Three credit bureaus are the foundation of the U.S. credit reporting system. They include Equifax, Experian, and TransUnion, and they collect, store, and distribute your financial information to lenders. Every loan, credit card, mortgage, or rental application depends on the data inside these three systems.

These bureaus do not just store information. They define how the financial system sees you.

I run a credit repair company, and I review hundreds of tri-bureau reports every month. The same person often appears with three different credit realities. One bureau may show a clean report, another may show outdated collections, and another may show incorrect balances.

That inconsistency is not rare. The Consumer Financial Protection Bureau has reported hundreds of thousands of consumer complaints related to credit reporting accuracy issues, many involving discrepancies across Equifax, Experian, and TransUnion.

Source: https://www.consumerfinance.gov/about-us/newsroom/

This is why understanding the three credit bureaus is not optional. It directly affects your approval odds, interest rates, and financial access.

What Are the Three Major Credit Bureaus?

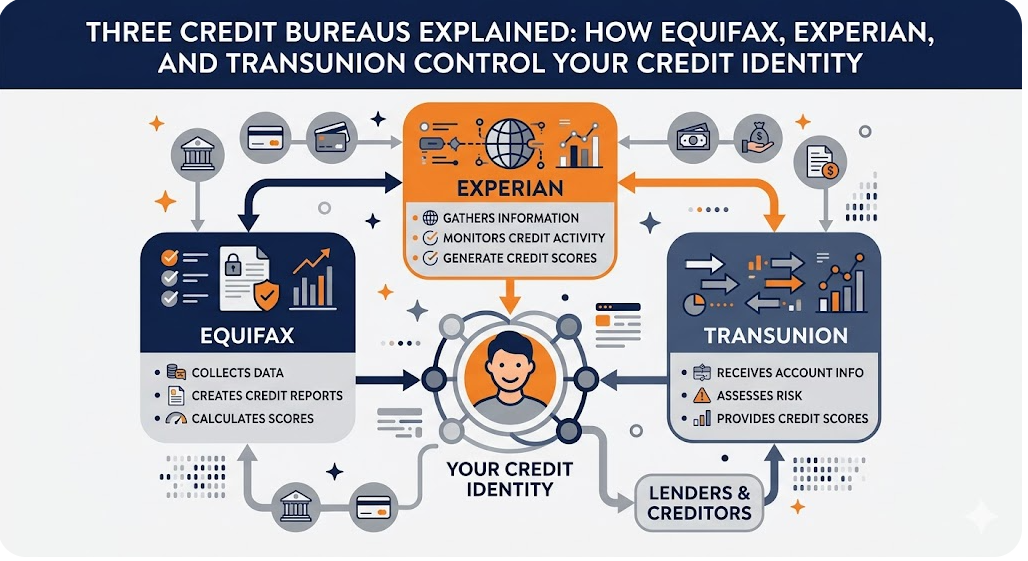

The three major credit bureaus in the United States are Equifax, Experian, and TransUnion. These companies operate independently and compete as private data organizations. They are not government agencies, although they are regulated under federal credit reporting laws such as the Fair Credit Reporting Act (FCRA).

Each bureau builds a separate credit file for you. There is no shared system that guarantees identical data across all three. Instead, each bureau relies on voluntary reporting from lenders.

Equifax may receive an update from a credit card issuer earlier than TransUnion. Experian may receive a different version of the same account data depending on how the lender formats and submits the report. This creates structural differences in credit files that most consumers never realize exist.

From a lending perspective, this matters because lenders do not always pull all three bureaus. Many lending decisions rely on just one bureau file, which means a single inconsistency can affect your outcome.

What Does a Credit Bureau Do?

A credit bureau acts as a centralized data processor between lenders and consumers. It does not issue credit or make approval decisions. Instead, it builds the information lenders rely on to decide whether you are financially trustworthy.

The first function of a credit bureau is data collection. Banks, credit unions, credit card companies, mortgage lenders, and collection agencies report account activity to one or more bureaus. Reporting is voluntary in many cases, which explains why data varies across the three systems.

The second function is credit report creation. Once data is received, the bureau organizes it into structured categories such as payment history, credit utilization, account age, and public records. This becomes your credit report.

The third function is data distribution. Credit bureaus sell access to your report to lenders, insurers, and landlords. Every time you apply for credit, your file is retrieved and analyzed in real time.

The fourth function is dispute processing. When consumers challenge inaccurate data, the bureau is required to investigate under FCRA guidelines. However, investigations often rely heavily on automated systems that re-check data with the original lender rather than manually reviewing evidence.

Last quarter alone, in our case audits, we saw multiple disputes marked “verified as accurate” even when documentation clearly showed reporting errors. This pattern is one of the most common frustrations in credit repair work.

How Many Credit Bureaus Are There?

There are dozens of credit reporting agencies in the United States, but only three nationwide bureaus dominate lending decisions: Equifax, Experian, and TransUnion.

