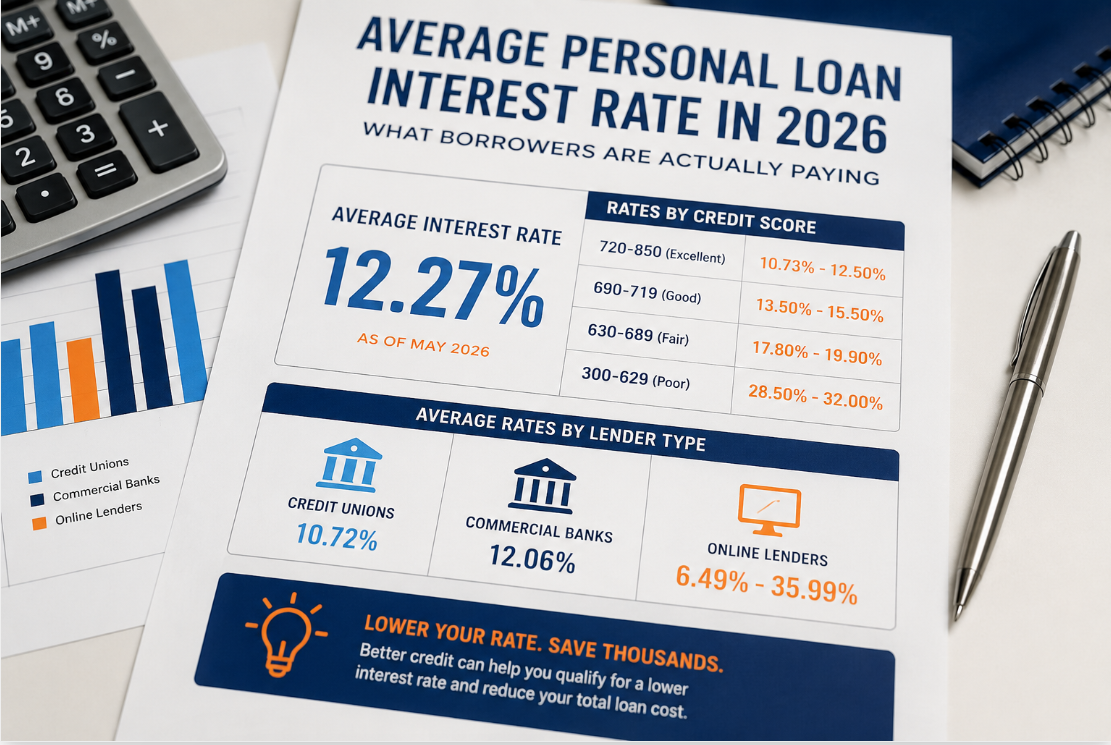

The average personal loan interest rate is 12.27% as of May 2026, according to Bankrate Monitor data. What you actually pay depends heavily on your credit score, your lender, and the loan term you choose. Rates range from as low as 5.96% for top-tier borrowers to as high as 35.99% for those with weak credit.

Running a credit repair company, I see this firsthand every week. Clients come in after being offered 25%+ on a personal loan, and once we clean up their credit report, some qualify for rates nearly half that. One of the most common calls we get goes something like: "I just got approved — is 22% normal?" The short answer: it depends on your credit score. The long answer is below.

Real talk from borrowers on Reddit's r/personalfinance confirms this frustration. Users in a widely-discussed thread reported receiving rates anywhere from 8% to 30% for the same loan amount — all because their credit scores were different. See the thread here.

Average Personal Loan Interest Rate: Current Numbers (May 2026)

The average personal loan interest rate is 12.27% for a borrower with a 700 FICO score, a $5,000 loan, and a three-year term (Bankrate, May 2026).

That number, though, masks a wide range across lender types:

Average rate across all lenders: 12.26%

Average rate at credit unions: 10.72%

Average rate at commercial banks: 12.06%

Rate range at online lenders: 6.49% to 35.99%

The Federal Reserve tracks two-year personal loan rates at commercial banks. That figure came in at 11.40% in February 2026, down from 12.32% in 2024. Rates have been trending lower since their peak in 2024, though they remain well above pre-2022 levels.

