If you found TST on your credit report, you're probably trying to determine whether it's legitimate, how it got there, and whether it could affect your credit score.

Toast, Inc. is best known for its restaurant point-of-sale systems, payment processing services, and business financing products.

Because consumers and business owners often recognize the Toast brand but not the abbreviation "TST," seeing it on a credit report can create confusion.

At our Houston credit repair office, we frequently review credit reports where consumers believe an unfamiliar abbreviation indicates fraud or identity theft. In many cases, the entry is tied to a legitimate financing application, business account, or inquiry that was forgotten or misunderstood.

Knowing why TST appears on your report is critical whether any action is necessary.

What Is TST on My Credit Report?

TST often refers to Toast, Inc., a restaurant technology and payment processing company. If TST appears on your credit report, it's related to a business financing application, credit inquiry, payment processing account, or another financial relationship associated with Toast services.

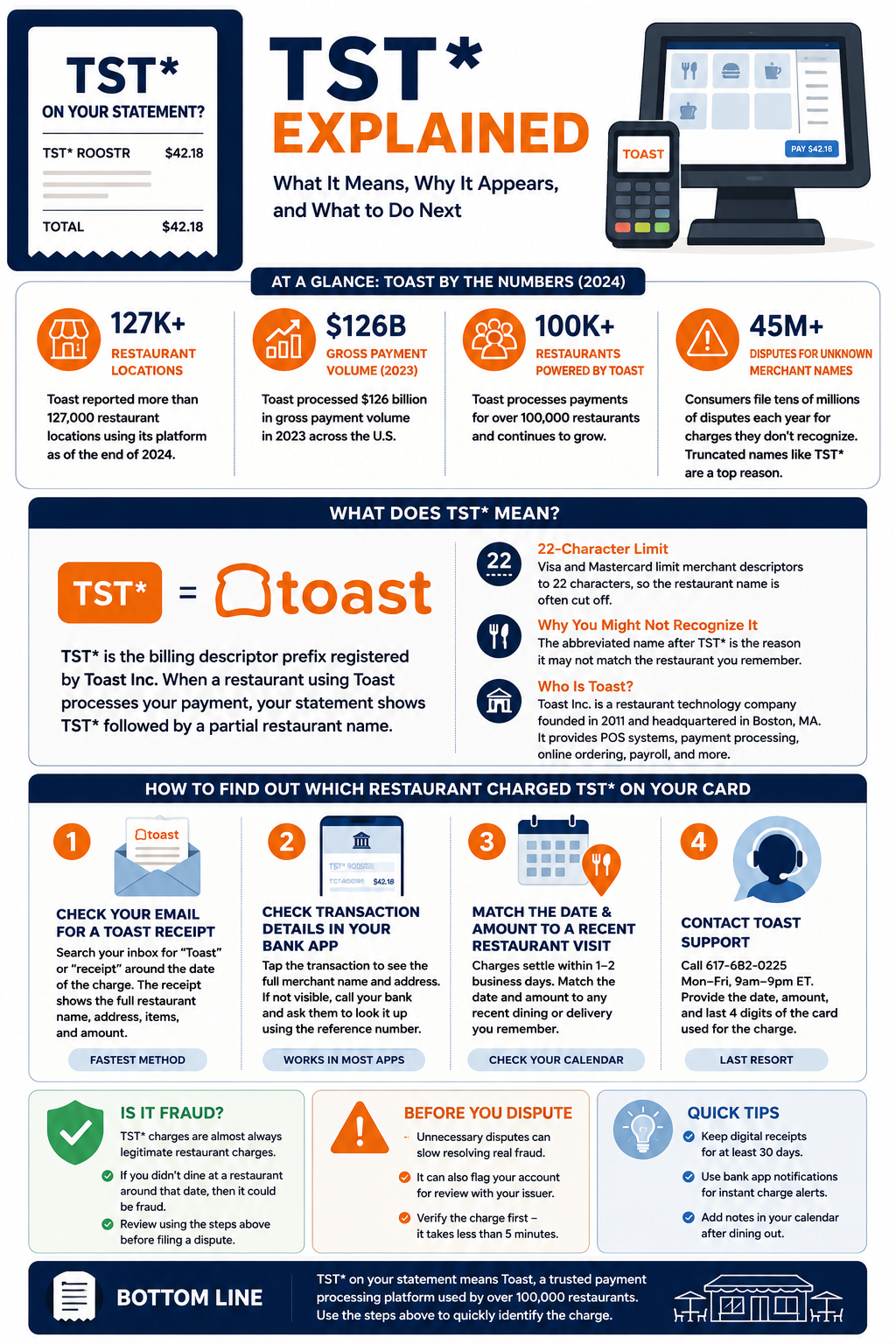

What Does TST* Mean on a Bank or Credit Card Statement?

TST* is the billing descriptor prefix registered by Toast Inc. with card networks including Visa, Mastercard, and American Express. When a restaurant that uses Toast processes your payment, the charge appears with TST* in front of a partial version of the restaurant's name. Visa and Mastercard limit merchant descriptors to 22 characters, which is why the restaurant name after TST* is often cut off and hard to recognize.

Toast Inc. is a restaurant technology company founded in 2011 and headquartered in Boston, Massachusetts. The company went public on the New York Stock Exchange in 2021 under the ticker TOST. Toast provides restaurants with point-of-sale hardware, payment processing, online ordering software, payroll tools, and kitchen display systems. Payment processing is a core part of its business, which is why TST* appears on so many restaurant charges.

The 22-character limit set by card network rules is the reason the restaurant name after TST* is truncated. A restaurant named "The Blue Bird Cafe and Bakery" becomes TST* BLUE BIRD CAF on your statement. "La Paloma Mexican Kitchen" becomes TST* LA PALOMA ME. If the name after TST* does not immediately match a restaurant you remember, that abbreviation is the reason, not fraud.

