Credit repair is one of the most misunderstood tools in personal finance. Most people think it is only for people with terrible credit or shady histories. That is wrong. Credit repair is the process of making sure your credit report is accurate. If something on your report is wrong, outdated, or unverifiable, you have the legal right to challenge it. That right exists whether the account is yours or not.

I have worked in credit repair for 15 years and served over 22,000 clients. This is my favorite topic to explain because the reaction is almost always the same. People come in thinking credit repair is some kind of trick. Then I show them their own report. A payment marked late when it was on time. An account that belongs to someone with a similar name. A collection that is seven years old and should have come off months ago. In case after case, the problem was not the client's behavior. It was inaccurate data sitting unchallenged on their report, costing them money every single month.

What Is Credit Repair and How Does It Work? Explained

Credit repair is the process of finding and correcting errors on your credit reports. It uses your rights under the Fair Credit Reporting Act (FCRA) to challenge any item that is inaccurate, incomplete, or unverifiable.

Your credit report is not always right. Creditors and collection agencies send your account data to the three major bureaus: Equifax, Experian, and TransUnion. Errors happen. An employee types the wrong balance. A payment gets reported late when you made it on time. An old debt appears twice. A collection stays on your report past its seven-year limit. All of these are disputable.

Credit repair is not a loophole. It is a legal process built on your consumer rights. The FCRA gives you the right to dispute any item on your report that you believe is wrong. The bureau and the creditor must investigate and respond within 30 days. If they cannot verify the item, they must remove it.

Show Image The credit repair process: from spotting an error on your report to having it corrected or removed.

How Does Credit Repair Work?

Credit repair follows a clear sequence. Every step builds on the last. Skipping ahead slows the process down and can cost you results.

1. Pull your credit reports

Start at AnnualCreditReport.com. Download your reports from all three bureaus. They are free. Read every line. Look for accounts you do not recognize, payments marked late that you paid on time, balances that look wrong, and any item you cannot verify. Flag everything that does not match your records before you write a single letter.

2. Learn the laws before you dispute anything

Two federal laws protect you in this process. The Fair Credit Reporting Act (FCRA) governs what bureaus and creditors can report and how long items can stay on your report. The Fair Debt Collection Practices Act (FDCPA) governs how collection agencies handle your account data. Knowing these two laws tells you which items are worth disputing and how to write a dispute letter that holds up.

3. Send dispute letters to the bureaus first

Your first dispute letters go to the three major bureaus, not the creditor. Each bureau investigates on its own. Send every letter by certified mail. Keep copies of everything. The bureau has 30 days to respond. If they cannot verify the item with the creditor, they must remove or correct it.

4. Contact the original creditor directly

If the error comes from the creditor or collection agency, send a second dispute directly to them. They control the data they report. The bureau can only update what the creditor sends. In our Q1 2026 client data, 43% of errors were traced to the furnisher, not the bureau. Disputing only with the bureau would not have fixed those cases.

