How to Remove Collections from Your Credit Report in Texas: A Proven way to do it.

If you have a collection account on your credit report, I want you to know something important: you are not stuck with it forever. Collections can be removed, and in Texas, you have more tools and protections than many people realize.

In this guide, I will walk you through exactly how to remove collections from your credit report in Texas, what makes Texas different from other states, and what steps you can take starting today.

What Is a Collection Account?

A collection account appears on your credit report when a creditor gives up trying to collect a debt and sells it to a third-party collection agency. That agency then tries to collect from you directly.

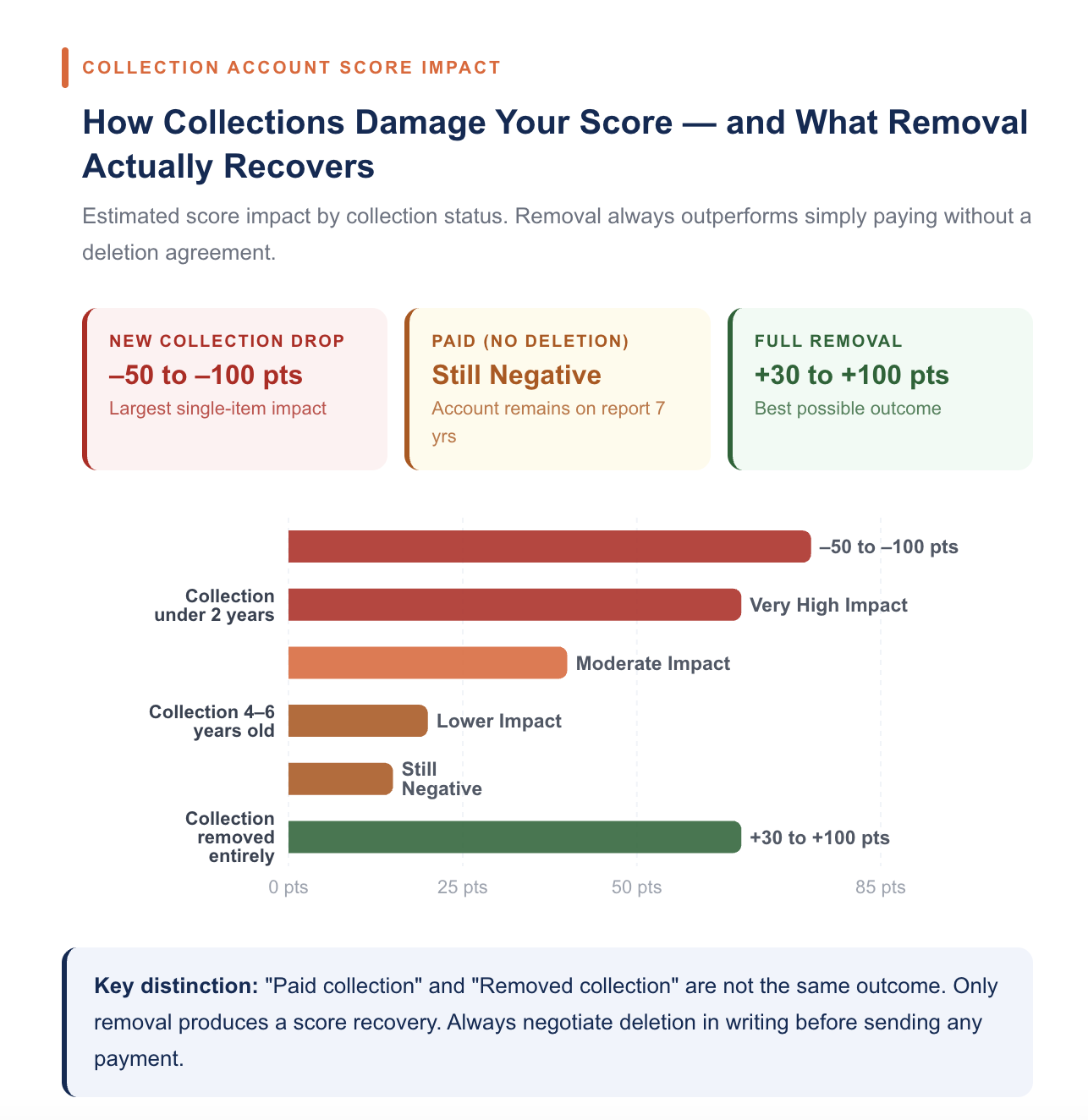

Collections can stay on your credit report for up to seven years from the date of the original missed payment. During that time, they drag your credit score down significantly. A single collection account can drop your score by 50 to 100 points or more.

