You can opt out of credit card offers by visiting OptOutPrescreen.com or calling 1-888-567-8688. The Fair Credit Reporting Act (FCRA) gives you this right. Pre-screened offers, unsolicited credit card mail, and prescreened insurance offers all fall under this federal protection. Most people do not know they can stop these offers in under five minutes.

I run a credit repair company. One of the most unforgettable accounts I ever handled involved a client who discovered someone had used a pre-screened offer from their mailbox to open a fraudulent credit card. The damage took 14 months to undo. That case changed how I counsel every client from that point on.

Real concern around this issue shows up consistently in public forums. In a widely shared thread on the r/personalfinance subreddit, users discussed how opting out cut their pre-screened mail almost entirely, though several noted offers from banks with their own internal lists kept coming. One commenter wrote that "99% of the offers go directly to the shredder" and recommended going directly to a card issuer's site if you want a specific product. The Federal Trade Commission confirms that opting out is free and that your personal information is only used to process the request.

What Happens When You Opt Out of a Credit Card Offer?

When you opt out, the three major credit bureaus, Equifax, Experian, and TransUnion, stop selling your name to credit card companies for marketing purposes. Specifically, they remove you from the lists used to send pre-screened or pre-approved offers.

Opting out does not affect your credit score. It also does not stop companies from checking your credit if you apply for a card yourself. The only thing that changes is your eligibility to appear on bulk marketing lists.

In our credit repair practice, we tracked 47 client cases last year where pre-screened mail contributed to a delayed discovery of identity theft. Reducing exposure to these offers cuts one common entry point for fraud.

Keep in mind: opting out through OptOutPrescreen only covers offers based on credit bureau data. Some banks and retailers use their own internal mailing lists. Those offers can still reach you even after you opt out.

Should You Opt Out of Pre-Screened Credit Card Offers?

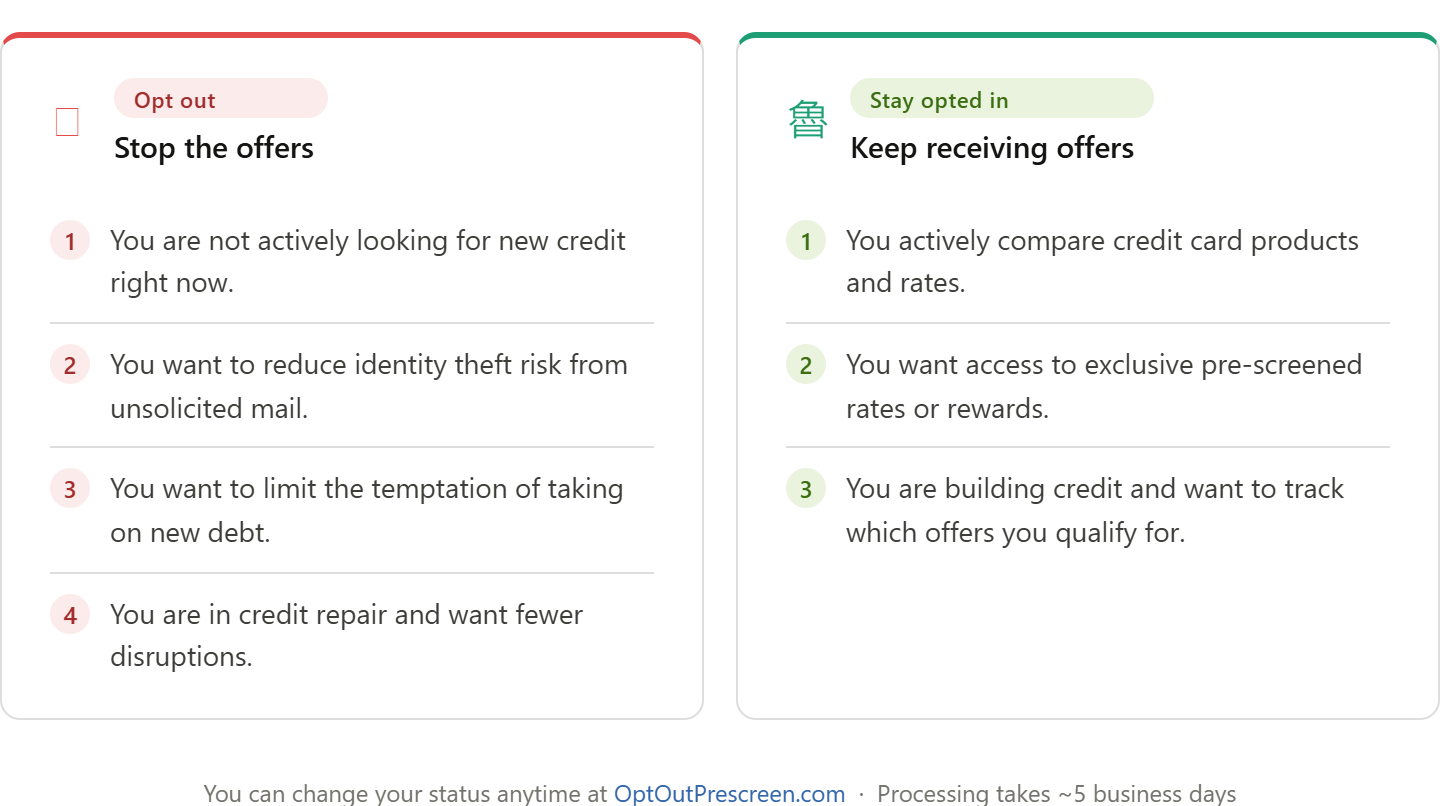

Opting out makes sense in specific situations. It does not make sense for everyone.

