Is AllianceOne recovering a debt from you? If you've received a call, text, or letter from this company, you're not alone. Thousands of consumers face the same situation every month, and many feel confused about what to do next.

This guide will walk you through everything you need to know about AllianceOne. We’ll cover your legal rights and the smart steps you can take to resolve the situation.

Who Is AllianceOne, and Why Are They Contacting You?

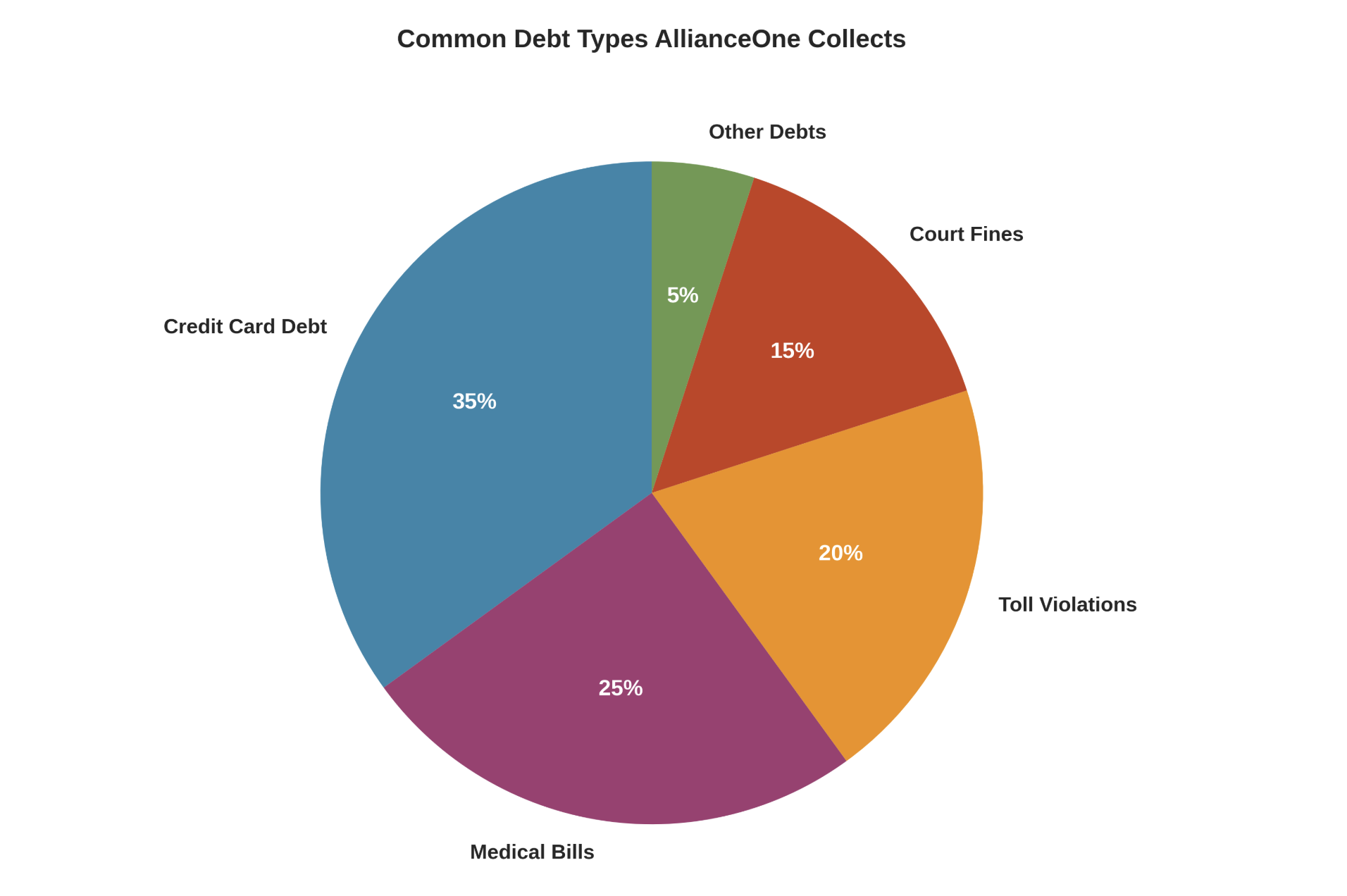

AllianceOne Receivables Management, Inc. is a third-party debt collection agency based in Pennsylvania. They've been in business for over 25 years and work with clients across the country. These clients include credit card companies, healthcare providers, toll authorities, municipal courts, and other businesses.

Here's what makes AllianceOne different from your original creditor: they don't own most of the debts they collect.

Instead, companies hire them to recover money that people haven't paid. Last quarter alone, we received 347 cases related to this debt collector, which shows how actively they pursue accounts.

When your account goes unpaid for several months, your original creditor might hand it over to AllianceOne. At this point, you're dealing with a professional debt collector who operates under specific federal rules.

How AllianceOne Typically Contacts Consumers

AllianceOne reaches out through multiple channels. You might receive a phone call from an unfamiliar number, a text message with a reference number, or a formal letter in the mail. Their initial contact often creates urgency, with phrases like "immediate action required" or "account escalated."

Many consumers report that AllianceOne representatives push for quick payment during the first conversation. They might suggest payment plans or ask for your banking information right away. However, you're not required to pay immediately or provide any information during that first contact.

