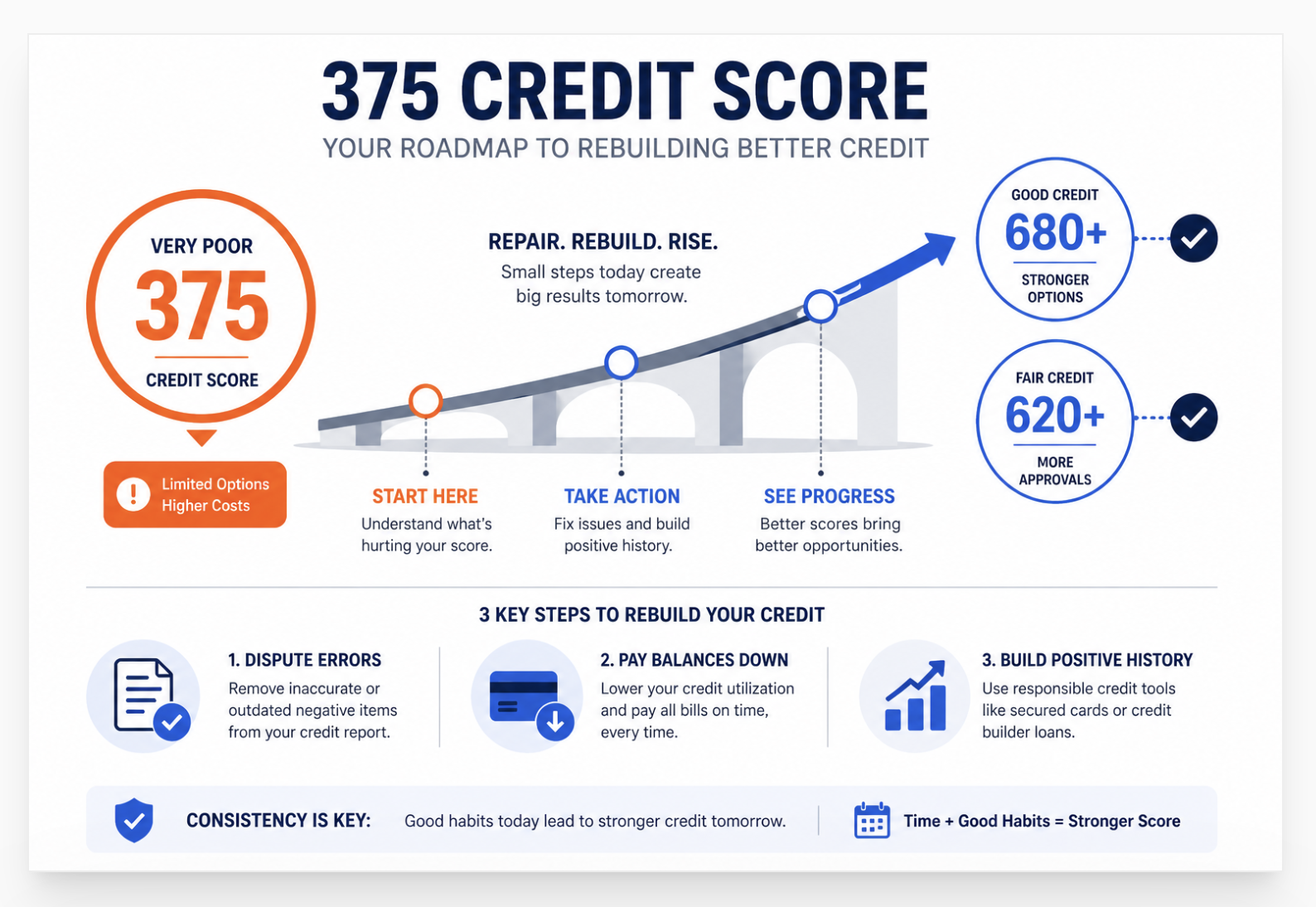

A 375 credit score is considered very poor credit. It usually signals serious negative marks in the credit file. That may include charge-offs, collections, missed payments, maxed-out balances, repossessions, or bankruptcies. Approval options at this level are limited, borrowing costs are high, and many lenders may decline applications outright. But a 375 score does not tell the full story. The credit file behind the score matters even more.