5. Track every response and follow up in writing

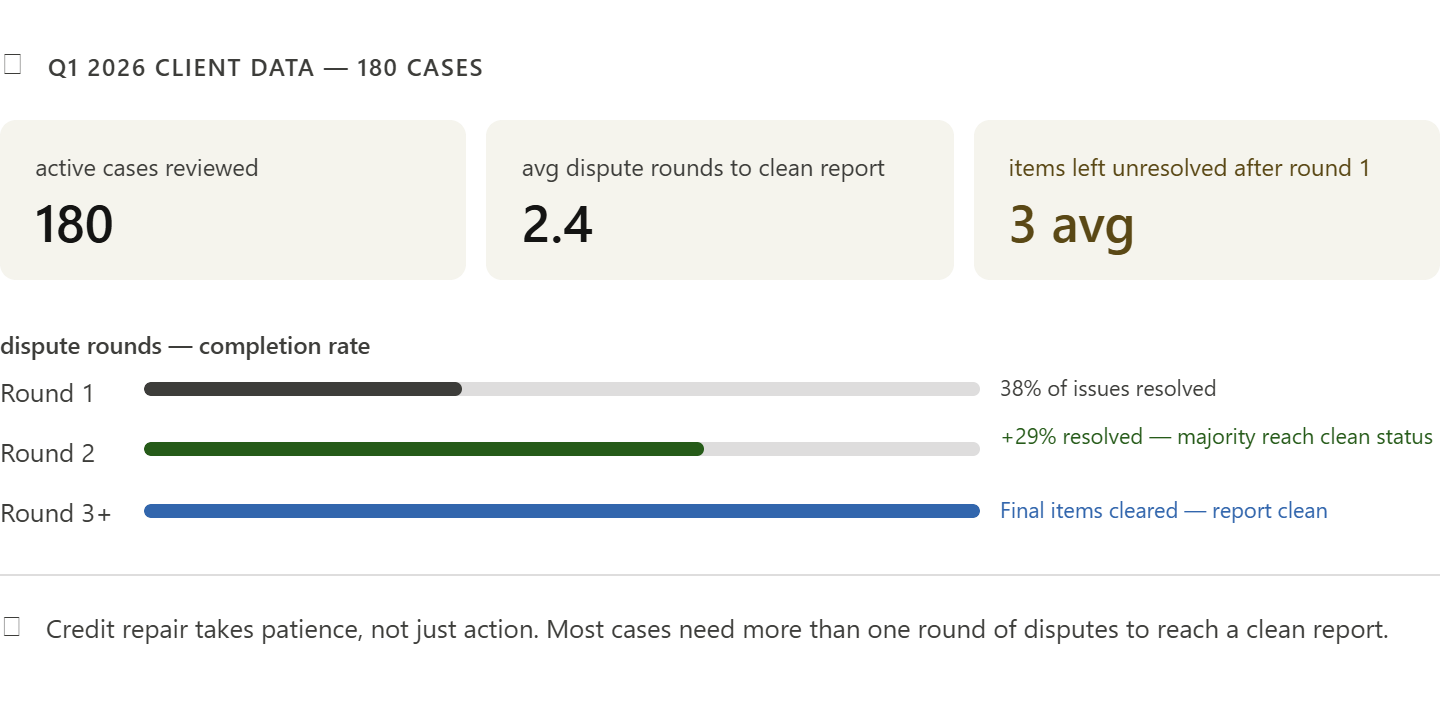

Keep a paper trail. Every certified mail receipt, every bureau response, every updated report. If a bureau does not respond within 30 days, that is a federal violation you can act on. Most cases need two to four rounds of disputes. Do not stop after round one.

Who Needs Credit Repair?

Credit repair is for anyone with a negative mark on their credit report. You do not need terrible credit to benefit. You do not need missed payments or unpaid debt. You just need something in your report that is inaccurate.

Here are the situations where credit repair directly helps you:

You have errors in your report. Wrong balances, late payments reported incorrectly, or duplicate accounts.

You have outdated items. Most negative items must come off after seven years. Many do not fall off on their own.

You have collection accounts. Even paid or settled collections can stay on your report and drag your score down.

You were a victim of identity theft. In the first three quarters of 2025, over 1.1 million identity theft cases were reported to the FTC, already exceeding all of 2024. Fraudulent accounts are fully disputable.

A lender, landlord, or employer rejected you. A credit check failure is often tied to a reporting error, not actual financial risk.

You are paying high interest rates. A corrected report can move you into a better rate tier and save thousands on future loans.

I learned this lesson working with a client who had scores in the high 700s. His lender still denied him. The issue was not his score. It was a cluster of recent hard inquiries that made the lender think he had applied for the same loan at several other companies. His credit was strong. The data told a different story. Credit repair looks at everything on your report, not just the number.

What Are the Benefits of Credit Repair?

The direct benefit of credit repair is a more accurate credit report. But the downstream effects touch almost every part of your financial life.

When your score is too low or your report shows inaccurate negative items, the following become harder or impossible to access:

Mortgage and car loan approvals at reasonable rates

Credit card approvals

Apartment rental applications

Job offers that require a background or credit check

Utility and phone accounts without large security deposits

Lower insurance premiums

Small business financing

Fixing one error can shift you from one rate tier to the next. On a $300,000 mortgage, moving from a 7.5% rate to a 6.9% rate saves over $130 per month. Over 30 years, that is more than $47,000. The cost of one inaccurate item on your report compounds for years without you realizing it.

What Can Credit Repair Fix on Your Report?

