RMP LLC: Who Are They and Why Are They Calling Me?

by Joe Mahlow • Updated on Jul. 10, 2026

Quick Guide: Dealing with RMP LLC Debt Collection

Summary: RMP LLC is a legitimate debt collection agency that purchases charged-off debts. Often for a fraction of the original balance and seeks to collect the full amount. Some consumers report aggressive tactics, so it’s important to proceed with caution and protect your rights.

Know Who You’re Dealing With: Verify that the debt is truly yours and that RMP LLC has the legal right to collect.

Request Written Validation: Under the FDCPA, you have the right to request written proof of the debt within 30 days of first contact.

Check the Statute of Limitations: If the debt is too old, they may not be able to sue you for it—even though they can still request payment.

Document All Communications: Keep records of calls, letters, and emails in case of disputes.

Negotiate Strategically: If the debt is valid, you may be able to settle for less than the claimed amount, especially since they bought it at a discount.

Protect Your Credit: Make sure any settlement includes written terms for removing or updating negative credit reporting.

Key Takeaway: Don’t rush into payment. Verify, document, and negotiate from a position of knowledge to avoid overpaying and to protect your credit score.

Getting random calls from debt collectors? Yeah, it's annoying as hell. If you've been dodging calls from RMP LLC, you're probably wondering who they are and what they want from you.

I run a credit repair company and deal with RMP LLC cases almost daily. Here's what I've learned from helping over 65,000 clients handle these situations.

This isn't theory, it's real-world experience from someone who fights these battles every single day.

If you want to learn more about who is RMP LLC and why they are contacting you, then stay on this page.

What Is RMP LLC?

RMP LLC, also known as RMP Services LLC or Receivables Management Partners LLC, is a debt collection company based in Ohio. They specialize in purchasing charged-off debts from original creditors and then attempting to collect the full amount from consumers.

The company operates as a debt buyer, which according to Investopedia, means they purchase debts for pennies on the dollar and then try to collect the full amount.

For example, they might buy a $5,000 credit card debt for just $200, but they'll still try to collect the entire $5,000 from you.

Here are the key facts about RMP LLC:

Founded: 2010

Location: Medina, Ohio

Business Type: Third-party debt collector and debt buyer

Industries: Credit cards, medical bills, personal loans, retail accounts

Annual Revenue: Approximately $15-20 million (based on industry estimates)

Is RMP LLC Legit?

Yes, RMP LLC is a legitimate debt collection company. They're not a scam operation, but that doesn't mean you should take their word for everything. The company is registered with the Better Business Bureau and operates under federal debt collection laws.

However, being legitimate doesn't mean they always play fair. Like many debt collectors, they may use aggressive tactics to pressure you into paying. They're required to follow the Fair Debt Collection Practices Act (FDCPA), but violations do occur.

Key legitimacy indicators:

Registered business entity in Ohio

BBB listing (though with mixed reviews)

Subject to FDCPA regulations

Licensed in states where required

Who Does RMP LLC Collect For?

RMP LLC collects for major creditors and often owns the debts outright. In my experience, they handle debts from:

Common creditors:

Chase, Capital One, Discover credit cards

Hospitals and medical groups

Verizon, AT&T, T-Mobile

Utility companies

Personal loan companies

Store credit cards (Target, Best Buy, etc.)

Debt categories:

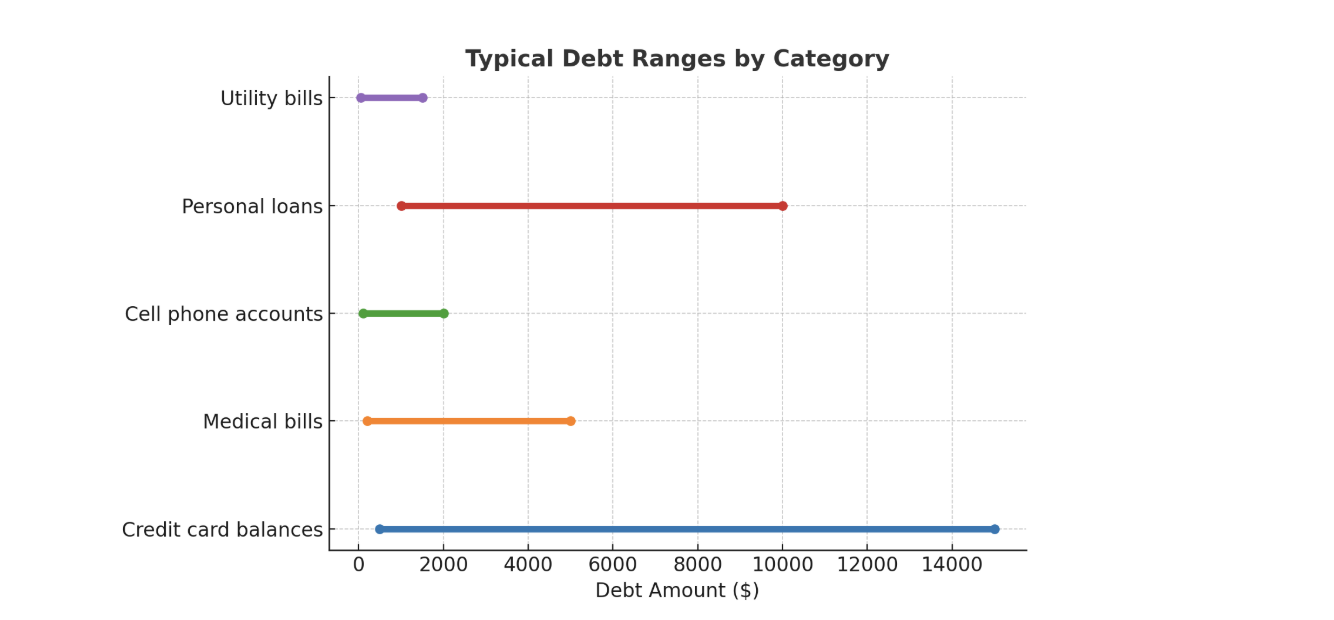

Credit card balances ($500-$15,000 typically)

Medical bills ($200-$5,000 range)

Cell phone accounts ($100-$2,000)

Personal loans ($1,000-$10,000)

Utility bills ($50-$1,500)

They usually get involved 6-18 months after you stop paying. Your original creditor has written off the debt and either hired RMP or sold it to them completely.

RMP LLC Phone Number and Contact Information

If you need to contact RMP LLC directly, here's their information:

Primary Contact:

Phone: (330) 723-7445

Address: 1040 N Court St, Medina, OH 44256

Business Hours: Monday-Friday, 8 AM - 5 PM EST

Website: Not publicly available

Important Note: If they're calling you from different numbers, this is common practice. Debt collectors often use multiple phone numbers and may even use local area codes to increase the chances you'll answer.

Other numbers reported by my clients:

(330) 725-xxxx series

(800) 854-xxxx series

Various local area codes

Why Is RMP LLC Calling Me?

RMP LLC is calling because they think you owe money on an old debt. It's that simple. Here's the typical timeline I see with my clients:

Account gets "charged off" (written off as bad debt)

Creditor sells debt to RMP LLC or hires them to collect

RMP starts calling you 1-3 months later

Real Example 1: Credit Card Scenario

Maria, one of my clients, had a $4,200 Chase credit card balance. She lost her job and couldn't pay for 7 months. Chase charged off the debt and sold it to RMP LLC for roughly $420 (10 cents on the dollar).

RMP started calling Maria demanding the full $4,200 plus $800 in accumulated fees and interest. They bought a $420 debt but wanted $5,000 from her. Maria ignored the calls for 6 months until her credit score dropped another 40 points. That's when she hired me.

Result: We negotiated a $1,500 settlement and got the account deleted from her credit report.

Real Example 2: Medical Bill Collection

James had knee surgery and owed $1,800 after insurance. He thought his insurance would cover more and never paid. After 14 months, the hospital sold the debt to RMP LLC.

RMP called James daily for 3 weeks demanding $1,800 plus $300 in collection fees. James panicked and almost paid the full amount until he contacted my office.

Result: We validated the debt, found the hospital never properly billed his secondary insurance, and got the entire debt removed.

RMP LLC Collections: What to Expect

When RMP LLC collections contacts you, here's what typically happens:

Initial Contact:

Phone calls (often multiple per day)

Written validation notice within 5 days

Attempts to get you to acknowledge the debt

Payment arrangement offers

Collection Tactics:

Frequent phone calls (legally limited to once per day per number)

Letters and notices

Settlement offers (often 40-60% of the balance)

Threats of legal action (though lawsuits are less common for smaller debts)

What They Cannot Do:

Call before 8 AM or after 9 PM

Harass or threaten you

Call your workplace if you've told them not to

Discuss your debt with third parties

Lie about the consequences of not paying

How to Deal with RMP LLC

As a credit repair professional, I recommend this approach when dealing with RMP LLC:

Step 1: Don't Ignore Them

Ignoring debt collectors rarely makes them go away. They may eventually sue or continue reporting negative information to credit bureaus.

