NCB Management Services: Your Rights & How To Handle Them

by Joe Mahlow • Updated on Jul. 10, 2026

Summary: Dealing with NCB Management Services

NCB buys and collects debts, but you have rights. Here’s how to protect yourself.

Request debt validation: Ask for proof the debt is yours and accurate.

Dispute mistakes: Challenge wrong amounts, dates, or accounts with the bureaus.

Stop harassment: You can limit calls and demand written contact.

Negotiate smart: Settle or set up payments you can afford—always get it in writing first.

Stay calm, document everything, and confirm details before making payments.

If NCB Management Services has been calling or sending letters, that’s a tough spot. But, you don’t have to panic. This debt collector reaches thousands of people every day, but most consumers aren’t clear on their rights.

In this guide, I’ll break down who NCB Management Services really is, why they’re reaching out, and exactly what you can do to protect yourself and your credit.

What Is NCB Management Services?

NCB Management Services, Inc. is a national debt buyer and collection agency. NCB has been buying and collecting consumer debt on a large-scale and national basis for nearly 20 years and is associated with some of the largest banking brands. NCB was founded in 1994 by current Chairman Brett Silver.

NCB Management Services operates as both a third-party debt collector and a debt buyer. This means they either collect debts on behalf of original creditors or purchase old debts for pennies on the dollar and then attempt to collect the full amount from consumers.

The company is headquartered in Trevose, Pennsylvania, and holds various state licenses to operate as a debt collection agency. This agency is licensed as NMLS number: 209072. They're registered with the Better Business Bureau and are members of industry associations like RMAi (Receivables Management Association International).

Debt Collection Agency vs. Debt Buyer

Know who you’re dealing with so you can choose the best next step.

Debt Collection Agency

Hired by the original creditor to collect. The original creditor still owns the debt.

Who owns the debt: Original creditor

Your leverage: Request validation; negotiate fees and late marks

Credit reporting: Usually reports under the original account

Best moves: Validate, dispute errors, get payment terms in writing

Debt Buyer

Purchases debts for pennies on the dollar and tries to collect as the new owner.

Who owns the debt: The buyer now owns it

Your leverage: Demand full chain-of-title & accurate documentation

Credit reporting: May add a separate collection tradeline

Best moves: Validate, negotiate lower settlement, remove tradeline if possible

Ownership Matters: Who owns the debt decides what documents they must show.

Validation First: Always request debt validation before paying.

Credit Impact: Collections can appear differently on your report—dispute inaccuracies.

Negotiate Smart: Get all terms in writing; push for pay-for-delete when possible.

Not sure which one you’re dealing with? Get tailored next steps in minutes.

Yes, NCB Management Services Inc is a legitimate debt collection agency. However, being legitimate doesn't mean they always operate within the bounds of consumer protection laws.

They're subject to federal regulations like the Fair Debt Collection Practices Act (FDCPA) and must follow state-specific collection laws.

NCB Management Services collects debts from various sources:

Original Creditors:

Major credit card companies

Banks and financial institutions

Medical providers

Utility companies

Telecommunications companies

Purchased Debt Portfolios:

NCB frequently purchases old debt portfolios from original creditors. When a creditor writes off a debt as uncollectable, they often sell these accounts to companies like NCB for a fraction of the original balance. NCB then attempts to collect the full amount from consumers.

Common Debt Types They Handle:

Credit card debt

Personal loans

Auto deficiency balances

Medical bills

Utility bills

Cell phone bills

How Does NCB Management Services Inc Contact Consumers?

NCB Management Services Inc operates under strict regulatory oversight. They must comply with federal and state laws governing debt collection practices. However, violations still occur, which is why consumer awareness is crucial.

The company uses various collection methods:

Phone calls

Written notices

Email communications

Text messages (with consent)

Legal action when necessary

They have collection departments that specialize in different types of accounts and use automated systems to manage large volumes of consumer accounts.

Why NCB Management Services Is Calling You

There are several reasons why NCB Management Services might reach out:

Recent Account Default

If you recently stopped making payments on a credit card, loan, or other account, the original creditor may have hired NCB to collect the debt. This typically happens after 90-180 days of non-payment.

Old Debt Purchase

NCB may have purchased your old debt from the original creditor. For example, if you had a $2,000 credit card debt that was charged off three years ago, NCB might have purchased it for $200 and now wants to collect the full $2,000 plus interest and fees.

Real-World Example: Sarah received a letter from NCB about a Capital One credit card debt from 2019. She thought the debt was resolved when Capital One stopped calling her two years earlier. What actually happened was Capital One sold her debt to NCB, who now owns the account and has the right to collect it.

Mistaken Identity

Sometimes debt collectors contact the wrong person due to similar names, addresses, or Social Security numbers. This is more common than you might think and is a serious violation of your rights.

