A 677 credit score is considered "fair," allowing access to most loans and credit cards, but often with higher interest rates. It indicates some past financial issues, like missed payments or high balances, but lenders still see you as a manageable risk. With consistent on-time payments and debt reduction, it's possible to raise your score to "good" within a few months.

Alright, let’s talk about something we all care about but maybe don’t fully understand: credit scores. And not just any number, but that one that feels like it’s always almost there but not quite - the 677 credit score.

If you’ve got a 677 credit score or found out that’s where you land on your latest TransUnion credit score chart, you might be asking:

- Is 677 credit score ok?

- Can I get a loan with a 677 credit score?

- Am I screwed for getting a car or a credit card?

Think of your 677 credit score like getting a B- on a test. It's not failing, but there's definitely room for improvement. You're sitting in what credit experts call the "fair" range, which means you have some decent financial opportunities ahead, but also some challenges to work through.

Let’s break it all down.

Is 677 Credit Score Good or Bad?

It’s not good and it’s not bad either. It’s somewhere in the middle, confusing? Yeah, but not until you understand it.

The thing about credit scores is they're like a report card for your financial habits. A 677 credit score puts you right in the middle of the pack. If we’re being blunt, it’s like getting a C+ in school. You passed. But you’re not winning any awards.

According to Experian, credit scores typically fall into these buckets:

- Excellent: 800-850

- Very Good: 740-799

- Good: 670-739

- Fair: 580-669

- Poor: 300-579

Your 677 sits right at the border between "fair" and "good." It's like being on the edge of moving up to the next level in a video game - you're close, but not quite there yet.

Most lenders will work with you at this score level, but you might not get their best offers. Think of it like shopping for a car - you can still buy one, but you might not get the premium package at the discounted price.

Related Content: What Can You Get With a 700 Credit Score?

What Does Having a 677 Credit Score Really Mean?

First off, 677 is what lenders call a "fair" credit score. It’s not bad. But it’s not amazing either. Most credit scores fall between 300 to 850, and anything between 670 to 739 is considered "good", according to Experian.

So at 677, you’re on the lower end of that "good" zone, or right at the edge between fair and good. That means you’re doing alright, but you could use a bit of polish to unlock better deals.

How Lenders See You With a 677 Credit Score

When you have a 677 credit score, you're telling lenders that you've had some ups and downs with money. Maybe you missed a few payments here and there, or perhaps you're carrying more debt than ideal. It's like having a friend who usually shows up on time but occasionally runs late - reliable enough to trust, but with some room for improvement.

The credit bureaus like TransUnion calculate your score based on several factors. Your payment history makes up about 35% of your score, which is huge. Then there's how much you owe compared to your credit limits (30%), how long you've had credit accounts (15%), what types of credit you use (10%), and any new credit applications (10%).

With a 677, something in this mix isn't quite hitting the mark. Maybe you're using too much of your available credit, or perhaps there was a period where payments got a bit shaky.

What Can You Do With a 677 Credit Score?

Here’s the good news: you’re not locked out of opportunities. You can still get loans, credit cards, and even finance a car. But you'll probably pay more in interest.

So, what are your loan options with a 677 credit score?

Let's dig into the actuals.

Can I Get a Loan With a 677 Credit Score?

Yes, you can. But the type of loan and how much interest you’ll pay depends.

A 677 credit score personal loan is definitely possible. However, you'll want to manage your expectations about the terms you'll receive. Let’s say you’re eyeing a personal loan. According to Forbes, borrowers with a "fair" credit score can expect interest rates between 17.8% to 19.9% on average (Forbes). Yikes, right?

Personal loan lenders typically approve borrowers with fair credit, but your interest rate will be higher than someone with excellent credit. While someone with a 750+ score might get a personal loan at 6-8%, you might be looking at rates between 10-18%, depending on the lender and loan amount.

The key is shopping around. Different lenders have different appetites for risk. Some online lenders specialize in working with borrowers who have fair credit scores. Credit unions can also be more flexible than traditional banks because they're member-owned and often more willing to look at your whole financial picture, not just your credit score.

