Atlanta's housing market moves fast. Prices climb, inventory stays tight, and competition is real. But if your credit score has taken hits from medical debt, missed payments, or collections, you might feel like homeownership isn't meant for you yet.

Honestly, with the right knowledge and mindset. It is.

An Atlanta bad credit loan is not a workaround or a desperate measure. It's a legitimate financial tool that thousands of Georgia buyers use every year to get into their first home. The programs exist. The lenders are approved. And the path forward is more accessible than most people realize.

This guide covers everything you need to know about credit repair Atlanta. From first-time buyer programs in Atlanta to the exact loan options available at a 500 credit score, including smaller personal loans for buyers who need financial breathing room before they close.

Bad Credit Doesn't Mean No Options — Here's What Atlanta Lenders Actually Look At

Before you assume rejection, understand what lenders actually evaluate. Credit score is one factor, not the only factor.

Lenders look at your debt-to-income ratio (DTI), your employment history, your down payment size, and your overall loan risk profile.

A borrower with a 540 credit score, two years of steady employment, and 10% down can get approved, while a borrower with a 620 credit score and unstable income gets denied.

In Atlanta, a growing network of FHA-approved lenders, credit unions, and community lenders actively works with low-credit borrowers. They compete for this business. That competition works in your favor.

The most important thing you can do before applying for any Atlanta bad credit loan is pull all three of your credit reports at AnnualCreditReport.com. You need to know exactly what lenders will see. You also need to dispute any errors before they cost you an approval.

