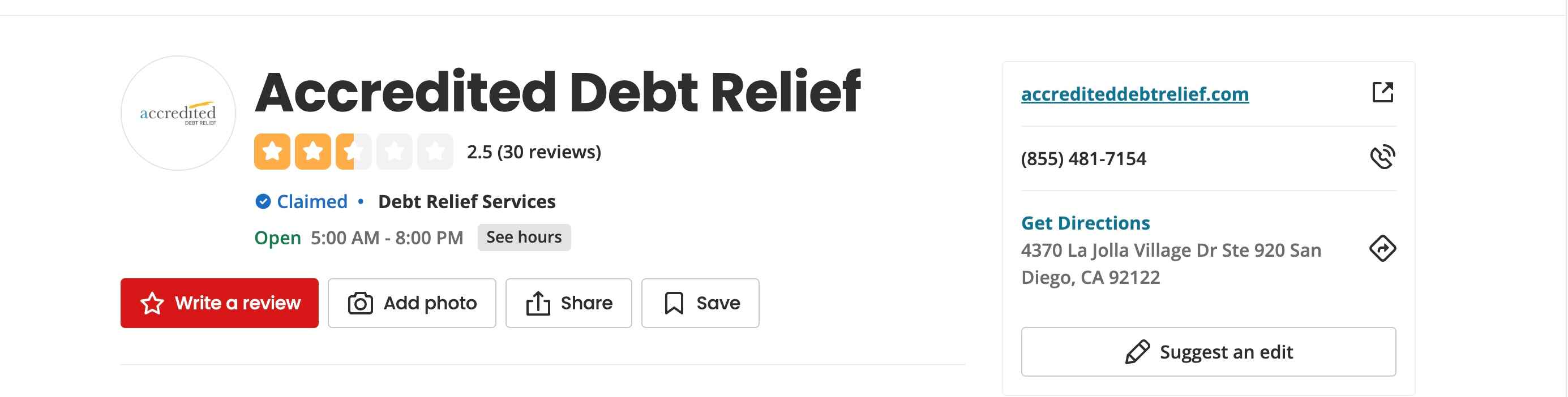

Accredited Debt Relief presents itself as a solution for those drowning in debt, promising to negotiate with creditors and reduce overall payments.

They paint a picture of financial ease, a way out of the overwhelming burden. But as Tom discovered, the reality can be a far cry from the promise. What starts as a beacon of hope can quickly turn into a financial nightmare, leaving you worse off than before. Let us share his story.

Tom had always been someone who worked hard and paid his bills.

But after a rough year—unexpected car repairs, medical bills, and a cut in hours at work—he found himself buried in credit card debt. Feeling overwhelmed and unsure of where to turn, he signed up with Accredited Debt Relief, a company that promised to lower his monthly payments and help him pay off his debts faster.

At first, it felt like a smart move. They told him to stop paying his credit cards and send money to them instead. So he did.

Month after month, Tom made his payments faithfully, hoping he was getting closer to financial freedom. But two years later, his credit score was worse than ever, collection calls hadn’t stopped, and none of the debts had been fully taken care of.

Frustrated, he finally reached out to ASAP Credit Repair to see if there was another way.

Is Accredited Debt Relief Legitimate?

After the shock wore off, Tom, being the practical guy he was, had to ask himself a crucial question: was he dealing with a scam, or just a really bad service?

He did his research, and yes, Accredited Debt Relief is a legitimate company, in the sense that they are registered and operate legally. But "legitimate" doesn't automatically translate to "effective" or "consumer-friendly," as Tom was about to discover.

🔎A quick search for "Accredited Debt Relief reviews" paints a pretty bleak picture.

🚩A mixed bag of feedback: Some positive, but mostly negative.

🚩A common thread of frustration and disappointment: Many users report similar experiences to Tom's.

🚩Promises unfulfilled: The promised debt relief often doesn't materialize.

🚩Credit scores tanking: Users frequently see their credit scores worsen.

🚩A general feeling of being misled: Many feel the company's marketing doesn't match the reality.

🚩An overwhelming sentiment of caution: Most reviews advise potential customers to proceed with extreme care.

The company has a website, they answer the phone, and they have legal paperwork. But that doesn't change the fact that their methods can leave you in a worse position than when you started.

😲 Tom realized that "legit" in this context meant they had the legal right to do what they were doing, even if what they were doing was causing him more harm than good.

Recommended Read: The Truth About Clear One Advantage – Why Jorge Chose a Different Path

How ASAP not “Accredited Debt Relief” Helped Tom Take Back Control

We didn’t just send a generic dispute letter. We dug deep and went after every piece of documentation that the collectors and credit bureaus are legally required to provide.

📌 For each of the 4 accounts, we requested:

- A copy of the original signed agreement or contract showing Tom’s obligation to pay

- An itemized breakdown of all charges and payments made on the account

- Proof of ownership transfer, showing the chain of custody from the original creditor to the current collection agency

- A copy of the last bill or statement sent before the account was sent to collections

- Documentation showing that Tom was notified, as required by law, before the account was reported to the credit bureaus

- Any communication logs proving the collector attempted to validate the debt within the required timeframe

- Metro 2 compliance formatting proof to ensure the account was reported in accordance with industry standards

In most cases, the collection agency or creditor was unable or unwilling to provide these documents.

That gave us leverage.

