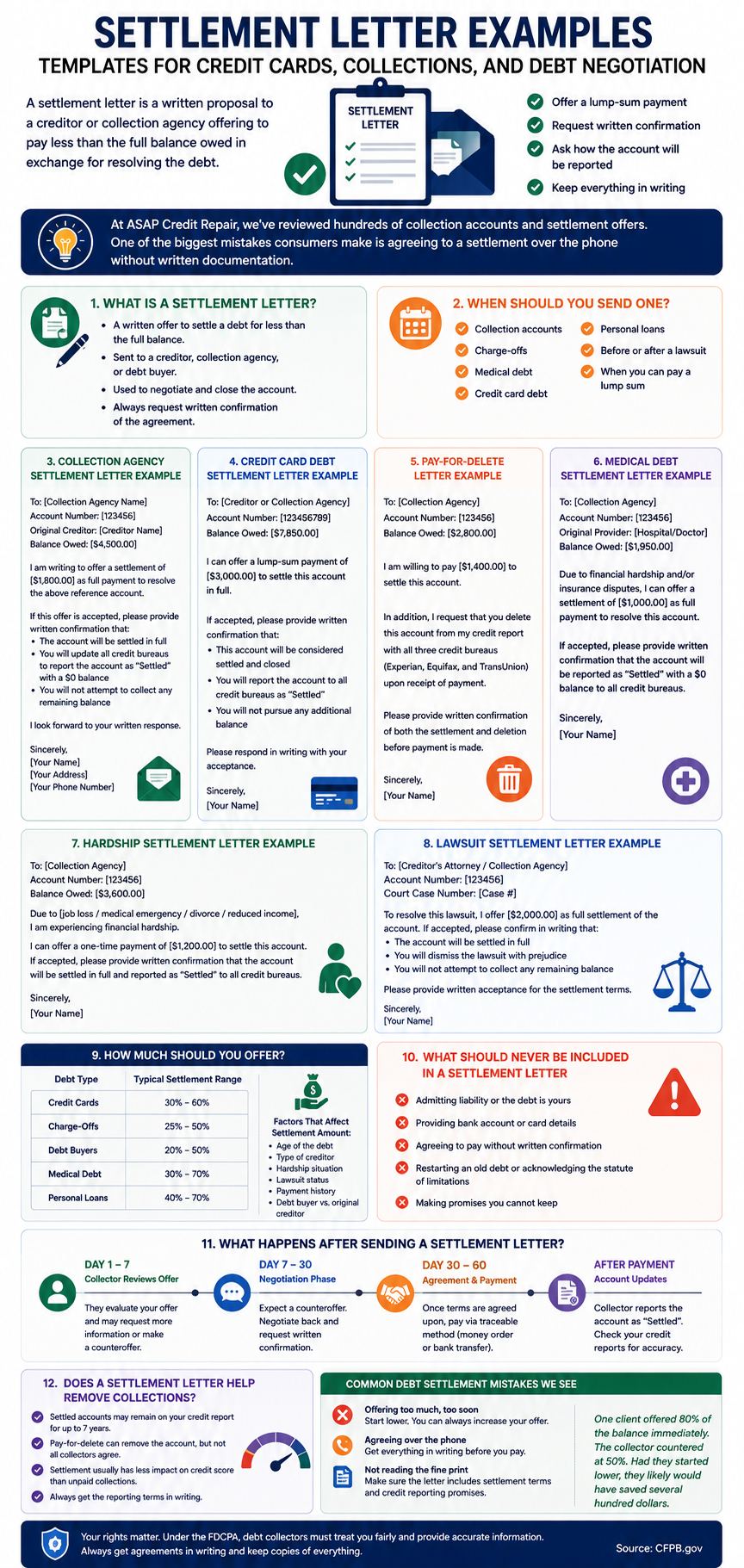

If you are looking for settlement letter examples or template for your debt, then you are on the right place.

What Is a Settlement Letter?

A settlement letter is a written proposal to a creditor or debt collector offering to pay less than the full balance in exchange for resolving the account. It is sent when you want to negotiate a payoff amount, and it creates a paper trail. Without a written offer and written confirmation, no settlement agreement exists that you can enforce.

