Unsubsidized vs Subsidized Loans Explained: Who pays your interest while you are in school? With subsidized loans, the government pays it. With unsubsidized loans, you pay it even while sitting in class. That gap can add hundreds or thousands to your balance by graduation. Both are federal loans. Both need a FAFSA. But they cost very different amounts over time.

Running a credit repair company, I see the effects of this choice every week. One of the most unforgettable cases came from a client who finished college with $22,000 in unsubsidized loans. She paid no interest while in school. By the time repayment started, her balance had grown to nearly $26,500 before she made one payment. That extra $4,500 was entirely preventable.

According to LendingTree's 2025 student loan report, 44% of all federal loans in the 2024–25 school year were unsubsidized. Only 15% were subsidized. Total federal student debt now sits at $1.696 trillion, a record. Most borrowers do not know why their balance grows before their first payment. Knowing how unsubsidized vs. subsidized loans differ is the first step to changing that.

What Is the Difference Between Subsidized and Unsubsidized Student Loans?

The core difference between unsubsidized vs subsidized loans is interest timing.

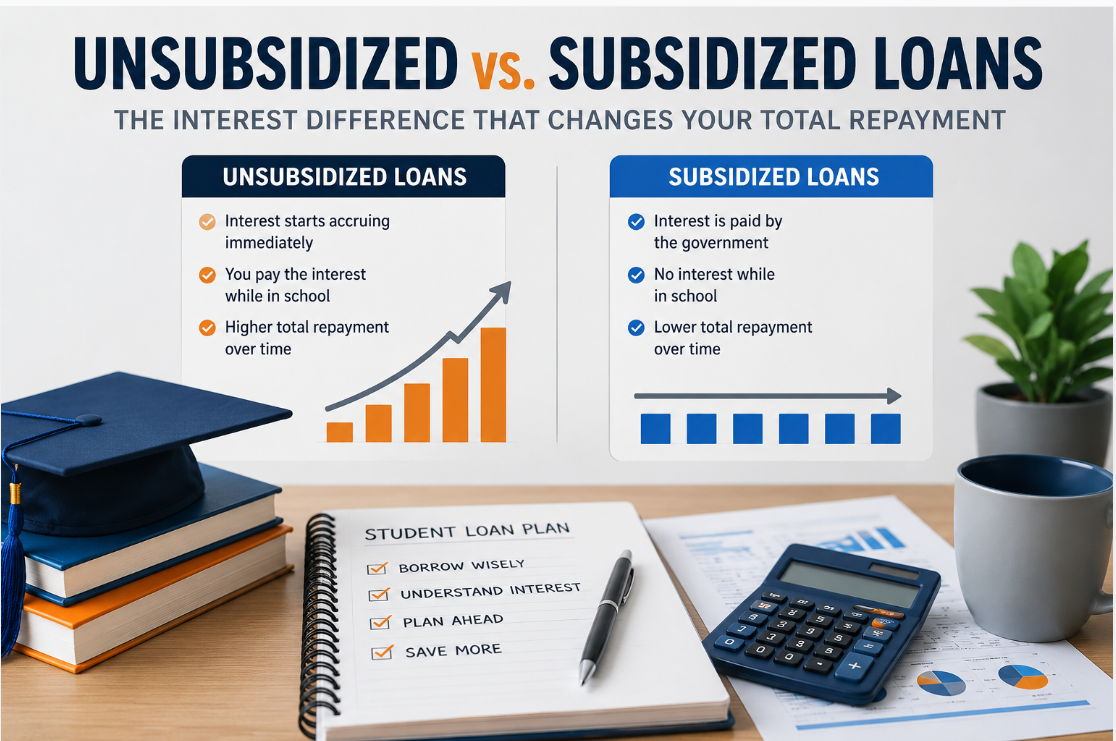

Subsidized loans are need-based. The Department of Education pays your interest while you are in school at least half-time. It also covers interest during your six-month grace period and any approved deferment. Your loan balance stays flat during all of those windows.

Unsubsidized loans are not need-based. Interest starts building the day your funds arrive. You can skip payments while in school. But interest keeps running. When repayment begins, that unpaid interest gets added to your balance. You then pay interest on top of interest.

Both loan types carry the same fixed rate for undergrads, 6.53% for 2024–25, per the Federal Student Aid Knowledge Center. Subsidized loans cap at $3,500 for first-year students, with a $23,000 lifetime limit. Unsubsidized loans allow up to $5,500 (dependent) or $9,500 (independent) in year one, with a $57,500 lifetime cap for undergrads. The rate is not the problem. The problem is when the interest starts running.

What Is an Unsubsidized Loan?

A Direct Unsubsidized Loan is a federal loan open to both undergrads and grad students. You do not need to show financial need. You just file the FAFSA and enroll at least half-time.

Interest builds daily from the date your school gets the funds. At 6.53%, a $10,000 unsubsidized loan adds about $1.79 in interest per day, per College Finance's accrual breakdown. Over four years, that one loan grows by roughly $2,600 before you make a single payment.

When repayment starts, your servicer adds that $2,600 to your $10,000 balance. Your new starting balance is $12,600. Interest then builds on $12,600, not the original $10,000. This process is called interest capitalization.

That is why unsubsidized loans cost more. Not because of a higher rate. Because of when the clock starts.

What Is a Subsidized Loan?

A Direct Subsidized Loan is a federal loan for undergrads with shown financial need. The FAFSA measures need by comparing your family's expected payment to your school's cost of attendance.

The government covers your interest during three clear periods. First, while you are enrolled at least half-time. Second, during the six-month grace period after you leave school. Third, during any approved deferment.