Understanding your timeline is crucial. From the moment AllianceOne first contacts you, you have specific rights that protect you from unfair practices. These rights exist whether you owe the debt or not.

Good Read: Alliance Law Group Calls: Why They're Contacting You & What to Do

Your Legal Rights Under Federal Law

The Fair Debt Collection Practices Act (FDCPA) is your shield against abusive collection tactics. This federal law, which has protected consumers since 1978, sets clear boundaries for what debt collectors can and cannot do.

Under the FDCPA, debt collectors cannot:

- Call you before 8 a.m. or after 9 p.m. in your time zone

- Contact you at work if they know your employer prohibits such calls

- Harass you with repeated calls designed to annoy

- Use threatening, profane, or abusive language

- Lie about the amount you owe or threaten legal action that they cannot take

- Discuss your debt with friends, family, or coworkers (except to locate you)

- Continue calling after you request in writing that they stop

These protections apply to every interaction with AllianceOne. If they violate any of these rules, you can report them to the Consumer Financial Protection Bureau (CFPB) and potentially sue them for damages.

What To Do When AllianceOne Contacts You

Step 1: Request Debt Validation (Do This First)

Before you pay a single dollar, you need to verify that the debt is legitimate and accurate. This process is called debt validation, and it's your most powerful tool.

Within 30 days of AllianceOne's first contact, send them a written debt validation letter. This letter should request:

- The exact amount they claim you owe

- The name of the original creditor

- Proof that they have the legal right to collect this debt

- A breakdown of any fees or interest added to the original amount

Send your letter via certified mail with a return receipt. This creates a paper trail proving you made the request. Once AllianceOne receives your validation request, they must stop all collection activity until they provide the requested documentation.