So while a 677 credit score personal loan is possible, it’s not going to be cheap.

677 Credit Score Car Loan: Yes or No?

Again, yes, but brace yourself.

Many lenders are willing to approve car loans for scores starting around 660 because the car itself serves as collateral. If you can't make payments, they can repossess the vehicle. But your interest rate could be higher.

For example, someone with a credit score above 720 might get a 4% rate on a new car loan. Someone with a 677 might get something closer to 8-10%. That’s a chunk of change over the life of a loan.

According to Experian's State of the Automotive Finance Market report, borrowers with credit scores between 661-780 received an average interest rate of 9.73% for new car loans and 15.08% for used car loans. Your 677 puts you right in this range.

Here's a pro tip: consider getting pre-approved for financing before you hit the dealership. This gives you negotiating power and prevents dealers from marking up your interest rate. Banks, credit unions, and online lenders all offer auto loan pre-approval.

Credit Card Options for a 677 Credit Score: Yay or Nay?

Here’s where things get better. Credit cards are a bit more flexible.

Finding the right 677 credit score credit card requires a bit of strategy. You won't qualify for premium rewards cards that require excellent credit, but you have several solid options.

Let me tell you bluntly that you’ll not get the top-tier cards with travel perks and cashback out the wazoo, but you can still get solid credit cards with decent limits.

Look for ones that help you build credit while offering a few basic rewards. There are credit cards designed for fair credit. These might include secured credit cards where you put down a deposit, or unsecured cards with modest credit limits. Some popular options include cards from Capital One, Discover, or Credit One Bank.

The goal with any new credit card should be improving your score. Keep your utilization low (under 30% of your limit, ideally under 10%), make payments on time, and resist the urge to max out your new card.

Expert advice: Avoid cards with annual fees if you can.

Is 670 Credit Score Good Compared to 677?

You might wonder about the difference between a 670 credit score and your 677. Honestly, they're pretty similar. Both fall in that "fair to good" range, and lenders will treat them roughly the same way.

The difference of seven points isn't huge in practical terms. You might see slightly better interest rates or terms with a 677, but we're talking small differences. Both scores suggest you're a moderate risk borrower who can access credit but might pay a bit more for it.

What’s Holding Your Score Back?

Let’s say you’re like Jake. Jake has a 677 credit score. He pays his bills, but sometimes late. He’s got two credit cards, both kinda close to their limits. And he once forgot to pay a $100 medical bill that went to collections. Classic.

These small things add up. And that’s where a debt collection company: 677 credit score could be a factor. If you have accounts in collections, even if they’re small, they drag you down. Clearing those or negotiating with debt collectors can give your score a quick boost.

You might be interested:Credit Score Recovery After Student Loan Problems: Timeline and Strategies