Yes, You Can Get a Loan with Extremely Bad Credit — If You Know Where to Look

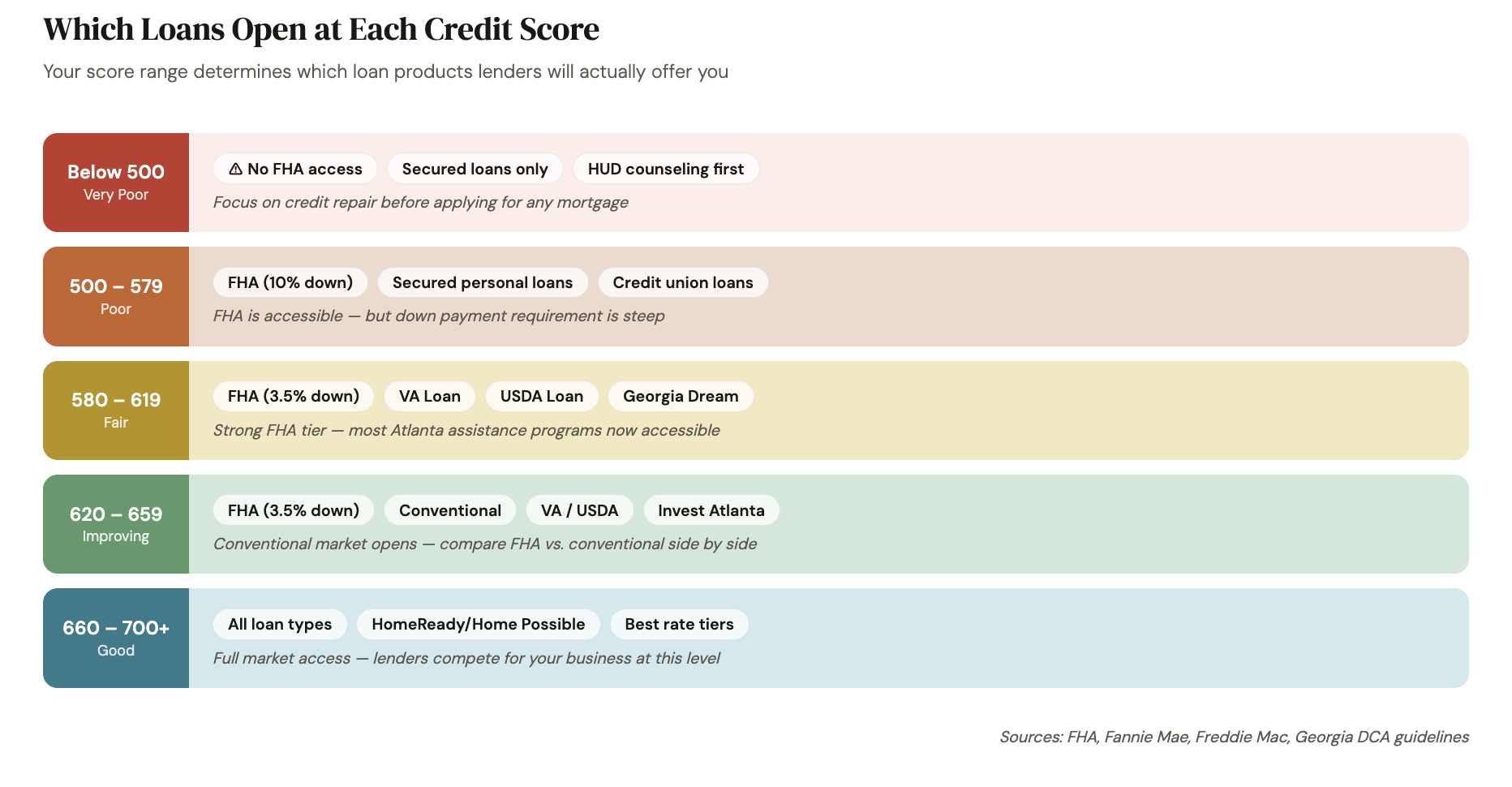

A score below 500 puts you in "extremely bad credit" territory. Conventional lenders, your major banks and mortgage companies, will likely decline your application outright. But government-backed loans operate on different rules, and that's where your real opportunity lives.

FHA loans are the most widely used Atlanta bad credit loan product for home buyers. The Federal Housing Administration insures these loans, which means approved lenders take on less risk. As a result, they accept borrowers that conventional lenders won't touch.

Here's how the FHA score breakdown works in practice:

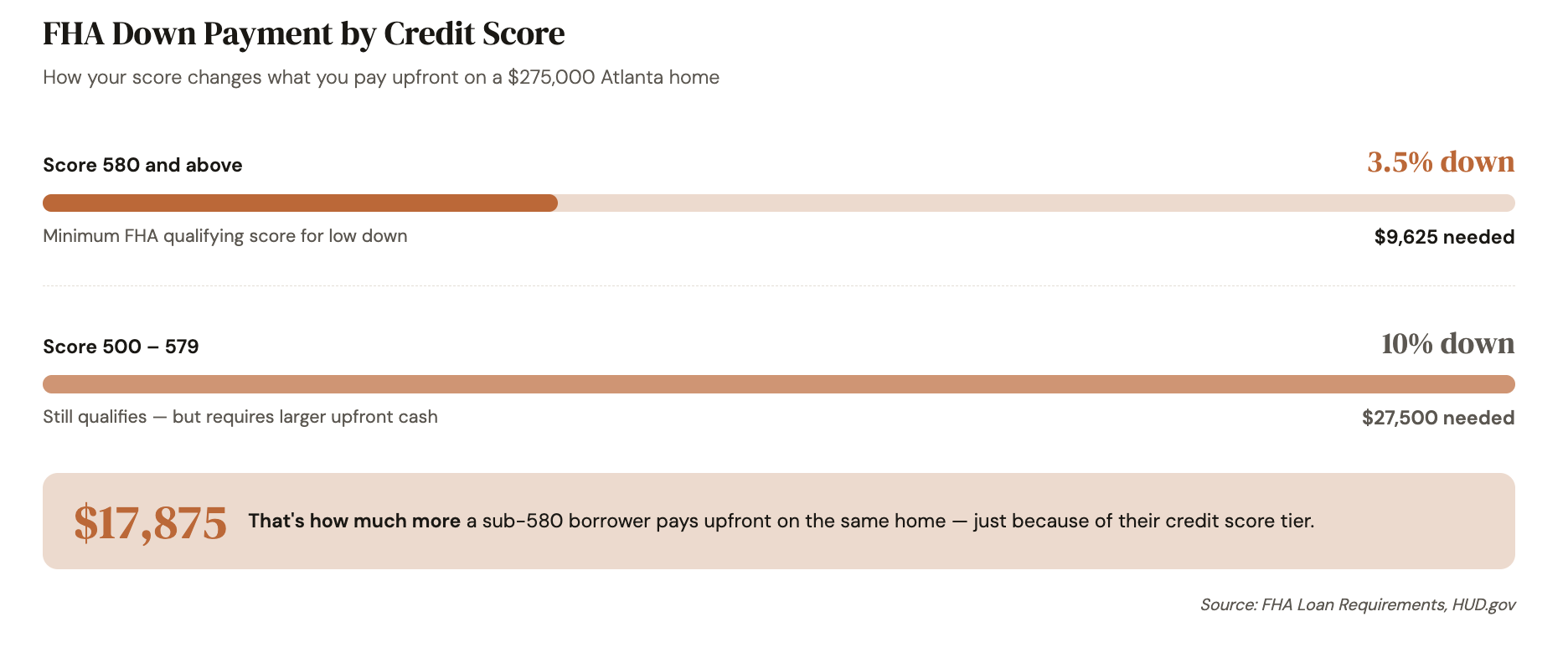

- 500–579 credit score: You can qualify, but you need a 10% down payment

- 580 and above: Your required down payment drops to just 3.5%

On a $275,000 home, a realistic entry-level price in many Atlanta neighborhoods, the difference in upfront costs can be significant. It’s $27,500 versus $9,625.

That gap matters enormously for first-time buyers.