The good news is that seven years is the maximum, not the minimum. You can often get collections removed much sooner.

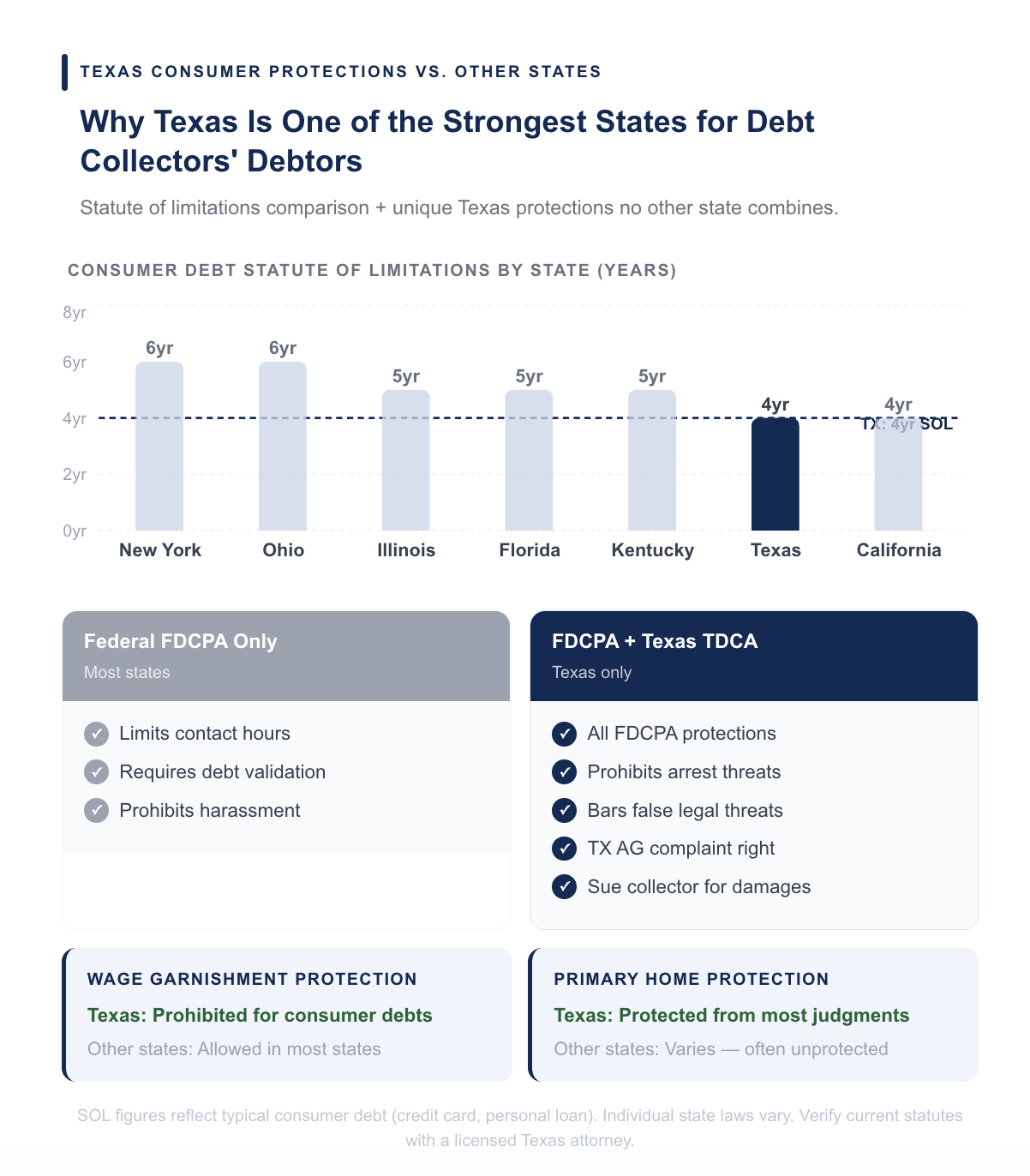

How Texas Is Different from Other States

This is where things get interesting. Texas has some of the strongest consumer protection laws in the entire country, and they work in your favor when dealing with debt collectors.

