Nelson and Kennard: Everything You Need To Know About This Company

by Joe Mahlow • Updated on Jul. 10, 2026

NK

Nelson & Kennard — Quick Summary

Tactics, rights, responses, and next steps

Who they are

Founded: 1986 • HQ: McClellan, CA • Focus: debt collection for credit cards, auto deficiency balances, personal loans, and some commercial debt.

Operates in CA, OR, WA, CO, NM, HI, NV, MA, and OK.

Collection tactics

Letters and frequent phone calls, starting with demand letters.

Quick escalation to lawsuits if ignored; reports of poor notice/service.

Complaints of FDCPA violations: unverified debt, wrong info, harassment.

Your rights (FDCPA)

Request debt validation within 30 days of first contact.

Limit communication to writing, set call times, stop work calls.

Harassment protection: document profanity, threats, or excessive calls.

How to respond

Step 1: Don’t ignore — risk of lawsuits/garnishment.

Step 2: Send a Debt Validation Letter within 30 days.

Step 3: Document letters, calls, names, dates.

Step 4: Options: dispute, negotiate, payment plan, or bankruptcy.

Settlement & complaints

Settlements often range 40–80%. Always get terms in writing and ask for “paid in full” reporting. Common complaints: failed verification, improper fees, and mishandled payment plans.

If they sue you

Respond within 20–30 days. Defenses: lack of standing, expired statute of limitations, FDCPA violations, wrong creditor details. Missing deadlines leads to default judgments and garnishment.

Credit impact

Collections stay for 7 years. “Settled” hurts more than “paid in full.” Judgments damage credit and enable garnishment.

Final takeaways

Act fast: early responses preserve options.

Know your rights: FDCPA is your protection.

Get help: credit repair pros or attorneys can support you.

Getting contacted by Nelson and Kennard can be stressful, so as other companies claiming to be debt collectors.

Many consumers don't know what to expect from this debt collection law firm. After nearly two decades in credit repair, I've helped countless clients navigate situations with Nelson and Kennard.

This guide explains everything you need to know about this debt collector. You'll learn their tactics, your rights, and how to protect yourself.

Who Is Nelson and Kennard?

Nelson and Kennard, LLP formed in 1986 as a partnership between Donald G. Nelson and Robert Scott Kennard. The firm originally focused on automobile finance industry collections, including deficiency balances and bankruptcy creditor representation.

By 1995, they evolved into a full-service collection firm. They now handle credit card debt, consumer lines, commercial debt, and mortgage collections. The firm has expanded through mergers and currently services California, Oregon, Washington, Colorado, New Mexico, Hawaii, Nevada, Massachusetts, and Oklahoma.

Key Facts About Nelson and Kennard:

Founded in 1986

Law firm specializing in debt collection

Most employees are NOT lawyers, despite being a law firm

They represent debt purchasers and original creditors rather than buying debts themselves

Located in McClellan, California

What Types of Debt Does Nelson and Kennard Collect?

Nelson and Kennard focuses on various consumer debts:

Credit Card Debt

This is their primary collection area. They work with major credit card companies to recover unpaid balances. Capital One is one of their frequent clients, based on consumer complaints I've seen.

Auto Deficiency Balances

Their original specialty remains strong. When your car gets repossessed and sold for less than you owe, Nelson and Kennard pursue the remaining balance.

Personal Loans and Lines of Credit

They collect on various unsecured consumer debts from banks and finance companies.

Commercial Debts

Business-related collections, though less common for individual consumers.

Nelson and Kennard Collection Tactics

Understanding their methods helps you respond appropriately. Here's what to expect:

Initial Contact Methods

Nelson and Kennard uses standard debt collection activities including letters and telephone calls. They typically start with a demand letter claiming they represent your creditor.

Phone Call Patterns

Based on client experiences, they call frequently. Some clients report multiple calls per day from different representatives.

Legal Threats and Lawsuits

They file debt collection lawsuits when other collection efforts fail. This escalation happens quickly if you ignore their communications.

Red Flag: Some consumers report lack of proper notice and service of legal documents. Always verify any legal claims independently.

FDCPA Compliance Issues

Nelson and Kennard has received consumer complaints alleging violations of the Fair Debt Collection Practices Act (FDCPA), including failure to verify debts and attempting to collect debts not owed.

Court cases show they've been accused of sending collection letters that falsely identified consumers' original creditors and filing lawsuits with incorrect creditor information.

Nelson & Kennard Flowchart

Initial Contact

Letters and calls from Nelson & Kennard about a debt.

⬇

Debt Validation

Consumer can request proof of the debt within 30 days.

⬇

Negotiation or Settlement

Payment plan or lump-sum settlement may be offered.

⬇

Lawsuit Filed

If ignored, Nelson & Kennard may escalate to court action.

⬇

Judgment & Enforcement

Possible wage garnishment, bank levy, or liens if judgment is won.

