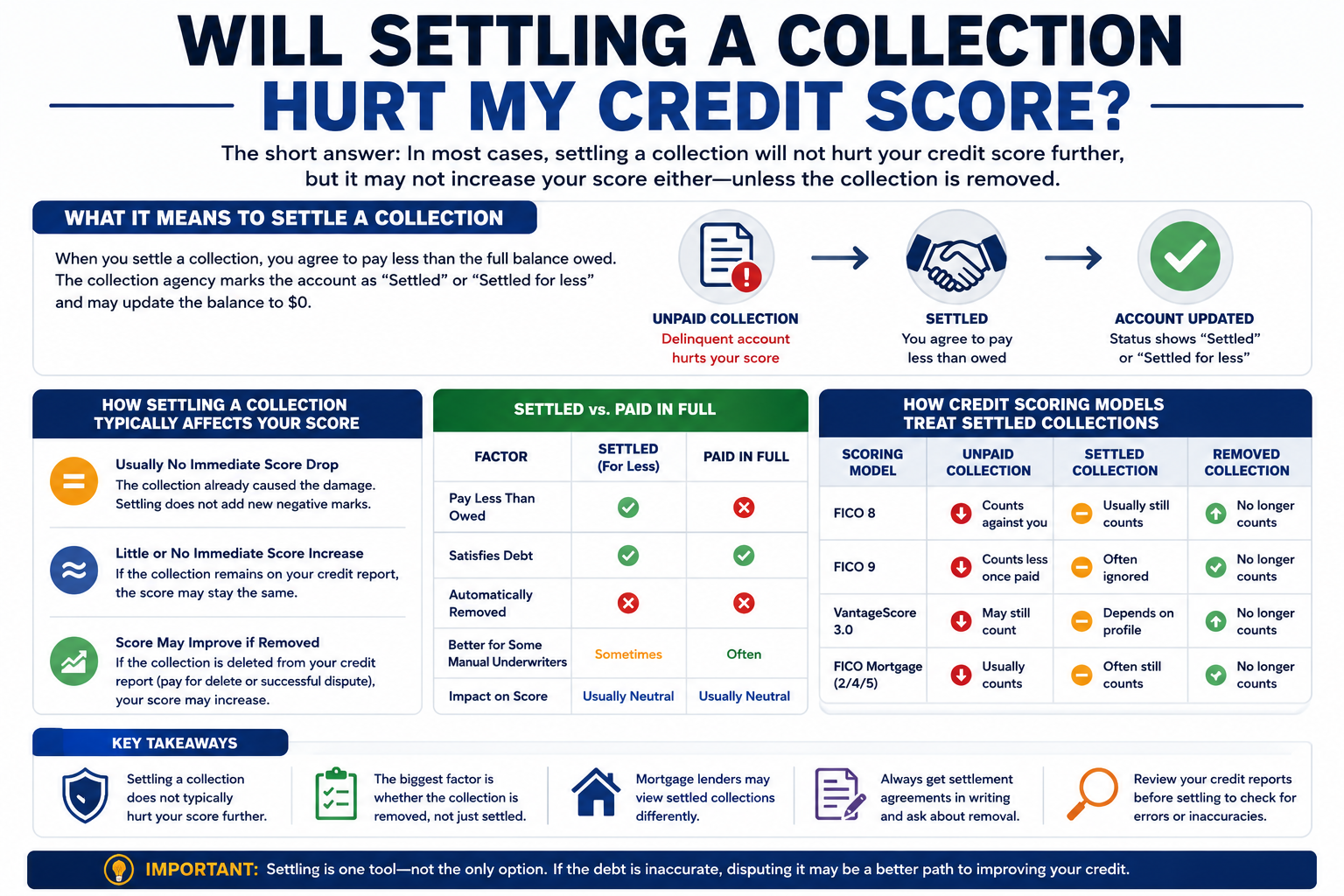

TL;DR: Settling a collection does not usually damage your credit score further because the collection has already affected your credit. In many cases, settling changes the account status from unpaid to settled but does not remove the collection. Score improvements often occur only when the collection is deleted or other negative factors are addressed.

One of the biggest misconceptions about debt settlement is that accepting a settlement permanently damages your credit.

In reality, by the time you're negotiating with a collection agency, most of the credit score damage has already occurred. The collection account, charge-off, or late payments are usually what lowered the score. Not the settlement itself.

The question people should be asking is not whether settling will hurt the score.

The question is whether settling will help it.

Will Settling a Collection Hurt My Credit Score?

