What Does a 674 Credit Score Mean?

If you have a 674 credit score, you're in the "good" credit range. This puts you ahead of many Americans but still leaves room for improvement. Your score shows lenders that you handle credit fairly well, but you might have some areas that need work.

Think of your credit score like a report card for how you manage money. A 674 is like getting a B- or C+. It's decent, but with some effort, you could easily get an A.

According to FICO, the average credit score in the United States is 717 as of April 2024. This means your 674 score is about 43 points below the national average.

But don't worry because this gap is totally manageable to close.

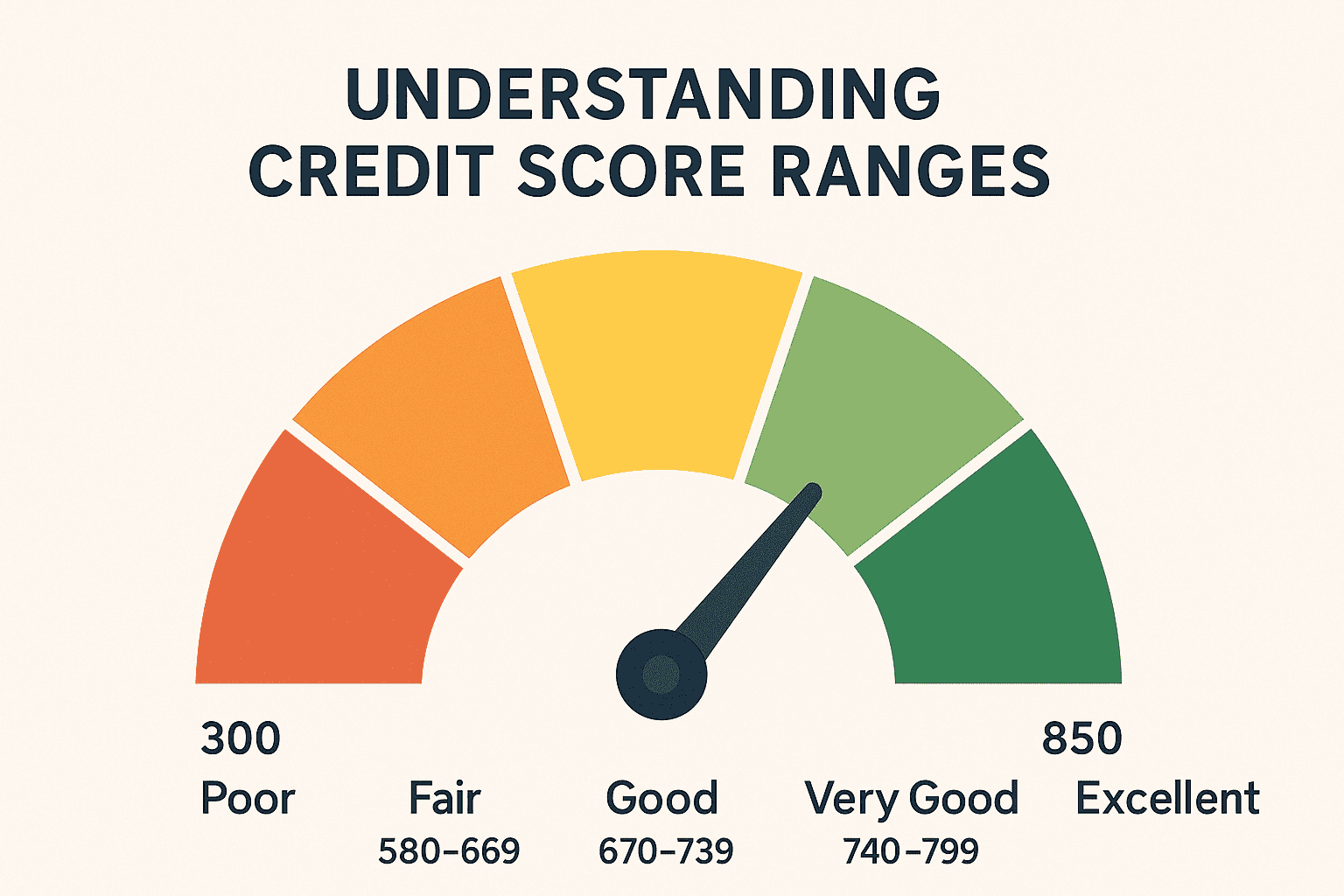

Understanding Credit Score Ranges

Here's how credit scores break down:

Your 674 score puts you in a solid position. You're not struggling like someone with poor credit, but you're also not getting the absolute best deals, yet.