Your Rights When Dealing with Nelson and Kennard

The Fair Debt Collection Practices Act (FDCPA) protects you. Here are your key rights:

Debt Validation Rights

You can send Nelson and Kennard a Debt Validation Letter to determine whether they have correct information about your unpaid debt. They must provide:

Original creditor information

Amount owed

Proof they have authority to collect

Communication Controls

You can limit how they contact you:

Request written communication only

Specify acceptable call times

Tell them to stop calling your workplace

Harassment Protection

Document any harassment including profanity, verbal abuse, or excessive phone calls. These violations can result in damages up to $1,000 plus attorney fees.

How to Handle Nelson and Kennard Contact

Here's my recommended approach based on years of client cases:

Step 1: Don't Ignore Them

The debt will not go away and neither will Nelson and Kennard. The debt will only grow and Nelson and Kennard will get their money. Ignoring them leads to lawsuits and wage garnishment.

Step 2: Request Debt Validation

Send a written debt validation letter within 30 days of their first contact. This forces them to prove:

Settlement can save you money, but approach it strategically:

Settlement Timing

Consider settlement when receiving frequent phone calls and threatening letters, or if you've been sued. Early settlement in debt typically gets better offers.

Typical Settlement Ranges

Based on client experiences, Nelson and Kennard often accepts:

40-60% for older debts

60-80% for recent debts

Lump sum payments get better discounts

Settlement Negotiation Tips

Get everything in writing before paying

Negotiate for "paid in full" reporting instead of "settled"

Don't give bank access - use cashier's checks or money orders

Start low - they expect negotiation

Tax Consequences

Forgiven debt over $600 may be taxable income. Request IRS Form 1099-C if they report cancellation of debt.

Common Nelson and Kennard Complaints

Consumer complaints reveal recurring issues:

Billing Disputes. Consumers report improper fees being added, such as $65 personal service fees despite no lawsuit being filed.

Verification Problems. Some consumers report they fail to provide contracts or assignment agreements proving legal authority to collect.

Payment Plan Issues. One consumer set up a $66 monthly payment plan in 2019, but Nelson and Kennard never processed the automatic payments as agreed.

Legal Representation Claims. Court records show accusations that Scott Kennard didn't conduct meaningful review before signing collection letters sent to hundreds of consumers.

When Nelson and Kennard Sues You

If you've been sued or threatened by Nelson and Kennard, don't delay taking action to stop a default judgment. Don't let them seize bank accounts, garnish wages, or file liens against your property.

Lawsuit Response Timeline

You typically have 20-30 days to respond to a lawsuit, depending on your state. Missing this deadline results in automatic judgment against you.

Common Defenses

Based on their violation history, potential defenses include:

One case involved a consumer incurring over $38,000 in legal fees defending against Nelson and Kennard's lawsuit. This shows why early resolution matters.

How to Stop Nelson and Kennard Harassment

If they cross legal lines, you have options:

Document Violations

Record instances of:

Calls before 8 AM or after 9 PM

Threats of illegal action

Disclosure of debt to third parties

Continued contact after cease and desist

File Complaints

Report violations to:

CFPB (Consumer Financial Protection Bureau)

State Attorney General

FTC (Federal Trade Commission)

In 2019 alone, CFPB received 21 complaints against Nelson and Kennard, ranking them number 561 among financial companies for complaint volume.

Legal Action

FDCPA violations can result in:

Up to $1,000 in damages per violation

Attorney fees paid by the collector

Actual damages for harassment

Alternative Solutions to Consider

Sometimes working directly with original creditors works better than dealing with Nelson and Kennard:

Contact Original Creditor. The original creditor may still own your debt. They often offer better payment terms than collection agencies.

Credit Counseling. Nonprofit credit counseling can help negotiate with creditors and create manageable payment plans.

Debt Management Programs. These consolidate payments and may reduce interest rates, though they won't reduce principal balances.

Impact on Your Credit Score

Nelson and Kennard contact affects your credit in multiple ways:

Collection Account Reporting

They report unpaid collections to credit bureaus. This remains on your credit report for seven years from the original delinquency date.

Settlement vs. Payment in Full

"Settled" accounts hurt your score more than "paid in full" accounts. Always negotiate for better reporting terms.

Lawsuit Judgments

Court judgments appear on credit reports and severely damage your score. They also enable wage garnishment and asset seizure.

First Missed Payment

Initial 30-day late mark. Small score dip but warning sign.

Debt in Collections

Collection account reported. Major drop (up to 100+ points).

Settlement vs Payment

“Settled” status damages more than “Paid in full.”

Lawsuit & Judgment

Court judgment reported. Severe long-term score damage.