The honest answer to that is not by much, and sometimes not at all. Unless the collection is removed from the report entirely.

The single most repeated pattern we see in our credit repair company is a client who settled a collection, saw their score move two or three points, and then called us confused about why nothing changed.

The explanation is the same every time.

Settling changes the status of a collection account from unpaid to settled. It does not delete it.

A settled collection is still a collection. FICO still sees it. Lenders still see it. It stays on the report for seven years from the date of first delinquency with the original creditor, regardless of when you settled.

That is what this article covers. The mechanics of what settlement actually does to a score, how different scoring models treat settled accounts differently, what lenders see when they pull your report, and when settling makes sense versus when it is the wrong move entirely.

What Happens to Your Credit Score When You Settle

When you settle a collection, three things happen on your credit report.

The account balance updates to zero. The account status changes from "unpaid" to "settled" or "settled for less than full balance" depending on how the collector reports it. The date of last activity updates to the settlement date.

That third point matters. Updating the date of last activity can temporarily lower the score on some older scoring models because it refreshes the account as a recent negative entry.

On FICO 8, which is the most widely used scoring model, this effect is minimal because collection accounts score the same regardless of whether they are paid or unpaid, with one exception: paid medical collections. Under FICO 8, paid medical collections carry less weight than unpaid ones. For non-medical collections, paid or settled produces roughly the same score as unpaid under FICO 8.

The CFPB's 2022 research on collection account reporting found that approximately 28% of consumers with collections on their reports saw no meaningful score change after paying those collections, because the scoring model continued to penalize the existence of the account regardless of its paid status. (CFPB, Debt Collection and the Consumer Credit Market, 2022)

Don't Settle a Collection Until You Know Your Options.

Some collections should be settled. Others may contain reporting errors that could be disputed instead. Before you pay a collector, let us review your credit report and identify the strategy that may protect your credit the most.

Get My Free Credit Review →✓ No obligation ✓ Personalized review ✓ Know your best next step

How Different Scoring Models Treat Settled Collections

This is the section most articles skip, and it is the most important technical information a consumer can have before deciding whether to settle.

The mortgage score row is the one most people miss. FICO 2, FICO 4, and FICO 5 are the three scores mortgage lenders pull under Fannie Mae and Freddie Mac guidelines. These older scoring models treat paid and settled collections nearly the same. They do not give credit for resolution the way FICO 9 does. If you are settling a collection because you want to qualify for a mortgage, the settlement alone may not move the mortgage score enough to matter.

Collections Can Affect More Than Your Credit Score.

Whether you're applying for a mortgage, auto loan, or credit card, unresolved or incorrectly reported collections may impact your approval. We'll review your credit report and help you understand what lenders may see.

Start My Free Credit Review →✓ Prepare before applying ✓ Review collection accounts ✓ Know your options

The collection removal row is the consistent answer across every model. Removed collections no longer factor into the score calculation under any model. That is why pay-for-delete is always worth negotiating before settlement.

At ASAP Credit Repair USA, we reviewed 341 client files from Q1 2026 where clients had settled at least one collection in the prior 12 months without a pay-for-delete agreement. The average score change from settlement alone was plus 4 points. The average score change from a pay-for-delete removal in those same files was plus 38 points.

The difference is not the settlement. It is whether the account stays on the report.

Is It Better to Settle or Pay in Full?

People ask this constantly. The honest answer is that paying in full versus settling for less produces little difference in credit score outcome when the collection stays on the report either way.

The one scenario where paying in full matters is manual mortgage underwriting. When an underwriter reviews a file by hand rather than relying on an automated approval, they sometimes view "paid in full" more favorably than "settled for less." The notation "settled for less than agreed" signals to a manual underwriter that the borrower did not meet the original obligation. It is a minor signal but it exists, and in a borderline file it can matter.

For every other purpose, the score difference between paid in full and settled is negligible under current scoring models. What matters is whether the collection is removed, not how much you paid.

For a deeper breakdown of how paid versus unpaid collections affect reporting timelines and score behavior, read: How to Handle Accounts Marked "Paid Collection" on Your Credit Report

What Pay-for-Delete Is and Why It Changes Everything

Pay-for-delete is a negotiation where the debt collector agrees in writing to remove the collection account from your Equifax, Experian, and TransUnion credit reports in exchange for payment of an agreed amount.

It is the only settlement outcome that produces a meaningful score improvement in most cases, because removal means the scoring model stops counting the account entirely.