This is a number that we don’t often see at ASAP, but we still have some cases and scores in this range that are some of the most important files we work on because the damage is often clear, but so is the path forward. One account I remember involved a client who came in with a score in the 300s after medical collections, late payments, and a repossession.

At first, it looked impossible. After correcting reporting issues, bringing current accounts into good standding, and rebuilding positive history, the file started moving. That is something we see often. Low scores can improve faster than people think when the right problems are fixed first.

Real borrower discussions on Reddit show that consumers with scores in the 300s often feel stuck. Many believe approval is impossible. That is not always true. Resources from the Consumer Financial Protection Bureau continues to show that payment history and amounts owed are major credit score factors. That means targeted changes can create meaningful movement, even from a very low starting point.

The better question is not only what a 375 credit score means, but what is causing it and what actions create the fastest recovery.

Last quarter alone, we worked with 41 clients whose first mortgage application was denied. In 27 of those 41 cases, the denial traced to a credit issue we identified on the first bureau audit. Sixteen of those 27 involved at least one inaccurate entry suppressing the score. Nine clients had their errors removed within 45 days and reapplied successfully within 90 days of the original denial. The adverse action notice told them exactly where to look.

First Mortgage Application Denied: Start Here

When your first mortgage application gets denied, the lender must send a written adverse action notice within 30 days listing the specific reasons. Read that notice first. It identifies whether the denial came from credit, income, DTI, property, or documentation. Each reason has a different fix and a different timeline. Do not reapply until you address the specific cause listed.

Mortgage denial stings. For first-time buyers, it can feel like the door to homeownership just closed permanently. It did not. Denial is a diagnosis, not a verdict.

The Equal Credit Opportunity Act requires every lender to tell you specifically why they denied your application. That notice , called an adverse action notice , arrives within 30 days. It contains more useful information than most people realize. The reasons listed are not vague. They are specific enough to act on.

Common reasons listed on adverse action notices:

- Credit score below program minimum

- Debt-to-income ratio too high

- Insufficient employment history

- Insufficient income for the requested loan amount

- Incomplete application or unverifiable documentation

- Derogatory credit history (collections, charge-offs, late payments)

- Property did not meet appraisal or condition requirements

Each listed reason is a task. Fix the task, reapply. As the CFPB's mortgage consumer guide confirms, adverse action notices give you legal rights to the specific information behind the denial , you can use that information to appeal, correct errors, or improve your profile before a new application.

The 6 Most Common Mortgage Denial Reasons and How to Fix Each One

The hard minimums by loan type: FHA requires 500 (10% down) or 580 (3.5% down). Conventional loans require 620. Most FHA lenders set their own overlay at 620-640. USDA and VA have no official minimums but most lenders require 580-620 in practice.

Credit score denials hit in two ways. Either you fall below the program floor entirely, or you qualify technically but the score means a higher rate, stricter conditions, and additional documentation requirements that your file cannot meet.

The fastest score improvement actions: dispute inaccurate entries at all three bureaus simultaneously (30-45 days, 30-60 points per removed item), reduce credit card utilization below 10% on every card (one billing cycle, 20-40 points), and get added as an authorized user on an aged clean account (30-60 days, 20-50 points). Our credit repair guide for first-time home buyers covers the specific FICO models lenders use , FICO 2, 4, and 5 , which score files differently from the FICO 8 you see on Credit Karma.

DTI measures your monthly debt payments as a percentage of your gross monthly income. Lenders use two DTI figures: the front-end ratio (housing costs only) and the back-end ratio (all monthly debts). Most conventional loans cap the back-end DTI at 43-50%. FHA allows up to 56.9% with compensating factors. The 28/36 rule covers this in detail , our full breakdown of the 28/36 DTI rule and mortgage qualifying explains each ratio and which loan programs enforce which limits.

A DTI denial means one thing: your monthly debt load relative to income disqualified the loan amount you applied for. You have four levers: reduce your monthly debt payments, increase verifiable gross income, apply for a smaller loan amount, or use a loan program with a higher DTI ceiling (FHA instead of conventional).

