How do you remove collections without paying in Columbus, Ohio?

Most people assume you have to pay off collections to get them off your credit report. That’s what collection agencies want you to believe.

But based on what we’ve seen working with clients in Columbus, that’s not always how it works.

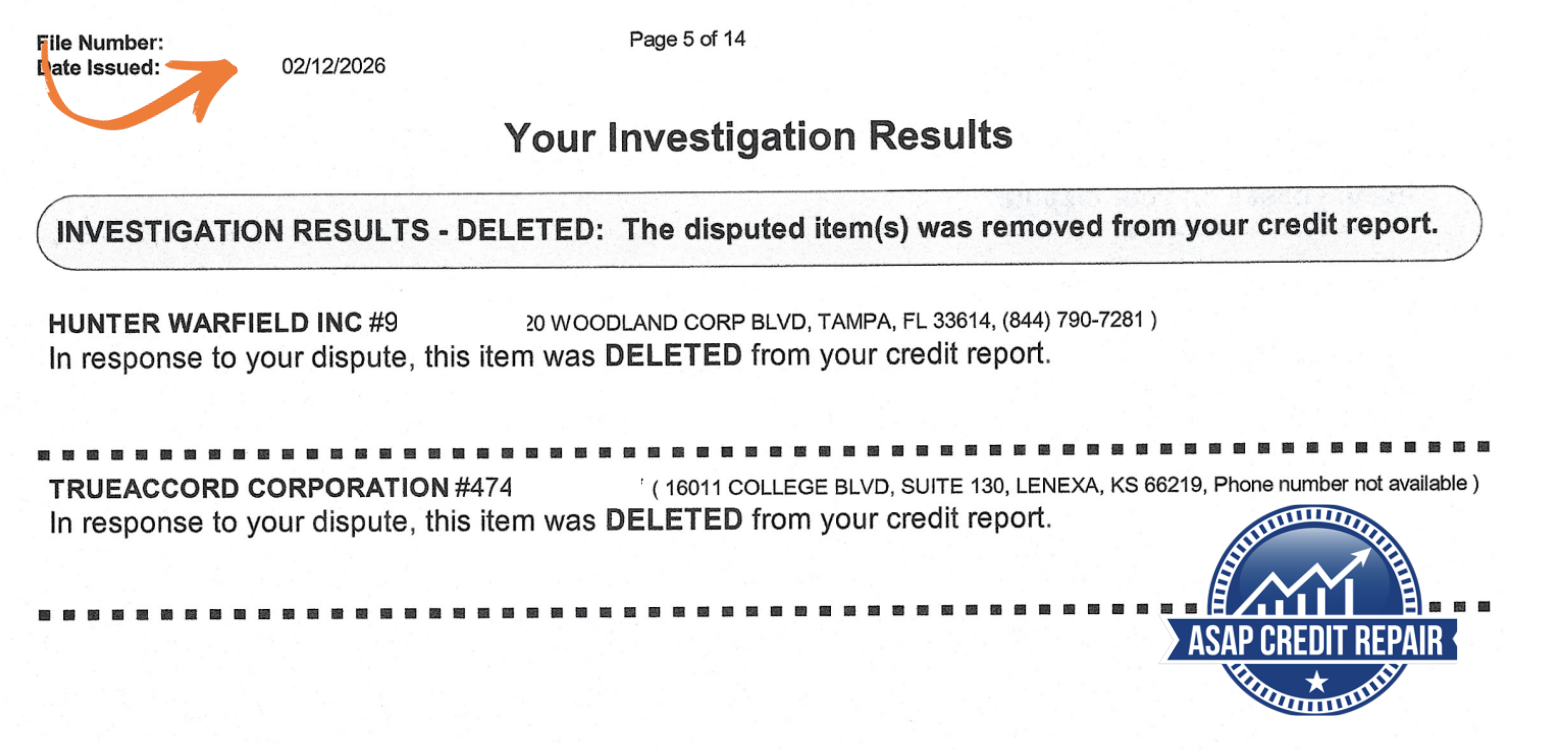

We’ve reviewed credit reports where collection accounts were lowering scores by 60 to 100+ points, even when the debt was years old. In many cases, those accounts contained reporting issues, incomplete information, or couldn’t be properly verified through the credit bureaus. When challenged correctly, some of these accounts were removed without a single payment being made.

Here’s the key insight.

Collection agencies are required to report accurate and verifiable information. If they can’t validate the account, it doesn’t have to stay on your credit report.

In this guide, you’ll learn how to remove collections without paying, when this strategy actually works, and the exact steps you can take to improve your credit in Columbus without wasting money on the wrong approach.