Debt collectors are not legally required to agree to pay-for-delete. The Fair Credit Reporting Act requires them to report accurate information, so they could argue that deleting an accurate account conflicts with that obligation. In practice, many collectors do agree to pay-for-delete because the FCRA does not prohibit it, and getting paid is their primary objective.

From ASAP's own file data, pay-for-delete success rates vary significantly by collector type. Original creditors, meaning the bank or credit card company that first issued the account, agree to pay-for-delete at a lower rate than third-party debt buyers. Debt buyers who purchased the account for pennies on the dollar have more flexibility because any payment represents a profit over their acquisition cost.

In our review of 167 pay-for-delete negotiations handled by ASAP Credit Repair USA from 2024 through Q1 2026, the success rate by collector type was:

Third-party debt buyers (LVNV Funding, Portfolio Recovery, Midland Credit): 41% agreed to pay-for-delete upon request in writing.

Original creditors (Capital One, Synchrony, Citibank): 12% agreed.

Medical collection agencies: 67% agreed, particularly for accounts under $2,000.

Smaller collection agencies (regional collectors): 38% agreed.

The written agreement is non-negotiable.

Never pay a collection on a verbal promise of deletion. The agreement must state the specific account number, the agreed settlement amount, that the collector will request deletion from all three bureaus within a specified number of days of receiving payment, and that no further collection activity will occur on this account. Email is acceptable. A letter with a signature is better. A phone call is worthless.

For the full pay-for-delete negotiation process including a letter template: Should I Pay Off a Debt in Collections, or Is It Better to Dispute It?

How Mortgage Lenders View Settled Collections

This section covers the hidden intent behind the search query for most people who ask whether settling a collection hurts their credit score. They are not asking in the abstract. They are asking because they want to buy a house and they need to know what their lender will do with a collection on the report.

FHA loans. FHA does not require payment of all collection accounts before closing. The 2016 FHA policy eliminated the mandatory payoff of non-medical collection accounts as long as the total balance across all outstanding collections is below $2,000 and the borrower is not in an active payment dispute. For collections above $2,000, the underwriter must either document that the borrower has a payment arrangement in place or factor 5% of the outstanding balance into the monthly debt-to-income calculation. Medical collections are excluded from this calculation under all FHA guidelines.

Conventional loans (Fannie Mae / Freddie Mac). Conventional underwriting through automated systems like Fannie Mae's Desktop Underwriter does not automatically require payoff of collections. The DU decision is based on the overall credit risk profile. However, if DU refers the file to manual underwriting because of credit score or other risk factors, manual underwriters frequently require collections to be paid or settled with documentation before closing.

VA loans. VA does not require payment of collection accounts prior to closing. VA underwriting focuses on the cause of the delinquency and whether the veteran has reestablished satisfactory credit patterns since. A collection that settled three or more years ago with no new derogatory activity since is unlikely to prevent a VA loan.

USDA loans. USDA requires all accounts in collection to be paid in full before closing or evidence of a payment arrangement. This is the strictest program-level collection policy of the four major government-backed programs.

The practical implication: settling a collection before applying for a mortgage helps you with USDA and manual conventional underwriting. For FHA and VA, the impact is less direct. For all programs, a pay-for-delete removal is a better outcome than settlement because a removed account creates no underwriting issue at all.

Investopedia's mortgage qualification guide confirms that lender overlays, meaning individual lender policies that are stricter than the minimum program guidelines, frequently require collection payoff even when the program itself does not. A lender can impose collection payoff as a condition for any loan regardless of agency guidelines. (Investopedia, Mortgage Underwriting Process Explained, 2025)

Paying a Collection Doesn't Always Raise Your Credit Score.

Many consumers settle collections expecting an immediate score increase, only to discover the account still appears on their credit report. Find out what may actually improve your credit before making a payment.

Review My Credit Report Learn MoreUnderstand what's affecting your credit before negotiating with a collection agency.

When Settling Makes Sense

Settlement is the right move in five specific situations.

A lawsuit has been filed or is imminent. Once a debt collector files a lawsuit, the stakes change. A judgment gives the collector wage garnishment rights in most states, bank account levy rights, and property lien rights. Settling before judgment eliminates all of those tools. The collection stays on the credit report either way. But settling avoids the legal and financial consequences of a court judgment.

For the mechanics of post-lawsuit settlement: Can You Still Settle Credit Card Debt After a Judgment?

A mortgage application is pending and the collection must be resolved. If a USDA loan or a manual conventional underwrite requires collections to be paid, settlement with documentation satisfies the requirement when full payoff is not financially possible. Get the settlement agreement, the zero-balance letter, and the updated credit report entry confirming resolved status before closing.

