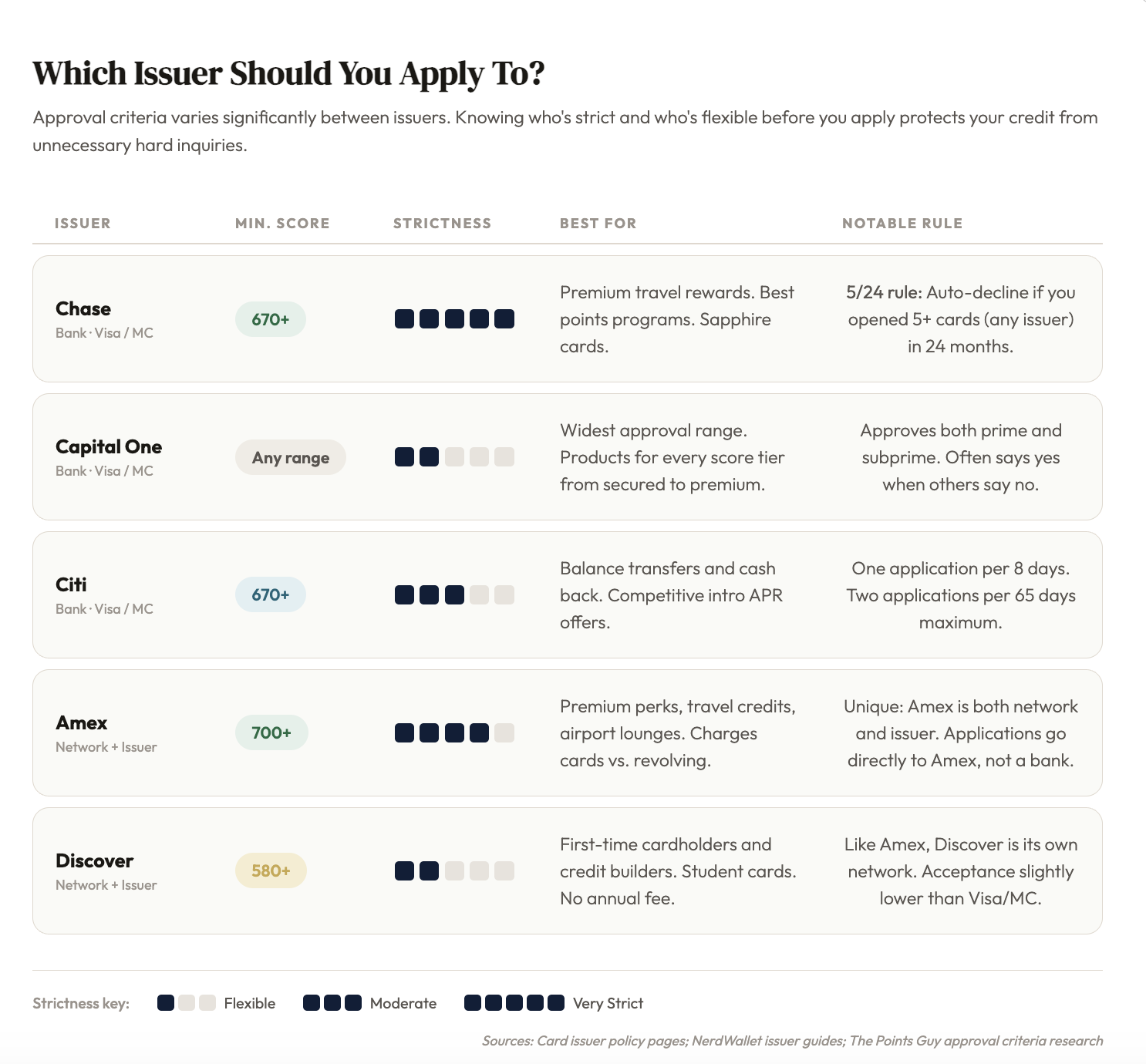

Consider the Actual Card Issuer

Chase: Strict approval criteria. Generally requires 670+ scores. Known for the "5/24 rule" (automatic decline if you opened 5+ cards across all issuers in past 24 months). Strong rewards programs.

Capital One: More flexible approval across credit ranges. Offers both prime and subprime products. Often approves applicants other banks decline.