By Joe Mahlow | Updated: March 2026 | Columbus, OH

- Columbus residents carry an average credit score of 637, squarely in the "fair" range

- You can remove collections from your credit report without paying in several legal ways

- Ohio's FDCPA and OCSPA consumer protections are among the strongest in the country

- The Ohio statute of limitations on most debts is 6 years. After that, collectors can't sue

- Credit bureaus must investigate disputes within 30 days under federal law (FCRA)

- Debt validation, goodwill deletion, and dispute letters are all payment-free removal options

If you live in Columbus, Ohio and you're staring at a collection account on your credit report, you're not alone and you're not out of options. A collection entry can cut your credit score by 50 to 110 points, block you from getting approved for a home loan, car financing, or even an apartment in the Short North. But here's what most people don't realize: you do not always have to pay a collection account to get it removed from your credit report.

This guide covers every legitimate, legal method Columbus residents can use to remove collections without paying, including your specific rights under Ohio law, how to write effective dispute letters, and when a collection account may already be unenforceable against you.

What Is a Collection Account and Why Is It on Your Credit Report?

A collection account appears on your credit report when an original creditor, such as a hospital, credit card company, or utility provider, that gives up trying to collect directly and sells or transfers the debt to a third-party collection agency. That agency then has the right to report the account to the three major credit bureaus: Equifax, Experian, and TransUnion.

Under the Fair Credit Reporting Act (FCRA), a collection account can remain on your credit report for up to seven years from the date of the original delinquency, not from when it was sold to collections. This is an important distinction because many Columbus consumers mistakenly believe the seven-year clock resets every time the debt changes hands. It does not.

Can You Really Remove Collections Without Paying in Columbus, OH?

Yes, and there are multiple legitimate, legal strategies to do it. Whether a collection is removable without payment depends on three factors: how old the debt is, whether the information on your report is 100% accurate, and whether the collector followed proper legal procedures when reporting it. Columbus residents are protected by both federal law (FDCPA, FCRA) and Ohio state law (OCSPA), giving you several angles to pursue.

Method 1: Dispute Inaccurate or Unverifiable Information

The most powerful and most underused tool available to Columbus consumers is the credit dispute. Under the FCRA, if any information in a collection account on your report is inaccurate, incomplete, or unverifiable, you have the right to dispute it, and the credit bureau must investigate and respond within 30 days.

What counts as inaccurate? More than you might think. Common errors include the wrong original creditor name, an incorrect balance, a wrong date of first delinquency (which affects when the 7-year clock expires), duplicate entries for the same debt, collection accounts that belong to someone else with a similar name, and debts discharged in bankruptcy that still appear active.

Pull All Three Credit Reports

Go to AnnualCreditReport.com and download your Equifax, Experian, and TransUnion reports. The same collection may appear differently across all three bureaus, and errors on one don't automatically appear on the others.

Document Every Error You Find

Note the collection agency name, account number, reported balance, date opened, and date of first delinquency. Cross-reference these against any original bills, statements, or notices you have from the original creditor.

Write a Formal Dispute Letter

Write directly to each credit bureau that shows the error. State what is wrong, cite the FCRA section 611, and request investigation and removal. Send via certified mail with return receipt so you have proof of delivery and date.

Wait for the 30-Day Investigation Window

The bureau notifies the collection agency, which must verify the information. If the collector cannot verify it, or fails to respond, the bureau must remove the entry. Many smaller Columbus debt buyers lack proper documentation.

Escalate If Needed

If your dispute is rejected and you believe the decision was wrong, file a complaint with the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov and with Ohio's Attorney General at ohioattorneygeneral.gov. Both have teeth.

Method 2: Send a Debt Validation Letter

Under the FDCPA, if a debt collector contacts you, you have the right to send a debt validation letter within 30 days demanding proof that the debt is yours and that they have the legal right to collect it. If they cannot provide valid documentation, they must cease all collection activity, and you can request removal of the entry from your credit report.

Debt validation is especially powerful in Columbus because many collection accounts have been sold multiple times. By the third or fourth owner, original documentation, including signed agreements, itemized billing records, and chain-of-title paperwork, is often lost or incomplete. A firm validation demand frequently results in the collector going silent or voluntarily removing the account rather than risk an FDCPA complaint.

For a closer look at how charge-offs relate to collection entries and what additional removal steps apply, see our guide on deleting charge-offs from your credit report. The dispute logic applies equally for Columbus consumers.

