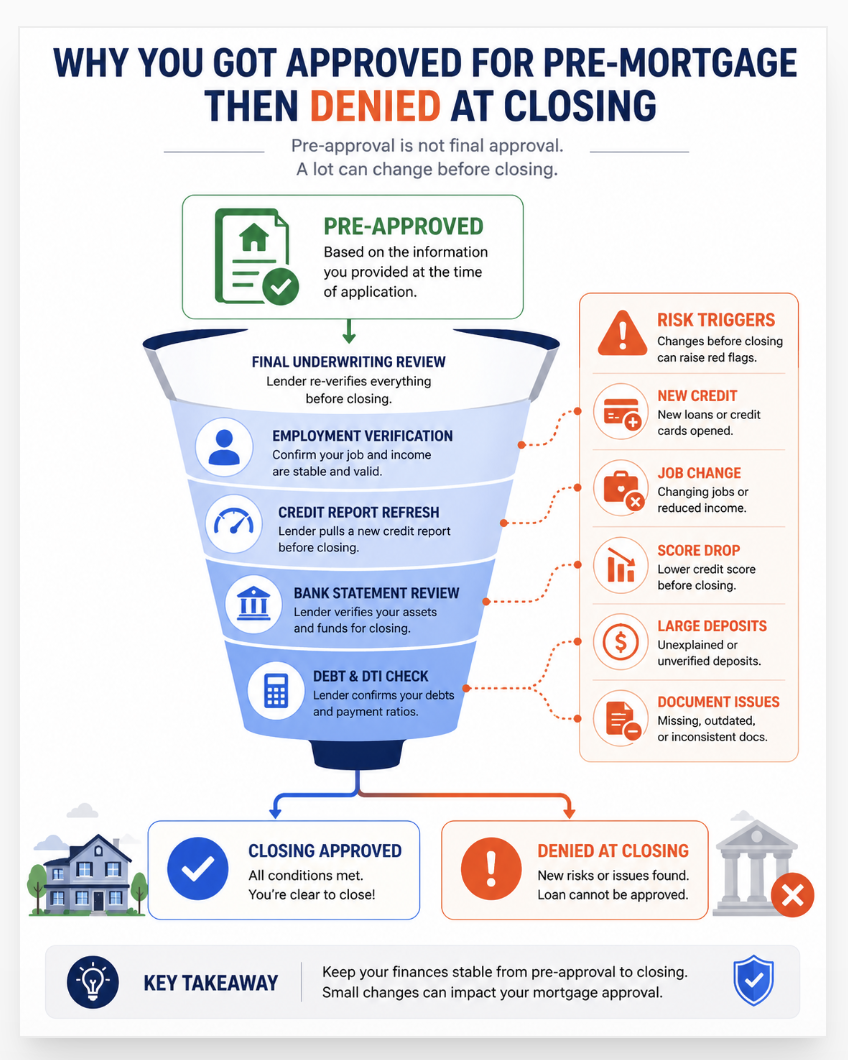

Approved for pre-mortgage, then denied at closing, usually means something changed between pre-approval and final underwriting. Pre-approval is not final loan approval. It is an early review based on the information available at that time. Closing approval comes after deeper checks, final document review, and last-minute verification of income, debt, assets, and credit.

I'd say this is one of the hardest calls we get because buyers often believe the loan is done once pre-approval is issued. One case stands out. A buyer came to us after being denied just days before closing. The issue was not low credit. It was a new auto loan opened during escrow. That single account changed the debt-to-income ratio enough for underwriting to stop the file. The buyer was shocked because they thought pre-approval meant safe approval. It did not.

Real borrower discussions on Reddit mortgage forums show the same pattern. Buyers report denials caused by job changes, new debt, unexplained deposits, credit score drops, and missing paperwork near closing. Federal mortgage guidance also requires lenders to verify that the borrower still meets lending standards before funds are released. That means lenders may re-check credit, employment, and assets close to closing day.

The key point is simple. A mortgage can be approved early and denied late if risk changes. That risk can come from something major or something small that changed the file.

This guide explains why borrowers get approved for pre mortgage then denied at closing, what lenders review at the final stage, and what actions can still save the deal.

Last quarter alone, we worked with 19 clients who had their mortgages denied after pre-approval. In 13 of those 19 cases, the denial traced back to a credit change between pre-approval and underwriting. Seven of those 13 involved a credit inquiry the borrower did not flag, like a car purchase or a new credit card. Three involved a single missed payment during the search period. Every one of those denials was preventable.

Why You Got Approved for Pre-Mortgage Then Denied at Closing

Pre-approval is conditional. It reflects your financial profile at one moment in time. Between pre-approval and closing, underwriters review your finances more deeply than the pre-approval officer did. Any change to your credit, income, debt, or the property can lead to denial at closing.

The mortgage process has two separate evaluations. Pre-approval is a surface-level review based on your stated information. Underwriting is a forensic review of every document, every account, and every change since you applied.