At ASAP Credit Repair USA, we educate clients on reading their statements carefully before filing disputes. An unnecessary dispute on a legitimate charge does not help your credit and can sometimes flag your account for review with your card issuer. Verifying a TST* charge before disputing takes less than five minutes using the steps in this article.

How to Find Out Which Restaurant Charged TST* on Your Card

Four methods identify the specific restaurant behind a TST* charge. Check your email for a Toast receipt. Look at the full transaction detail in your bank app. Match the charge date and amount to your calendar or any dining out you remember. Or call Toast's support line directly. Most people find the answer within two minutes using one of the first two methods.

Toast sends digital receipts by email or text when you provide contact information at checkout. Search your email inbox for "Toast" or "receipt" and filter by the date of the charge. The receipt shows the full restaurant name, address, itemized order, and the exact amount charged. This is the fastest method and works for most people who provided an email at the restaurant.

Fastest method | Works when you provided email at checkoutOpen your bank or credit card app and click on the TST* transaction. Most banks display the full merchant information behind the transaction, including the full business name and sometimes the address. This information is often more complete than what appears on a paper or PDF statement. If your app shows only TST* with no additional detail, call your bank's customer service line and ask them to look up the full merchant information using the transaction reference number.

Works with most major bank apps | Click the transaction for full detailNote the exact date and amount of the TST* charge. Think back to any restaurant visits on or around that date. Restaurant charges settle within one to two business days of the visit, so the statement date is close to the actual dining date. If you paid with a card at any restaurant in the past two to three days near the charge date, that is almost certainly the source. Check your calendar or any food delivery apps you use for context.

Works for people with consistent dining patternsToast's customer support can identify the specific restaurant behind a TST* charge when you provide the charge date, amount, and the last four digits of the card used. The general Toast support line is 617-682-0225. When you call, explain that you see a TST* charge on your statement and need to identify the merchant. This option takes more time than the first two but is useful when the charge amount or date does not match anything in your recent memory.