Step 2: Request Debt Validation

Within 30 days of their first contact, send a debt validation letter requesting:

Proof they own the debt

Documentation of the original debt amount

Proof of your obligation to pay

Contact information for the original creditor

Need help verifying a debt?

ASAP Credit Repair can help you confirm whether a debt is valid and guide you through the dispute process.

Settlements are often reported as "settled for less than full balance"

Legal Considerations and Statute of Limitations

The statute of limitations affects whether RMP LLC can successfully sue you:

Typical Timeframes by State:

3 years: Most states for credit cards and open accounts

4 years: Several states including California and Florida

6 years: Some states for written contracts

10 years: A few states like Rhode Island

Important: Making a payment or acknowledging the debt can reset the statute of limitations. Never agree to pay anything without understanding your full legal position.

Red Flags: When RMP LLC Might Be Violating the Law

Watch for these potential FDCPA violations:

Illegal Practices:

Calling outside allowed hours (before 8 AM or after 9 PM)

Calling repeatedly throughout the day

Threatening arrest or wage garnishment without legal authority

Discussing your debt with family members or coworkers

Misrepresenting the amount owed or consequences of non-payment

Continuing to call after you've requested communication in writing only

What to Do About Violations:

Document everything (dates, times, what was said)

File complaints with CFPB and your state attorney general

Consider consulting with a consumer law attorney

You may be entitled to up to $1,000 in damages plus attorney fees

Settlement Strategies That Could Work

Based on my experience helping clients settle with RMP LLC and similar collectors:

Best Settlement Practices:

Start low (20-30% of the balance)

Get everything in writing before paying

Request "pay for delete" (removal from credit reports)

Use certified mail for all correspondence

Never provide direct bank account access

Typical Settlement Range:

Fresh accounts (under 1 year old): 60-80%

Older accounts (1-3 years): 40-60%

Very old accounts (3+ years): 20-40%

Accounts near statute of limitations expiration: 10-30%

Protecting Yourself from Future Collection Issues

To avoid future problems with debt collectors like RMP LLC:

Prevention Strategies:

Keep track of all debts, even small ones

Set up automatic payments for minimum amounts

Communicate with original creditors before accounts charge off

Monitor your credit reports regularly (use annualcreditreport.com)

Keep detailed records of all payments and correspondence

Avoid debt settlement companies that charge upfront fees

When to Seek Professional Help

Consider hiring a professional if:

You Should Get Help If:

The debt amount is over $5,000

You're facing potential legal action

You've experienced FDCPA violations

You're unsure about the debt's validity

You need help negotiating settlements

Your credit report has multiple collection accounts

Want a gold standard credit repair? We got you!

Final Thoughts on Dealing with RMP LLC

RMP LLC is a legitimate debt collector, but that doesn't mean you should pay without question. As someone who helps people navigate these situations daily, I've seen too many clients pay debts they didn't owe or settle for more than necessary because they didn't understand their rights.

Remember these key points:

Always validate the debt before paying

Negotiate settlements in writing

Know your rights under the FDCPA

Consider the statute of limitations

Get professional help for complex situations

The biggest mistake I see people make? Paying without validating or negotiating. The second biggest? Ignoring the problem completely.

The most important thing is to take action. Whether that means disputing an invalid debt, negotiating a settlement, or seeking legal help for violations, doing nothing is rarely the best strategy. Your credit score and financial future are worth protecting.

About the Author

As a credit repair company owner with over 10 years of experience, I've helped thousands of clients deal with debt collectors. This article is based on our experience handling these situations daily, combined with thorough research of debt collection laws and industry practices.

Disclaimer: This article is for informational purposes only and is not legal advice. Any mention of companies or organizations is for reference purposes only and does not imply endorsement, affiliation, or that they are involved in the situation described. Always verify information with the relevant company or a qualified professional before taking action.

Related Articles — ASAP Credit Repair

ASAP

Related Reading

Helpful articles related to debt collectors, suspicious numbers, and what you can do next.

Who is Torres Credit Services?

Learn how Torres Credit Services operates, when to verify the debt, and steps to protect your rights under the FDCPA.