Can Bad Credit Block Your Student Loan?

The short answer: No. Bad credit won't prevent you from getting student loans. Federal student loans don't require credit checks for most borrowers, and private loan options exist even with poor credit history.

Whether you have a FICO score below 620 or limited credit history, you can still finance your education. Understanding your options helps you make informed decisions about funding college.

Your Student Loan Options

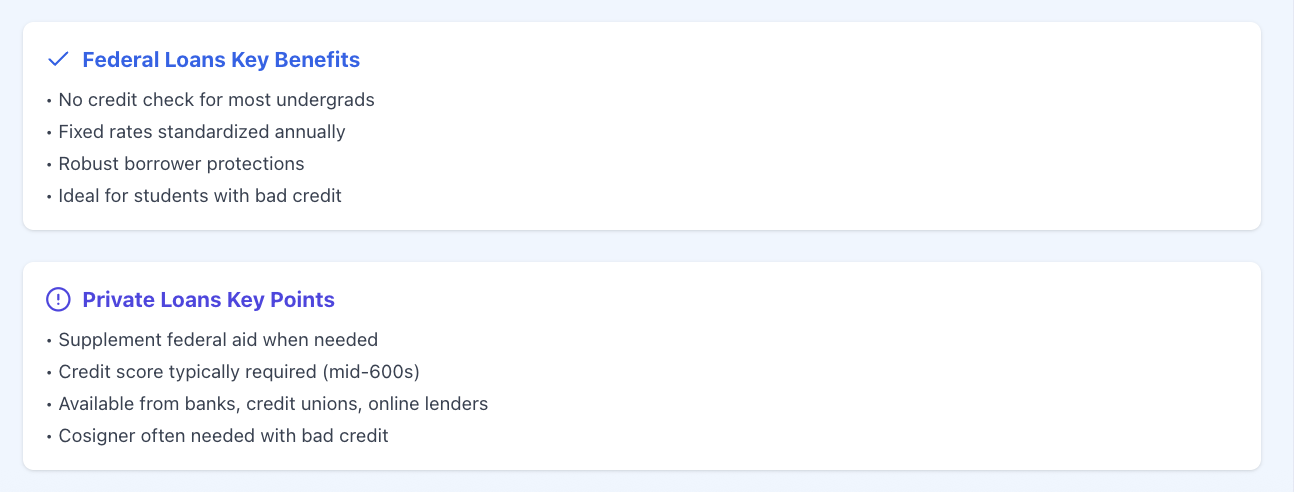

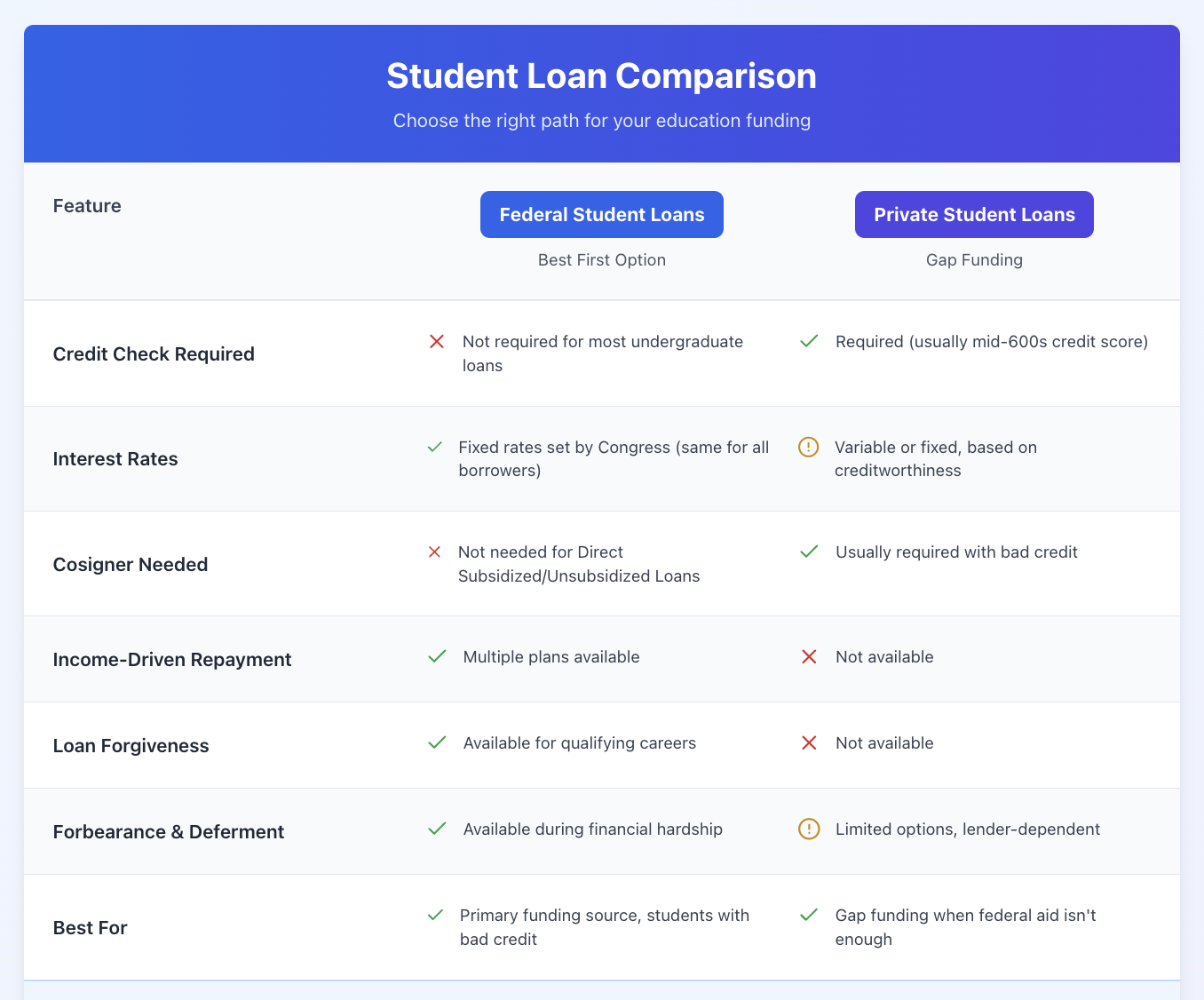

1. Federal Student Loans (Best First Option)

Federal loans come from the U.S. Department of Education and don't consider credit scores for most borrowers. These loans offer competitive fixed rates and robust borrower protections, making them ideal for students with bad credit.

Benefits of federal loans:

- No credit check required for most undergraduate loans

- Fixed interest rates set by Congress (same for all borrowers)

- Income-driven repayment plans available

- Loan forgiveness programs for qualifying careers

- Forbearance and deferment options during financial hardship

- No cosigner needed for Direct Subsidized and Unsubsidized Loans

Current federal loan rates for 2025-26: Federal student loan interest rates are standardized annually and apply equally to all borrowers regardless of credit history.

Recommended Read: How to Apply for Student Loans Without Damaging Your Credit Score

2. Private Student Loans (Gap Funding)

Private loans from banks, credit unions, and online lenders can supplement federal aid when you need additional funding. While these typically require good credit (usually a score in the mid-600s), you have options with bad credit.

Below is a side-by-side comparison of these two options:

How to Apply for Federal Student Loans

Eligibility Requirements

To qualify for federal student aid, you must:

- Be a U.S. citizen or eligible noncitizen

- Have a valid Social Security number

- Be enrolled or accepted in an eligible degree or certificate program

- Demonstrate financial need (for some loan types)

- Maintain satisfactory academic progress

- Register with Selective Service (if male and 18-25)

Complete the FAFSA

The FAFSA application for 2025-2026 opened on Nov. 21 for the upcoming school year. Submit it as early as possible since some aid is awarded first-come, first-served.

The FAFSA determines your eligibility for:

Direct Subsidized Loans

- Available based on financial need

- Government pays interest while you're in school

- Only for undergraduate students

- Borrowing limits apply

Direct Unsubsidized Loans

- Available regardless of financial need

- Interest accrues during all periods

- Available to undergraduate and graduate students

- Higher borrowing limits than subsidized loans

Direct PLUS Loans

- For graduate students or parents of undergraduates