Knowing The Different Credit Scores Scoring Model

FICO vs VantageScore

Your 674 score might be different depending on which scoring model is used:

FICO Scores (Most Common):

- Used by 90% of top lenders

- Ranges from 300-850

- Has industry-specific versions (auto, mortgage, credit card)

- Your mortgage FICO might be 20-30 points different from your credit card FICO

VantageScore:

- Used by Credit Karma and some monitoring services

- Also ranges 300-850 but calculates differently

- Often shows higher scores than FICO

- Less commonly used by actual lenders

This is why you might see different scores on different websites. Always ask lenders which score they use when making decisions.

Why Your Scores Vary Between Bureaus

Your score might be:

- Experian: 674

- Equifax: 668

- TransUnion: 682

This happens because:

- Not all lenders report to all three bureaus

- Information might be updated at different times

- Each bureau might have slightly different information about you

What You Can Get With a 674 Credit Score

Credit Cards You'll Qualify For

With a 674 score, most credit card companies will approve you. You can get:

- Cash back credit cards

- Travel rewards cards

- Cards with 0% interest for new purchases

- Balance transfer cards to pay off other debts

However, you might not qualify for premium cards like the Chase Sapphire Reserve or American Express Platinum. These cards usually want scores of 740 or higher.

Example: Sarah has a 674 credit score and applied for a cash back credit card. She got approved with a $5,000 credit limit and 18% interest rate. If she had a 740+ score, she might have gotten a $10,000 limit and 15% interest rate.

Loans Available to 674 Credit Score

Your 674 score opens doors to most types of loans:

- Home Loans: You can definitely get a mortgage. FHA loans are easy to qualify for with your score. Conventional loans are also possible. You'll pay a bit more in interest than someone with excellent credit, but not too much more.

- Auto Loans: Car dealerships and banks will lend to you. Expect interest rates between 6-12% depending on the loan term and your income.

- Personal Loans: Available from banks, credit unions, and online lenders. Interest rates typically range from 10-18%.

What You Might Not Get

Some financial products prefer higher credit scores:

- Premium credit cards with the best rewards

- The absolute lowest mortgage rates

- Unsecured personal loans over $50,000

- Some business credit cards

What's Probably Hurting Your Score

Most people with 674 credit scores have one or more of these issues:

High Credit Card Balances

This is the biggest problem for most people. If you're using more than 30% of your credit limits, it hurts your score. For example, if you have a $1,000 credit limit and owe $400, that's 40% usage - too high.

Late Payments

Even one late payment can drop your score significantly. A single 30-day late payment might cost you 60-110 points depending on your overall credit history.

Limited Credit History

If you're young or new to credit, you might not have enough history for a higher score. Credit scoring likes to see several years of responsible credit use.

Too Many New Accounts

Applying for lots of credit cards or loans in a short time can hurt your score. Each application creates a "hard inquiry" that temporarily lowers your score.

How Much Your 674 Credit Score Costs You

The difference between a 674 score and excellent credit can cost thousands of dollars over time.

Mortgage Example: According to Investopedia, the interest rate difference can be 0.75% higher for a borrower with a 620 FICO score versus a borrower with a 740+ FICO score. On a $300,000 home loan, this could mean paying $75,000 more over 30 years.

Scenario: Mike has a 674 credit score and got approved for a $250,000 mortgage at 7.2% interest. His monthly payment is $1,695. If he had a 740+ score, he might have gotten 6.5% interest with a monthly payment of $1,580. That's $115 less per month, or $1,380 per year!

Credit Cards: If you carry balances, higher interest rates cost you more every month. The difference between 18% and 15% interest might seem small, but it adds up quickly.