Settlement letters work because creditors and debt collectors know that collecting nothing is worse than collecting part of the balance. When an account goes delinquent long enough, the original creditor may charge it off and sell it to a debt buyer like Midland Credit Management, LVNV Funding, or Portfolio Recovery Associates for 2 to 5 cents on the dollar. That debt buyer now owns the balance and will settle for far less than what you owed the original creditor.

The letter does not bind the collector. It opens a negotiation. The collector can accept, reject, or counter your offer. That is why the structure and the amount you propose both matter.

A settlement letter must include four things to be effective.

- Clear identification of the account by number and original creditor name

- A specific dollar amount you are offering, not a percentage

- A request for written confirmation before any payment is made

- A request for how the account will be reported to Experian, Equifax, and TransUnion after settlement

As a debt negotiation specialist reviewing hundreds of settlement outcomes would confirm, the single most common mistake is sending payment before receiving a signed written agreement, because the FDCPA does not prevent a collector from cashing a check and then selling the remainder to another agency unless the written agreement explicitly prohibits it.

When Should You Send a Debt Settlement Letter?

Send a settlement letter when the debt is already in collections or charged off, when you have a lump sum available to offer, and when you want to resolve the account for less than the full balance. Settlement letters are not for current accounts in good standing. They are for accounts that are already damaged.

| Situation | Right Time to Send | Leverage Level |

|---|---|---|

| Collection account (third-party collector) | Any time. Debt buyer paid pennies for the account. | High |

| Charge-off still with original creditor | 120 to 180 days past due, before it is sold | Moderate |

| Medical debt | Before it reaches a collector. Hospitals have more flexibility. | High |

| Credit card debt | After charge-off or once with a debt buyer | Moderate |

| Debt past the statute of limitations | Immediately. Time-barred debt is your strongest leverage. | Highest |

| Active lawsuit filed against you | Before default judgment. Time is critical. | Lower — act fast |

| Personal loan at a bank | After significant delinquency, not before 90 days past due | Moderate |

From the perspective of a consumer debt attorney advising clients before trial, the best time to send a settlement letter in a lawsuit situation is the moment the complaint is served, not after the deadline to answer has passed, because a default judgment eliminates most of your negotiating position and gives the collector legal tools to garnish wages and freeze accounts without further court action.

Settlement Letter Example for a Collection Agency

A collection agency settlement letter identifies the account, states the lump-sum offer, requests written confirmation before payment, and asks for specific credit bureau reporting language. Send via certified mail, return receipt requested. Keep a copy for your records.

Credit Card Debt Settlement Letter Example

Credit card settlement letters typically offer between 30 and 50 percent of the outstanding balance. Major card issuers accept fewer settlements than debt buyers. If the account was sold to a collector, the negotiating range opens significantly. Start your offer at 25 to 30 percent and expect a counter around 40 to 50 percent.

| Debt Type | Starting Offer | Typical Accepted Range | Notes |

|---|---|---|---|

| Credit Cards — Original Creditor | 35% | 40–60% | Harder to settle before charge-off |

| Credit Cards — Debt Buyer | 20% | 25–45% | Buyer paid 2–5 cents on dollar. Most room to negotiate. |

| Charge-Offs | 20% | 25–50% | Older charge-offs settle lower |

| Medical Debt | 25% | 30–60% | Hospitals have flexibility pre-collection |

| Personal Loans | 35% | 40–65% | Secured collateral reduces bank flexibility |

| Lawsuit Debt | 45% | 50–75% | Collector has more leverage post-filing |

Pay-for-Delete Settlement Letter Example

A pay-for-delete letter requests that the collector remove the tradeline from your credit report entirely, as a condition of payment. Major creditors and large debt buyers rarely agree to pay-for-delete. Smaller collection agencies and some medical debt collectors sometimes do. Any promise of deletion must be in writing before payment is sent.

Pay-for-delete used to be common. It became less so after the three credit bureaus updated their data furnisher agreements to discourage it. But the practice is not illegal. Collectors can still agree to delete a tradeline if they choose.

The accounts most likely to accept pay-for-delete are small local collection agencies, medical billing collectors, and accounts where the balance is under $1,000. Large national debt buyers like Portfolio Recovery Associates or LVNV Funding rarely agree to deletion because their data furnisher contracts with the bureaus restrict it.

Medical Debt Settlement Letter Example

Medical debt has more settlement flexibility than most debt types. Hospitals and medical billing offices often accept 30 to 50 percent of the balance, especially before the account goes to a third-party collector. In 2025, the three major credit bureaus removed most medical debts under $500 from credit reports, and new CFPB rules proposed removing all medical debt from credit reports entirely. These changes affect how you negotiate.