The bottom line on current rates: you are not looking at a cheap borrowing environment. Rate shopping across at least three lenders is not optional; it is necessary.

What Is a Good Interest Rate for a Personal Loan?

A good personal loan interest rate is anything below the national average of 12.27%. For borrowers with excellent credit, a rate below 10% is achievable and realistic.

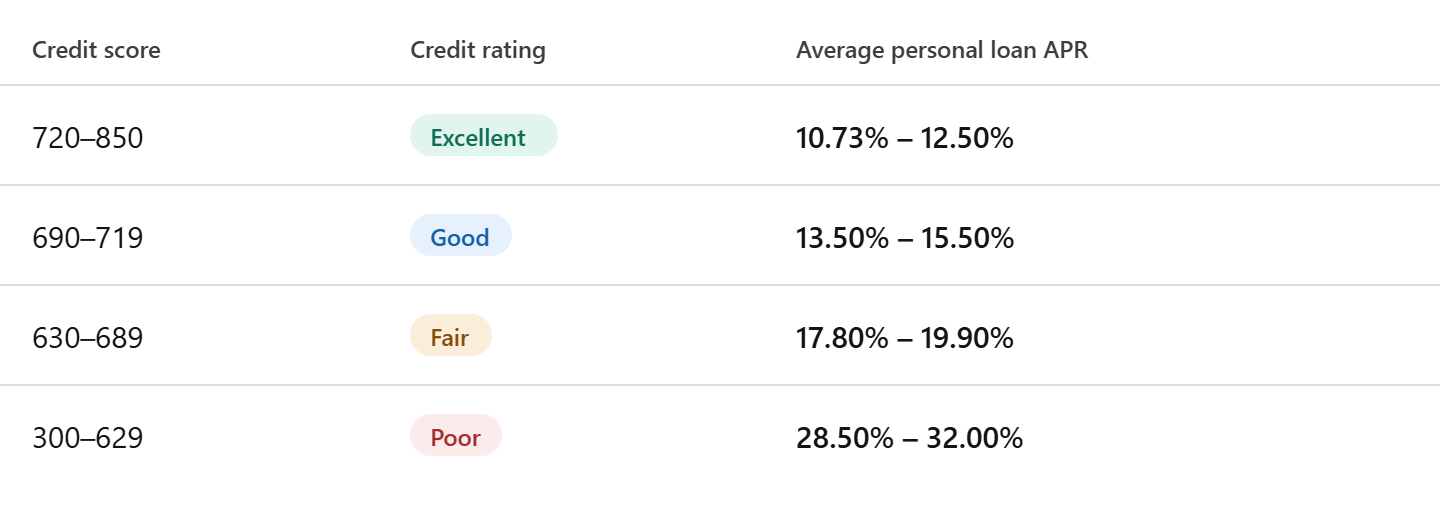

Here is how rates break down by credit score, based on Bankrate research:

Borrowers with excellent credit (720+) received an average rate of 13.31% through NerdWallet's pre-qualification platform in 2024. The lowest rates in the market today start at 5.96% from lenders like LendingClub, but those go only to the most creditworthy applicants.

A good rate is relative to your credit profile. If your score is 680, getting 17% may not be great — but 20% or higher would be avoidable with better preparation.

Average Personal Loan Interest Rate vs. APR: What Is the Difference?

Understanding the average personal loan interest rate means knowing it is not the same as the APR. The APR (Annual Percentage Rate) and the interest rate are not the same. The interest rate is the cost of borrowing the principal. The APR includes the interest rate plus any origination fees, closing costs, or lender charges expressed as a yearly percentage.

The Truth in Lending Act (TILA) requires lenders to disclose your APR. Always compare APRs across lenders, not just interest rates. A loan with a 9% interest rate but a 5% origination fee can cost more than a 10% loan with no fees.

For example, on a $10,000 loan with a 5% origination fee, you receive only $9,500, but you still repay $10,000 plus interest. The effective APR in that scenario climbs significantly above the stated rate.

Quick rule: Use APR to compare total cost across lenders. Use the interest rate to calculate your monthly payment.

How Much Does a Personal Loan Cost?