Your Step-by-Step 674 Credit Score Improvement Plan

Month 1: Get Organized

- Check your credit reports from all three credit bureaus (Experian, Equifax, TransUnion) at annualcreditreport.com

- Look for errors like accounts that aren't yours or wrong payment histories

- Set up automatic payments for all your bills to prevent future late payments

- Calculate your credit utilization on each card

Month 2-3: Attack High Balances

- Pay down credit cards to under 30% of their limits

- Focus on the highest utilization cards first

- Make multiple payments per month if needed to keep balances low

- Don't close old credit cards - this hurts your credit history length

Month 4-6: Build Good Habits

- Keep utilization under 10% on all cards

- Pay all bills on time, every time

- Don't apply for new credit unless absolutely necessary

- Consider asking for credit limit increases on existing cards

Month 7-12: Fine-Tune Your Strategy

- Monitor your progress with free credit monitoring

- Dispute any remaining errors on your credit reports

- Consider becoming an authorized user on someone else's old, well-managed account

- Think about credit mix - having different types of credit (cards, car loan, etc.) can help

Advanced Tips for Faster Results

The Authorized User Strategy

Ask a family member with excellent credit to add you as an authorized user on their oldest credit card. This can boost your score by 20-50 points quickly. Make sure they:

- Have perfect payment history

- Keep low balances

- Have had the card for many years

Credit Utilization Tricks

- Pay your credit cards before the statement closes each month

- Keep one card with a small balance (1-3% of the limit) and pay the rest to zero

- Ask for credit limit increases but don't use the extra credit

Timing Your Applications

When you do need new credit, apply for multiple loans of the same type within 14-45 days. Credit scoring treats these as one inquiry instead of multiple hits to your score.

Mistakes to Avoid When You Have a 674 Credit Score

Don't Close Old Credit Cards

Even if you don't use them, old cards help your credit score by:

- Increasing your total available credit

- Lengthening your credit history

- Improving your credit mix

Don't Apply for Too Much Credit

Each application can lower your score by 5-10 points. Multiple applications in a short time look desperate to lenders.

Don't Ignore Small Balances

Even $10 left on a credit card counts toward your utilization ratio. Pay attention to all your accounts.

Don't Fall for Credit Repair Scams

Companies that promise to fix your credit quickly are usually scams. You can dispute errors yourself for free. Legitimate credit repair takes time and effort.

What to Expect: Your Timeline

- Months 1-2: Your score might dip slightly as you make changes and old negative items are still on your report.

- Months 3-4: You should see 10-20 points of improvement as your utilization drops and payment history improves.

- Months 6-8: Potentially 30-50 points higher if you've been aggressive about paying down balances and maintaining perfect payments.

- Months 12+: You could reach the 740+ "very good" range with consistent effort.

Remember, credit scoring is a marathon, not a sprint. Small, consistent improvements add up to big results over time.

Monitoring Your Progress

Use these free tools to track your improvement:

- Credit Karma: Provides VantageScore updates

- Your credit card companies: Many offer free FICO scores

- Your bank or credit union: Often provides free credit monitoring

- AnnualCreditReport.com: Free credit reports (but not scores)

Check your score monthly but don't obsess over daily changes. Scores fluctuate normally, and updates aren't instant.

Debt-to-Income Ratio: The Other Important Number

Your credit score is only half the story. Lenders also care about your debt-to-income ratio (DTI).

How to Calculate DTI

Total monthly debt payments ÷ Total monthly income = DTI

Example: If you make $5,000/month and have $1,500 in debt payments, your DTI is 30%.

DTI Requirements by Loan Type

Mortgages:

- Conventional loans: Usually want 36-45% DTI maximum

- FHA loans: Can go up to 57% DTI in some cases

- VA loans: More flexible, but typically prefer under 41%

Auto Loans:

- Most lenders want DTI under 35-40%

- Subprime lenders might accept up to 50%

Personal Loans:

- Traditional banks: Usually want DTI under 35%

- Online lenders: Might accept up to 45%

Improving Your DTI

- Increase income through side jobs or raises

- Pay down existing debt before applying for new loans

- Don't take on new monthly obligations before major purchases

Specific Credit Products for 674 Scores

Credit Cards That Typically Approve 674 Scores

With your 674 score, you're in a sweet spot where most credit card companies want your business. The Capital One Quicksilver is often a great first choice because it gives you 1.5% cash back on everything with no annual fee. If you're looking for something with higher rewards, the Citi Double Cash card offers 2% back, though you might get a lower credit limit initially.

