Looking for bad credit mortgage lenders in Charlotte, this article is for you.

If you've ever sat across from a loan officer and watched their expression shift the moment they pulled your credit report, you know the feeling. That quiet pause. The professional smile that doesn't quite reach their eyes.

I've talked to a lot of people at that moment. People who walked out of that office were convinced homeownership just wasn't going to happen for them. Not in Charlotte. Not with their credit score. Not this year.

But here's what I want you to know before we go any further: bad credit does not disqualify you from buying a home in Charlotte in 2026. What it does do is change where you look, who you work with, and what you need to prepare. And that's exactly what this guide covers.

Understand What "Bad Credit" Actually Means to a Charlotte Lender

Before you start calling lenders, you need to know how they're going to see you. Because "bad credit" means something different depending on who you ask.

To a conventional lender, anything below 620 starts raising flags. Below 580, most of them stop the conversation altogether. But that's conventional lenders. And conventional lenders aren't your only option in Charlotte.

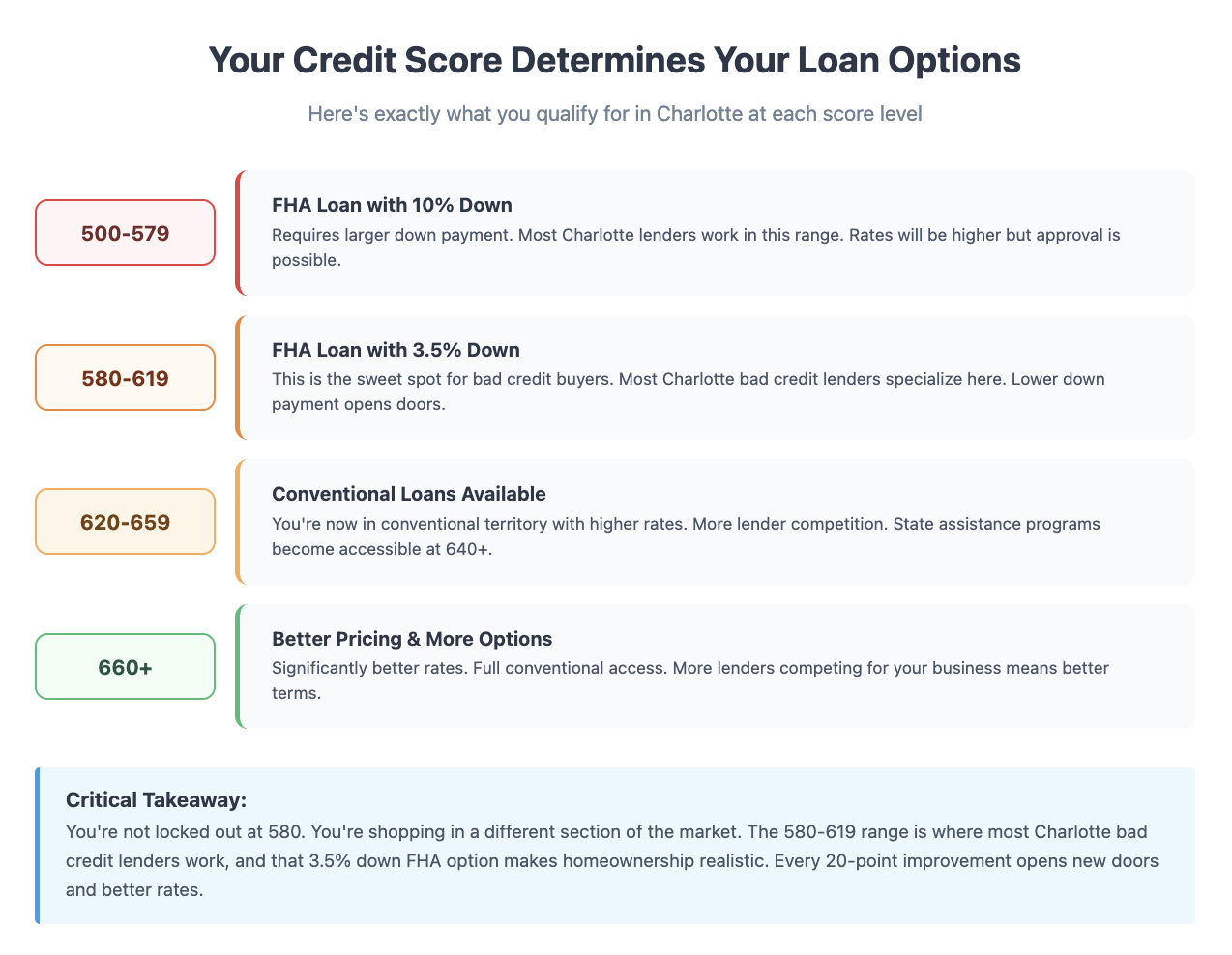

Here's a basic breakdown of how credit scores map to mortgage products:

- 500–579: FHA loan with 10% down payment required

- 580–619: FHA loan with 3.5% down. Most bad credit mortgage lenders in Charlotte work in this range

- 620–659: Conventional loans become available, though at higher rates

- 660 and above: Better pricing, more options, more lender competition

If your score falls anywhere between 500 and 650, you're not out. You're just shopping in a different section of the market. Knowing that going in changes everything about how you approach the process.

And one more thing worth saying clearly: your credit score is a snapshot, not a sentence. It reflects where you've been. It doesn't have to determine where you go.

Recommended Read: First-Time Home Buyer Programs in Atlanta for Low Credit Borrowers

Know the Types of Bad Credit Mortgage Lenders Operating in Charlotte

Not every lender in Charlotte is going to want your business if your score is below 640. That's just the reality. But the ones who do specialize in this space and they're worth knowing.

When I started researching the Charlotte mortgage market for buyers with damaged credit, a few categories kept coming up. Here's who you're actually looking for:

FHA-Approved Lenders

These are your most straightforward options. The Federal Housing Administration backs FHA loans, which means lenders take on less risk when they approve a borrower with lower credit. Most FHA-approved lenders in Charlotte accept scores starting at 580, and some work down to 500 with a larger down payment. Look for lenders who explicitly advertise FHA products. Not all banks push them.

Credit Unions

Charlotte has a strong credit union presence. Carolinas Telco Federal Credit Union, Local Government Federal Credit Union, and Self-Help Credit Union all serve the Charlotte metro area and carry reputations for working with members whose credit histories aren't perfect. Credit unions are member-owned, which tends to make their underwriting more human and less algorithmic.

Community Development Financial Institutions (CDFIs)

Self-Help Credit Union (which is also a CDFI) deserves special mention here. CDFIs exist specifically to serve borrowers who get overlooked by the traditional banking system. They operate in Charlotte in a meaningful way and offer mortgage products designed for buyers with complicated financial histories.

Non-QM Lenders

Non-qualified mortgage lenders operate outside the standard Fannie Mae and Freddie Mac guidelines. They offer products like bank statement loans, asset-depletion loans, and other alternatives for borrowers whose situations don't fit a conventional mold. Rates are higher, terms require more scrutiny, but for the right borrower, they fill a real gap.

The key is not to stop at the first "no." Bad credit mortgage lenders in Charlotte exist across all of these categories. You may need to knock on a few doors before the right one opens.

Get Your Financial Picture Together Before You Apply

Here's something a lot of buyers skip, and it costs them. Walking into a lender's office without knowing your own numbers puts you at a disadvantage from the first minute of the conversation.

Before you contact a single Charlotte lender, do this:

- Pull all three credit reports for free at AnnualCreditReport.com (Equifax, TransUnion, and Experian each keep separate files)

- Write down every debt you carry. Things like balances, monthly payments, and interest rates all matter.

- Calculate your debt-to-income ratio: add up all monthly debt payments, divide by your gross monthly income

- Identify any errors in your reports and dispute them in writing immediately

That last one matters more than people realize. Inaccurate collection accounts, duplicate negative entries, and outdated derogatory marks appear on credit reports more often than they should. Under the Fair Credit Reporting Act, bureaus must investigate disputes within 30 days. A single removed error can move your score 20 to 50 points, sometimes enough to shift you into a better loan tier entirely.

Lenders respond differently to borrowers who walk in prepared. Knowing your own DTI, understanding your score, and having documentation ready signals that you're a serious buyer, not a long shot. That matters in a relationship-driven lending environment like Charlotte's.

Related Content: FHA vs Conventional Loans in Chicago: Credit Score Requirements Explained

What Charlotte Bad Credit Borrowers Can Actually Expect in 2026

Let's talk real numbers, because vague encouragement doesn't help you plan.