Method 3: Check Ohio's Statute of Limitations

Ohio law sets a clear limit on how long a creditor or collector can take legal action against you for an unpaid debt. Once that window closes, the debt is considered "time-barred," meaning collectors can no longer sue you to collect it. While a time-barred debt can still technically appear on your credit report, it gives you powerful leverage to negotiate removal or defend against any collection pressure.

| Debt Type | Ohio Statute of Limitations | Still Reportable? | Can Collector Sue? |

|---|---|---|---|

| Credit Card Debt | 6 years | Up to 7 yrs | No (after 6 yrs) |

| Medical Debt | 4 years | Up to 7 yrs | No (after 4 yrs) |

| Written Contract | 8 years | Up to 7 yrs | No (after 8 yrs) |

| Oral Contract | 6 years | Up to 7 yrs | No (after 6 yrs) |

| Auto Loan Deficiency | 6 years | Up to 7 yrs | No (after 6 yrs) |

| Court Judgment | 10 years (renewable) | 7 yrs from judgment | Yes (if renewed) |

Whether your collection is inaccurate, unverifiable, or already past Ohio's statute of limitations. There are options. Our team has helped thousands of residents identify and remove entries they didn't have to pay a cent on.

Get Your Free Credit Analysis →Method 4: Send a Goodwill Deletion Letter

A goodwill deletion letter is a direct appeal to the collection agency or original creditor asking them to remove a negative item as a gesture of goodwill, typically because the the debt has been paid or because your financial hardship was temporary and you have since demonstrated responsible behavior.

This method works best when the account is paid or when you had an isolated financial hardship such as a job loss, medical emergency, or family crisis, that caused the missed payments. You are not disputing accuracy. You are asking the creditor to exercise discretion. While this strategy has a lower success rate than disputes or validation letters, it costs nothing and takes minimal effort. For original creditors with whom you have an ongoing relationship, goodwill letters sometimes succeed where disputes cannot.

To understand how this approach compares to negotiated removal strategies, our guide on pay-for-delete success rates walks through the scenarios where each method performs best.

Method 5: Identify FDCPA or FCRA Violations

Sometimes the fastest path to removal is not disputing the debt itself. It is identifying procedural violations by the collector. Both the FDCPA and FCRA impose strict rules on how collectors must operate, and violations give you leverage that many collectors would rather settle quietly than defend in court.

Common FDCPA Violations That May Force Removal

- Calling before 8 a.m. or after 9 p.m. Columbus local time

- Contacting you at work after you've told them not to

- Threatening legal action on a time-barred debt

- Failing to include the required debt validation notice in their first communication

- Using abusive, obscene, or threatening language

- Reporting a debt they know to be false or disputed without noting it as disputed

- Attempting to collect a debt discharged in bankruptcy

If you identify a violation, you can sue the collector in federal court for up to $1,000 in statutory damages plus actual damages and attorney fees. More practically, threatening a credible FDCPA lawsuit often results in the collector agreeing to delete the tradeline entirely in exchange for a release, at no cost to you.

How to File a Complaint in Columbus, Ohio

Columbus residents can file FDCPA complaints with the FTC at reportfraud.ftc.gov, with the CFPB at consumerfinance.gov/complaint, and with the Ohio Attorney General's Consumer Protection Section at ohioattorneygeneral.gov. The OCSPA violation complaints go directly to the Ohio AG's office and can result in enforcement action beyond what federal law provides alone.

Method 6: Wait Out the 7-Year Reporting Clock

This is the least proactive strategy, but for some Columbus residents it is the most realistic. Under the FCRA, most negative information, including collection accounts, must be removed from your credit report automatically after seven years from the date of original delinquency. No payment, no letter, no dispute required.

If a collection is five or six years old and you have newer negative items that are more urgent to address, waiting out the remaining time on older collections while focusing your energy on fresher damage may be the most efficient use of your credit repair efforts. Additionally, if a collection is approaching its seven-year expiration and a collector is attempting to re-age the account (report a false, more recent delinquency date to extend its shelf life), that is a clear FCRA violation you can dispute immediately.

How Does Removing a Collection Impact Your Columbus Credit Score?

The impact of removing a collection account depends on whether you have other negative items, how old the collection is, and which credit scoring model is being used. For Columbus residents whose primary goal is qualifying for a mortgage, auto loan, or apartment rental, even a moderate score increase from a single removal can be the difference between approval and rejection.

Columbus, OH vs. Other Cities: How Does Your Credit Situation Compare?

Columbus residents deal with a credit landscape shaped by rising delinquency rates, a manufacturing-to-tech job market transition, and a population growth rate that outpaces wage growth in many neighborhoods. If you're navigating collections in Columbus, the strategies are the same ones consumers use across major metros, but your Ohio-specific legal protections are notably stronger than in many other states.

For comparison, we've documented similar removal strategies for residents in other cities. If you have out-of-state collections or are curious how the process differs elsewhere, our guide on removing collections without paying in Albuquerque walks through a similar framework with New Mexico-specific consumer law context.