For travel lovers, the Capital One Venture card could work well for you, giving you 2 miles per dollar spent. The Chase Sapphire Preferred might be a stretch at 674, but some people do get approved, especially if they have a good relationship with Chase already.

If you're carrying balances on other cards, a balance transfer card like the Citi Simplicity could save you hundreds in interest with its 0% intro rate. Just remember that most balance transfer cards charge a 3-5% fee upfront.

Store cards are usually easy approvals for 674 scores. The Target RedCard and Amazon Prime Visa are popular choices because you can use them anywhere, not just at those specific stores.

Best Lenders for 674 Credit Scores

When you're shopping for an auto loan with a 674 score, credit unions should be your first stop. They're member-owned, so they often offer better rates than big banks. If you're not already a member of one, many credit unions let you join for a small donation to a charity they support.

Car Loans With 674 Credit Score

For online auto lending, Capital One Auto Finance has a reputation for working with good credit borrowers and often beats dealer financing. Bank of America and Wells Fargo are solid choices too, especially if you already have accounts with them since existing relationships can sometimes help with approval odds.

674 Credit Score Personal Loans

Personal loans can be trickier, but SoFi tends to approve borrowers with good credit and steady income, even if the score isn't perfect. LightStream, which is part of SunTrust, specializes in debt consolidation loans and often has competitive rates for people in your credit range. Marcus by Goldman Sachs is another online option that's been getting good reviews from borrowers.

Housing Loans For 674 Credit Score

For mortgages, don't just go with the first lender you find. Quicken Loans (now Rocket Mortgage) handles a lot of volume and can often move quickly, but local credit unions and community banks sometimes offer better rates. The key is to shop around and get quotes from at least three different lenders within a 45-day window so it only counts as one inquiry on your credit report.

How Credit Affects Your Daily Life

Utility Services

When you move to a new place, your 674 credit score should work in your favor with utility companies. Most electric, gas, and water companies will turn on service without requiring a deposit when they see your good credit history. If your score was in the poor range, you might be looking at deposits of $200-500, but at 674, you should be clear of those extra costs.

The same goes for internet and cable service. Companies like Comcast, Verizon, and AT&T typically check credit before setting up service, but your score should qualify you for their standard terms without any upfront deposits. If you were dealing with poor credit, these companies might ask for $100-300 per service line.

Cell Phone Plans

Your 674 score opens the door to postpaid cell phone plans from all major carriers. Verizon, AT&T, T-Mobile, and smaller carriers will likely approve you without requiring security deposits. These postpaid plans usually offer better phone deals and more features than prepaid options.

If your credit was lower, you might be looking at deposits of $200-400 per phone line, which can add up quickly if you're setting up a family plan. Some people with lower credit scores choose prepaid plans to avoid these deposits, but with your 674 score, you shouldn't need to compromise.

Insurance Rates

Here's something many people don't realize: your credit score can significantly impact your car insurance rates in most states. Insurance companies have found that people with better credit tend to file fewer claims, so they offer lower rates to good credit customers.

With your 674 score, you're probably getting decent rates, but if you could bump that score up to the 740+ range, you might save 10-25% on your auto insurance premiums. That could mean $300-600 less per year for a typical family. The states that don't allow credit-based insurance pricing are California, Hawaii, Massachusetts, and Michigan, so if you live in one of these states, your credit won't affect your car insurance rates.

Homeowners and renters insurance work similarly. Better credit usually means lower premiums, and poor credit can increase your rates significantly. When you're shopping for insurance, it's worth mentioning your good credit score to agents since some companies offer better rates than others for people in your credit range.