Negotiate with the hospital or medical provider directly before the debt reaches a collection agency. Once a medical bill is sold to a third-party collector, your point of contact changes and the flexibility that hospitals have reduces. Hospitals also have financial hardship programs, charity care funds, and income-based discount programs that collection agencies do not offer.

Hardship Settlement Letter Example

A hardship settlement letter pairs your financial situation with the settlement offer. It explains why you cannot pay the full balance and why accepting your offer now is better than pursuing the full amount later. Creditors respond better to documented hardship than to unexplained low offers. Keep the hardship explanation factual and brief.

Common hardship reasons that collectors respond to include job loss, divorce, medical emergency, disability, death of an income-earning spouse, and reduced hours. The goal is not to generate sympathy. The goal is to make it logical for the collector to accept less now rather than risk collecting nothing later.

Lawsuit Settlement Letter Example

When a collector has already filed a lawsuit, a settlement letter must also address dismissal of the case. Settling the debt without getting written dismissal language leaves the lawsuit active. You need both a signed settlement agreement and a written commitment to file a dismissal with prejudice with the court.

Collection Account on Your Report After Settlement? It May Be Removable.

A settled account that was reported with wrong dates, incorrect balances, or inaccurate status can be disputed and removed under the Fair Credit Reporting Act, separate from the settlement itself. A free 3-bureau audit shows every item on your report and which entries do not meet FCRA reporting standards.

Get My Free 3-Bureau Credit Audit → Secure · 2 minutes · No credit card requiredHow Much Should You Offer in a Settlement Letter?

Most debt settlements are negotiated between 20 and 60 percent of the outstanding balance, depending on the age of the debt, the creditor type, and whether the account has been sold to a debt buyer. Start your first offer below your maximum. Expect a counteroffer. The collector's first counter is rarely their final position.

| Debt Type | Starting Offer | Typical Settlement Range |

|---|---|---|

| Credit Cards — Original Creditor | 30% | 40–60% |

| Credit Cards — Debt Buyer | 20% | 25–45% |

| Charge-Offs | 20% | 25–50% |

| Medical Debt | 25% | 30–60% |

| Personal Loans | 35% | 40–65% |

| Lawsuit Debt | 45% | 50–75% |

| Debt Past Statute of Limitations | 10–15% | 15–30% |

Three factors shift where in the range a specific settlement lands. First is how old the debt is. Older accounts have less documentation and are closer to or past the statute of limitations, giving the collector less leverage. Second is whether the account is with the original creditor or a debt buyer. Debt buyers paid almost nothing for the account and have the most flexibility. Third is whether you can pay the full settlement immediately. Lump-sum offers settle lower than payment plans because collectors prefer certainty over monthly risk.

From the perspective of a bankruptcy attorney reviewing a client's accounts before recommending settlement versus bankruptcy, the statute of limitations on each account is the first number calculated, because a time-barred debt that a collector cannot sue on in court is worth significantly less than an account still within the legal collection window, and that difference in value translates directly into a lower acceptable settlement percentage.

What Should Never Be Included in a Settlement Letter?

Six things in a settlement letter can destroy your legal position, restart the statute of limitations clock, or hand the collector evidence they will use against you in court. Avoid every one of them.

Phrases like "I owe this debt" or "I know I owe this" can be used as admissions in court. In some states, a written acknowledgment of a debt restarts the statute of limitations. Always include the phrase "I do not admit liability for this debt."

Risk: Resets statute of limitations · Creates admission for court useNever include payment information in a settlement letter. Wait for written confirmation of the agreement, then pay by money order or cashier's check. Do not pay by ACH, wire, or personal check until you have confirmed the settlement in writing and verified the collector's identity.

Risk: Unauthorized account access · Payments accepted without binding the collectorA verbal settlement agreement is not legally enforceable. If a collector says they accept your offer over the phone, do not send payment until you receive a signed written confirming agreement. Calls can be recorded selectively and used by the collector, but not by you unless you are in a one-party consent state.

Risk: No enforceable agreement · Remaining balance can be sold after paymentIf you offer a payment plan in a settlement letter and miss a payment, the collector may void the agreement and pursue the full original balance. Only offer what you can pay. Lump-sum offers are stronger and settle for lower percentages than payment plans.