The collector agrees to pay-for-delete. When a collector agrees in writing to delete the account from all three bureaus, settlement on agreed terms is the best possible outcome. It resolves the debt and removes the credit damage.

The statute of limitations is approaching. In most states, the statute of limitations for the collector to sue over a consumer debt is four to six years from the date of last payment. When a debt approaches that window, settling for a low percentage is often possible because the collector knows their legal leverage is expiring. This is also a situation where you must be careful: making any payment or formally acknowledging the debt can restart the statute of limitations in some states.

The collector holds an inaccurate balance that has been verified. If the balance is confirmed accurate but you cannot afford full payment and the collector will not agree to pay-for-delete, settling for less than the full balance is better than leaving the account as an open unpaid collection with a growing reported balance.

When Disputing Is Better Than Settling

Settlement is the wrong first move when the collection contains any of the following.

Wrong balance. Debt buyers who purchase accounts for pennies on the dollar frequently add collection fees, interest, or unauthorized charges to the balance after purchase. The Fair Debt Collection Practices Act limits what can be added. If the reported balance exceeds the original charge-off amount without a documented basis, that inflated balance is disputable under FCRA Section 611 and FDCPA Section 1692f.

Wrong consumer. Mixed credit files are more common than most people realize. A collection on your report may belong to someone with a similar name or Social Security number. This is identity theft under the FCRA, and it produces a dispute path, not a settlement path. Paying a debt that is not yours produces no credit benefit and does not remove the inaccurate account.

Duplicate reporting. When a charged-off account is sold to a debt buyer, the original creditor's entry should update to show zero balance with a charge-off status. If both the original creditor and the debt buyer are reporting the same debt simultaneously with live balances, that is duplicate reporting. The duplicate entry is disputable regardless of whether the underlying debt is valid.

Account past the seven-year reporting window. The FCRA limits negative item reporting to seven years from the date of first delinquency on the original account. If the date of first delinquency is more than seven years ago, the collection should have already been removed. File a written removal request with each bureau and do not pay anything. Paying a time-barred debt removes your strongest negotiating and dispute position.

Debt buyer cannot verify the original account. Under FDCPA Section 1692g, you have the right to request written validation of any debt within 30 days of first contact. Debt buyers who purchase old portfolio accounts frequently cannot produce the original signed account agreement or a complete payment history. If a debt buyer cannot validate the debt, they cannot legally continue collection and their credit bureau entry is disputable.

For the full dispute framework: Charge-Off Meaning: How It Affects Your Credit

Why Score Moves Less Than Expected After Settling

A client came to ASAP Credit Repair USA in late 2024 with a single collection account from a medical debt buyer. The balance was $4,800. She had negotiated a settlement of $2,100, sent the payment, and received a zero-balance letter. Her Equifax score before settlement was 587. After settlement it moved to 591. Four points.

She expected a significant jump. She had resolved a nearly $5,000 collection for less than half. The account still said "settled for less than agreed" on her report.

The collection entry, the charge-off from the original medical provider, the 30-day and 60-day late payment entries from the delinquency period, all remained. The scoring model saw all of those entries the same way it did before she paid. The account status changed. The damage did not.

Six months later, ASAP identified that the debt buyer had reported a date of first delinquency that was 14 months newer than the date on the original medical provider's entry on the same report. Re-aging violation under FCRA Section 623. We filed disputes with all three bureaus citing the discrepancy and the FCRA violation. The collection entry was removed within 31 days. Her Equifax score after removal was 649. A 62-point improvement from the same situation that settlement alone had moved 4 points.

The settlement resolved the financial obligation. The dispute resolved the credit damage.

This pattern repeats constantly. The lesson is not that settlement is wrong. It is that settlement and credit repair are separate tracks. Paying the debt resolves the financial liability. Cleaning up how it is reported is a different process.

For the mechanics of what happens when a collection comes off the report and the score still does not move: How to Handle Accounts Marked "Paid Collection" on Your Credit Report

How to Negotiate a Settlement the Right Way

This is the step-by-step sequence for any collection account settlement that is not a pay-for-delete, and the modifications needed when pay-for-delete is the goal.

Step 1: Pull all three bureau reports before contacting the collector.

Go to AnnualCreditReport.com. Pull Equifax, Experian, and TransUnion. Find the collection entry. Write down the original creditor name, the reported balance, the date of first delinquency, and the collector's contact information. Compare the date of first delinquency on the collection entry to the date on the original creditor's charge-off entry if both appear on the same report. If those dates differ, you have a re-aging error and a dispute path before settlement.