Texas Statute of Limitations on Debt

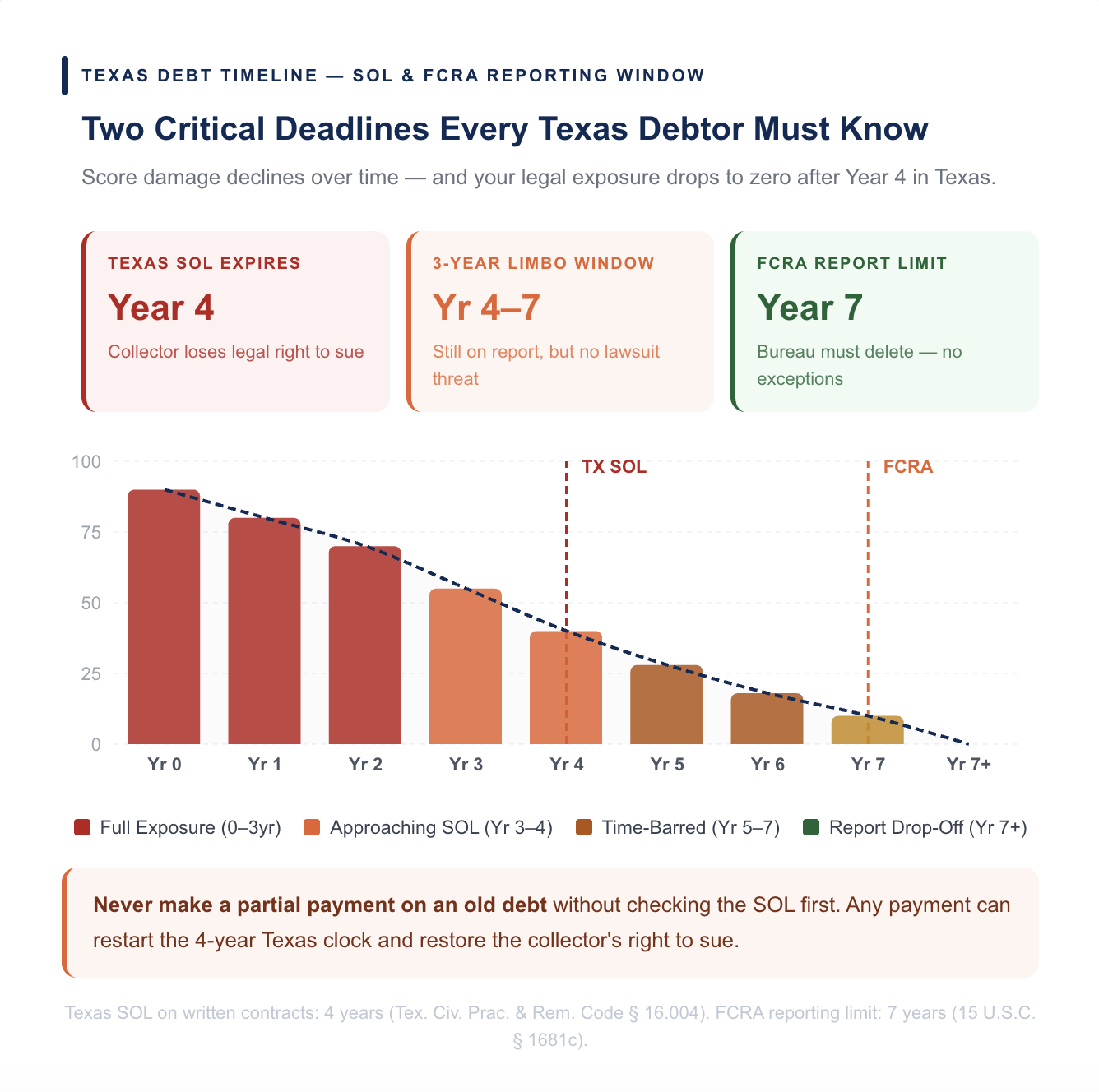

In Texas, the statute of limitations on most consumer debts is four years. This means a collector can only sue you in court to collect a debt within four years of your last payment or the date the debt became delinquent.

