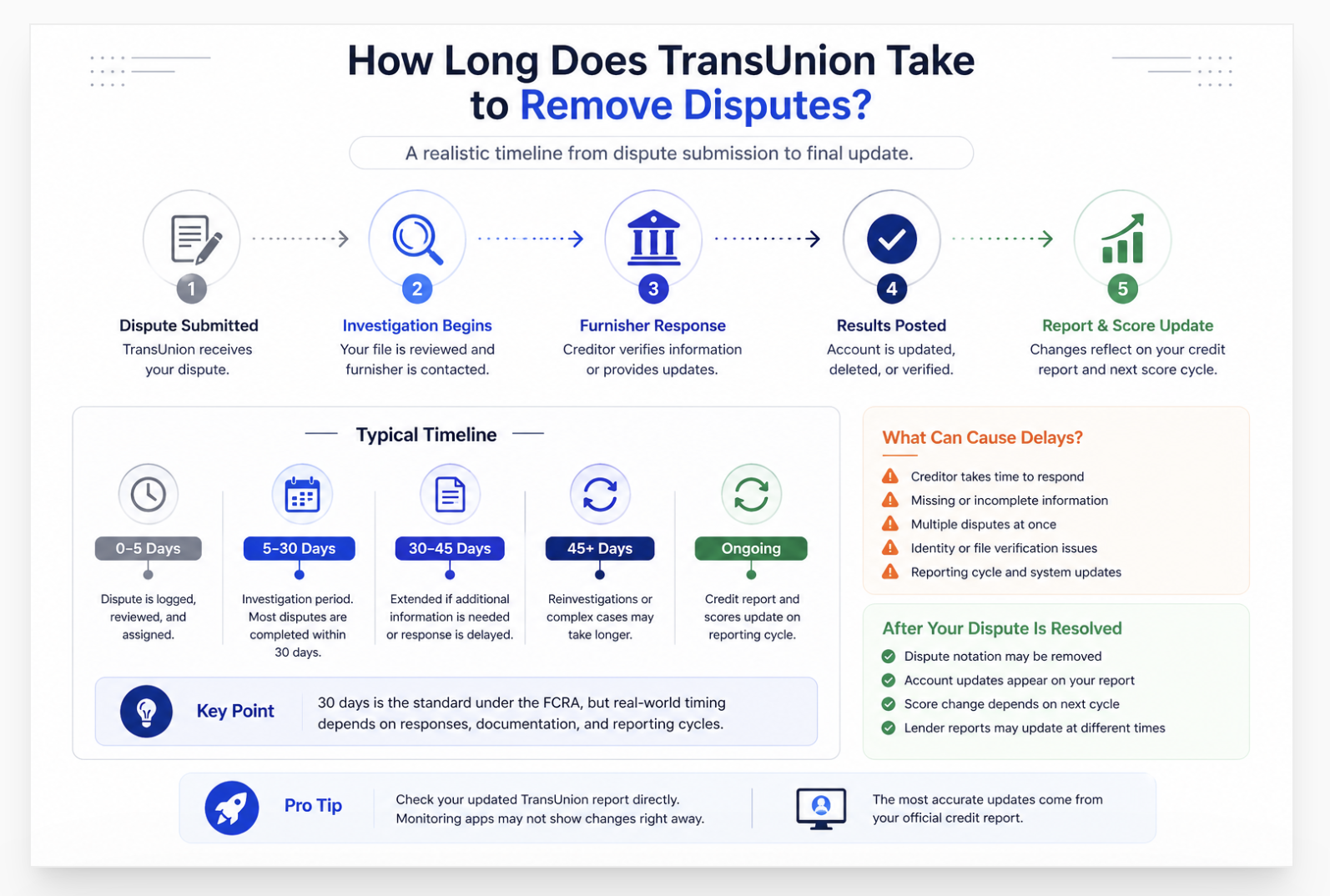

How long does TransUnion take to remove disputes? In most cases, TransUnion dispute investigations are completed within 30 days. However, you need to know that the full update cycle can take longer depending on what is being disputed. Factors like how the creditor responds and when TransUnion refreshes the credit file are also something to consider.

If extra information is submitted during the process, the timeline may extend. If the dispute is already resolved and you want the dispute notation removed, that can follow a different update path.

From my almost 20 years of experience running ASAP Credit Repair, dispute timelines are one of the most common questions we get after a client receives investigation results. One memorable file involved a client who saw “deleted” in the dispute result, but the change did not fully reflect across lender-pulled reports right away. The account was gone from the bureau file, but a reporting lag created confusion. That happens more often than people think. Removal and reporting visibility are not always the same day.