Last quarter, we identified 14 ASAP Credit Repair clients whose DTI dropped below the qualifying threshold after paying off one specific debt. In most cases, it was a car loan or a high-balance credit card with a large minimum payment. Eliminating that one monthly obligation freed $300-$500 in DTI room, which moved them from denial territory to approval territory without changing the home price or income.

Credit score and DTI together cause over 60% of first mortgage denials. Credit score denials usually fix in 60 to 90 days through disputes and utilization reduction. DTI denials fix through debt payoff , targeting the debt with the highest monthly payment, not the highest balance. Both are solvable. The adverse action notice identifies which one applies to your file.

Mortgage lenders verify every dollar of income with documents , not just your word. W-2 employees typically need two years of W-2s, recent pay stubs, and employment verification. Self-employed borrowers need two years of tax returns, a year-to-date profit and loss statement, and sometimes a letter from a CPA.

Income denials come from three sources. First, income that cannot be documented , cash income, informal payments, or undeclared side work. Second, inconsistent income history , a job change in the past 12 months, gaps in employment, or a drop in income from year one to year two on tax returns. Third, self-employment losses shown on tax returns that lenders count as negative income, reducing your qualifying amount.

The specific fix depends on which income problem caused the denial. For documentation gaps: gather the missing documents before reapplying. For employment gaps: most lenders want 12 consecutive months at the current employer before approving. For self-employment: lenders use a two-year average of your net self-employment income from Schedule C. If year two shows higher income than year one, waiting until the higher-income year has 24 months of history may help.

Incomplete application denials are the most straightforward to resolve. The adverse action notice lists exactly which documents were missing, wrong, or unverifiable. These denials have nothing to do with your credit profile or financial strength. They happen when a document arrives unsigned, a bank statement is missing a page, an employer verification form is incomplete, or a required disclosure was not returned in time.

Gather every listed missing item. Confirm the format the lender needs , some want PDFs, some want originals. Reapply with the same lender immediately. Most will process the corrected application without a new hard credit pull if the original pull was recent and conditions have not changed.

A property appraisal denial is the only reason on this list that has nothing to do with your personal financial profile. The appraisal found either that the home was worth less than the purchase price, or that the property's condition failed to meet the loan program's minimum standards.

FHA loans have strict property condition requirements. Peeling paint, broken windows, roof damage, and certain structural problems can disqualify a property even at full market value. Conventional loans have fewer property condition requirements but will still decline if the appraisal comes in below the purchase price.

Options when a property fails appraisal: negotiate the purchase price down to match the appraised value, require the seller to fix the condition issues before closing, make up the difference in cash between the appraised value and purchase price, or walk away using the appraisal contingency in your offer. For FHA property condition denials specifically, asking the seller to complete the required repairs often resolves the issue before the next appraisal inspection.

Some mortgage denials cite not the credit score itself but specific derogatory items on the report. An active collection account above a certain threshold. A charge-off within the past 12 months. A 30-day late payment that appeared in the past 12 months , some lenders require 12 months of clean history above a score threshold before approving.

Lenders who use manual underwriting (which most FHA files require below 620) review individual items, not just the score. A 610 score with one recent 30-day late payment looks different to an underwriter than a 610 score with a clean 24-month payment history and a charge-off from 5 years ago.

Collection accounts require a decision before reapplying: pay-for-delete (most effective but not always possible), dispute if inaccurate, or wait. The rule for waiting: a collection account's damage to your score diminishes over time. A collection from four years ago hurts less than one from six months ago, even if the balance is identical. Some lenders have internal policies excluding collections over a certain age from underwriting review regardless of the score.

Can You Reapply for a Mortgage After Being Denied?

Yes. No mandatory waiting period exists after a mortgage denial. You can reapply immediately. However, applying again with the same file produces the same denial. Address the specific cause listed on your adverse action notice first. Then reapply , with the same lender or a different one. Most first-time buyers who fix the denial reason close within 6 to 12 months of the original application.

The denial does not go on your credit report. It does not follow you to other lenders. It does not create a waiting period at the FHA, VA, or Fannie Mae level. The hard inquiry from the original application stays on your report for two years but only affects your score for 12 months.