The Charlotte housing market in 2026 still reflects elevated home prices compared to pre-2020 levels. The median home price in the Charlotte metro area sits in the $360,000–$380,000 range, depending on the neighborhood and the quarter. For a bad credit buyer using an FHA loan with 3.5% down on a $365,000 home, here's what the math looks like:

- Down payment (3.5%): approximately $12,775

- Loan amount: approximately $352,225

- Interest rate at 580–619 score: likely 7.25%–7.75% in the current rate environment

- Monthly principal and interest: approximately $2,400–$2,500

- FHA mortgage insurance premium (MIP): approximately $249/month

- Estimated total monthly payment (before taxes and insurance): approximately $2,650–$2,750

Those numbers are real. They're not designed to scare you. They're designed to help you plan. If your current rent is $1,800, you can see exactly what the gap is and start working toward closing it.

The financial and emotional impact of homeownership compounds over time:

Bad credit doesn't mean you skip those benefits. It means you pay a bit more to access them while you rebuild. And every payment you make starts doing exactly that.

Must Read: Easy Ways On How to Get an FHA Loan with Low Credit Score

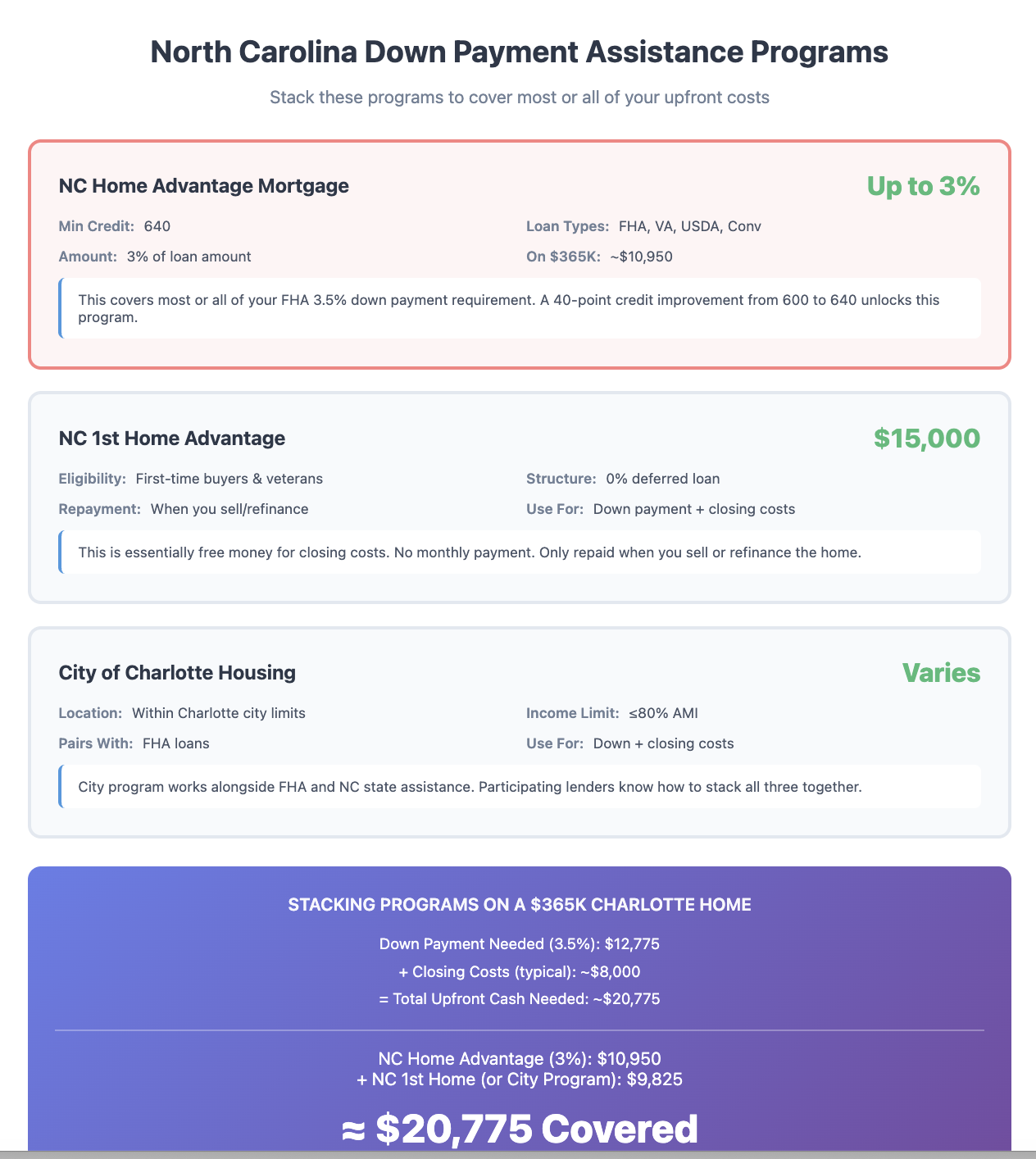

Use Charlotte and North Carolina Programs to Reduce Your Upfront Costs

One of the biggest barriers for bad credit buyers isn't the credit score itself — it's the down payment and closing costs. Charlotte and North Carolina have programs that directly address this, and bad credit buyers qualify for several of them.