Navigating debt validation letters, FDCPA complaints, and bureau disputes simultaneously is time-consuming and easy to get wrong. Here's what our team handles directly on your behalf:

- Full three-bureau audit to identify every inaccurate, outdated, or unverifiable collection entry

- Custom dispute letters citing Ohio OCSPA and federal FCRA protections

- Debt validation requests sent to collection agencies with legal follow-up

- Identification of FDCPA and FCRA violations that could force removal

- Re-aging detection to catch illegal attempts to extend a collection's shelf life

- Ongoing credit score monitoring and guidance for post-removal rebuilding

Columbus residents have a higher-than-average number of medical and utility collections on file. Many of these contain errors that qualify for removal, often without any payment required.

Start My Free Credit Review →What You Should Never Do When Dealing With Collectors in Columbus

- Don't make a partial payment on an old debt. Even $1 can restart Ohio's 6-year statute of limitations, giving collectors renewed legal footing.

- Don't verbally acknowledge you owe the debt. On a recorded call, this can count as acknowledgment under Ohio law.

- Don't ignore lawsuits. If a collector files a lawsuit in Franklin County Municipal Court or the Franklin County Court of Common Pleas, failing to respond results in a default judgment against you, which is far harder to remove.

- Don't dispute accurate, recent collections without a strategy. Disputing a collection that the collector can easily verify and that has real documentation may result in the entry being verified and left in place, with fewer future dispute options.

- Don't accept verbal promises from collectors. Always get any agreement to remove a tradeline in writing before making any payment.

References and Further Reading

The information in this guide is grounded in federal and Ohio-specific consumer law. For direct access to the source materials, the following high-authority references are recommended:

- Consumer Financial Protection Bureau (CFPB): Collections & Credit Reports: The federal regulator's official guidance on how collection accounts work, your dispute rights, and how to file complaints against collectors.

- Federal Trade Commission (FTC): Fair Debt Collection Practices Act (Full Text): The complete statutory text of the FDCPA, including all consumer rights, collector prohibitions, and enforcement provisions that apply to Columbus residents.

- Upsolve: Ohio Debt Collection Laws: A comprehensive, attorney-reviewed breakdown of both the FDCPA and Ohio Consumer Sales Practices Act protections specific to Ohio residents, updated March 2026.

Frequently Asked Questions

Can I remove a collection from my credit report without paying it in Ohio?

Yes. Columbus residents can remove collection accounts without paying through several legal methods: disputing inaccurate or unverifiable information, sending a debt validation letter, leveraging expired statutes of limitations, identifying FDCPA or FCRA violations, or sending a goodwill deletion request. Automatic removal also occurs after seven years from the original delinquency date under the FCRA.

How long does a collection stay on my credit report in Columbus, OH?

Under federal law (FCRA), a collection account can remain on your credit report for up to seven years from the date of the original delinquency, regardless of how many times the debt has been sold or how many collection agencies have held it. The seven-year clock does not restart when a new collector takes over the account.

What is Ohio's statute of limitations on debt collection?

Ohio's statute of limitations is six years for most consumer debts, including credit card debt and oral contracts, and eight years for written contracts. Medical debt typically falls under a four-year limit. Once these periods expire, collectors can no longer sue you to collect, though the debt may still appear on your credit report until the seven-year FCRA limit passes.

Does paying off a collection account improve my credit score?

It depends on which scoring model is used. Older FICO models (8 and below) still weigh a paid collection negatively, meaning paying it may not increase your score much. Newer models like FICO 9 and VantageScore 3.0+ ignore paid collections entirely. If score improvement is your goal, negotiating a pay-for-delete agreement, where the collector agrees to remove the entry upon payment, which is more effective than simply paying and leaving the entry on your report.

What happens if I ignore a collection account in Columbus?

Ignoring a collection does not make it disappear. The entry will remain on your credit report for up to seven years, continuing to damage your score. If the debt is still within Ohio's statute of limitations, the collector can also sue you in Franklin County court. A default judgment, which results from not responding to a lawsuit, allows collectors to pursue wage garnishment and bank levies, which are far more difficult to resolve than the original collection.

Can a debt collector contact me at work in Ohio?

No. Under the FDCPA, debt collectors are prohibited from contacting you at work if you notify them, verbally or in writing, that your employer does not permit such calls. Ohio's OCSPA provides additional protections. If a collector continues to call your workplace after being told to stop, that is an FDCPA violation, and you can sue for damages or use the violation as leverage to negotiate removal of the collection from your credit report.

Is it worth hiring a credit repair company for collections in Columbus?

For consumers with multiple collection accounts, potential FDCPA violations, or complex dispute situations, professional credit repair can accelerate and strengthen the removal process significantly. A reputable firm knows which errors are most disputable, how to frame letters to maximize bureau response rates, and when escalation to regulatory complaints is warranted. For a single, straightforward dispute, the DIY approach is viable. For multiple entries or older debts with complicated histories, professional help typically produces faster and more complete results.