Expired Debt

NCB may be attempting to collect on time-barred debt where the statute of limitations has expired. While they can still contact you about old debt, they cannot legally sue you for it in most states.

Your Rights When Dealing with NCB Management Services

The Fair Debt Collection Practices Act (FDCPA) provides significant protections for consumers dealing with debt collectors like NCB Management Services.

Here are your key rights:

Right to Debt Validation

Within five days of first contact, NCB must send you a debt validation notice that includes:

The amount of the debt

The name of the original creditor

Your right to dispute the debt within 30 days

Information about obtaining verification if you dispute the debt

Right to Request Verification

If you dispute the debt within 30 days, NCB must provide verification of the debt before continuing collection efforts. Consumers report that NCB Management Services often fails to validate debts, even when requested. Many individuals submitted documentation requesting debt validation but received no response, leaving them unable to verify the legitimacy of the debts.

Protection from Harassment

NCB cannot:

Call before 8 AM or after 9 PM

Contact you at work if you tell them it's not allowed

Use profane or threatening language

Call repeatedly to harass you

Contact third parties about your debt (except your attorney, spouse, or credit reporting agencies)

Right to Cease Communication

You can send a written cease and desist letter telling NCB to stop contacting you. Once they receive this letter, they can only contact you to confirm they're stopping collection efforts or to notify you of specific legal action.

How to Handle NCB Management Services calls

When NCB Management Services contacts you, follow these steps:

Step 1: Don't Panic or Ignore

Ignoring debt collectors rarely makes the problem disappear. Instead, it can lead to lawsuits and wage garnishments. Take action to understand and address the situation.

Step 2: Validation of Debt

Send a debt validation letter within 30 days of first contact. Request:

Proof that you owe the debt

The original creditor's name and account information

Documentation showing NCB's authority to collect the debt

A complete payment history

Step 3: Check Your Credit Reports

Review your credit reports from all three bureaus (Experian, Equifax, TransUnion) to see how the debt appears. Look for inaccuracies in dates, amounts, or account status.

Step 4: Verify the Statute of Limitations

Research your state's statute of limitations for the type of debt NCB is trying to collect. If the debt is time-barred, you have strong legal protection against lawsuits.

Step 5: Document Everything

Keep detailed records of all communications with NCB, including:

Dates and times of phone calls

Names of representatives you spoke with

Written correspondence

Payment agreements or settlements

Bonus Tip: Know Your Options

You have several ways to handle NCB Management Services. Choose what fits your situation and budget.

Dispute the Debt

If the debt isn’t yours or the balance is wrong, send a written dispute and request validation. Don’t pay until it’s verified.

Negotiate a Settlement

Many collectors accept less than the full amount. Aim for a written agreement—consider asking for pay-for-delete when possible.

Set Up a Payment Plan

Arrange affordable monthly payments that won’t strain your budget. Get the plan in writing before paying.

Seek Legal Help

If your rights were violated (harassment, incorrect reporting, improper notices), consult a consumer law attorney.

Want expert help choosing the best path and improving your credit?

Debt collection companies like NCB Management Services usually don't favor the idea of a lawsuit when consumers fail to pay what they supposedly owe. This is because lawsuits are hectic and time-consuming. When debt collection agencies contact you, they hope to settle the debt out of court by creating a payment plan that works for both parties.

Settlement Strategies

Start by offering 10-25% of the total balance

Get any agreement in writing before making payment

Negotiate for a "pay for delete" agreement to remove the account from your credit report

Never provide bank account information over the phone

Payment Plan Options

If you can't settle for a lump sum, NCB may accept a payment plan. Ensure any payment agreement includes:

The total amount to be paid

Monthly payment amounts and due dates

What happens if you miss a payment

Whether the account will be reported as "paid" or "settled"