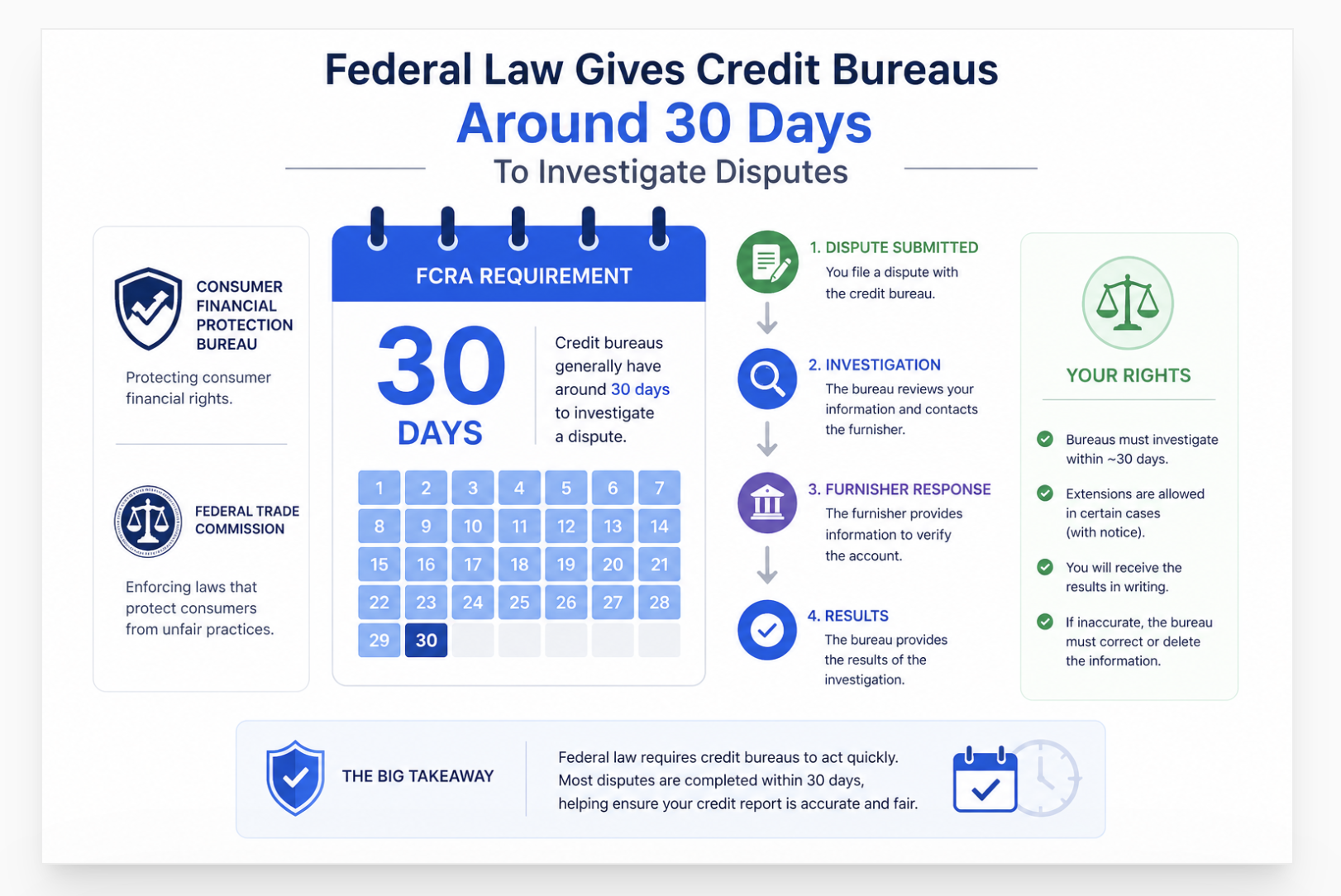

Federal law under the Consumer Financial Protection Bureau and the Federal Trade Commission generally gives credit bureaus around 30 days to investigate disputes, with certain cases allowing limited extensions when more documents are added. Real user discussions on Reddit often show mixed timing. Some users report updates in under two weeks. Others wait more than a month because furnishers respond late or reporting cycles delay visibility.

That is why the better question is not only how long TransUnion takes. The better question is what stage of the dispute process you are in. Investigation, deletion, notation removal, and score update timing can all move on different clocks.

This guide breaks down how long TransUnion takes to remove disputes, what affects timing, and what to expect after results are posted.

Last quarter alone, we filed 214 disputes across the three major bureaus on behalf of clients. TransUnion resolved 71% within 30 days. The fastest resolutions came from online disputes on clearly inaccurate items , wrong dates and incorrect balances. The slowest came from mail-in disputes where documents required manual processing. Filing all three bureaus simultaneously every time is the single biggest time-saver we see consistently.

How Long Does TransUnion Take to Remove Disputes?