We sent follow-up notices to the credit bureaus, pointing out specific violations of the Fair Credit Reporting Act (FCRA) and Fair Debt Collection Practices Act (FDCPA). We demanded the immediate deletion of each account due to:

✅ Incomplete documentation

✅ Failure to validate the debt

✅ Reporting inaccuracies across different bureaus

✅ Lack of proper legal notices prior to reporting

Within just a few weeks, all 4 accounts were permanently deleted from Tom’s credit reports.

That’s how real credit repair works: not just disputes—but demands for legal proof and pressure where it counts.

The first thing we did was pull Tom’s full credit report.

We found several negative accounts still listed—including debts Accredited had supposedly “settled.” Some were still marked as unpaid. Others were showing as settled for less, which was keeping his credit score low.

We got to work:

✅ Sent out legal disputes to all three credit bureaus

✅ Requested full documentation from the creditors

✅ Challenged any inaccurate, outdated, or unverifiable information

Within just weeks, we had multiple accounts removed from Tom’s credit report.

His score jumped—and he finally had a fresh start.

Here’s the actual proof of Tom’s deleted accounts:

Debt Relief Like Accredited Isn’t Always What It Seems

When you're in debt, it's easy to fall for programs that promise quick fixes. But companies like Accredited Debt Relief don't always explain the full picture.

Let’s break down why programs like these often do more harm than good:

🛑 You’re Told to Stop Paying Your Bills

To get creditors to negotiate, these companies ask you to stop making payments. That’s when the real damage begins.

Your accounts fall behind. Late payments turn into charge-offs. And those black marks stay on your credit for seven years.

Good Read: Mike’s Toyota Charge-Off – How We Got It Deleted & Boosted His Credit Score

🛑 Settled Accounts Still Hurt Your Score

Even when a debt gets “settled,” it doesn’t mean it disappears. It’s usually reported as settled for less than owed—which is a signal to lenders that you didn’t fulfill the original terms.

That’s enough to tank your score and scare off future lenders.

🛑 You Could Get Sued While in the Program

While you're waiting to save enough money for them to settle your debt, creditors can still come after you.

We've seen it before: wage garnishments, frozen bank accounts, even judgments.

Debt relief programs DO NOT protect you from lawsuits.

🛑 You Might Not Actually Save Money

Companies like Accredited debt relief often take thousands in fees before a single payment goes to your creditors.

Plus, the forgiven amount can be taxed as income.

In the end, you may have paid more—and your credit is worse than when you started.

🛑 You're Left With Bad Credit for Years

These programs typically last 3 to 5 years, and during that time your credit is frozen in place. You can’t qualify for loans, decent credit cards, or even a rental.

By the time it’s over, your financial opportunities have passed you by.

Frequently Asked Questions About Accredited Debt Relief

You've got questions about Accredited Debt Relief, and after hearing Tom's story, you've got every right to be wary.

Let's cut through the fluff and get to the hard truths.

Q: What is Accredited Debt Relief?

A: Accredited Debt Relief presents itself as a debt settlement company. They promise to negotiate with your creditors to reduce the amount you owe, offering a seemingly easier path out of debt. In theory, they aim to lower your monthly payments and help you become debt-free faster. In practice, well, that's where things get murky.

Q: What is Accredited Debt Relief?

A: Accredited Debt Relief presents itself as a debt settlement company. They promise to negotiate with your creditors to reduce the amount you owe, offering a seemingly easier path out of debt. In theory, they aim to lower your monthly payments and help you become debt-free faster. In practice, well, that's where things get murky.

Q: How does Accredited Debt Relief work?

A: They typically instruct you to stop making payments to your creditors and instead deposit money into a dedicated account. Once you've accumulated enough funds, they claim to negotiate settlements with your creditors. This process can take years, and during that time, your credit takes a serious hit.

Q: Is Accredited Debt Relief Legit?

A: Legally, yes. They're a registered company. But "legit" doesn't mean "good for you." While they operate within legal boundaries, their practices can be highly detrimental to your financial health.

Q: Does Accredited Debt Relief hurt your credit?

A: Absolutely. Stopping payments to your creditors leads to late payments, charge-offs, and potentially even lawsuits. Settled accounts still negatively impact your score. In short, your credit score takes a significant beating while enrolled in their program.

Q: How long does Accredited Debt Relief hurt your credit?

A: The damage can last for years. Late payments and charge-offs remain on your credit report for up to seven years. Even after the program ends, the negative impact can linger, affecting your ability to obtain loans, credit cards, or even rent an apartment.

Don't let promises of easy debt relief lead you down a dangerous path. There are better, more sustainable ways to regain control of your finances.

What You Can Do Instead

Before giving up your credit score, your options, and your peace of mind—consider starting with credit repair.

✅ You keep control of your accounts

✅ You avoid court judgments or wage garnishment

✅ You get the chance to dispute invalid or outdated debts

✅ You protect your credit while fixing it

Tom didn’t think he had options left. But once we stepped in, everything changed.

Accredited Debt Relief: Better Think Twice

Don’t let debt relief companies like Accredited Debt Relief hold you back. If you’re stuck in a debt settlement program—or thinking about joining one—talk to us first.

There may be a better way.

🔹 Start a chat with us now → [Click Here]

🔹 Call us at 📞 888-656-0803

🔹 Text us at 📲 281-545-5001