NCB Management Services Lawsuit Risks

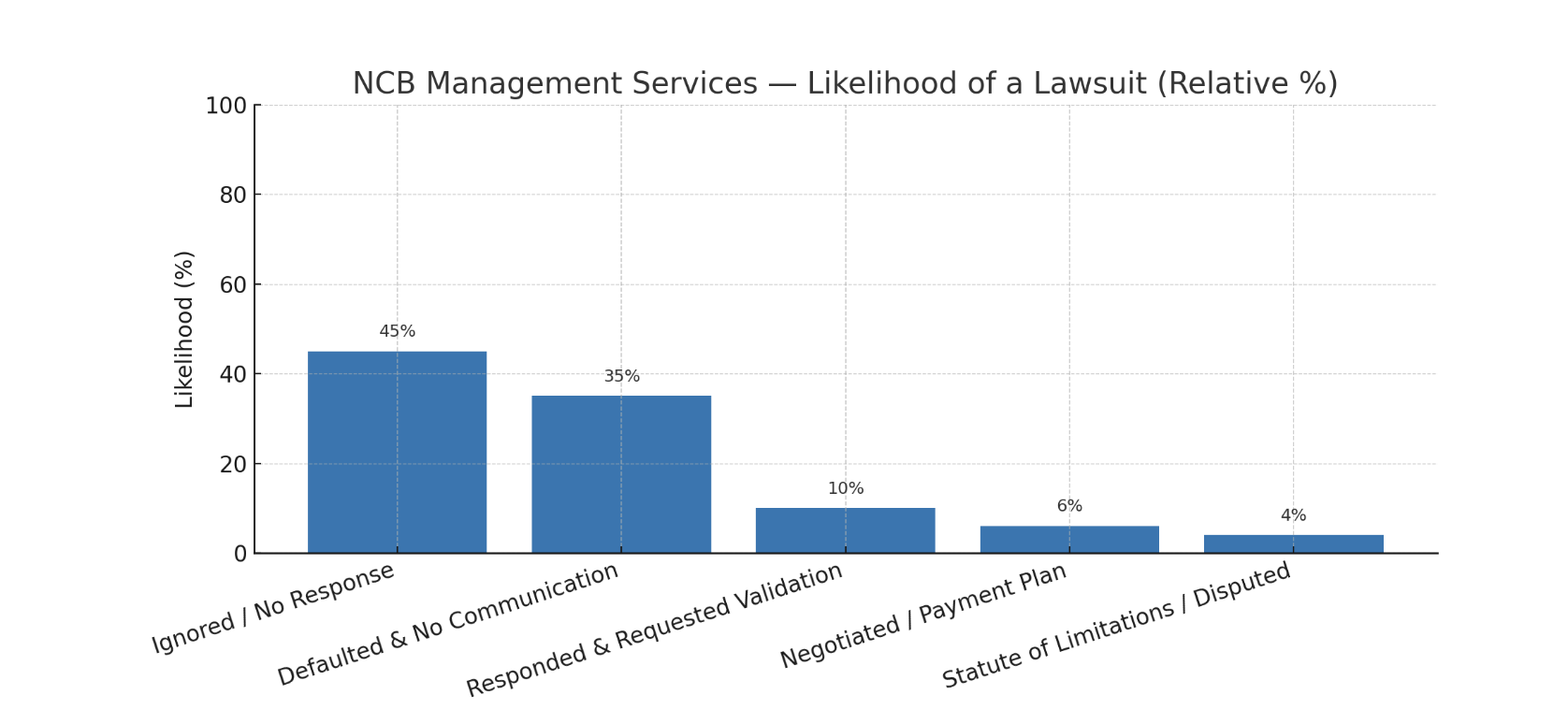

One of consumers' biggest fears when contacted by debt collection agencies like NCB management is the potential of a lawsuit. Since NCB is a legitimate debt collector, they can, and sometimes do, take legal action if debts aren’t addressed.

Here’s what you need to know:

Common Lawsuit Triggers:Debt Lawsuits often happen when a consumer ignores repeated collection attempts or fails to respond to validation requests.

Potential Outcomes: If NCB files a lawsuit, you could face a judgment, wage garnishment, or bank account levy—but only if the court rules in their favor.

Protect Yourself: Respond to all communications, keep detailed records, request debt validation, and check the statute of limitations for your account. Consulting a consumer attorney can help you navigate any legal threats safely.

Bottom line: Most debts are resolved without lawsuits. Knowing your rights and taking action quickly greatly reduces the risk of court involvement.

Protecting Your Credit and Financial Future

Dealing with NCB Management Services requires a strategic approach to protect your credit score and financial well-being:

Monitor Your Credit Reports

Check your credit reports regularly for accuracy. If NCB reports inaccurate information, dispute it with the credit bureaus. As a credit repair professional, I've seen significant score improvements when inaccurate collection accounts are removed.

Understand Credit Impact

Collection accounts can significantly damage your credit score. However, the impact lessens over time, and newer credit scoring models give less weight to paid collections.

Plan for the Future

Once you resolve the NCB account, focus on rebuilding your credit through:

Making all payments on time

Keeping credit card balances low

Not closing old credit accounts

Avoiding new collection accounts

When to Seek Professional Help

Consider consulting with a consumer attorney or credit repair professional if:

NCB is violating the FDCPA

You're facing a lawsuit

The debt may not be yours

You need help negotiating a settlement

The account is negatively affecting your credit score

Many consumer attorneys work on contingency for FDCPA violations, meaning you don't pay unless they win your case.

Conclusion

NCB Management Services is a legitimate debt collection agency, but that doesn't mean you're powerless when they contact you. Remember that debt collection is often a negotiable process. Whether you're dealing with a legitimate debt or fighting an incorrect collection account, staying informed and taking action early are your best defenses.

If you're struggling with NCB Management Services or other debt collection issues, seek help. Using your consumer rights can often lead to better outcomes than trying to handle everything yourself.