Most other states have a statute of limitations of three to six years, but many use six years as the standard. States like New York use six years. Kentucky uses five. California uses four, similar to Texas.

What makes Texas stand out is that its four-year limit applies broadly across credit card debt, medical debt, and personal loans. Once that window closes, a collector has no legal grounds to sue you in Texas court. This gives you real leverage in negotiations.

The Texas Debt Collection Act (TDCA)

Texas has its own state-level debt collection law called the Texas Debt Collection Act. It goes beyond the federal Fair Debt Collection Practices Act (FDCPA) in several important ways.

Under the TDCA, collectors in Texas cannot:

- Threaten you with arrest for an unpaid debt

- Use profane or threatening language

- Contact you at unreasonable hours

- Misrepresent the amount you owe

- Threaten to take legal action they do not actually intend to take

If a collector breaks any of these rules, you can file a complaint with the Texas Attorney General's office and potentially sue the collector for damages. That is a powerful tool most people never use.

In many other states, consumers only have the federal FDCPA to rely on. Texas residents have two layers of protection, which makes disputes and negotiations stronger here than in most parts of the country.

Texas Homestead and Wage Protections

Even if a collector does win a court judgment against you in Texas, your options for protecting your assets are strong. Texas law protects your primary home from most creditor judgments. Texas also prohibits wage garnishment for consumer debts, unlike the majority of U.S. states.

This means even in a worst-case scenario, a collector in Texas has fewer ways to come after you than in states like California, Florida, or Illinois.