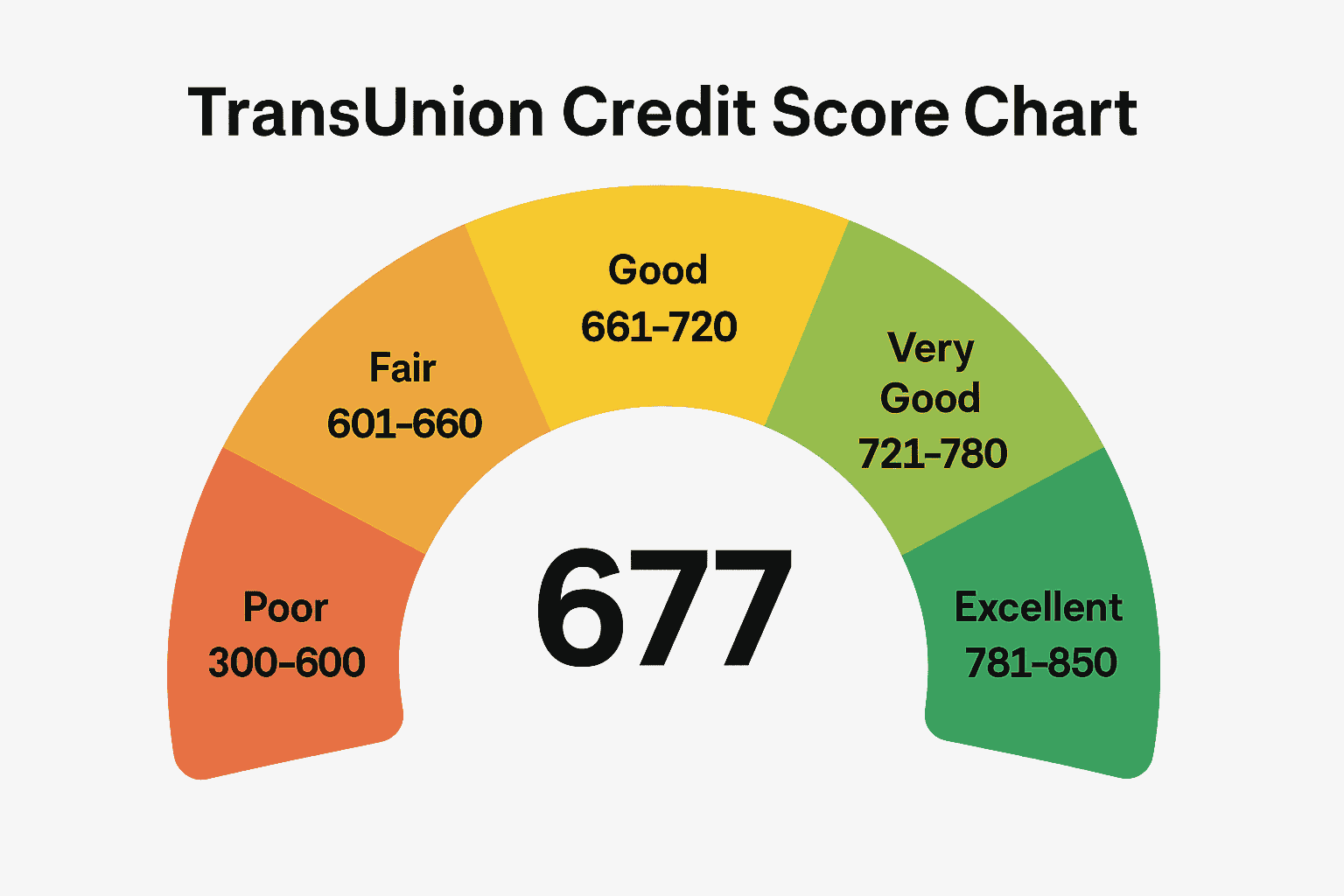

Understanding TransUnion Credit Score Chart

If you pulled your 677 credit score TransUnion report, you're looking at one of the three major credit bureau scores. TransUnion uses the VantageScore and FICO models, just like the other bureaus.

The TransUnion credit score chart shows that your 677 falls in their "Fair" category (601-660) or potentially "Good" category (661-720), depending on which scoring model they're using. Different lenders might pull from different bureaus, so your score could vary slightly between TransUnion, Experian, and Equifax.

Don't stress if you see small variations between bureaus. It's normal and happens because each bureau might have slightly different information about your credit history.

Common Problems People Face With a 677 Credit Score

Let me paint you a picture of what typically leads to a 677 credit score. Most people in this range share similar challenges.

High credit utilization is probably the biggest culprit. If you're using more than 30% of your available credit limits, it's dragging your score down. For example, if you have a $1,000 credit limit and you're carrying a $400 balance, that's 40% utilization - too high for optimal scoring.

Late payments also play a major role. Even one payment that's 30 days late can knock 60-110 points off your score. If you've had a few late payments in the past couple of years, they're still affecting your score.

Another common issue is having too many new credit inquiries. Every time you apply for credit, it creates a "hard inquiry" that can lower your score by a few points. Multiple inquiries in a short period can add up.