Citi: Moderate approval criteria. Good for people with solid credit looking for specific rewards categories or balance transfer options.

American Express: Mixed approval difficulty. Some cards require excellent credit. Others approve fair credit. Unique perks and merchant acceptance slightly lower than Visa/Mastercard.

Discover: Moderate approval standards. Often approves customers building credit. Good for first-time cardholders. Acceptance improving but still lags Visa/Mastercard.

Avoid Common Application Mistakes

Applying for too many cards too quickly. Each application triggers a hard inquiry dropping your score 5-10 points temporarily. Multiple applications signal financial stress to issuers.

Ignoring spending patterns. A travel rewards card doesn't help if you never travel. A gas card doesn't help if you take public transit. Match cards to actual spending.

Focusing only on rewards without considering approval odds. Applying for cards you won't qualify for wastes hard inquiries and delays your actual card acquisition.

Not checking pre-qualification first. Many issuers offer pre-qualification tools using soft pulls that don't affect credit. Use these before applying to gauge approval odds.

Closing old cards to make room for new ones. This hurts your credit utilization ratio and average account age. Keep old cards open unless they have problematic annual fees.

Recommended Content: How to Pay Off Credit Card Debt Fast (On Low Income)

Frequently Asked Questions About How Credit Cards Work

Can I use my credit card after the expiration date?

Technically yes for in-person chip transactions, but you shouldn't. While the card physically still works, the payment network expects an updated card after expiration. Continuing to use an expired card may trigger fraud alerts, confuse merchants, and cause declined transactions. Issuers mail replacement cards 30-60 days before expiration specifically so you never need to use an expired card.

How many credit cards should I have to maximize my credit score?

There's no magic number. People with excellent credit (800+) average 7 cards, but having seven cards doesn't guarantee a high score. Focus on keeping utilization under 30% across all cards, making on-time payments, and maintaining cards long-term. Two to three cards usually provide sufficient benefits without excessive complexity.

Does applying for multiple credit cards hurt my credit score?

Yes, but the impact is usually temporary and modest. Each application creates a hard inquiry that drops scores 5-10 points. The impact fades within months and disappears entirely after 12 months. However, many applications in short periods signal financial stress and may cause issuers to decline you. Space applications 3-6 months apart.

What credit score do I need to get approved for a credit card?

This varies by card and issuer. Premium rewards cards typically require 750+ scores. Most mainstream rewards cards accept 670+ (good credit). Starter cards approve 580-669 (fair credit). Secured cards approve almost anyone, including those building or rebuilding credit. Check issuer pre-qualification tools before applying.

Are pre-approved credit card offers guaranteed approval?

No. Pre-approved offers mean you passed initial screening, but you still must submit a full application. The issuer verifies information and checks current credit before final approval. You can still be declined if circumstances changed since the pre-screening or if you don't meet all criteria.

Should I close credit cards I'm not using?

Usually no. Closing cards reduces your total available credit, potentially increasing utilization ratios. It also may lower your average account age if you close old cards. Keep cards open unless they have annual fees you can't justify or the credit limit is needed elsewhere. Use them occasionally to keep them active.

Next Steps: Choosing Your Credit Card

Understanding how credit cards work provides the foundation for smart application decisions. The next step is matching cards to your specific credit profile and spending habits.

If you have excellent credit (750+): Compare premium rewards cards based on your top spending categories. Consider annual fees against earning potential. Look for sign-up bonuses that justify the application.

If you have good credit (670-749): Focus on no-annual-fee rewards cards matching your spending patterns. Compare 0% intro APR offers if you're carrying balances or planning large purchases.

If you're building credit (below 670): Start with secured cards or cards specifically marketing to your credit range. Avoid applying for cards with approval criteria above your score. Consider authorized user positions on family members' accounts.

Use pre-qualification tools on issuer websites. These soft pulls don't affect credit and show whether you're likely to be approved before formally applying.

Compare cards strategically using comparison tools focusing on rewards rates, fees, APRs, and benefits that match how you actually use credit cards.

Credit cards remain one of the most widely used financial products despite their complex history and mechanics. Understanding how they truly work transforms you from a passive cardholder into an informed consumer making strategic credit decisions.