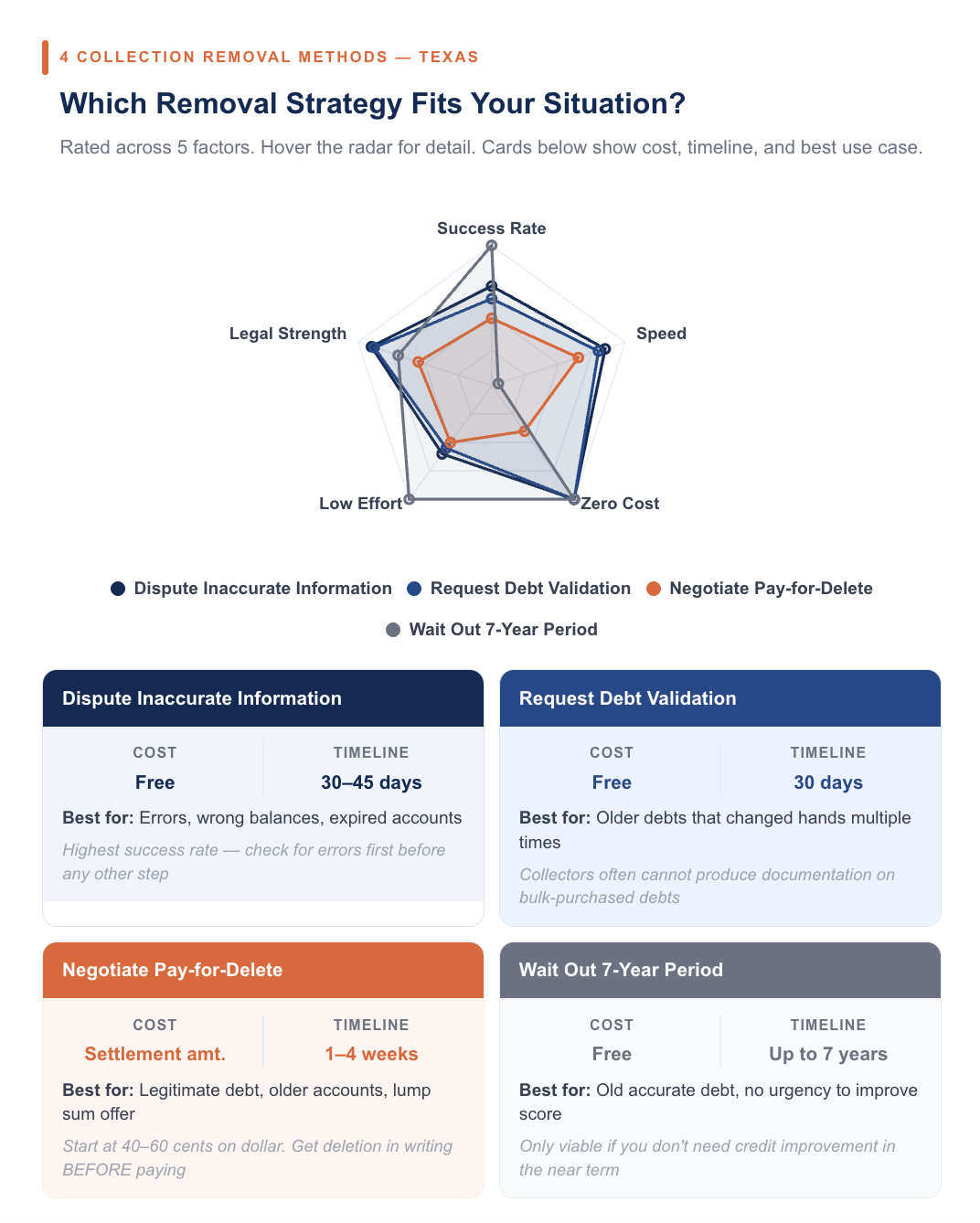

Four Ways to Remove Collections in Texas

There are four main methods I use and recommend when helping people remove collections from their credit reports in Texas.

1. Dispute Inaccurate Information

The first thing I always do is check the collection account for errors. You would be surprised how often collection accounts contain mistakes.

Common errors include:

- Wrong account balance

- Incorrect date of first delinquency

- Account listed more than once

- Debt that belongs to someone else

- Collection that is past the seven-year reporting limit

If you find any errors, you have the right to dispute them under the Fair Credit Reporting Act (FCRA). Send a written dispute letter to Equifax, Experian, and TransUnion. Each bureau has 30 days to investigate. If they cannot verify the information, they must delete it.

2. Request Debt Validation

When a collector contacts you, you have the right to request a debt validation letter within 30 days. This requires the collector to prove that the debt is yours, that the amount is correct, and that they have the legal right to collect it.

Many collection agencies buy debt in bulk and do not have proper documentation. If they cannot validate the debt, they must stop collection activity and the account may be removed from your credit report.

This method works especially well with older debts that have changed hands multiple times.

3. Negotiate a Pay-for-Delete Agreement

A pay-for-delete agreement is when you offer to pay the debt (in full or as a settlement) in exchange for the collector removing the account from your credit report entirely.

This is not guaranteed. Collectors are not legally required to agree to it. But many do, especially on older debts or when you offer a lump sum settlement.

Here is how I approach it:

- Always get the agreement in writing before you pay anything

- Start by offering 40 to 60 cents on the dollar for older debts

- Be firm about requiring full deletion as a condition of payment

- Never make a payment without a signed written agreement

Keep in mind that paying a collection without a pay-for-delete agreement will mark the account as "paid collection." That is slightly better for lenders to see, but the collection still stays on your report and continues to hurt your score.

4. Wait Out the Reporting Period

If the collection is accurate, you cannot be forced to pay it, and if you do not want to negotiate, you can simply wait. Collections fall off your credit report automatically after seven years from the date of the original missed payment.

As the collection ages, its impact on your score gradually decreases. A collection that is five years old hurts your score much less than one that is six months old.

I only recommend this approach if the debt is old and the damage is already limited. If you need to improve your credit soon, one of the other three methods will work faster.

What Happens If You Ignore a Collection in Texas

I want to be honest with you here. Ignoring a collection is not always the wrong move, but you need to understand the risks first.