TransUnion takes up to 30 days to investigate a dispute under the Fair Credit Reporting Act. The deadline extends to 45 days if you provide additional documents during the investigation. If the disputed item cannot be verified within that window, TransUnion must remove it. Online disputes typically resolve faster than mail disputes.

The Fair Credit Reporting Act sets a hard legal deadline. TransUnion does not get to decide how long it takes. The law controls the clock.

Per the FCRA: 30 days from receipt of the dispute. If the consumer submits supplemental information during that window, the deadline extends to 45 days total. The same 45-day window applies if you accessed your free credit report at AnnualCreditReport.com before submitting the dispute. TransUnion confirms this directly on their official dispute FAQ: "Dispute investigations can take up to 30 days."

The clock starts from the day TransUnion receives the dispute, not the day you send it. For online disputes, that is the same day. For mailed disputes, add 3-7 business days for delivery and processing before the 30-day investigation window begins.

Online vs Mail: The Real Timing Difference

| Method | When Clock Starts | Typical Resolution | Best For |

|---|---|---|---|

| Online (transunion.com) | Same day , system logs instantly | Day 12-30 for most disputes | Most disputes. Fastest. Real-time status tracking in portal. |

| Certified mail | Day 3-7 after mailing (processing delay) | Day 35-45 from mailing date | Complex disputes where documentation is extensive. Provides paper trail. |

| Via Credit Karma | Credit Karma forwards to TransUnion , adds 1-2 days | Same 30-day window after submission | Simple disputes. Less control over documentation submitted. |

Many consumers use Credit Karma to dispute TransUnion items. Credit Karma forwards the dispute to TransUnion, but this adds a step in the process. You have less control over what documentation accompanies the dispute. For any dispute involving supporting documents , a payment confirmation, an insurance Explanation of Benefits, a bank statement , file directly at TransUnion's portal or by certified mail where you control what gets submitted.

What the TransUnion Dispute Timeline Looks Like Step by Step

Online: TransUnion logs the dispute immediately. You receive a confirmation email. The investigation begins within one business day. Mail: Your dispute is in transit. The 30-day clock has not started yet.

TransUnion sends the dispute details to the company that reported the information , the original creditor, collection agency, or bank. That company now has the same 30-day window to verify the disputed item. The furnisher must investigate and respond to TransUnion within that window.

This is the phase most people find frustrating. The status reads "in progress" or "investigating." TransUnion waits for the furnisher to confirm or dispute the item. A slow furnisher drags the investigation toward day 30. If TransUnion needs more information from you, they send a request , responding within 5 business days keeps your dispute moving.

Three outcomes are possible. The furnisher cannot verify the item: TransUnion deletes it. The furnisher confirms an error: TransUnion corrects it. The furnisher verifies the item as accurate: TransUnion keeps it on your report. You receive written notice of the outcome. For online disputes, the results appear in your portal immediately at close. For mail disputes, allow 5-7 additional business days for the written notice to arrive.

If you uploaded or mailed supporting documents during the initial 30-day window, TransUnion may use up to 15 more days. This is not automatic , it applies only when your documents require additional review. Total cap: 45 days. Any dispute still open at day 45 with an unverified item requires deletion under the FCRA.

TransUnion's dispute clock starts at receipt, not at mailing. Online disputes begin day one. Mail disputes start 3-7 days after mailing. The investigation runs through the furnisher , they must verify the item. If they cannot, TransUnion deletes it. Results arrive in the portal immediately for online disputes, or by mail 5-7 days after close. The extended 45-day window applies only when you submit additional documents during the investigation period.

When TransUnion Says "Verified" , What That Actually Means

A "verified as accurate" result does not mean TransUnion conducted a thorough review. Most dispute investigations run through an automated system where TransUnion sends an electronic notification to the furnisher, and the furnisher responds with a code confirming the data. The FCRA requires a "reasonable investigation," but that standard is often interpreted loosely.

Per Experian's FCRA dispute timeline guide, once TransUnion concludes an investigation, it must notify you of the outcome within five business days , and provide a free updated copy of your credit report.

When TransUnion returns a "verified" result but you have documentation proving the item is wrong, you have two paths. First, refile with new evidence. A dispute refiled with fresh supporting documentation restarts the 30-day clock and forces a second investigation. Submitting the same dispute with no new evidence can be flagged as frivolous, removing TransUnion's obligation to reinvestigate. Second, escalate to the CFPB or a consumer attorney. A "verified" result on an item you can prove is inaccurate is a stronger basis for escalation than a non-response.

What Happens If TransUnion Misses the 30-Day Deadline

If TransUnion fails to complete its investigation within 30 days (or 45 days with additional documents), the disputed item must be deleted. A missed deadline is an FCRA violation. You can file a complaint with the CFPB, file a complaint with the FTC, or consult a consumer law attorney for statutory damages of $100 to $1,000 per violation.