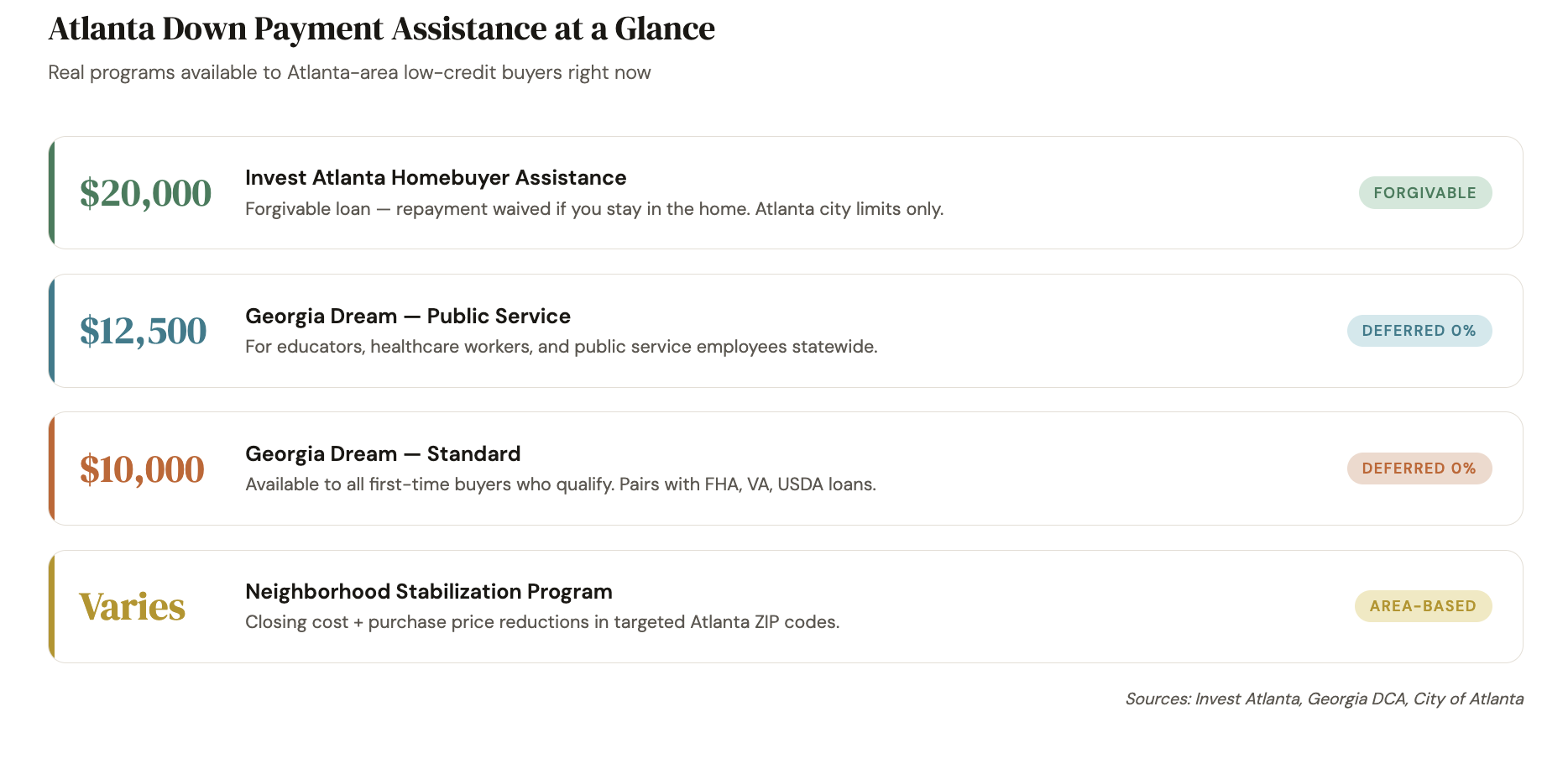

The Georgia Dream Homeownership Program, administered by the Georgia Department of Community Affairs, layers directly on top of FHA loans. It offers down payment assistance of up to $10,000 for standard borrowers, and up to $12,500 for buyers who work in public service or have a family member with a disability. That assistance comes as a 0% interest deferred loan. You don't repay it until you sell, refinance, or pay off the home.

For buyers with scores below 500, your clearest first move is working with a HUD-approved housing counselor. They identify what's dragging your score, build a 90-to-180-day repair plan, and connect you with lenders who specialize in hard-to-approve borrowers.

The Atlanta Neighborhood Development Partnership (ANDP) offers free counseling and has helped thousands of Atlanta residents move from denied to approved.

Need a $4,000 Loan with Bad Credit? Here Are Your Real Atlanta Options

Not every borrower needs a mortgage right now. Some need a $3,000 to $5,000 personal loan to consolidate debt, cover moving costs, or handle a financial emergency while they work toward homeownership. Bad credit makes this harder, but not impossible.

Recommended Read: Why Is It So Hard to Get Approved for a Mortgage With Bad Credit

Credit unions are your first stop. Georgia's Own Credit Union and Delta Community Credit Union both serve the Atlanta metro area. Credit unions are member-owned nonprofits, so their approval criteria are more flexible than traditional banks. They weigh your relationship with the institution, your income stability, and your overall financial picture, not just your credit score. Members with scores in the 520–580 range regularly get approved for personal loans up to $5,000.

Online lenders have changed the bad credit lending market significantly. Lenders like Upstart, Avant, and LendingPoint use alternative data — employment history, education, income trends — alongside your credit score. A borrower with a 570 score and two years at the same employer has a realistic shot at a $4,000 loan through these platforms.

Community Development Financial Institutions (CDFIs) serve Atlanta's underbanked communities specifically. Access to Capital for Entrepreneurs (ACE) operates across Georgia and provides personal and small business loans to borrowers who don't meet conventional standards. These institutions exist because they believe access to credit is an equity issue — not just a financial one.