Risk: Agreement voided · Full balance reinstatedDo not threaten to sue the collector unless you have an actual FDCPA claim ready to file. Empty threats harm your credibility in negotiation. Do not include frustration or accusations. Settlement letters are business documents. Keep the tone neutral and factual.

Risk: Reduces settlement acceptance rate · Can be used against youSending any payment on a debt past the statute of limitations can restart the SOL clock in many states. This turns a time-barred debt the collector cannot sue on into a fresh debt with full legal collection power. Never make any payment, including a small one, without first checking whether the debt is time-barred and understanding your state's SOL reset rules.

Risk: Restarts statute of limitations · Exposes you to lawsuit on debt you could have ignoredWhat Happens After Sending a Settlement Letter?

After sending a settlement letter, the collector has three options: accept, reject, or counter. Most collectors counter. The timeline from first letter to resolved account typically runs 14 to 60 days when both parties are negotiating in good faith.

| Timeframe | What Typically Happens | Your Action |

|---|---|---|

| Days 1–7 | Collector receives and routes the letter internally. No response yet is normal. | Confirm delivery via certified mail tracking. |

| Days 7–21 | Collector responds with acceptance, rejection, or counteroffer. Phone calls may increase. | Do not accept verbal agreements. Request all responses in writing. |

| Days 21–45 | Negotiation round two. Counter their counter. Stay below your maximum. | Send second offer letter if no response by day 30. |

| Days 45–60 | Final agreement reached or offer withdrawn. Signed agreement received. | Submit payment only after signed written agreement is in hand. |

| After Payment | Collector marks account as settled. Bureau reporting updates within 30–60 days. | Confirm bureau reporting. Dispute any inaccurate status within 30 days. |

Does a Settlement Letter Help Remove Collections?

A standard settlement marks the account as "settled for less than full amount" on your credit report. The collection tradeline stays on your report for up to seven years from the original delinquency date. It does not disappear because you paid. A pay-for-delete settlement requests full removal of the tradeline as a condition of payment. Deletion is not guaranteed but is possible with smaller collectors and medical billing agencies.

Three outcomes exist after a collection is resolved through a settlement letter.

- Settled: Balance shows zero. Status shows "settled for less than full amount." This stays on the report and has a negative impact, though less than an open unpaid collection.

- Paid in full: Some collectors agree to report settled accounts as paid in full. This is worth requesting even when pay-for-delete is refused.

- Pay-for-delete: The tradeline is removed entirely. Best possible outcome for your score. Requires written agreement before payment.

Even after a settlement, the original delinquency can remain on your report until the seven-year removal date. Removing it earlier requires a dispute under the Fair Credit Reporting Act. Inaccurate dates, wrong balances, and unverifiable items all create grounds for dispute regardless of settlement status. Understanding how to remove collections from your credit report through the FCRA dispute process shows how settlement and dispute work together as a two-part strategy.

As an FCRA consumer rights attorney reviewing post-settlement files would note, the most overlooked opportunity after settling a collection is auditing whether the original delinquency date is reported correctly on all three bureaus, because a furnisher who re-ages the date incorrectly can be disputed for a removal that settlement alone would never produce.

Common Debt Settlement Mistakes We See

After reviewing thousands of settlement outcomes, the same mistakes appear. They are not about writing skill. They are about sequence, documentation, and starting position. Most of them are avoidable with the right preparation.

Starting too high. One client offered 80% of their balance immediately because they wanted to close the account fast. The collector countered at 50%. Had they started at 25%, they likely would have settled between 30 and 35 percent and saved several hundred more dollars. Your opening offer sets the anchor for the entire negotiation.

Paying before getting written confirmation. A client settled a $2,800 account for $1,100 over the phone, sent a personal check, and received a call two months later from a different collector claiming the remaining $1,700. Nothing was in writing. They paid the full settlement amount and had no proof. The original collector had sold the remainder.

Ignoring the statute of limitations. Two clients in the same week sent settlement letters on accounts that were time-barred in their state. Both letters included small payment offers. In one of those states, a written payment promise restarts the SOL clock. Checking the original delinquency date against state SOL rules before sending any letter is not optional. It changes how much leverage you have and how low you can negotiate.

Settling without addressing credit bureau reporting. A client settled a $900 medical collection and received written confirmation. The account was later reported as "charged off" instead of "settled." Their score did not improve. They had to dispute the status, which took another 45 days. The settlement agreement should have included specific reporting language. If it does not, disputes are the fallback, not the plan.