Some people also struggle with having too little credit history. If you're relatively new to credit or only have one or two accounts, there isn't enough information for the scoring models to give you a higher score.

Tips to Bump That 677 Credit Score Higher

The good news about having a 677 credit score is that you're in a sweet spot for improvement. Small changes can make a big difference when you're in the fair range.

- Pay down credit cards. Start with your credit utilization. Pay down your balances so you're using less than 30% of your available credit on each card. If possible, aim for under 10%. This can boost your score within a month or two.

- Pay on time, every time. Set up automatic payments for at least the minimum amount due on all your accounts. Payment history is the biggest factor in your credit score, so consistency here is crucial. Even one late payment hurts.

- Don’t close old accounts. Keep those credit lines open if possible.

- Check for errors. Sometimes credit reports have mistakes. Use sites like Credit Karma to check yours.

- Ask for limit increases. Consider asking for credit limit increases on your existing cards. This immediately improves your utilization ratio without requiring you to pay down balances. Just don't use the extra credit! More available credit = lower usage ratio.

- Remove Collections: If you have any collections or charge-offs on your report, consider negotiating pay-for-delete agreements. This means you pay the debt in exchange for the creditor removing the negative mark from your report. But the best way? Remove those items and you’ll see faster results. Don’t know how? Don’t worry, we can do it for you!

Other Financial Opportunities With a 677 Credit Score

Despite not being in the excellent range, a 677 credit score opens several doors.

You can still qualify for most types of credit, including mortgages, auto loans, personal loans, and credit cards.

Home Buying with a 677 Credit Score

For home buying, FHA loans accept credit scores as low as 580, and many conventional loans approve borrowers with scores around 620-640. Your 677 puts you in a comfortable position for mortgage approval, though you might not get the lowest interest rates available.

How About Having a Job?

Many employers run credit checks, especially for positions involving money handling. A 677 won't disqualify you from most jobs, though some highly sensitive financial positions might prefer higher scores.

Can I Rent an Apartment with a Fair Credit Score?

You can also qualify for most apartment rentals. Landlords typically look for scores above 600-650, so your 677 should clear most rental requirements.

Real Talk: Should You Worry About a 677 Score?

Nope. You shouldn’t panic. But you should take steps to improve it. Your financial future depends on it.

Here’s the deal: Credit impacts everything from getting a house to landing a job. A better score saves you thousands over time. Higher credit = lower interest = more money in your pocket.

And if you’re dealing with collections? Talk to a debt collection company: 677 credit score might sound like a weird phrase, but finding the right help can clean up your credit history faster than you think.

One More Thing…

Ever wonder what people are saying about this online? The 677 credit score reddit threads are filled with stories. Some folks climbed from 677 to 750 in a year. Others got stuck because they didn’t know what was dragging them down. The key is knowledge. You’ve got that now.