NC Home Advantage Mortgage

The North Carolina Housing Finance Agency offers down payment assistance of up to 3% of the loan amount through the NC Home Advantage Mortgage program. It pairs with FHA, VA, USDA, and conventional loans and accepts credit scores as low as 640 for most products. At 640, the assistance covers most or all of your FHA down payment requirement on a typical Charlotte home.

If your score sits at 620 right now, a 20-point improvement opens this door. That's a realistic target on a 60-to-90-day timeline with focused credit repair.

NC 1st Home Advantage Down Payment

First-time buyers and military veterans in North Carolina can access an additional $15,000 in down payment assistance through this program. It's structured as a 0% interest deferred loan that only becomes due when you sell, refinance, or pay off the home. For a bad credit buyer stretching to cover closing costs on top of a down payment, this program can be the difference between closing and walking away.

City of Charlotte Housing Program

The City of Charlotte offers its own homebuyer assistance for buyers purchasing within city limits. The program provides closing costs and down payment help for buyers at or below 80% of the area median income. Participating lenders in the program are familiar with working alongside FHA financing, which makes this a natural pairing for bad credit buyers.

Stacking a city program with an FHA loan and NC state assistance is exactly how a lot of Charlotte buyers with imperfect credit manage to close. It's not a shortcut — it's the system working the way it was designed to.