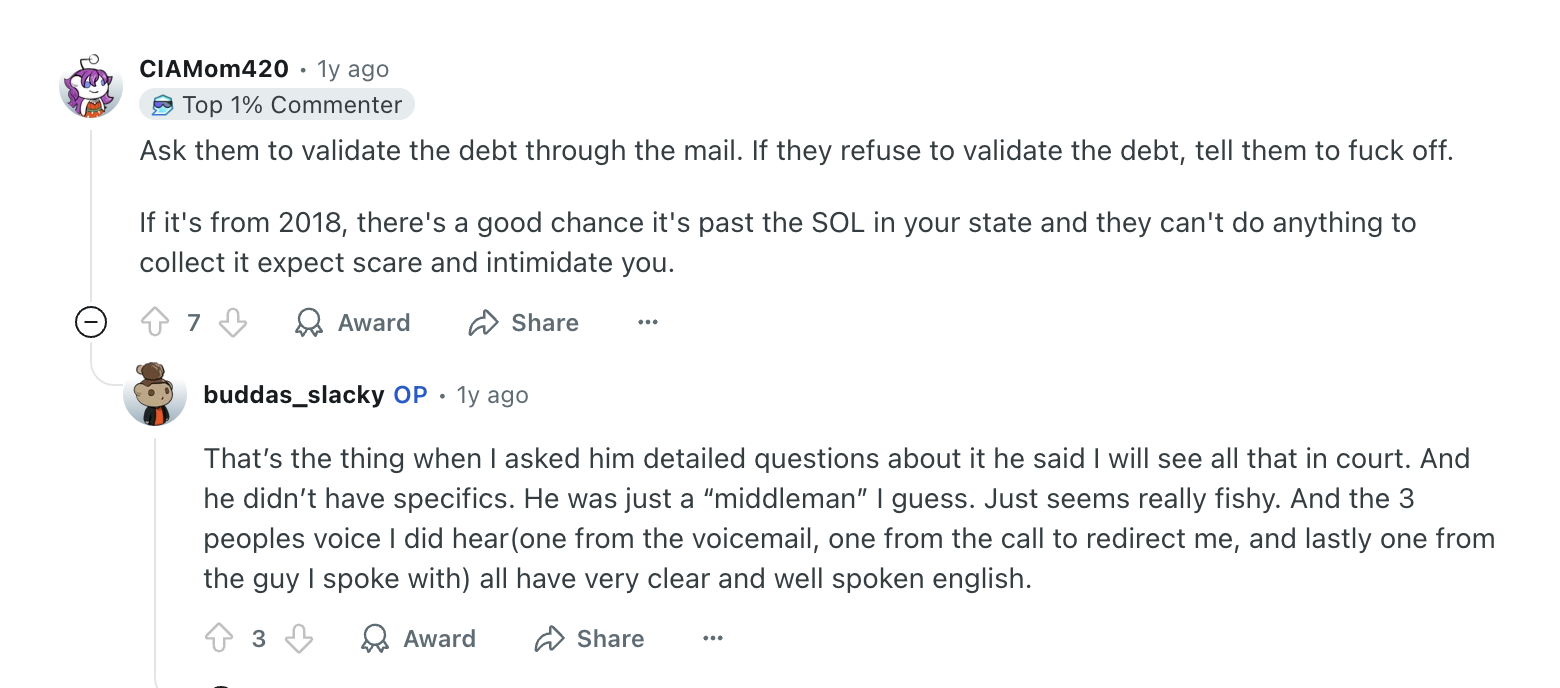

A Reddit thread in r/personalfinance highlighted concerning debt collector behaviors that consumers should recognize.

One user posted: "So today I got left a voicemail saying I was going to be processed served for a debt in the county where I live. I was confused so I called the number back(stupid I know). So the guy looks me up by phone number and says yes you have a credit card debt from 2018. He gives me the address for the debt and, while yes I did live there, I didn’t live there in 2018 or at least from 2013. He proceeds to tell me that I owe 3200 for the credit card. Doesn’t tell me any exacts but he does say 14 payments were made and then stopped so I can’t dispute the dept."

Good thing there were helpful responses on what to do:

This real experience shows exactly what to watch for.

Watch for these concerning behaviors:

Verification Issues

Refusing to provide debt documentation

Claiming they "don't need to prove" the debt

Providing incomplete or inconsistent information

Pressure Tactics

Demanding immediate payment without validation

Threatening immediate legal action

Claiming special limited-time offers

Communication Violations

Calling multiple times per day

Contacting family or employers about your debt

Using abusive or threatening language

Final Takeaway About Nelson and Kennard

Nelson and Kennard is a legitimate debt collection law firm, but they're not infallible. They make mistakes, violate laws, and sometimes pursue debts they can't prove.

Understanding your rights and their tactics levels the playing field. Whether you need to dispute the debt, negotiate a settlement, or defend against a lawsuit, knowledge empowers you to make the best decisions for your financial future.

Remember, every situation is unique. What worked for one client may not work for another. Consider your specific circumstances and don't hesitate to seek professional guidance when needed.

The key is taking action rather than avoiding the problem. Nelson and Kennard will pursue legitimate debts aggressively, but they must follow the law while doing so. Make sure they do.

Disclaimer: This article is provided for educational purposes only and does not constitute legal advice.

All information about Nelson & Kennard and related consumer experiences is based on publicly available data and client reports.

We do not claim affiliation with Nelson & Kennard or guarantee specific outcomes.

If you are facing legal action, please consult with a qualified attorney.