Apartment Rentals

Most landlords and property management companies want to see credit scores of 650 or higher, so your 674 score should open most doors. However, some competitive rental markets or luxury properties might prefer scores of 700+.

When you're apartment hunting, your good credit should mean you only need to put down one month's rent as a security deposit. If your credit was poor, you might be looking at two or three months' rent upfront, which can be a huge financial burden when you're trying to move.

Some landlords might ask for higher income requirements if your credit isn't perfect. Instead of the typical requirement of earning three times the monthly rent, they might want you to earn four times the rent. But with your 674 score, you should be able to meet the standard requirements at most places.

Employment and Credit

Jobs That Check Credit

If you're looking for work in banking, finance, or government positions requiring security clearance, employers will likely check your credit as part of the background process. Some retail jobs that involve handling money, insurance companies, and certain healthcare positions also review credit histories.

The good news is that employers don't see your actual credit score. They see a modified version of your credit report that shows your payment history and debt levels but not the three-digit number. They also can't see medical debt in most cases, and they must get your written permission before checking your credit.

Your 674 score suggests responsible financial management, which is exactly what these employers want to see. They're looking for people who pay their bills on time and don't have overwhelming debt that might tempt them to make poor decisions at work.

Protecting Your Credit During Job Search

If you're between jobs, protecting your credit becomes even more important. The stress of unemployment can make it tempting to skip bills or rely heavily on credit cards, but this is exactly when you need to be most careful.

Contact your lenders right away if you lose your job. Many have hardship programs that can temporarily reduce your payments or pause them entirely. It's much better to be proactive and call them before you miss a payment than to try to fix the damage afterward.

Consider picking up side income through gig work, freelancing, or part-time jobs to keep money coming in. Even a small income stream can help you maintain your minimum payments and keep your credit intact while you search for your next full-time position.

Legal Rights and Protections

Fair Credit Reporting Act (FCRA)

You have important rights when it comes to your credit information, and knowing these rights can save you time and money. The Fair Credit Reporting Act gives you the right to get one free credit report from each of the three major bureaus every year. You can spread these out and check one report every four months to keep a regular eye on your credit.

You also have the right to dispute any information on your credit reports that you believe is wrong. This includes accounts that aren't yours, incorrect payment histories, or outdated information that should have been removed. The credit bureaus have 30 days to investigate your dispute and either correct the information or explain why they're keeping it.

If someone has accessed your credit report, you have the right to know about it. You should receive notices when companies check your credit for lending decisions, and you can place fraud alerts on your file if you suspect identity theft.

Dispute Process

When you find an error on your credit report, online disputes are usually the fastest way to get results. The credit bureau websites have dispute forms that walk you through the process step by step. You'll need to explain what's wrong and provide any documentation you have to support your claim.

If the online dispute doesn't work, you can mail a dispute letter with copies of supporting documents. Keep copies of everything you send, and use certified mail so you have proof they received it. Follow up if you don't hear back within 30 days.

If the credit bureaus don't fix obvious errors, you can escalate your complaint to the Consumer Financial Protection Bureau. They track these complaints and often help resolve disputes that seem to be going nowhere.

Statute of Limitations on Debt

How Long Debts Can Be Collected:

- Credit cards: 3-6 years (varies by state)

- Medical debt: 3-6 years

- Auto loans: 4-6 years

- Mortgages: 6-20 years

Important: Debts can stay on credit reports for 7 years even after statute of limitations expires.

Debt Collector Rules

What They Can Do:

- Contact you about legitimate debts

- Report to credit bureaus

- Sue you for the debt (if within statute of limitations)

What They Cannot Do:

- Call before 8 AM or after 9 PM

- Call you at work if you tell them not to

- Threaten violence or arrest

- Discuss your debt with others

- Continue calling after you request written communication only

Financial Emergency Planning

Maintaining Credit During Hardship

If you lose your job or face a medical emergency, your first instinct might be to stop paying credit cards to focus on essentials like rent and groceries. While this makes sense from a survival standpoint, it can destroy your credit score and make your financial recovery much harder.

Instead, contact your lenders immediately when you realize you're facing hardship. Most credit card companies have programs to help customers going through tough times. They might temporarily reduce your minimum payments, lower your interest rates, or even pause payments for a few months.