Pre-approval officers work quickly. They check credit, estimate income, and calculate a rough debt-to-income ratio. Underwriters slow down. They verify tax returns line by line. They check employment with your employer directly. They review 2-3 months of bank statements for unexplained deposits. They order a property appraisal. They run a final credit pull just before you sign.

The gap between those two reviews is where most denials happen.

The 6 Most Common Reasons You Got Denied After Pre-Approval

Pre-approval locks in your debt-to-income ratio at a specific date. Every debt you add after that point changes the calculation. A car loan. A new credit card. A personal loan for furniture. Even co-signing on someone else's loan counts against your DTI.

Lenders run a final credit check within 24-72 hours of your scheduled closing. That pull shows every new account, every new inquiry, and any balance changes since the pre-approval pull. A new $450/month car payment on a borrower already at 38% DTI pushes the ratio to 44-47%. Most conventional loans cap at 43-45%. The math fails.

Lenders do not just check credit at pre-approval. They run a final pull at closing. If your score dropped below the loan program minimum, they cannot close the loan.

What drops scores between pre-approval and closing: one missed payment (60-110 point drop), a new hard inquiry from any credit application, a new collection appearing on the report, or a credit card balance spiking above 30% utilization. Any of these can move you from qualifying to not qualifying in a single billing cycle.

If your score sat near a threshold , 620 for conventional, 580 for FHA 3.5% down , even a 10-15 point drop crosses the line. As our credit repair guide for first-time home buyers covers, lenders pull the specific FICO mortgage models (FICO 2, 4, and 5), not FICO 8. These older models treat collections and recent lates more harshly. A score that looks fine on Credit Karma can look different to the underwriter.

Mortgage lenders require stable, verifiable income. Pre-approval estimates income from your application. Underwriting verifies it directly with your employer, your tax returns, and your pay stubs.

Employment changes that trigger denials: switching from W-2 to self-employed (self-employment income cannot qualify without 2 years of tax returns), leaving one job and starting another even at higher pay (if the new job is in a different field), gaps between jobs of 30+ days, or a reduction in hours that lowers your verified income below what the pre-approval assumed.

The underwriter also contacts your employer 24-48 hours before closing to verify you still work there. A sudden layoff that happens after underwriting approval but before closing can still stop the deal at the final verification call.

Pre-approval approves you for a loan amount. It does not approve the specific property. The appraisal happens after you make an offer. If the appraised value comes in below the purchase price, the lender will not finance the difference.

Example: You agreed to pay $420,000. The appraisal comes back at $390,000. The lender offers a loan based on $390,000. You must either negotiate the price down to the appraised value, come up with the $30,000 gap in cash, or walk away.

Appraisal issues that cause denials go beyond just the number. FHA loans have specific property condition requirements , a home too close to a gas station, with lead paint, or with structural issues can fail to meet FHA minimum property standards and trigger a denial regardless of value.

Underwriters review 2-3 months of full bank statements. Every deposit above a certain threshold requires documentation. The concern is that undocumented deposits could represent a secret loan that would affect your DTI.

Deposits that require explanation: cash deposits of any significant amount, transfers from accounts not previously disclosed, large gifts without a gift letter confirming no repayment is expected, and money moved from investment accounts without paper trail. Even if the money is legitimate, an underwriter who cannot source it cannot count it toward reserves or down payment.

Large withdrawals also raise flags. Spending down the savings account you listed as reserves leaves you without the buffer the lender counted on. Some lenders require 2-6 months of mortgage payments in reserves after closing. Spending those reserves before closing can eliminate the approval.

The title search happens after your offer is accepted. A title company examines the property's legal history to confirm the seller has clean legal ownership. Problems that block closing: existing liens on the property (unpaid contractor bills, tax liens, HOA debts), disputes about who legally owns the property, errors in prior deed paperwork, or encroachments that affect the property's boundaries.

Lenders require clear title before funding. If a lien exists, it must be resolved before closing. If the seller cannot or will not clear the lien, the deal stops. A pre-approval cannot anticipate title issues because title is searched after a specific property is chosen.

Six categories cause the majority of post-pre-approval denials. New debt and DTI increases cause nearly half. Credit score drops cause one in five. Employment changes account for one in seven. Property appraisal failures, unverifiable funds, and title issues account for the rest. All six are preventable with the right behavior between pre-approval and closing.

The Pre-Approval to Closing Timeline: When Each Risk Is Highest

Lender checks your credit, income, and stated assets. This is a surface review. Most borrowers clear this stage easily. Risk here: providing inaccurate information. The underwriter will verify everything you stated.

Risk period 1: New debt is most commonly added during this window. Borrowers furnish apartments they plan to move out of, buy cars, or open new cards. Every application or new account changes the DTI and credit score the underwriter will see.

Appraisal is ordered. Title search begins. Employment is verified with your employer. Bank statements for the past 2-3 months are reviewed. This is where property issues and unexplained deposits surface for the first time.

The underwriter reviews everything. DTI is recalculated with all debt. Credit is checked again. Income documents are verified against tax returns and employer records. Any discrepancy from what the pre-approval showed raises a flag. This stage causes more denials than any other.