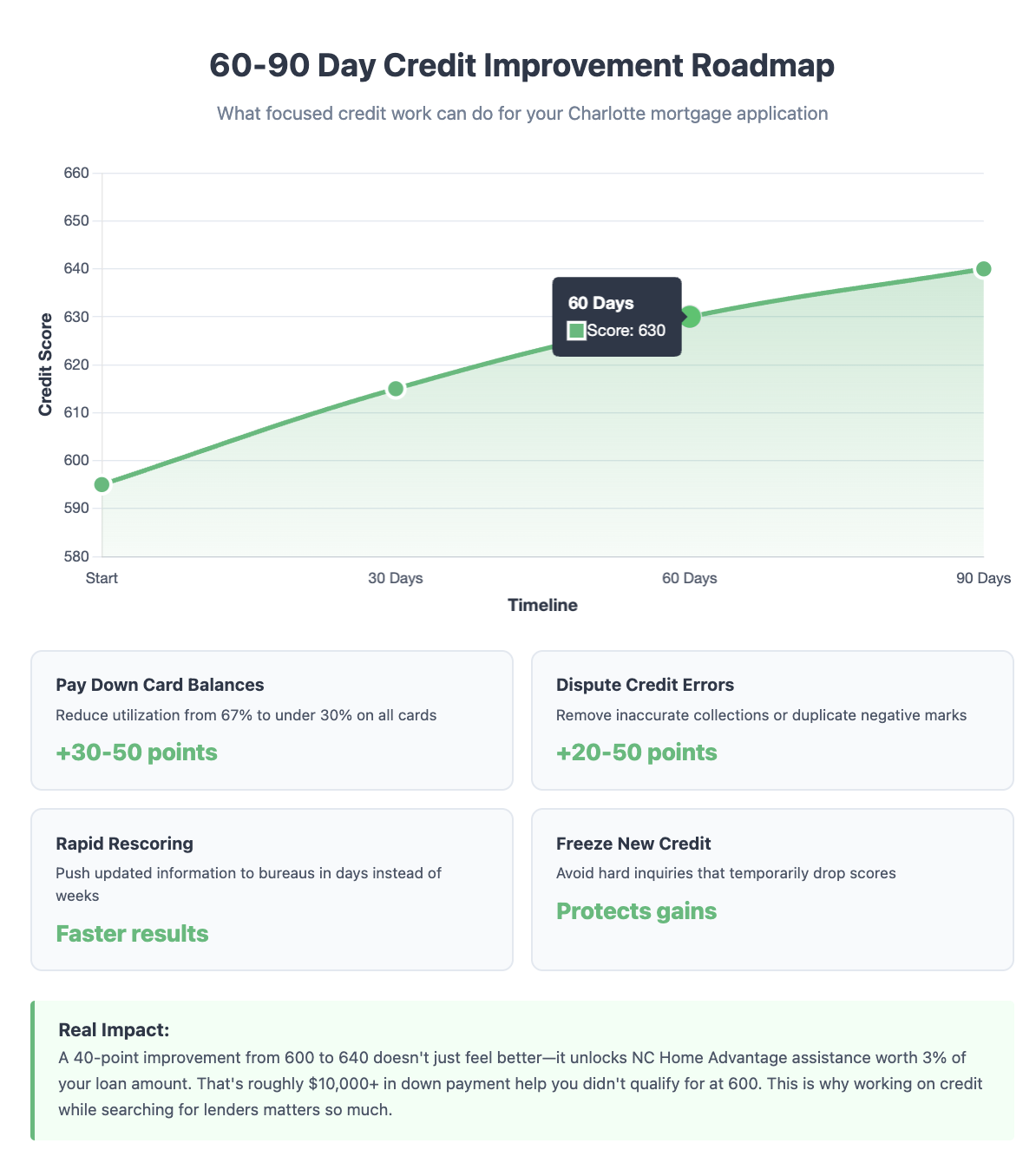

Work on Your Credit While You Search for a Lender

Applying for a mortgage and repairing your credit aren't two separate phases; you do one at a time. Run them in parallel. The improvements you make in the next 60 to 90 days can change your rate, your loan type, and your monthly payment, sometimes significantly.

Here's what actually moves the needle fast:

Pay down revolving credit card balances.

Credit utilization, or how much of your available credit you're using, makes up 30% of your FICO score. If you carry $4,000 on a card with a $6,000 limit, you're at 67% utilization. Get that below 30% and watch your score respond within a billing cycle or two.

Don't open anything new.

Every hard credit inquiry temporarily drops your score. In the 90 days before you apply, freeze new credit applications entirely.

Ask your lender about rapid rescoring.

If you pay down a balance or get an error removed, rapid rescoring pushes the updated information to the bureaus in days instead of weeks. Many Charlotte mortgage lenders offer this as part of the application process, and it can lift your score just enough to lock a better rate before closing.

Handle outstanding collections carefully.

Not every old collection account is worth paying before you apply. Some older debts near the end of their reporting window (North Carolina follows a 7-year federal reporting limit for most negative accounts) may be close to dropping off naturally. Paying them can sometimes restart activity on the account. Talk to your housing counselor before making any decisions on aged collections.

The point isn't to achieve perfect credit before you buy. The point is to walk into the lender's office in the strongest position you can reach in the time you have.

Find a HUD-Approved Housing Counselor in Charlotte First

Before you pick a lender, talk to a HUD-approved housing counselor. This step costs little to nothing, takes an hour or two, and regularly changes the outcome for bad credit buyers in Charlotte.

HUD-approved counselors help you understand your credit report, identify which programs you qualify for, connect you with the right lenders, and walk you through what to expect at each stage of the mortgage process. They don't work for lenders. They work for you.

The Charlotte area has several HUD-approved agencies, including the DreamKey Partners (formerly Charlotte-Mecklenburg Housing Partnership) and the Latin American Coalition, which serves Spanish-speaking buyers throughout the metro. The NC Housing Finance Agency website also maintains an updated list of approved counselors by county.

Going in without this step is like starting a road trip without checking the route. You might get there eventually, but you'll probably miss some turns that would have saved you a lot of time and money.

You're Closer Than You Think

Bad credit feels like a wall. But in Charlotte's mortgage market in 2026, it's more like a detour. A longer path, yes. A more expensive one in the short term, absolutely. But still a path.

The buyers who make it through aren't always the ones with the best credit. They're the ones who do the work before they walk in the door. They pull their reports. They talk to a counselor. They find the right lender for their actual situation, not the lender they assumed they had to use.

Every point you add to your score from here matters. Every debt you pay down matters. Every dollar you save toward a down payment matters.

Charlotte is a city that's still growing, still adding homeowners, and still creating first-time buyers out of people who weren't sure it was possible for them.

You can be one of them.

Disclaimer: This article provides general financial information and does not constitute professional financial or legal advice. Work with a licensed mortgage professional or HUD-approved housing counselor for guidance tailored to your specific situation.