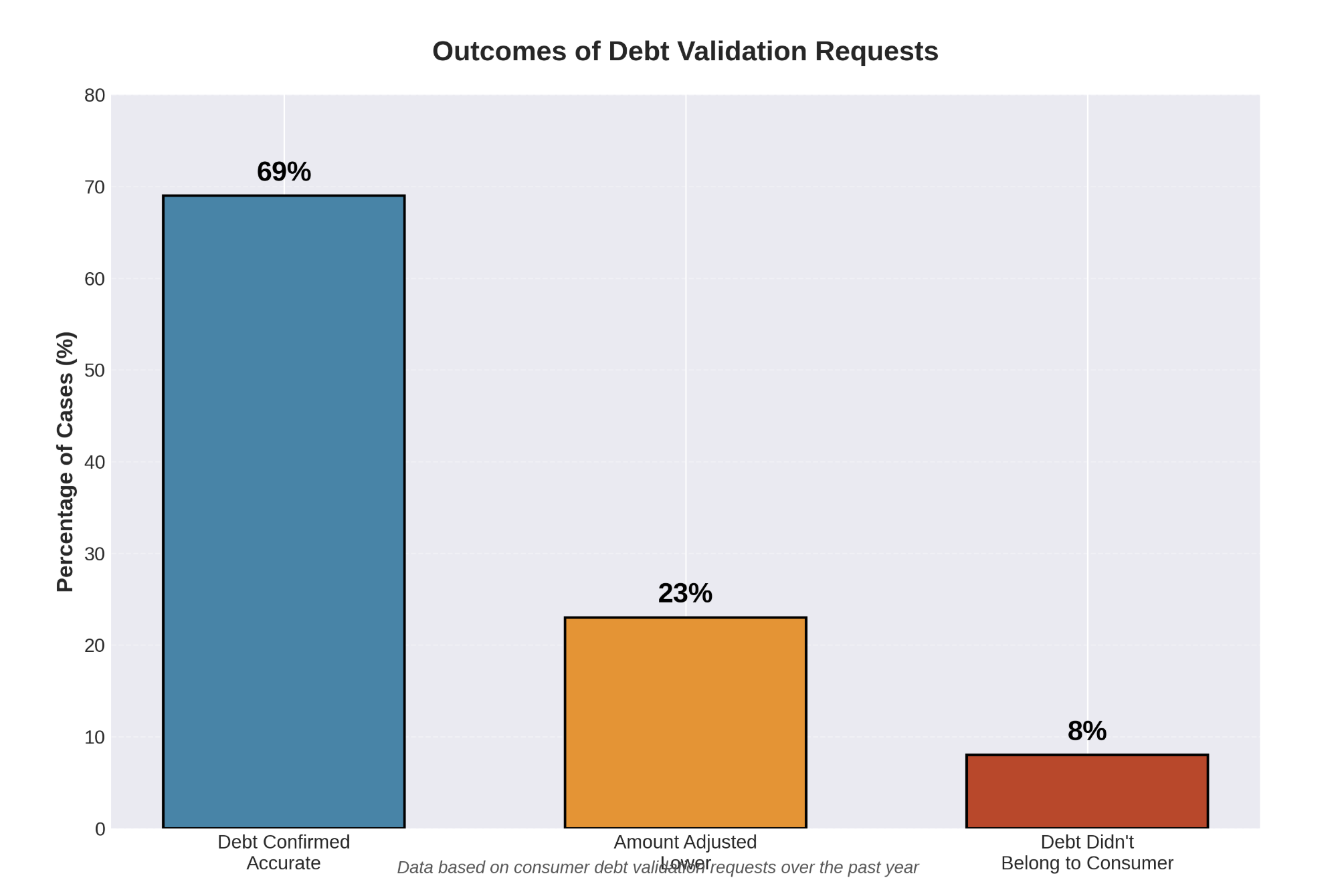

Why does this matter? Our data shows that in the past year, approximately 23% of debt validation requests revealed errors in the amount owed, and 8% showed the debt didn't belong to the consumer at all.

Don't skip this step.

Step 2: Verify the Debt Independently

After you request validation from AllianceOne, do your own investigation. Pull your credit reports from all three major bureaus: Experian, Equifax, and TransUnion. You can get these free reports once per year at AnnualCreditReport.com.

Look for the account AllianceOne claims you owe. Check these details:

- Does the original creditor's name match what AllianceOne told you?

- Is the amount the same?

- Do the dates align with when you might have missed payments?

- Are there any discrepancies in the account information?

If you find errors on your credit report, dispute them immediately with the credit bureaus. They have 30 days to investigate and must remove inaccurate information if AllianceOne cannot verify it.