Can I write my own settlement letter?

Yes. You do not need a lawyer. Use the templates above, customize them with your account information and offer amount, and send via certified mail with return receipt. Keep copies of every letter you send and every response you receive. The paper trail matters if the collector disputes the agreement later.

What percentage should I offer to settle a debt?

Start at 20 to 25 percent for debt buyers and older charge-offs. Start at 30 to 35 percent for credit card debt still with the original creditor. Start at 45 to 50 percent for active lawsuit debt. These are opening positions, not final numbers. Expect the collector to counter higher. Your goal is to reach an agreed number below your maximum before the offer window closes.

How long does debt settlement take?

From first letter to signed agreement typically runs 14 to 60 days. Bureau reporting updates within 30 to 60 days after payment clears. Full credit score recovery from a settlement depends on other factors in your file and typically takes 6 to 24 months, depending on whether the collection is removed or simply marked as settled.

What happens if a collector rejects my offer?

Ask for a counteroffer in writing. Wait 30 days and send a second letter at a slightly higher amount, noting the escalation. Check whether the debt is approaching or past the statute of limitations, because that changes the collector's leverage significantly. CBS News reports that collectors are not required to accept any settlement offer, but most will negotiate when they believe full collection is unlikely.

Can I settle debt before a lawsuit?

Yes, and that is the best time to do it. Pre-lawsuit settlement gives both parties full negotiating flexibility. Once a lawsuit is filed, the collector has invested legal costs and has more leverage. Settlement before any court action also avoids a public record of the lawsuit on your credit file in states where court judgments appear in the public records section of credit reports.

Is a settlement letter legally binding?

Your letter alone is not binding until the collector accepts it in writing. A signed written settlement agreement between both parties is legally binding. Never send payment based on verbal acceptance alone. Verbal promises from collectors are not enforceable.

Do debt collectors accept settlement letters?

Most do, especially debt buyers who purchased the account for 2 to 5 cents on the dollar. Industry data from 2025 shows that roughly 55% of accounts enrolled in settlement programs are eventually settled. The collector's acceptance rate improves when the offer is realistic, the account is old, and the consumer demonstrates genuine inability to pay the full balance.

Settled Accounts Still Hurting Your Credit Score? Start Here.

A settled collection with inaccurate dates, wrong balances, or reporting errors can still be removed through the FCRA dispute process. A free 3-bureau audit across Equifax, Experian, and TransUnion shows every item and which ones do not meet reporting standards. 100% money-back guarantee on fees paid for work that does not produce a result.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card required-

What Happens If a Debt Collector Refuses a Settlement Offer? CBS News · May 2025 — Covers what your options are after a rejection, how to counter, and what leverage factors including the statute of limitations change when a first offer is declined. Directly relevant to what to do after sending a settlement letter and not hearing back.

-

What Is the Success Rate of Debt Settlement? CBS News · April 2025 — Data on settlement completion rates, the role of hardship documentation in collector acceptance decisions, and what separates successful settlement attempts from failed ones. Useful context for understanding where your specific account falls in the probability range.

-

How to Know If You Are Judgment-Proof From Debt Collectors CBS News · April 2026 — Explains when settlement may not be necessary because the collector lacks the legal tools to enforce collection through garnishment or account freezes. Understanding judgment-proof status changes whether a settlement letter is the right first move or whether waiting is a better strategy.

TL;DR: Debt settlement letters can help you negotiate a lower payoff amount on credit card debt, collection accounts, medical bills, and other unpaid debts. Many creditors and collection agencies are willing to accept less than the full balance, especially on older debts that have already been charged off or sent to collections. A good settlement letter explains your situation, offers a specific amount, and asks for written confirmation before any payment is made. The goal is not just to reduce what you owe but to get clear terms in writing and avoid future disputes. This guide includes real settlement letter examples, common negotiation strategies, and mistakes that can cost consumers money during the debt settlement process.

Settlement Letter Examples: Templates for Credit Cards, Collections, and Debt Negotiation

At ASAP Credit Repair, we've reviewed hundreds of collection accounts and settlement offers. One of the biggest mistakes consumers make is agreeing to a settlement over the phone without written documentation.

We created the visual below, to give you an idea about the points we'll be discussing on this content.