Last resort | Works when other methods failWhen Is a TST* Charge Actually Fraudulent?

A TST* charge is most likely fraudulent when you have not visited any restaurant in weeks, when the amount does not match any dining experience you would recognize, or when you see multiple TST* charges on the same day for amounts that look like test transactions. Small test charges such as $1.00 or $0.01 followed by a larger charge are a common fraud pattern. If any of those patterns apply, dispute the charge immediately.

- Amount matches a typical restaurant bill for your area.

- Date falls within the past two to three days of a dining out trip.

- You provided your email and have a Toast receipt in your inbox.

- The abbreviated name after TST* resembles a restaurant you recognize.

- Only one TST* charge for the date in question.

- The charge matches what you remember paying at the table.

- You have not eaten at any restaurant recently.

- The amount is a round number like $1.00 or $0.01 (test charge).

- Multiple TST* charges appear on the same day.

- The charge appears in a city or state you have not visited.

- The charge appeared on a card you rarely use for restaurants.

- Toast support cannot identify the merchant for the charge amount and date.

Card skimming at restaurants is a real and ongoing fraud vector. Criminals attach devices to card readers that capture card data when you swipe or insert. Toast's hardware does include tap-to-pay and chip reader options that reduce skimming risk, but not all restaurants use the most updated hardware. If you suspect your card data was captured at a restaurant, dispute the TST* charge, request a new card number, and monitor your statement for additional unauthorized charges over the next 30 days.

How to Dispute a TST* Charge You Do Not Recognize

Dispute a TST* charge through your card issuer's dispute process, not by calling Toast. Your card issuer is the party responsible for investigating unauthorized charges under the Fair Credit Billing Act for credit cards and Regulation E for debit cards. Toast is the payment processor. The issuer is who made you the account agreement and who has the legal obligation to investigate and credit you if the charge is unauthorized.

| Card Type | Law That Protects You | Dispute Window | Max Liability If Disputed |

|---|---|---|---|

| Credit card | Fair Credit Billing Act (FCBA) | 60 days from statement date | $50 maximum. Most issuers waive this entirely. |

| Debit card | Regulation E (Electronic Fund Transfer Act) | 2 business days from discovery for $50 limit. 60 days from statement for $500 limit. | $50 if reported within 2 days. $500 if reported within 60 days. Unlimited if after 60 days. |

| Prepaid debit card | Regulation E (2019 Prepaid Rule) | Same as debit card windows | Same as debit card limits. Prepaid cards have full Regulation E protection as of 2019. |

Most major card issuers allow you to open a dispute directly through the mobile app. Open the app, locate the TST* transaction, and look for a dispute or report a problem option. You enter a brief explanation, select unauthorized charge as the reason, and submit. The issuer issues a provisional credit within one to five business days while the investigation runs. If the investigation confirms the charge was unauthorized, the credit becomes permanent and you receive a new card number.

Does a TST* Charge Affect Your Credit Score?

A TST* charge on a credit card does not directly affect your credit score. Charges and payments on a credit card affect utilization and payment history, but the merchant name does not. If you dispute a legitimate TST* charge and the dispute is resolved in the merchant's favor, no credit impact occurs. If the dispute reveals fraud and your card is compromised, the impact comes only if fraudulent activity runs up your balance before you catch it, which raises your utilization ratio.

The connection between a TST* charge and your credit comes down to two scenarios. The first is a high balance from fraudulent charges that were not caught quickly. If a thief uses your card at multiple Toast-processing restaurants before you notice, the accumulated balance raises your credit utilization and can lower your score within the same billing cycle. The second is a dispute that results in a missed minimum payment because you withheld payment pending resolution. The Fair Credit Billing Act allows you to withhold payment on a disputed amount without penalty while the investigation runs, but only on the disputed portion and only if you followed the correct dispute process.

Unfamiliar Charges Leading You to Check Your Credit Report?