Switching lenders after denial makes sense in specific situations. A different lender may use different overlays , internal standards stricter than the federal program minimum. One lender may decline a 605 score FHA application because their internal floor is 620. Another lender may approve the same file at 605 because they operate at the FHA minimum with no overlay. The loan program's rules stay the same. Each lender's internal standards differ.

| Denial Reason | Reapply Timeline | Same Lender? | Key Action |

|---|---|---|---|

| Credit score , just below minimum | 60-90 days | Yes or different | Disputes + utilization paydown first |

| Credit score , well below minimum | 6-18 months | Different lender, same program | Full credit rebuild required |

| DTI too high | 30-90 days | Same lender fine | Pay off target debt first |

| Income insufficient | 90 days to 2 years | Same or different | Document income change or apply for lower loan amount |

| Missing documents | Days to weeks | Same lender , call them first | Gather and resubmit immediately |

| Property appraisal | Negotiation-dependent | N/A , property issue not credit | Renegotiate price or find different property |

Per Bankrate's mortgage denial guide, borrowers who shop multiple lenders after a single denial frequently find approval , not because their file changed, but because different lenders apply different overlays to the same program minimums. Always get the specific denial reason before deciding whether to fix and reapply with the same lender or shop elsewhere immediately.

How Long After Mortgage Denial Can I Reapply?

No waiting period is required after a mortgage denial. You can reapply the next day. The question is not when to reapply , it is whether you have fixed the denial reason. Most lenders require at least 30 to 90 days of changed circumstances before a new application produces a different outcome. Applying immediately with an unchanged file wastes time and adds a hard inquiry.

The one exception: FHA loans after foreclosure or bankruptcy. FHA imposes specific waiting periods after major derogatory events. A Chapter 7 bankruptcy requires a 2-year waiting period from discharge before FHA eligibility restores. A foreclosure requires a 3-year wait. A deed-in-lieu of foreclosure requires 3 years. Conventional loans have slightly different timelines. These waiting periods are program requirements , not lender preferences , and cannot be waived without documented extenuating circumstances.

Gather the required documents, resubmit to the same lender. No waiting period. The lender may process the corrected file within 30 days without a new credit pull if conditions are unchanged.

File disputes immediately at all three bureaus. Pay card balances to below 10% utilization. Get added as an authorized user. Reapply after 60 days of improvement. Request a rapid rescore from your lender for faster score update.

Pay off the target debt. Wait one statement cycle for the updated balance to report. Confirm the DTI calculation with your loan officer. Reapply with updated bank statements showing the payoff. Most lenders recalculate DTI with the payoff letter even before the statement closes.

Significant score rebuilding takes time. Add a secured credit card, get added as an authorized user, dispute all inaccuracies, and maintain zero new missed payments. Six months of consistent positive behavior typically produces 50-100 points of improvement for borrowers in the 550-580 range.

FHA requires 2 years from the bankruptcy discharge date. Conventional requires 4 years from discharge. Use the waiting period to rebuild credit aggressively , starting on the discharge date , so the score at the 2-year mark qualifies for the best available rate rather than the minimum threshold.

No mandatory waiting period follows a mortgage denial. The timeline to reapply depends entirely on how long it takes to fix the denial reason. Documentation denials resolve in days. DTI and credit score denials resolve in 60 to 90 days for most borrowers. Bankruptcy and foreclosure carry FHA-specific waiting periods of 2 and 3 years respectively. Shopping multiple lenders simultaneously within a 45-day window counts as a single credit inquiry under FICO's rate-shopping rules.

Does a Mortgage Denial Hurt Your Credit Score?

No. A mortgage denial does not lower your credit score. The hard inquiry from the application costs 5 to 10 points and stays on your report for 12 months of score impact (2 years on record). The denial decision itself adds no negative mark. Multiple mortgage inquiries within a 45-day window count as one inquiry under modern FICO models.

Your credit report shows credit applications and payment behavior. It does not show approval or denial decisions. A lender reviewing your report for a car loan or credit card two months from now sees the mortgage inquiry. They do not see that the application was denied.

The real concern after a denial is the additional inquiry from a new application. If you reapply with a second lender immediately, that generates a second hard pull. Under FICO 8 and newer models, all mortgage inquiries within a 45-day shopping window count as one. Inquiries outside that window each count separately.