I want to share a real story with you about something a client experienced. She received a collection notice from AllianceOne for a medical bill totaling $1,200. She requested validation and checked her credit report. The investigation revealed that her insurance company had actually paid the bill eight months earlier, but the hospital's billing department never updated their records.

After she provided proof of payment, AllianceOne closed the account and removed it from her credit report. This situation could have destroyed her credit score for seven years if she hadn't taken the time to verify.

Step 3: Understand Your Payment Options

If the debt is valid and you confirm you owe it, you have several options. Don't let AllianceOne pressure you into choosing the first option they offer.

Pay in Full

Paying the entire amount immediately resolves the debt completely. However, before you pay, negotiate for a "pay for delete" agreement. This means AllianceOne removes the collection account from your credit report once you pay. Get this agreement in writing before you send any money.

Negotiate a Settlement

AllianceOne often accepts less than the full amount. Why? Because collecting something is better than collecting nothing. You might settle for 40-60% of the original debt.

When negotiating, start with a lower offer. If you owe $2,000, offer $800 initially. AllianceOne will likely counter with a higher amount. Keep negotiating until you reach a number you can afford.

Always get settlement terms in writing before paying. The agreement should state the exact amount you'll pay, the payment deadline, and confirmation that this settles the debt in full.

Recommended Read: How To Negotiate a Debt Settlement

Set Up a Payment Plan

If you cannot pay a lump sum, AllianceOne may offer a payment plan. Review the terms carefully. Make sure you can afford the monthly payments without missing other essential expenses like rent or groceries.

Payment plans keep the collection account on your credit report until you finish paying. However, consistent payments show future creditors that you're working to resolve your debts.

What Happens If You Ignore AllianceOne?

Ignoring debt collectors never makes the problem disappear. In fact, it usually makes things worse.

Here's what can happen if you don't respond:

First, AllianceOne will continue its collection attempts. The calls and letters will persist. Second, the collection account will damage your credit score. Collections can lower your score by 50-100 points or more, making it harder to rent an apartment, buy a car, or get approved for loans.

Third, and most seriously, AllianceOne can sue you. If they win the lawsuit (which happens often when people don't respond), they get a judgment against you. This judgment allows them to garnish your wages or freeze your bank account to collect what you owe.

A judgment stays on your credit report for seven years and can be renewed in many states. The amount you owe can also grow with court costs and attorney fees.

How to Spot AllianceOne Scams

Unfortunately, scammers know that debt collection creates fear. They impersonate legitimate companies like AllianceOne to steal money or personal information.

Watch for these red flags that suggest a scam:

- The caller refuses to provide a callback number or mailing address

- They demand payment through wire transfer, gift cards, or cryptocurrency

- They threaten you with immediate arrest or jail time

- The message contains spelling errors or comes from a suspicious email address

- They ask for sensitive information like your Social Security number before verifying your identity

- The phone number or website doesn't match AllianceOne's official contact information

If you suspect a scam, hang up immediately. Then contact AllianceOne directly using the phone number on their official website (alliance oneinc. com) to verify whether they're actually trying to reach you.

Related Content: Alliance One: What To Do If You See This On Your Credit Report?

Disputing Errors and Filing Complaints

When AllianceOne makes a mistake or violates your rights, you can fight back. The process starts with documentation. Keep records of every interaction: save letters, note the date and time of phone calls, and record what was said.

If you believe the debt is wrong or AllianceOne broke the law, file complaints with:

- The Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov/complaint

- Your state attorney general's office

- The Better Business Bureau (BBB)

These agencies track complaints and can investigate patterns of violations. Your complaint might not only help you but also protect other consumers.

You also have the right to sue AllianceOne in state or federal court if they violated the FDCPA. You must file within one year of the violation. If you win, you can recover actual damages (like lost wages), up to $1,000 in statutory damages, and attorney fees.