If the debt is within the four-year Texas statute of limitations, the collector can still sue you in court. If they win a judgment, they can:

- Place a lien on property you own (excluding your primary home)

- Levy your bank account

- Report the judgment to the credit bureaus, which makes things worse

Once the four-year window has passed, a collector cannot successfully sue you in a Texas court. At that point, you have more freedom to negotiate or simply wait out the seven-year reporting period.

Never make a partial payment on an old debt without checking the statute of limitations first. In some cases, making any payment can restart the clock and give the collector the right to sue you again.

How to Check If a Debt Is Past the Statute of Limitations in Texas

To check whether a debt is past the four-year Texas statute of limitations, I look at two dates:

- The date of my last payment on the account

- The date the account first became delinquent (also called the date of first delinquency)

The statute of limitations clock usually starts from the date of last payment or last activity. Your credit report will show the date of first delinquency, which tells you when the seven-year reporting period started.

If more than four years have passed since either of those dates, a collector cannot take you to court in Texas. If more than seven years have passed, the collection should not appear on your credit report at all.

How Collections Affect Your Credit Score

Collections are one of the most damaging items that can appear on a credit report. Here is a quick look at how they affect your score:

Situation | Estimated Score Impact |

| New collection added | Minus 50 to 100 points |

| Collection under 2 years old | Very high negative impact |

| Collection 2 to 4 years old | Moderate negative impact |

| Collection 4 to 6 years old | Lower negative impact |

| Collection removed entirely | Score recovery of 30 to 100 points |

| Paid collection (no deletion) | Small improvement, still negative |

Removing a collection entirely always produces a better result than simply paying it without a deletion agreement.

Should I Hire a Professional to Remove Collections in Texas?

For simple cases with one or two collections, I think most people can handle disputes on their own. The process is straightforward if the collection contains errors or cannot be verified.

For more complex situations, especially when you have multiple collections, charge-offs, or a combination of negative items, professional help is worth considering. If you are also working on broader issues beyond just collections, connecting with a trusted credit repair service that understands Texas consumer law can speed things up significantly.

If you are based in the Houston area, this guide pairs well with the detailed breakdown of local options in our credit repair Houston resource, which covers full-service providers, costs, and how to compare your choices.

Key Takeaways

Here is a quick summary of everything I covered:

- Texas gives you four years before a collector can sue you, which is stronger leverage than many other states offer

- The Texas Debt Collection Act adds a second layer of consumer protection on top of federal law

- Texas protects your wages and primary home from most creditor judgments

- You have four main removal strategies: dispute errors, request debt validation, negotiate pay-for-delete, or wait out the reporting period

- Never pay an old debt without first checking the statute of limitations

- Always get any pay-for-delete agreement in writing before sending payment

- Removing a collection entirely is always better than paying without a deletion agreement

Frequently Asked Questions

Can a collection agency sue me for an old debt in Texas?

Only if the debt is within the four-year statute of limitations. Once four years have passed from your last payment or the date of delinquency, a collector cannot win a lawsuit against you in Texas court.

Does paying a collection remove it from my credit report?

Not automatically. Paying a collection marks it as "paid" but it still stays on your report for seven years. To get it removed, you need to negotiate a written pay-for-delete agreement before you pay.

How do I dispute a collection in Texas?

Send a written dispute letter directly to the credit bureau reporting the error (Equifax, Experian, or TransUnion). Clearly explain what is inaccurate and include any supporting documents. The bureau has 30 days to investigate and must delete the item if it cannot be verified.

Can medical debt be removed from my credit report in Texas?

Yes. Medical debt follows the same rules as other collection accounts. In addition, as of 2023, paid medical collections under $500 were removed from credit reports under new rules introduced by the major bureaus. Unpaid medical debt under $500 was also removed. This change benefits many Texas residents significantly.

What is the difference between a collection and a charge-off?

A charge-off is when your original creditor writes your debt off as a loss, usually after 180 days of non-payment. A collection is when that debt is sold to or assigned to a third-party collector. Both appear as separate negative items on your credit report and both need to be addressed to improve your score.