Personal loan costs depend on three variables: the loan amount, the APR, and the loan term. To understand what the average personal loan interest rate actually costs in dollars, here is a real example using the current figure of 12.27%:

Loan amount: $10,000

Term: 3 years

APR: 12.27%

Monthly payment: ~$333

Total interest paid: ~$1,990

Total repayment: ~$11,990

Stretch that same loan to 5 years:

Monthly payment: ~$225

Total interest paid: ~$3,500

Total repayment: ~$13,500

The five-year term saves you $108 per month — but costs you $1,510 more in total interest. Shorter terms cost less overall. Longer terms reduce your monthly burden but increase your total cost.

Origination fees add another layer. Some lenders charge 1% to 12% of the loan amount upfront. On a $10,000 loan with an 8% origination fee, you walk away with $9,200 but owe repayment on the full $10,000.

What Factors Affect the Average Personal Loan Interest Rate?

Six factors determine the average personal loan interest rate a lender offers you. Your credit score carries the most weight, but lenders look at the full picture.

1. Credit score: The higher your score, the lower your rate. Moving from a 630 to a 720 can cut your rate by 5% to 8% with most lenders.

2. Debt-to-income ratio (DTI) Lenders want your DTI below 36%. A DTI above 40% can either disqualify you or push your rate higher. To calculate yours: divide your total monthly debt payments by your gross monthly income.

3. Loan term Shorter loan terms often come with lower rates. Lenders see a 2-year loan as less risky than a 7-year loan.

4. Loan amount Smaller loans sometimes carry higher rates. Lenders need to profit even on small balances, which can push up the APR on loans under $2,500.

5. Lender type Credit unions typically offer lower rates than banks or online lenders. Federal credit unions cap rates at 18% by law. In our experience reviewing client loan offers, credit unions consistently beat bank offers by 1% to 3% for the same borrower profile.

6. Employment and income stability Lenders want proof of consistent income. Self-employed borrowers or those with irregular income often receive higher rates or face more stringent requirements.

Fixed vs. Variable Personal Loan Interest Rates

Most personal loans carry fixed interest rates. Your rate and monthly payment stay the same for the life of the loan. Fixed rates work best for borrowers who want payment predictability and are taking out a loan for two years or more.

Variable rates fluctuate based on a benchmark index, usually tied to the prime rate. Variable-rate personal loans are less common, but when they appear, they start lower. The risk: if the Fed raises rates, your payment rises too.

For most borrowers, fixed-rate personal loans are the safer choice. Variable rates make sense only for short-term loans you plan to repay quickly — within 12 to 18 months — before a rate increase has time to affect your cost.