These three systems are the standard across:

Credit cards

Auto loans

Mortgages

Personal loans

Tenant screening

Other reporting agencies exist, but they serve niche roles. Some track rental payments, others track banking behavior, and others focus on insurance claims or medical debt reporting. These are secondary systems and do not carry the same weight in mainstream lending decisions.

When lenders refer to “your credit,” they are almost always referring to data from the three major bureaus.

What Are the Three Major Credit Agencies?

The term “credit agencies” is commonly used interchangeably with credit bureaus, although “bureau” is the more technically accurate term.

The three major credit agencies are still Equifax, Experian, and TransUnion. Each agency functions as a separate database system with its own reporting logic and update cycle.

Even though they serve the same purpose, they do not operate in sync. For example, Experian is often faster in updating credit card balances, while TransUnion is frequently used in auto lending risk models, and Equifax is heavily involved in mortgage underwriting ecosystems.

These differences are not formal scoring rules but reflect real-world lender behavior and integration patterns.

Why Do the Three Credit Bureaus Show Different Information?

The three credit bureaus show different information because the credit system is not centralized. It is fragmented by design.

The first reason is inconsistent lender reporting. Some lenders report to all three bureaus, while others report to only one or two. There is no universal requirement for complete reporting coverage.

The second reason is reporting timing delays. A payment or balance update may appear in Experian within days but take weeks to reflect in TransUnion or Equifax. These timing gaps create temporary but sometimes significant differences in credit files.

The third reason is data formatting variation. Lenders submit raw data in different structures. Each bureau interprets and converts that data into standardized fields. Small interpretation differences can result in mismatched balances, account statuses, or credit limits.

In consumer discussions across credit communities like r/CRedit, users frequently report identical accounts appearing differently across bureaus due to timing and reporting inconsistencies. Source: https://www.reddit.com/r/CRedit/

From a practical standpoint, this means your credit profile is not stable in real time. It is constantly shifting depending on which bureau is updated first.

Why Credit Scores Differ Between the Three Credit Bureaus

Credit scores differ because they are built on top of different data sets and sometimes different scoring models.

The two dominant scoring systems are FICO and VantageScore. Both models evaluate similar credit factors, but they assign different weights to those factors.

Payment history is always important, but credit utilization, account age, and recent inquiries may carry different importance depending on the model. As a result, the same credit profile can produce different scores across systems.

Differences between bureaus amplify this effect. If one bureau shows a higher balance or a recently reported delinquency while another does not, the resulting scores will naturally diverge.

Even hard inquiries can create temporary score gaps. A lender may report an inquiry to one bureau immediately while another bureau updates later, causing short-term inconsistencies in credit scoring.

This is why lenders often see multiple scores for the same consumer and still rely on internal lending thresholds rather than a single number.

How to Check All Three Credit Bureaus

Consumers can access all three credit reports through AnnualCreditReport.com, which is the only federally authorized free credit report service.

This system allows full access to Equifax, Experian, and TransUnion reports.

A complete review is essential because each report may contain different accounts, balances, or errors. Relying on a single bureau creates blind spots in credit monitoring.

In many client reviews, we find cases where one bureau shows a closed account while another still shows it as open. These inconsistencies can directly impact loan approvals and interest rates.

What Happens When One Credit Bureau Has Incorrect Data?

When one credit bureau reports incorrect information, it can distort your financial profile and affect lending decisions.

The correction process begins with a formal dispute. The consumer submits evidence directly to the bureau, which then contacts the data furnisher, usually the lender, to verify accuracy.

Under FCRA requirements, both the bureau and the lender must investigate the claim within approximately 30 days.

However, investigations often rely on automated matching systems. If the lender confirms the data without reviewing supporting documentation, the error may remain unchanged.

This is why disputes sometimes require escalation or repeated filings across all three bureaus.

Why the Three Credit Bureaus Matter in Real Financial Decisions

The three credit bureaus matter because they directly influence lending outcomes.

A borrower may be considered low risk on one bureau and moderate risk on another. That difference can change approval decisions, interest rates, and credit limits.

Lenders do not always pull all three reports. Some rely on one bureau exclusively, which means a single inaccurate file can disproportionately affect your financial opportunities.

From a credit system perspective, your financial identity is not one score. It is three parallel credit identities that do not always align.

Final Understanding of the Three Credit Bureaus

The three credit bureaus—Equifax, Experian, and TransUnion—form the backbone of the U.S. credit system. They collect financial data independently, maintain separate credit files, and influence nearly every lending decision.

Get a 3-bureau credit review and find out what Equifax, Experian, and TransUnion are reporting about you today.

Get Started →Because they operate independently, your credit profile is not unified. It exists as three separate versions that evolve at different speeds based on lender reporting behavior and internal data processing systems.

Understanding how these bureaus work gives consumers a strategic advantage. It allows for better credit monitoring, faster dispute correction, and more accurate interpretation of lending decisions.

A strong credit profile is not just about improving a score. It is about ensuring consistency, accuracy, and alignment across all three credit bureaus so lenders see a complete and correct financial picture.