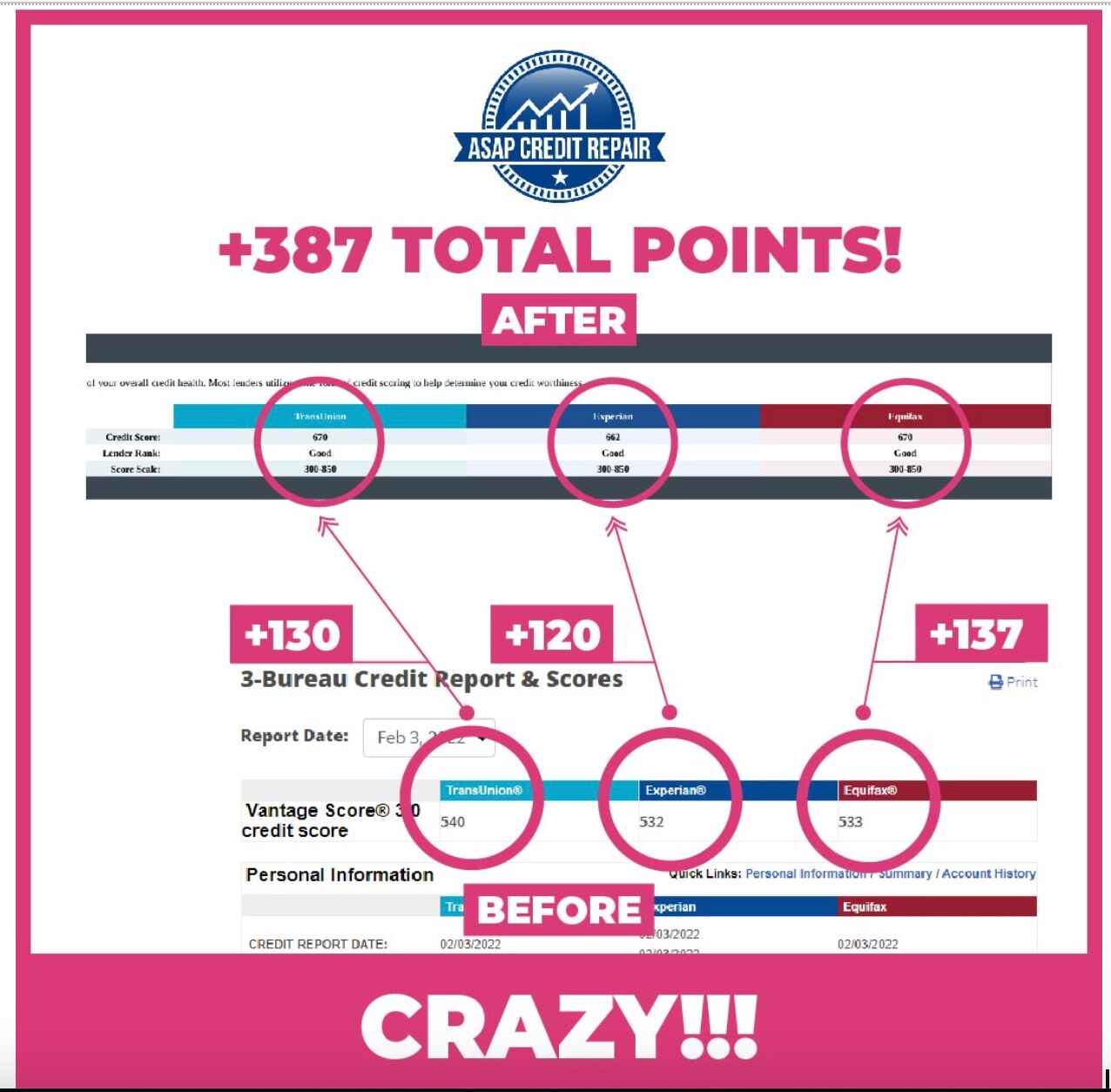

At ASAP Credit Repair, we’ve helped clients in this exact range take real steps to turn things around. From clearing up debt collections to improving credit habits, many went from 677 to the 700+ club in under a year. Some even qualified for better loan rates after just a few months of focused changes. So if you’re sitting at 677, know this — with the right strategy, you’re closer to "good" than you think.

Final Thoughts

Having a 677 credit score means you're in a transition phase. You're not in the danger zone where credit is hard to find, but you're also not in the sweet spot where lenders compete for your business with their best offers. The most important thing to remember is that credit scores aren't permanent. They change based on your financial behavior. A 677 today could easily become a 720 or higher within 6-12 months with the right strategies.

Here’s the plan:

- Tidy up your payments

- Lower your credit usage

- Avoid new debt you don’t need

- Keep your old accounts open

- Deal with any collections or errors fast

And hey, if you’ve read this far, that means you care about your financial future. That’s already a big step.

Remember, everyone's credit journey is different. What matters most is that you understand where you stand and have a plan to keep moving forward.

Your 677 credit score doesn’t define you. But what you do next? That totally does.