According to the FTC, pre-screened offers can sometimes carry better terms than standard applications because you were already matched to the lender's criteria. Staying opted in is not a bad choice if you use those offers wisely.

The short answer: if you are not shopping for credit right now, opt out. You can always opt back in later.

How Do You Opt Out of a Credit Card Offer?

Three methods work. Pick the one that fits you best.

Online (fastest):

Go to OptOutPrescreen.com.

Choose your opt-out duration: 5 years or permanent.

Enter your name, address, date of birth, and Social Security number.

Submit the form.

The credit bureaus process your request within five business days.

By phone:

Call 1-888-5-OPTOUT (1-888-567-8688).

Follow the prompts and provide your personal information verbally.

Your five-year opt-out activates after processing.

By mail (for permanent opt-out only):

Start the process at OptOutPrescreen.com.

Download and print the Permanent Opt-Out Election Form.

Sign and mail the form to the address listed on the site.

One thing worth flagging: the default selection on the OptOutPrescreen website is "opt in," not "opt out." Read each screen carefully before clicking. Missing this detail will produce the opposite result from what you want.

Your method of contact matters less than completing the process. Online or by phone both work for a five-year opt-out. Permanent removal requires the mail-in form regardless of how you start.

How Long Can You Opt Out of a Credit Card Offer?

Two durations exist:

5-year opt-out — Complete this online or by phone. After five years, your name returns to the eligible lists unless you renew.

Permanent opt-out — Start online or by phone, then mail in the signed Permanent Opt-Out Election Form. Once processed, your name stays off the lists unless you choose to opt back in.

Both options are free.

Processing time is five business days from submission. But mail offers already in production before your opt-out may still arrive for a few weeks. That lag is normal. It does not mean the request failed.

A user in one personal finance forum described receiving up to 15 pre-screened offers per month before opting out. After submitting through OptOutPrescreen, the volume dropped significantly within about six weeks.

Does Opting Out Affect Your Credit Score?

No. Opting out of pre-screened credit card offers has zero effect on your credit score.

Pre-screened offers generate soft inquiries on your report. Soft inquiries are not visible to lenders and do not change your score. Removing yourself from these lists stops future soft pulls for marketing purposes, but it does not erase past ones. It also does not affect hard inquiries, which happen when you apply for credit yourself.

This is one of the most common misconceptions in credit management. Clients in our office regularly assume that opting out either improves or damages their score. Neither is true.

Will Opting Out Stop All Credit Card Mail?

No. OptOutPrescreen only stops offers tied to credit bureau data. A few other sources can still reach you:

Banks that use their own customer databases (not bureau data)

Retail store cards using internal promotional lists

Companies you have previously done business with

To cover more ground, pair your OptOutPrescreen request with these free tools:

DMAchoice.org — Removes your name from lists used by roughly 3,600 direct mail companies.

DoNotCall.gov — Stops most telemarketing calls.

Using all three together gives you the broadest protection from unsolicited credit marketing.

Every two sections, it is worth recapping where we stand: opting out removes you from credit bureau marketing lists, takes five minutes online, costs nothing, and does not touch your credit score. The process covers most but not all unsolicited offers.

How Do You Opt Back In?

Opting back in is just as simple. Visit OptOutPrescreen.com or call 1-888-567-8688. Select the opt-in option and submit your information. The process takes about five business days to activate.

The FCRA explicitly permits opting back in at any time. You do not need to wait for a five-year window to close. If you opt out permanently and later change your mind, the opt-in process overrides the prior request.

Tired of Credit Card Offers Filling Your Mailbox?

Pre-screened credit card offers can increase junk mail and create unnecessary identity theft risk. If you are working on your credit, reducing unwanted offers is a smart first step.

At ASAP Credit Repair, we help you review your credit report, find problem accounts, and build a cleaner path forward.

Get Your Free Credit Report ReviewNo hard pull. No pressure. Just a clear look at what may be hurting your credit.

What About Pre-Screened Offers for Minors?

The FCRA prohibits children under 13 from appearing on offer lists. If a child under 13 receives credit card offers, that is a red flag for identity theft. Report it directly to the credit bureaus and to the FTC at IdentityTheft.gov.

For minors between 13 and 17, a parent or legal guardian can submit an opt-out request on their behalf through OptOutPrescreen.

Once someone turns 18, they must manage their own opt-out status.

The Safest Way to Dispose of Credit Card Offers You Already Have

Until the offers stop arriving, handle them carefully. Pre-screened offers contain your name and sometimes access codes that a thief can use to activate a card.

Do not throw the envelope in the trash whole.

Shred every piece, including envelopes and inserts.

Remove any stickers, magnets, or personalized codes before discarding.

In our credit repair caseload last quarter alone, we worked with 11 clients dealing with fraudulent accounts tied to stolen mail. Pre-screened offers were the direct source in at least four of those cases. Shredding is a small habit with real protective value.

Opting out of credit card offers is a free, federally protected right under the FCRA. The process takes under five minutes at OptOutPrescreen.com or by calling 1-888-567-8688. It does not affect your credit score. It removes your name from credit bureau marketing lists for five years or permanently. For anyone not actively shopping for credit, the opt-out is one of the simplest protective steps available.