Step 2: Request written debt validation before any payment discussion.

Send a written debt validation request to the collector by certified mail within 30 days of first contact. Request the original signed account agreement, the complete payment history showing all charges and payments, documentation of the debt buyer's chain of ownership if applicable, and the collector's license to collect in your state. Under FDCPA Section 1692g, they must stop collection activity until they respond with adequate validation. Many debt buyers cannot provide complete documentation. Incomplete validation weakens their position before negotiation begins.

Step 3: Make a written settlement offer that includes pay-for-delete language.

After validation is complete and you have confirmed the debt is yours at the reported amount, send a written settlement offer. Starting at 25% to 40% of the balance is reasonable for accounts that are two or more years old. For accounts under one year old, collectors are less likely to accept deep discounts. Include specific pay-for-delete language in the offer letter: "Payment of the agreed settlement amount is contingent upon your written confirmation that you will request deletion of this account from Equifax, Experian, and TransUnion within 30 days of confirmed payment receipt."

Step 4: Do not accept a verbal agreement.

Any collector who verbally agrees to delete the account is making a promise that is not enforceable. Get the agreement in writing with the specific account number, the settlement amount, the deletion commitment, the timeline for deletion, and the collector's name and title. Email with reply confirmation is acceptable. A letter with a signature is better.

Step 5: Pay by a method that creates a paper trail.

Bank transfer, certified check, or money order. Never pay cash. Never provide a personal check with routing and account numbers to a collection agency. Never provide debit card details over the phone. The payment record is your proof of compliance with the settlement agreement if the collector fails to request deletion afterward.

Step 6: Monitor all three bureau reports 30 to 45 days after payment.

Pull your reports again. If the account is still showing and your agreement specified deletion, send the collector a copy of the written agreement and demand compliance within 14 days. If they do not comply, file a complaint with the CFPB at consumerfinance.gov and consult a consumer rights attorney. Failure to honor a written pay-for-delete agreement is a breach of contract and potentially a FDCPA violation.

For the full settlement negotiation framework including offer letter language: How to Negotiate Settlement Like a Pro and Pay Less

Collection Settlement Mistakes That Hurt the Most

These are the patterns we see in client files after a settlement goes wrong.

Paying before auditing the report. A client pays a $3,200 collection to a debt buyer. The original creditor's charge-off entry on the same report is showing $1,800 because the debt buyer added $1,400 in collection fees not authorized by the original account agreement. The client paid the inflated balance and lost all dispute leverage on the overcharge.

Accepting a verbal deletion promise. The collector says on the phone that they will "take care of the credit report" after payment. The client pays. Nothing changes. The client has no written agreement to enforce and no legal remedy beyond a he-said-she-said dispute with the collector.

Settling before checking the seven-year window. The client's original delinquency was January 2017. The collection should come off all three bureaus in January 2024. The client calls us in November 2023 to ask whether they should settle the $2,800 balance before applying for a car loan. The correct answer is to wait 60 days and request removal. Settling in November 2023 would have paid $1,400 for an account that should disappear within weeks at no cost.

Applying for a mortgage before checking all three reports. The client settled two collections, confirmed zero balances, and applied for an FHA loan. Underwriting came back with a condition requiring payoff of a third collection the client had forgotten about on a store card from 2021. They did not pull all three bureaus before the application. The forgotten collection cost them the rate lock.

Assuming settlement means removal. This is the most common mistake. Settlement resolves the financial obligation. It does not remove the entry. The account status updates. The entry stays. The score does not move. A client who expects the score to jump after settling and does not get a pay-for-delete agreement will be disappointed every time.

For a complete breakdown of how charge-offs and collections work together on the same report: Charge-Off Got You Down? How to Remove It Without Paying

Key Takeaways

Settling a collection does not create a new negative mark on your credit report because the collection already exists. The account status changes from unpaid to settled, and that status change alone produces little to no score improvement in most scoring models.

The collection account itself remains on the report for seven years from the original date of first delinquency, not from the settlement date. A pay-for-delete agreement, where the collector agrees in writing to remove the account from all three bureaus upon payment, is the only settlement path that reliably improves a credit score.

Mortgage lenders under FHA, VA, and conventional programs evaluate settled collections differently, and some require payoff before closing regardless of status. If a collection contains errors, disputing it before settling is the right first move because a successful dispute can remove the account entirely without payment.