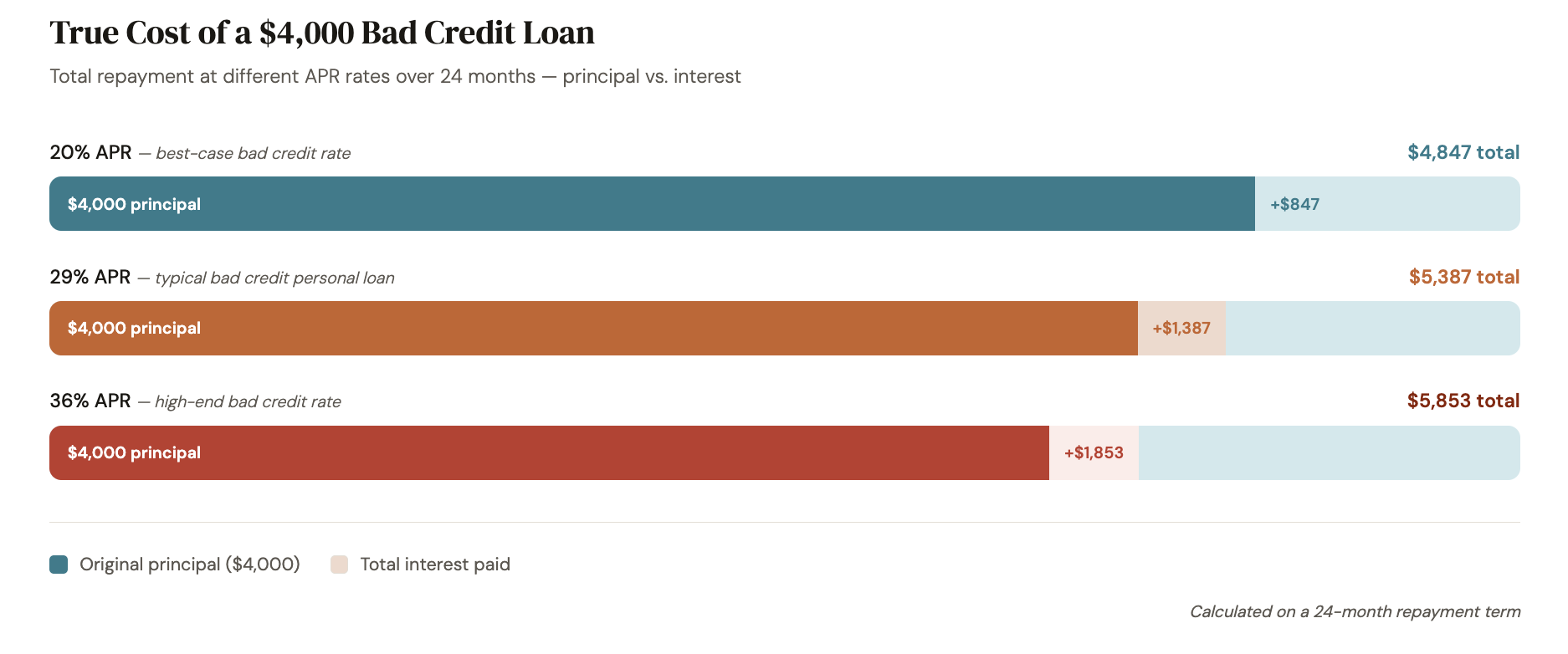

One number you must understand before signing anything: the APR. Bad credit personal loans in the $2,000–$5,000 range often carry APRs between 20% and 36%. On a $4,000 loan at 29% APR over 24 months, you'll repay close to $5,400 total. That's $1,400 in interest charges. Calculate the full repayment amount. Not just the monthly payment, before you commit.

The $2,000 No-Credit-Check Loan: What's Real and What's a Red Flag

People search for no-credit-check loans because they fear rejection. That fear is understandable. But "no credit check" is a phrase that demands careful reading before you sign anything.

Georgia has strong consumer protections when it comes to predatory lending. Traditional payday loans are effectively banned in the state due to strict interest rate caps. That's good news. It eliminates one of the most dangerous loan products from the market before you even encounter it.

Here's what legitimately exists in Atlanta for no-credit-check or soft-pull borrowing:

Payday Alternative Loans (PALs) through federal credit unions offer $200 to $2,000 with no hard credit check and interest rates capped at 28% APR. The application is straightforward, and decisions are fast. You must be a credit union member, but membership requirements are typically easy to meet.

Secured personal loans remove credit score risk for the lender because you back the loan with collateral, such as a savings account, a certificate of deposit, or a vehicle. Because the lender can recover its money if you default, approval rates climb significantly, and interest rates stay lower than those of unsecured bad credit products.

BNPL (Buy Now, Pay Later) platforms like Afterpay and Klarna run soft credit checks or none at all for smaller purchases. They won't hand you $2,000 in cash, but they help you manage necessary expenses — appliances, furniture, home essentials — without adding hard inquiries to your credit file.

If you find a lender promising $2,000 with no credit check, no income verification, and guaranteed approval — stop before you enter your Social Security number. Verify every lender through the Georgia Department of Banking and Finance's licensee lookup and the Better Business Bureau. Predatory lenders specifically target people with bad credit because desperation creates vulnerability.

Getting Approved with a 500 Credit Score: The Loan Products That Actually Deliver

A 500 credit score is not a dead end. It connects to specific loan products built for exactly this situation. Here's the clear breakdown:

FHA Home Loans: With a 500 score, you qualify with 10% down. This is the most direct path to Atlanta homeownership for buyers in this score range. Work with a Georgia Dream-approved lender to stack state assistance on top and reduce your out-of-pocket costs.