As NerdWallet's mortgage denial guide notes, the most damaging thing you can do to your credit score after a denial is opening new credit accounts while the mortgage process continues. New accounts reduce average account age, add hard inquiries, and in some cases increase your apparent debt obligations , all of which move you further from approval, not closer to it.

Checking your own credit report to understand what the underwriter saw costs nothing and triggers no inquiry. Pull your reports from AnnualCreditReport.com freely. Then read them with the adverse action notice in hand and compare what you see against what the lender listed. Our guide on building clean credit files across all three bureaus covers the simultaneous dispute process that removes inaccurate entries from all three reports within the same 30-day investigation window.

What should I do first after my mortgage application is denied?

Read the adverse action notice. Federal law requires lenders to send it within 30 days of denial. It lists the specific reasons your application failed. Each reason tells you exactly what to fix. After reading the notice, call your loan officer and ask for a detailed explanation of each listed reason , specifically the score or DTI number that caused the denial versus the number required for approval. That gap tells you how far you need to move and how long it will take.

Can I reapply with the same lender after denial?

Yes. Most lenders will reconsider your application after you fix the denial reason without requiring a completely new application process. Call the loan officer who handled your file. Ask what documentation they need to reopen the file and whether a new credit pull is required. Some lenders recalculate DTI or score with a payoff letter and updated documents without restarting the process. Others require a fresh application. Know which one applies before resubmitting.

Should I try a different loan program after denial?

Yes, if the denial came from program-specific requirements. A conventional loan denial at a 610 score does not mean an FHA denial , FHA accepts 580 and above (some lenders accept 550). A denial for insufficient funds for 20% down may qualify under FHA at 3.5% down. A veteran denied for a conventional loan may qualify for a VA loan with no down payment. Review every loan program available for your score, income, and property type before concluding that homeownership is not currently possible.

How can I improve my chances of approval the second time?

Fix every specific item on the adverse action notice before reapplying. Pull all three bureau reports and dispute any inaccurate entries immediately. Reduce credit card balances below 10% utilization on all cards. Do not open any new credit accounts, apply for any loans, or miss any payments between now and reapplication. Get pre-qualified with multiple lenders within a 45-day window to understand exactly which programs you currently qualify for and what changes produce approval. Come back to the application with documented improvements , a paid-off debt, a corrected credit entry, or an updated bank statement , not just a request to reconsider.

9 of 16 Clients With Credit-Related Denials Closed Within 90 Days of Their First Audit

The adverse action notice tells you the reason. A 3-bureau audit tells you what is on your report that caused it. Inaccurate entries, wrong balances, and incorrect dates are disputable. Removing them moves your score faster than any payment strategy. A free audit shows exactly what Equifax, Experian, and TransUnion report right now.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card required-

Why You Got Approved for Pre-Mortgage Then Denied at Closing Pre-approval is a conditional offer based on your profile at one moment in time. Closing denial comes from what changed between application and underwriting. This covers the 6 most common closing-stage denial reasons , new debt, credit score drop, employment change, low appraisal, unverified deposits, and title issues , with the exact rules for each and how to protect your file during the period between pre-approval and closing day.

-

Buying a Home With a Low Credit Score: Tips That Work If your mortgage denial came from a credit score below the program minimum, this covers the specific strategies for buying with a score in the 580-640 range. FHA program details, lender overlay differences, down payment assistance programs that do not require perfect credit, and the exact credit actions that produce the fastest score movement into the qualifying range for each loan type.

-

Is 621 a Good Credit Score? Many first mortgage denials happen at scores between 610 and 635 , close to but not at the conventional 620 floor or common lender overlays. This covers exactly what a 621 score gets you across loan programs, the rate difference between 621 and 660, and the fastest actions that move a score from the low 600s into the range where approval becomes straightforward rather than borderline.

Remember, 375 Credit Score

A 375 credit score is low, but it is not permanent. Credit scores respond to behavior, reporting accuracy, and time. When the right issues are addressed, movement can happen faster than many people expect.

Start by finding what is dragging the score down most. Then build a plan around that. Remove errors, reduce balances, and create fresh positive history.

A low score is a starting point, not the final result.