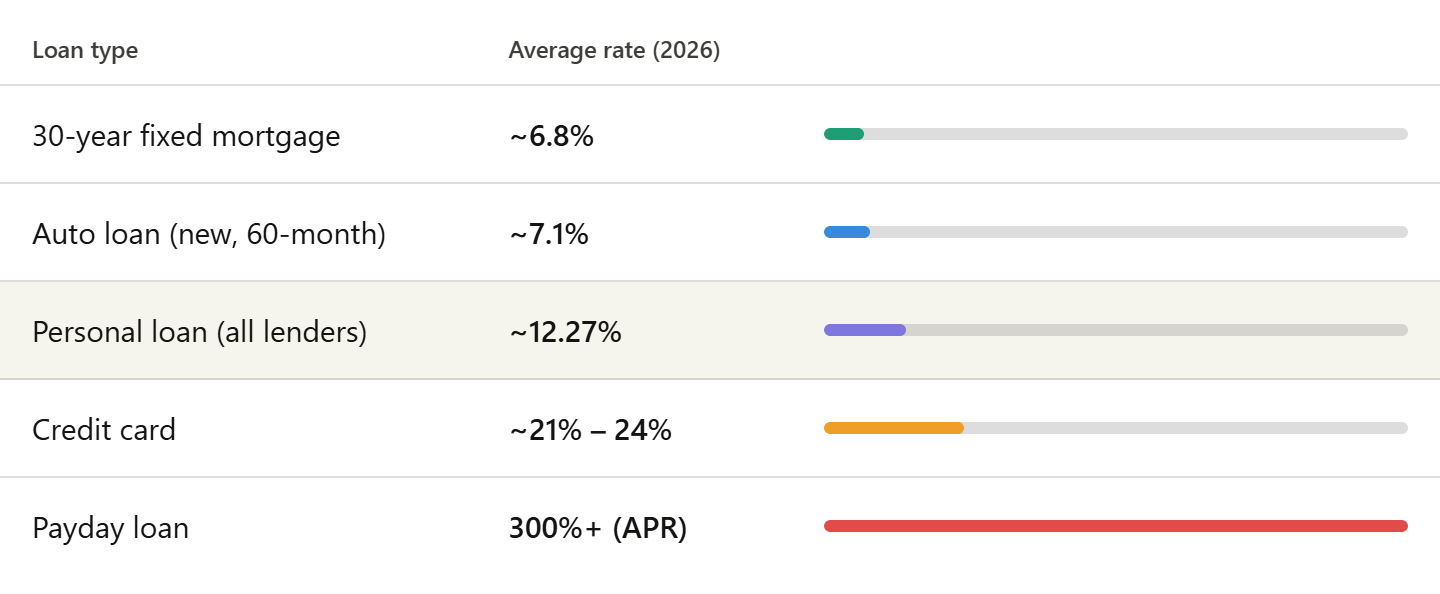

How Do Personal Loan Rates Compare to Other Loan Types?

Personal loan rates sit above mortgage and auto loan rates because they are unsecured. No collateral means more lender risk and higher rates.

Personal loans beat credit cards by a wide margin. Debt consolidation using a personal loan makes financial sense when your credit card APR exceeds 18%, and you qualify for a personal loan below that rate.

How to Get a Lower Personal Loan Interest Rate

Getting a lower rate is not luck. It is preparation. Here are the most effective steps, based on what works for our clients:

1. Check your credit report before applying. Dispute any errors with the credit bureaus. One removed collection account can raise a score by 20 to 40 points.

2. Pay down existing credit card balances. Credit utilization accounts for 30% of your FICO score. Dropping utilization from 60% to under 30% can move your score meaningfully.

3. Apply for pre-qualification with multiple lenders. Pre-qualification uses a soft pull and does not affect your score. Compare at least three offers before choosing.

4. Consider a co-signer. A co-signer with strong credit can unlock a lower rate — but they take on full liability if you default.

5. Choose a shorter loan term. If you can handle a higher monthly payment, a two-year term often comes with a better rate than a five-year term.

6. Look at credit unions first. Membership requirements vary, but credit unions consistently offer better rates than traditional banks.

Will Personal Loan Rates Go Down in 2026?

The Federal Reserve held rates steady at its first three meetings of 2026, keeping the federal funds target rate at 3.50% to 3.75%. Bankrate's 2026 forecast projects the average personal loan interest rate to settle around 12%, a modest decrease from the 12.21% recorded at the end of 2025.

Rates are unlikely to drop sharply this year. Inflation has ticked back up to 3.3% as of March 2026, which reduces pressure on the Fed to cut rates aggressively. Borrowers hoping for significantly lower rates may need to wait until late 2026 or beyond.

The better strategy: focus on improving your own credit profile. A 50-point credit score increase can drop your rate by more than any Fed cut will deliver in the next 12 months.

Paying Too Much Interest on a Personal Loan?

Your credit score directly affects the personal loan rate you qualify for. A few strategic credit improvements could help you secure a lower APR and save thousands in interest.

See what may be hurting your credit before applying for another loan.

No pressure. No hidden fees. Just a personalized review of your credit profile and loan-saving opportunities.

Is a Personal Loan Worth It at Current Rates?

A personal loan at 12% to 15% makes sense in these situations:

You carry credit card debt above 20% APR and want to consolidate

You need a fixed monthly payment for budgeting

You face a large, one-time expense (medical bill, home repair) with no better financing option

A personal loan at 25%+ rarely makes sense unless you have no other option. In that range, you are approaching credit card territory without the flexibility of revolving credit.

Last year alone, we saw over 300 clients take out personal loans at rates above 22% before coming to us. After credit repair work, roughly 60% refinanced to rates below 14%. The difference in total interest paid over a three-year term was often $2,000 to $4,000 per loan.

If your current rate offer feels too high, it probably is. The average personal loan interest rate you qualify for will improve with a better credit profile. Improving your credit first, even by 30 to 60 days of focused effort, can change the offer you receive.