VA Loans: If you served in the military, VA loans carry no official minimum credit score. Individual VA-approved lenders set their own floors, and many work with scores starting at 500. VA loans also require zero down payment. One of the most powerful benefits in the entire mortgage market.

USDA Loans: The U.S. Department of Agriculture backs loans for buyers in eligible suburban and rural areas surrounding Atlanta. Many USDA-approved lenders accept scores as low as 580, and these loans also require no down payment. Parts of Cherokee, Coweta, and Forsyth counties qualify.

Secured Personal Loans: For non-mortgage credit needs at a 500 score, secured loans remain your most accessible option. When collateral backs the loan, the lender's risk drops, and credit score becomes far less of a barrier.

What doesn't work at 500: unsecured personal loans from major banks, conventional mortgages, and most credit cards with favorable terms. Knowing where to apply — and where not to — saves you from unnecessary hard inquiries that push your score further down.

Atlanta-Specific Programs Built for Low-Credit First-Time Buyers

Beyond FHA and Georgia Dream, Atlanta has city-level programs that go even further:

Invest Atlanta's Homebuyer Down Payment Assistance provides forgivable loans up to $20,000 for buyers purchasing within Atlanta city limits. The loan forgives gradually as long as you remain in the home — meaning you may never repay a dollar of it. Income limits apply, and buyers must complete a HUD-approved homebuyer education course before closing.

Neighborhood Stabilization Programs in specific Atlanta ZIP codes offer additional help for buyers purchasing in targeted revitalization areas. These programs reduce the effective purchase price or cover closing costs in neighborhoods the city is actively rebuilding, which can make a dramatic difference in affordability.

The Atlanta Land Trust offers community land trust homes where buyers purchase the structure but lease the land at a minimal cost. This arrangement significantly reduces the total purchase price and makes homeownership viable at lower income and credit levels than traditional ownership requires.

Contact Invest Atlanta directly or work through ANDP to find out which programs apply to your target neighborhood and income level. Program availability changes throughout the year, and some run out of funding before December — moving quickly gives you more options.

Repair Your Credit While You Pursue Financing — The Parallel Strategy That Actually Works

Applying for an Atlanta bad credit loan and repairing your credit aren't mutually exclusive goals. Run both strategies at the same time and you'll get better terms faster.

Dispute collection errors first. The Fair Debt Collection Practices Act (FDCPA) requires collectors to verify debts in writing upon your request. Inaccurate collections — wrong balances, accounts you don't recognize, duplicate entries — are surprisingly common and fully removable. Each successful removal can add 20 to 40 points to your score.

Reduce your credit utilization below 30% if you carry any revolving balances. This single change influences 30% of your FICO score calculation and produces results within one to two billing cycles — faster than almost any other credit repair action.

Avoid opening new credit accounts in the 90 days before a mortgage application. Hard inquiries temporarily drop your score, and lenders flag recent credit activity as a risk signal during underwriting.

Know Georgia's statute of limitations on debt. The state uses a six-year limit for most written contracts, including credit cards and personal loans. Old collection accounts approaching that threshold may fall off your report naturally. Before you pay a collector on an old debt, verify its age and understand whether payment could restart the reporting clock.

A 30-point improvement in your credit score before closing can mean the difference between a 10% down payment and a 3.5% down payment on an FHA loan. On a $275,000 home, that's over $17,000 you keep in your pocket.

The Bottom Line: Your Atlanta Bad Credit Loan Path Starts Today

Bad credit creates obstacles. It does not create permanent walls.

The programs in this guide, like FHA loans, Georgia Dream, Invest Atlanta, VA, and USDA products, credit union personal loans, and CDFIs, all exist because lenders and government agencies recognize that credit scores don't tell the full story of a borrower's reliability or potential.

Your next move is concrete: pull your credit reports today, schedule a free session with a HUD-approved counselor through ANDP, and contact a Georgia Dream-approved lender. Come prepared with documentation of your income, employment history, and any assets you hold.

Atlanta's housing market won't wait. And now that you know your options, neither should you.