Once repayment starts, you pay the interest yourself. But no hidden interest built up while you were in school. Your balance at repayment matches what you borrowed, not more.

Subsidized loans are only for undergrads. Grad students do not qualify. A first-year student gets up to $3,500 in subsidized funds versus $5,500 in unsubsidized funds. To recap: unsubsidized vs. subsidized loans work the same way once repayment starts. The big difference is what happens before repayment begins.

Do Subsidized and Unsubsidized Loans Save Money?

Subsidized loans save real money. The numbers make this clear.

Take a first-year dependent student who borrows $3,500 in subsidized loans and $2,000 in unsubsidized loans at 6.53%. Over 51 months in school and a grace period, the subsidized loan costs her $0 in accrued interest. The unsubsidized loan builds roughly $354 in interest that capitalizes at repayment.

That $354 joins her principal. She then pays interest on that extra amount for the full 10-year term. Her total cost goes up because of the loan type, not the rate.

Studentaid.gov confirms this directly: a borrower who accepts both loan types and pays nothing in school will always pay more with unsubsidized loans. The rule is simple. Accept subsidized loans first. Use unsubsidized loans only for the remaining gap.

What Happens to Interest on Unsubsidized Loans While in School?

Interest on unsubsidized loans builds every single day. Most students skip payments while in school. That is allowed. But skipping does not stop the interest clock.

When repayment begins, the servicer runs interest capitalization. The CFPB explains it this way: unpaid interest attaches to the main balance, and future interest then builds on the new, larger amount. Every dollar that capitalizes costs more than a dollar over the loan's life.

One smart move is to pay just the interest each month while still in school. On a $5,500 unsubsidized loan at 6.53%, that is about $30 per month. That small payment stops capitalization entirely. Over a 10-year repayment plan, the savings on that one loan can top $500.

In our credit repair practice, this is the first thing we check for clients with large student loan balances. In 2024, we reviewed 63 cases where borrowers owed more than they originally took out. Nearly everyone traced back to unmanaged, unsubsidized loan interest during school.

How Do You Choose Between Subsidized and Unsubsidized Student Loans?

When comparing unsubsidized vs subsidized loans, the FAFSA makes the first decision for you. You cannot pick subsidized loans freely. You must qualify based on financial need.

File the FAFSA as early as possible each year. Then open your financial aid offer and check for subsidized loan amounts. Accept all subsidized loans before touching unsubsidized funds. Borrow only what you need from unsubsidized loans, because every extra dollar builds interest from day one.

Grad students have no choice in the unsubsidized vs. subsidized loans decision. Subsidized loans do not exist at the grad level. Every federal loan a grad student takes is unsubsidized at 6.53% (2024–25). Interest runs the full time they are in school.

If you do not qualify for subsidized loans as an undergrad, keep your unsubsidized balance as low as possible. Grants, scholarships, and work-study all cut down what you need to borrow.

Can You Have Both Subsidized and Unsubsidized Loans?

Yes. Most undergrads receive a mix of both in one aid package.

A dependent sophomore might get $4,500 in subsidized loans and $2,000 in unsubsidized loans. Both are federal direct loans. Both carry the same rate. But the subsidized portion costs less because it never builds interest while she is in class.

Having both types is common and easy to manage. Track them as two separate loan types. When repayment starts, you will know which portion carries capitalized interest. Target that balance first to lower your total cost.

Last year, we helped 40 clients restructure repayment plans that mixed both loan types. In almost every case, they had been putting payments toward the wrong loan first.

Which Loan Should You Pay Off First After Graduation?

Pay unsubsidized loans off first.

Both types carry the same undergrad rate. But unsubsidized loans start repayment with a higher true balance because of capitalized interest. Paying them down faster cuts the principal that drives new interest each day.

If you have unsubsidized loans from several years ago, use the avalanche method. Target the highest balance or most capitalized interest first while keeping up minimum payments on the rest.

Borrowers on income-driven plans should still direct extra payments toward unsubsidized balances. Lower monthly payments slow down principal payoff. Any extra cash speeds that back up.

Who Qualifies for Unsubsidized vs Subsidized Loans?

Subsidized Loan Requirements

To get a subsidized loan, you must be enrolled at least half-time at an eligible school. You must show financial need through the FAFSA. You must be an undergraduate student; graduate students do not qualify. You also need to meet Satisfactory Academic Progress, which means at least a 2.0 GPA and passing two-thirds of enrolled credits each term.

Student Loans Hurting Your Credit?

Late payments, growing balances, and reporting errors from student loans can lower your credit score fast. Get a free professional credit review and discover ways to improve your credit profile.

✔ Review student loan reporting issues

✔ Identify inaccurate negative accounts

✔ Build a smarter repayment and credit strategy

No obligation • Fast review • Trusted credit experts

Unsubsidized Loan Requirements

To get an unsubsidized loan, you must be enrolled at least half-time. You file the FAFSA, but financial need is not required. Graduate, professional, and undergraduate students all qualify.

Both loans need no credit check and no co-signer. That makes federal loans the right first step for any student. Look at private loans only after federal aid runs out. Private loans carry higher rates and fewer repayment protections.

The choice between unsubsidized vs. subsidized loans shapes your total debt load. Understanding this is one of the most useful steps any student can take before signing a financial aid offer. Subsidized loans protect your balance during school. Unsubsidized loans fill the gap when subsidized funds run out. The FAFSA opens the door to both. Filing it early and every year gives you the best shot at the most affordable aid.

Both loan types show up on your credit report. The way you handle unsubsidized vs. subsidized loans during and after school shapes that record. On-time payments build your score. Missed ones hurt it fast. If student loan debt has already damaged your credit, a professional credit review can help find errors, dispute inaccurate items, and build a clear repayment path.