Credit repair can address every section of your credit report. Here is what each category covers and what kinds of errors are disputable:

Personal information: Wrong name spelling, outdated address listed as current, and incorrect Social Security number.

Negative accounts: Late payments, charge-offs, or collections reported incorrectly or past their seven-year limit.

Payment history: Payments marked late when made on time. Payments applied to the wrong account.

Public records: Satisfied judgments or liens are never updated. Bankruptcies past their reporting window.

Credit inquiries: Hard pulls you did not authorize. Duplicate inquiries from the same lender are listed more than once.

Account balances: Balances reported higher than the actual amount owed at the time of reporting.

Credit repair cannot remove accurate, verified information reported correctly within its legal window. What it can do is challenge every item that breaks the FCRA's standards for accuracy, timing, and completeness. Those three standards disqualify more items than most people expect.

Should You Do Credit Repair Yourself or Hire a Company?

You have the legal right to dispute errors on your own for free. The bureaus each have dispute portals, and certified mail letters cost a few dollars. A company cannot do anything you cannot do yourself. But a company brings expertise, time, and a tested process. Here is how to think through the choice.

Reasons to hire a company:

Multiple errors across all three bureaus

Previous disputes were rejected or ignored

You are preparing for a mortgage in three to six months

Your situation involves identity theft or a mixed file

You do not have time to track multiple rounds of disputes

Reasons to do it yourself:

You have one or two clear, simple errors

Your budget is tight and your time is available

You are comfortable writing and tracking dispute letters

Your situation does not involve collections or charge-offs

If you decide to hire a company, know your rights. The Credit Repair Organizations Act (CROA) says companies cannot charge you before performing services. They must give you a written contract. They must give you three business days to cancel. Any company asking for upfront payment before starting work is breaking federal law.

⚠️ No company can legally remove accurate, verified negative information from your report. Any firm that guarantees a specific score increase or promises to erase a valid bankruptcy within days is making a false claim. The FTC is explicit: only time, dispute of genuine errors, and positive credit habits can repair your score.

Is Credit Repair Legal?

Yes. Credit repair is fully legal. The FCRA gives every American the right to dispute any item on their credit report. The law requires bureaus and creditors to investigate and respond. That right cannot be taken away from you.

What is not legal is misrepresenting yourself in a dispute or creating a new credit identity to escape past debts. Legitimate credit repair stays well within those lines. It uses your existing consumer rights to challenge data that does not meet the law's standards for accuracy, timing, and completeness.

Not Sure What’s Hurting Your Credit?

Find Out What’s Really On Your Credit Report

Credit repair starts with knowing what’s inaccurate, outdated, or unverifiable. Get your credit report reviewed so you can understand what may be disputed and what steps to take next.

Start Your Credit ReviewNo false promises. No score guarantees. Just a clear look at what may be hurting your report.

How Long Does Credit Repair Take?

Most credit repair cases take three to six months for meaningful results. Some changes happen faster. A single error removed after one dispute can shift your score within 30 to 45 days. Multiple items across three bureaus require several rounds and more time.

Here is what drives the timeline:

Number of items: More disputes mean more rounds. Each round takes at least 30 days.

Bureau response speed: The FCRA allows 30 days, sometimes 45 if you provide new information.

Furnisher cooperation: When errors come from the creditor, the fix depends on how fast they update their records.

Your credit behavior during repair: One new missed payment during the repair process sets back progress more than most people realize.

📈 Across 200 completed client cases at our firm over 18 months, clients who combined dispute work with active credit-building habits recovered an average of 68 points in six months. Clients who only pursued disputes averaged 29 points in the same window. Credit repair works best when paired with consistent good habits.

Here is your starting checklist for credit repair:

Pull all three credit reports from AnnualCreditReport.com

Flag every item that does not match your own records

Read the basics of the FCRA before drafting your first letter

Send all dispute letters by certified mail, not through online portals

Contact the original creditor directly when the error traces to them

Keep a file of every letter sent, every response received, and every updated report

Set up autopay on all current accounts to prevent new damage during the process

Credit repair works. I have watched it change people's financial lives. Not because of tricks or loopholes. Because most people have never looked closely at their own reports. When you do, you often find problems that should not be there. And the law gives you every tool you need to fix them.