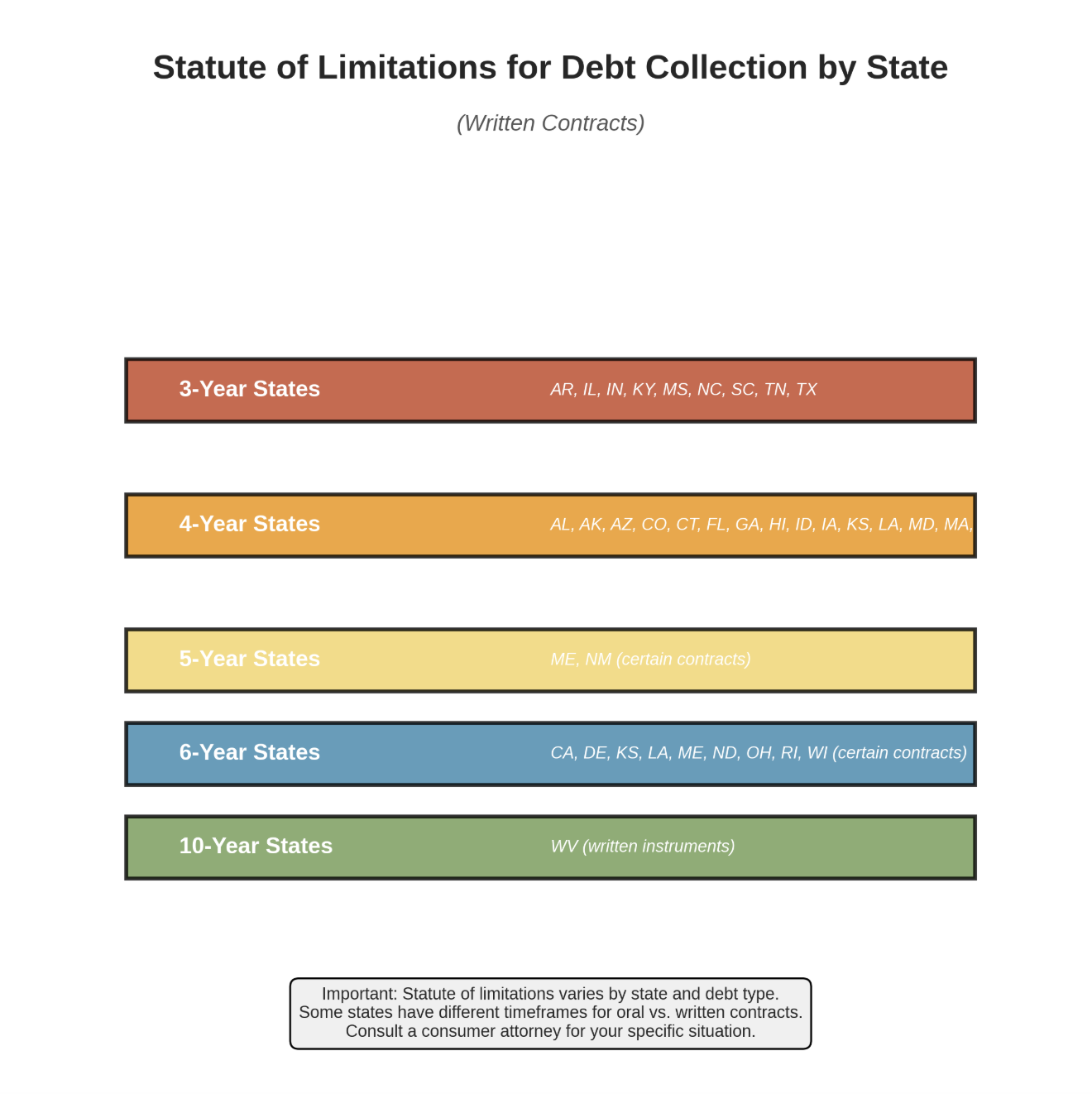

Special Situations: Time-Barred Debts

Here's something many consumers don't know: old debts have a statute of limitations. This is the time period during which a creditor can sue you to collect. The timeframe varies by state, typically ranging from three to six years.