Your mortgage lender also has options if you're struggling. Forbearance allows you to pause or reduce payments temporarily, while loan modification can permanently change your loan terms to make payments more affordable. The key is to call before you miss payments, not after.

Hardship Programs Available

Credit card companies don't advertise their hardship programs, but almost all of them have options for customers in financial distress. When you call, explain your situation honestly and ask specifically about hardship programs. You might be surprised by how willing they are to work with you, especially if you've been a good customer in the past.

Some programs let you make interest-only payments for a few months. Others might reduce your minimum payment or temporarily lower your interest rate. These programs can give you breathing room to get back on your feet without destroying your credit.

Mortgage forbearance became well-known during the COVID-19 pandemic, but it's always been available for borrowers facing genuine hardship. You can typically pause or reduce payments for three to six months, and some programs can be extended if needed. Just remember that you'll eventually need to make up the missed payments or modify your loan terms.

Building Emergency Fund

An emergency fund is your best protection against credit damage during financial hardship. Even $1,000 in savings can prevent you from missing payments during a short-term crisis like a car repair or medical bill.

Start small if you need to. Even $25 per month adds up over time, and you can increase the amount as your income grows or your debts decrease. Keep this money in a high-yield savings account where it earns interest but stays easily accessible.

Think of your emergency fund as insurance for your credit score. When unexpected expenses come up, you can pay them from savings instead of maxing out credit cards or missing payments. This keeps your credit healthy and gives you more options during tough times.

Regional and State Considerations

Geographic Credit Variations

High-Cost Areas:

- Lenders might accept higher DTI ratios

- Credit requirements might be more flexible

- Competition between lenders can mean better rates

Rural Areas:

- Fewer lender options

- Credit unions often have better rates

- USDA loans available for rural mortgages

State-Specific Credit Laws

Community Property States:

- Spouse's credit can affect you

- Debts acquired during marriage are joint

- Affects loan applications and credit decisions

Homestead Exemption States:

- Primary residence protection from creditors

- Affects mortgage and home equity decisions

- Varies significantly by state

Advanced Credit Optimization

Credit Mix Strategy

Ideal Credit Portfolio:

- 2-3 credit cards (different types)

- 1 installment loan (auto, personal, mortgage)

- Possibly a store card for specific benefits

- Mix of old and newer accounts

Types of Credit:

- Revolving: Credit cards, lines of credit

- Installment: Auto loans, mortgages, personal loans

- Open: Charge cards (full balance due monthly)

Advanced Utilization Strategies

Per-Card Optimization:

- Keep most cards at 0% utilization

- Keep one card at 1-3% utilization

- Never exceed 30% on any single card

- Pay before statement closes to control reported balances

Multiple Payment Strategy:

- Pay cards 2-3 times per month

- Track statement closing dates

- Make large purchases right after statement closes

- Pay off large purchases before next statement

Credit Age Optimization

Account Age Strategy:

- Never close your oldest card

- Keep second-oldest card active too

- Use old cards occasionally to keep them active

- Avoid closing cards unless there's an annual fee you can't justify

New Account Timing:

- Space new applications 3-6 months apart

- Apply for multiple cards of same type within 45 days if needed

- Avoid new accounts 6-12 months before major purchases

Special Situations

If You Need Credit Right Now

Sometimes you can't wait to improve your score. In these cases:

- Try credit unions, which are often more flexible

- Consider secured credit cards that require a deposit

- Look into "second chance" banking programs

- Check peer-to-peer lending platforms

- Ask family to cosign (carefully consider risks)

- Look into employer-based lending programs

If You're Planning a Major Purchase

Don't make credit changes 2-3 months before applying for a mortgage or car loan. Lenders want to see stability. Get pre-approved to understand your actual rates and terms.

Pre-Purchase Checklist:

- Don't apply for new credit

- Don't close existing accounts

- Don't make large purchases on credit

- Don't change jobs if possible

- Save extra money for down payment

If You Have Collections or Charge-Offs

These seriously hurt your score but become less important over time. Focus on paying current accounts perfectly while these age off your report (usually after 7 years).