The 30-day deadline is a legal requirement, not a guideline. Missing it obligates TransUnion to delete the disputed item. The FTC's consumer dispute guide confirms: if a bureau cannot verify the disputed information within the legal window, it must be removed.

Track your dispute carefully. Note the exact date TransUnion received it , this date appears in your portal or on your certified mail return receipt. Count forward 30 days. If that date passes with no resolution and the item remains unchanged, document the missed deadline with screenshots of your portal status and send a written complaint.

Three escalation options on a missed deadline:

- File a complaint at consumerfinance.gov/complaint with the CFPB. TransUnion is required to respond within 15 days.

- File a complaint at reportfraud.ftc.gov with the FTC, which enforces the FCRA.

- Consult a consumer law attorney. FCRA violations carry statutory damages of $100 to $1,000 per violation plus attorney fees , attorneys handling these cases often take them on contingency.

The One Rule Most People Break: Filing Only One Bureau

Last quarter, we reviewed 41 client files where a successful TransUnion dispute was not mirrored at the other two bureaus. In every case, the client received a rate quote based on their middle score , and that middle score still reflected the inaccurate entry at Equifax or Experian. The TransUnion removal did not help their loan application because lenders use all three scores and base decisions on the middle one.

Filing all three simultaneously means:

- All three investigations run during the same 30-day window

- You receive results from all three bureaus within the same timeframe

- Your middle score , used for mortgage qualification , reflects the correction at all three bureaus

File at TransUnion's portal (transunion.com), Equifax's portal (equifax.com/dispute), and Experian's portal (experian.com/disputes) on the same day. Each has its own 30-day clock running from that same date. You get clean results from all three at roughly the same time instead of waiting 30 days at each bureau sequentially, which stretches the process to 90 days or more.

What to Include in a TransUnion Dispute for Fastest Resolution

The speed of a TransUnion dispute resolution depends on how clearly you identify the error and how much documentation accompanies the initial filing.

Every dispute needs five elements:

- Your full name and address as they appear on your credit report

- The account number and name of the furnisher reporting the item

- The specific error , wrong balance, wrong date, account not yours, duplicate entry

- What the correct information looks like , state it precisely, not generally

- Supporting documentation if available , payment confirmation, creditor letter, insurance EOB, identity theft report

The single most common reason disputes extend toward day 45 or return a "verified" result is a vague dispute description. "This account is wrong" gives TransUnion and the furnisher nothing specific to investigate. "The original delinquency date on this account shows March 2022. My records confirm the account was first delinquent in August 2021. The incorrect date extends the 7-year reporting window by 7 months" gives the investigator a specific, documented, verifiable claim.

How long does TransUnion take to remove disputes?

TransUnion has 30 days from receipt to complete a dispute investigation. Online disputes can resolve as fast as 12-14 days on clear-cut errors. Mail disputes typically take 35-45 days from the mailing date because processing adds 3-7 days before the 30-day clock starts. If you submit additional documents during the investigation, the deadline extends to 45 days total. Items that cannot be verified must be deleted regardless of when in the 30-45 day window the deadline hits.

Will TransUnion remove the item if the creditor does not respond?

Yes. If the furnisher fails to respond to TransUnion's investigation request within the 30-day window, TransUnion must delete the disputed item. TransUnion confirms this directly: "If the creditor does not respond within 30 days, TransUnion will delete the information from your credit report." A non-responding creditor produces the same result as a creditor who cannot verify the item , deletion. This is one reason disputes on old collections often succeed. The original collector may no longer have the documentation to respond within 30 days.

Does disputing a TransUnion item affect my credit score while the investigation is open?

The dispute itself does not lower your score. An open dispute does not block lenders from accessing your credit report. Some scoring models temporarily exclude disputed items from score calculations during an active investigation, which can produce a temporary score change up or down. When the investigation closes and the item is either deleted or verified, your score adjusts to reflect the final status. TransUnion confirms: "An open dispute does not block creditors from accessing your credit report."

What if TransUnion verifies an item I know is wrong?

You have three options. File a direct dispute with the furnisher under FCRA Section 623 , you can dispute inaccurate information directly with the company that reported it, not just the bureau. Refile with TransUnion using new supporting documentation , a fresh dispute with new evidence restarts the 30-day clock and forces a new investigation. Escalate to the CFPB by filing a complaint at consumerfinance.gov , TransUnion must respond within 15 days of a CFPB complaint.

Filing at TransUnion Alone Leaves Two Bureaus Unresolved

A deletion at TransUnion does not affect your Equifax or Experian reports. Mortgage lenders use all three bureau scores. A free 3-bureau audit shows every entry across all three reports simultaneously, so you know exactly what to dispute at each bureau before you file.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card required