If a TST* charge or any unfamiliar transaction led you to pull your credit report and you found accounts or collection entries you do not recognize, a free 3-bureau audit shows every entry across Equifax, Experian, and TransUnion. Our team identifies what is accurate, what contains errors, and what may be disputable under the Fair Credit Reporting Act.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card requiredWhat does TST* mean on a Chase statement?

TST* on a Chase statement means the same thing as on any other card. It stands for Toast, a restaurant payment processing system. Chase processes the transaction the same way it processes any Visa or Mastercard purchase. The TST* prefix comes from Toast's registered merchant descriptor, not from Chase. If you see TST* on your Chase account and cannot identify it, open the Chase app, click the transaction, and the full merchant detail often appears below the statement descriptor.

Why does my statement show TST* instead of the restaurant name?

Card networks including Visa and Mastercard limit merchant billing descriptors to 22 characters. Toast registers its own merchant prefix TST* with card networks, and the remaining characters are used for the restaurant name. Most restaurant names are longer than the available space, so they appear truncated. A restaurant named "Magnolia Southern Kitchen" might appear as TST* MAGNOLIA SOUT. The truncation is a payment processing rule, not a sign that anything is wrong with the charge.

Can I get a refund for a TST* charge?

If the charge is fraudulent, your card issuer will refund it through the dispute process. If the charge is legitimate but you want a refund for another reason such as a problem with your order, you need to contact the restaurant directly. The restaurant processes refunds through their Toast system, and the credit typically appears on your statement within three to seven business days. Your card issuer cannot force a restaurant to issue a refund for a legitimate charge you authorized.

What is TST* on my Bank of America statement?

TST* on a Bank of America statement stands for Toast, the restaurant payment processor. Bank of America is the card issuer. Toast is the payment processor the restaurant uses. When the restaurant runs your card through Toast's system, Toast's merchant descriptor appears on the statement. The transaction is processed through Visa or Mastercard networks and Bank of America displays the descriptor exactly as Toast registered it, which is TST* followed by the restaurant name.

Does filing a dispute for a TST* charge hurt my credit?

No. Filing a billing dispute with your credit card issuer does not appear on your credit report and does not affect your credit score. The Fair Credit Billing Act gives you the right to dispute charges and the credit bureaus do not receive dispute information from card issuers. The only credit impact from a fraudulent TST* charge comes from the charge itself, if it raised your balance and therefore your credit utilization ratio before you caught it.

Found Something Unfamiliar on Your Credit Report Too?

An unfamiliar charge on your bank statement and an unfamiliar account on your credit report are two different problems, but they often show up together. If you found a collection entry, an account you do not recognize, or a hard inquiry you did not authorize on your Equifax, Experian, or TransUnion report, a free audit shows every entry and whether it is disputable. 20+ years in business. 3,000+ five-star reviews. 100% money-back guarantee on inaccurate item removal.

Get My Free Credit Blueprint → Secure · No hard inquiry · No credit card required-

402-935-7733 on Your Bank Statement: What This PayPal Charge Means The number 402-935-7733 is PayPal's billing phone number. It appears on statements when PayPal processed a purchase or subscription charge. This covers how to identify which PayPal transaction it corresponds to, how to tell if it is fraud, and how to dispute it if you did not authorize it.

-

JPMCB Card on My Credit Report: What It Means If checking your credit after seeing an unfamiliar charge, you may find JPMCB on your report. It stands for JPMorgan Chase Bank and appears when you have any Chase-issued card. This covers which cards show as JPMCB, how to dispute an unauthorized inquiry, and what to do if the account is not yours.

-

Unknown Collection Agency on Your Credit Report: How to Remove It If an unfamiliar charge led you to pull your credit and you found a collection agency you do not recognize, this covers your rights under the Fair Debt Collection Practices Act, how to request debt validation, and how to dispute an inaccurate or unverified collection entry under the Fair Credit Reporting Act.