Collection Strategies:

- Try to negotiate "pay for delete" agreements

- Get payment agreements in writing

- Consider settling for less than full amount

- Understand that paid collections still hurt your score

If You're Self-Employed

Special Challenges:

- Irregular income makes loan approval harder

- Need 2 years of tax returns for mortgages

- Profit and loss statements required

- Bank statements might be reviewed

Strategies:

- Keep detailed financial records

- Maintain higher credit scores to offset income uncertainty

- Consider stating income loans (if available)

- Work with lenders experienced in self-employed borrowers

If You're a Student or Young Adult

Building Credit Strategies:

- Student credit cards with lower requirements

- Secured credit cards to establish history

- Authorized user on parents' accounts

- Credit builder loans from credit unions

Avoiding Common Mistakes:

- Don't apply for too many cards at once

- Don't close your first credit card

- Don't max out cards even if you can pay them off

- Don't ignore credit while focusing on student loans

Long-Term Wealth Building

How Credit Affects Net Worth

Direct Impact:

- Lower interest rates = more money saved

- Better loan terms = more purchasing power

- Access to better credit products = more opportunities

Indirect Impact:

- Better insurance rates

- Lower deposits for services

- More housing options

- Some employment opportunities

Investment Considerations

Debt vs Investment Decision:

- Pay off high-interest debt first (credit cards)

- Consider investing while paying low-interest debt (mortgages)

- Emergency fund comes before aggressive investing

- Don't sacrifice credit health for investment returns

Credit as a Wealth Tool:

- Responsible use of credit can build wealth

- Real estate investing requires good credit

- Business financing needs strong personal credit

- Cash flow management through credit products

Building Long-Term Wealth

Improving your credit score isn't just about getting approved for loans. Better credit helps you:

- Save money on interest payments

- Get better insurance rates in some states

- Qualify for better apartments when renting

- Sometimes get better job opportunities (some employers check credit)

The money you save with better credit can be invested or saved for your future goals.

Action Plan Summary

Immediate Actions (This Week)

- Get your free credit reports from annualcreditreport.com

- Calculate your debt-to-income ratio

- Set up automatic payments for all bills

- List all your credit accounts and their balances

- Check which credit monitoring you have access to

30-Day Goals

- Pay down highest utilization cards to under 30%

- Dispute any errors found on credit reports

- Research specific credit products you might want

- Create a budget that prioritizes debt reduction

- Build or add to emergency fund

90-Day Goals

- Get all cards under 10% utilization

- Maintain perfect payment history

- Consider authorized user opportunities

- Track your credit score improvements

- Research lenders for any upcoming major purchases

12-Month Goals

- Reach 740+ credit score

- Have 3-6 months emergency fund

- Optimize your credit mix

- Prepare for major financial goals

- Build long-term wealth strategies

Final Thoughts

Your credit score affects much more than just loan approvals. It impacts your housing options, insurance costs, employment opportunities, and overall financial flexibility. The time and effort you invest in improving your credit will pay dividends for decades.

A 674 credit score is a good starting point, but it's definitely not your ending point. With focused effort and good habits, you can realistically reach 740+ within a year.

The key is to be patient and consistent. Don't get discouraged if progress seems slow at first. Every point of improvement is money in your pocket over the long term.

Ready to Fast-Track Your 674 Credit Score Improvement?

While you can certainly improve your credit on your own, working with professionals can accelerate your results and help you avoid costly mistakes. At ASAP Credit Repair, we specialize in helping people with credit scores like yours reach their financial goals faster.

Our experienced team knows exactly which strategies work best for 674 credit scores and can help you navigate complex credit situations, dispute errors effectively, and optimize your credit profile for maximum improvement.

Don't let another month pass with a credit score that's costing you money. Contact ASAP Credit Repair today for a free consultation and discover how we can help you unlock better rates, higher credit limits, and improved financial opportunities.

Call us now or visit our website to get started on your journey to excellent credit. Your future self will thank you for taking action today.

Related Content

610 Credit Score: What It Means, What You Can Get, and How to Improve It