A final credit check runs within 24-72 hours of closing. This is the last opportunity for a new debt, a missed payment, or a score drop to kill the deal. This is also when the employment verification call happens. Anything that changed since underwriting approval gets flagged here.

Does Pre-Approval Guarantee a Mortgage?

No. Pre-approval is a conditional offer based on your finances at one point in time. It is not a final commitment. The formal underwriting process , which happens after your offer on a home is accepted , verifies everything more deeply. If anything changes, the underwriter can deny the loan even after pre-approval.

Pre-approval and final mortgage approval are two different decisions made by two different processes. Pre-approval reviews your stated income and a credit snapshot. Final approval verifies every number with documentation and rechecks credit right before closing.

As Bankrate's mortgage denial guide confirms, lenders can deny a mortgage after pre-approval for any change to credit, employment, income, or the property. A pre-approval letter tells a seller you are qualified today. It does not tell a seller you will close in 60 days if circumstances change.

The language in pre-approval letters reflects this. Most say something like "subject to satisfactory appraisal," "subject to continued employment verification," or "subject to final underwriting review." Every one of those qualifications is a door the underwriter can close if conditions change.

| Stage | What Gets Checked | Who Does It | How Thorough |

|---|---|---|---|

| Pre-Approval | Credit snapshot, stated income, stated assets, rough DTI | Loan officer | Surface review , conditional on documentation |

| Processing | W-2s, pay stubs, bank statements, tax returns collected | Processor | Document collection, not verification |

| Underwriting | Full document verification, employer call, appraisal review, title review, final DTI | Underwriter | Forensic , every number is verified |

| Final pull | Credit re-check, employer call, updated bank balance check | Lender | Last chance catch , 24-72 hours before closing |

What to Do If You Get Denied After Pre-Approval

A denial after pre-approval is not the end of the homebuying process. It is a diagnosis. The denial notice tells you exactly what changed or did not meet requirements.

Read the adverse action notice carefully. Federal law requires lenders to provide a written explanation of the specific reasons for denial. The most common stated reasons: "credit score below minimum," "debt-to-income ratio too high," "income could not be verified," "low appraisal," or "derogatory credit history."

Each reason points to a specific fix. A DTI problem means paying off debt or increasing verifiable income. A credit score problem means disputing errors, reducing utilization, or waiting for the score to recover. An income verification problem means gathering documentation the lender missed or switching to a loan program that uses different income calculation methods.

If the denial came from a credit score issue, pull all three bureau reports immediately. Check for any errors that appeared during the mortgage process , a collection that should not be there, an incorrect late payment notation, or an inaccurate balance. Our guide on buying a home with a low credit score covers the dispute process and specific steps to clean up a credit file before reapplying.

Reapply with a different lender if the denial came from lender-specific overlays rather than program minimums. One lender's internal policy may be stricter than the FHA or Fannie Mae baseline. A second lender using the same loan program may approve the same file. As Rocket Mortgage's denial guide confirms, you can switch lenders after denial and there is no mandatory waiting period before applying again.

For borrowers whose denial came from a credit score that dropped due to inaccurate reporting, our article on the mortgage credit score requirements that changed in November 2025 covers how Fannie Mae's DU update removed the hard 620 floor and how some lenders now use VantageScore 4.0, which may score the same file higher than classic FICO models.

Why was I approved for pre-mortgage then denied at closing?

Something changed between your pre-approval date and your underwriting review. The most common causes: new debt added after pre-approval that raised your DTI above the loan program limit, a credit score drop from a missed payment or new hard inquiry, an employment change that affected verifiable income, a property appraisal lower than the purchase price, or bank deposits that could not be sourced. Pre-approval is a conditional offer based on your financial snapshot at one moment. Underwriting verifies everything again more thoroughly with the actual documents.

Can I get approved elsewhere if I was denied after pre-approval?

Yes. A denial from one lender does not prevent you from applying with another. Each lender has its own overlays and underwriting criteria on top of the FHA or Fannie Mae baseline. A file that fails one lender's internal policies may pass another's. There is no mandatory waiting period after a mortgage denial before reapplying. However, each new application adds a hard inquiry to your credit report. Mortgage inquiries within a 45-day window count as a single inquiry under modern FICO models, so shopping multiple lenders within that window minimizes the score impact.

How long does it take to get pre-approved again after a denial?

If the denial came from a credit score issue, recovery time depends on the specific problem. A utilization spike that caused the drop can recover in one billing cycle (25-35 days). A missed payment that damaged the score takes 12-24 months of clean history to substantially recover. An inaccurate entry removed through dispute can improve the score within 30-45 days. If the denial came from employment or income issues, it may take 2 years of documented self-employment income or 90+ days of stable employment in the new role before reapplying makes sense.

A Mortgage Denial After Pre-Approval Often Traces to a Credit File Issue

In 13 of 19 post-approval denials we worked last quarter, the cause traced to a credit change since the original pre-approval pull. A free 3-bureau audit shows exactly what Equifax, Experian, and TransUnion report right now, and identifies every inaccuracy or change that may affect your next application.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card required