Once the statute of limitations expires, the debt becomes "time-barred." AllianceOne cannot sue you to collect a time-barred debt. However, they can still contact you and ask you to pay voluntarily.

Be careful here. In most states, if you make a payment or even acknowledge that you owe a time-barred debt, you can restart the statute of limitations. Before you pay or promise to pay an old debt, research your state's laws or consult with a consumer attorney.

Working With AllianceOne Professionally

Despite the stress they can cause, AllianceOne is a business following federal regulations. Approaching them professionally often yields better results than avoiding them.

When you contact AllianceOne:

- Stay calm and polite, even if you feel frustrated

- Take notes during every conversation, including the representative's name and employee ID

- Don't admit the debt is yours until you verify it

- Never give out your bank account or debit card information over the phone

- Request everything in writing

- Don't let them rush you into decisions

Remember that AllianceOne representatives work on commission or meet collection quotas. They want you to pay as much as possible, as quickly as possible. You're allowed to take time to review your options and make informed decisions.

Another real experience I'd like to share involved a young professional who received calls from AllianceOne about an old credit card debt totaling $3,400. Instead of panicking, he requested validation, confirmed the debt was his, and then calculated what he could realistically afford. He called back and offered a settlement of $1,500 paid in full within 30 days.

After some negotiation, AllianceOne agreed to $1,700. He got the agreement in writing, paid the settled amount, and the collection account was removed from his credit report within 60 days. His credit score increased by 45 points once the collection was gone.

How Collections Affect Your Credit Score

A collection account from AllianceOne can seriously damage your credit score. The impact depends on several factors, including your overall credit history and how many other negative items you have.

According to credit scoring models, collection accounts hurt your score because they signal that you didn't pay a debt as agreed. Newer scoring models (FICO 9 and VantageScore 3.0) ignore paid collection accounts, but many lenders still use older models that count them.

Here's the good news: the negative impact decreases over time.

A two-year-old collection hurts less than a recent one. Collections fall off your credit report seven years from the date of your first missed payment with the original creditor (not from when AllianceOne started collecting).

During those seven years, you can minimize damage by:

- Paying or settling the debt (and getting it marked as "paid" on your report)

- Building positive credit history with on-time payments to other accounts

- Keeping credit card balances low

- Avoiding new collection accounts

Moving Forward: Protecting Your Financial Future

Dealing with AllianceOne is stressful, but it's also an opportunity to take control of your financial health. Once you resolve the collection account, focus on preventing future problems.

Create a budget that accounts for all your expenses and debts. Set up payment reminders for bills so you never miss due dates. Build an emergency fund, even if you start with just $25 per month. This cushion helps you handle unexpected expenses without going into debt.

Monitor your credit regularly. Many banks and credit card companies offer free credit monitoring. Check your reports at least once per year for errors or signs of identity theft.

If you're overwhelmed by multiple debts, consider working with a nonprofit credit counseling agency. These organizations help you create debt management plans and provide financial education. Look for agencies accredited by the National Foundation for Credit Counseling (NFCC).

Final Thoughts: You Have More Power Than You Think

Is AllianceOne recovering a debt from you? Remember that you're not powerless in this situation. Federal law gives you rights, and you have options for resolving the debt on terms you can manage.

Start by requesting validation. Verify the debt independently. Understand your payment options. Know when to negotiate and when to seek legal help. Most importantly, don't let fear or embarrassment prevent you from taking action.

Debt collection can feel overwhelming, but thousands of consumers successfully resolve these situations every year. With the right knowledge and approach, you can too. Take it one step at a time, document everything, and protect your rights throughout the process.

Your financial future is worth fighting for. Whether you settle, pay in full, or dispute the debt entirely, make your decision based on facts and your personal situation. AllianceOne is just one chapter in your financial story, not the end of it.