- Credit check required but no minimum score

- Can borrow up to full cost of attendance

- Starting July 2026, new parent PLUS loans have an annual limit of $20,000 and aggregate limit of $65,000

Direct Consolidation Loans

- Combines multiple federal loans into one

- Simplifies repayment with single monthly payment

- May extend repayment term

Important Guide: Understanding MOHELA PSLF Issues: What You Need To Know About Your Student Loan

Getting Private Student Loans with Bad Credit

Strategy 1: Add a Creditworthy Cosigner

A cosigner with strong credit and stable income significantly improves your approval odds and interest rate. The cosigner shares equal responsibility for the debt, so ensure you can make timely payments.

Cosigner benefits:

- Access to lower interest rates

- Better loan terms

- Increased approval likelihood

- Possible cosigner release after consistent payments

Strategy 2: Choose No-Credit-Check Lenders

Some private lenders evaluate applications based on factors beyond credit scores:

Outcomes-based lenders assess:

- Expected earning potential based on your major

- School attendance and enrollment status

- Academic performance

- Program completion likelihood

Income-share agreements offer:

- No upfront payments

- Repayment based on future income percentage

- Payment caps and forgiveness terms

Strategy 3: Improve Your Credit Profile

Before applying for private loans:

- Keep credit card balances below 30% of your credit limit

- Pay all bills on time for several months

- Dispute any credit report errors

- Reduce outstanding debt where possible

Understanding Bad Credit in Student Loan Context

According to credit bureau Experian, a score between 580 and 669 ranks as "fair," while 300 to 579 ranks as "very poor". These ranges may affect private loan approval, but won't impact federal loan eligibility.

What lenders see:

- Payment history (35% of score)

- Credit utilization (30% of score)

- Length of credit history (15% of score)

- Credit mix (10% of score)

- New credit inquiries (10% of score)

Alternative Funding Options

Scholarships and Grants

Free money that doesn't require repayment. Search for:

- Merit-based scholarships through your school

- Need-based grants via FAFSA

- Private scholarships from organizations and companies

- Employer tuition assistance programs

Work-Study Programs

Federal work-study provides part-time jobs for students with financial need, helping you earn money for education expenses while gaining work experience.

School Payment Plans

Many colleges offer installment plans letting you spread tuition payments over the semester or year without interest charges.

Private Lenders for Bad Credit Borrowers

Top Options (December 2025)

Several lenders specialize in serving borrowers with limited or poor credit:

Ascent: Offers outcomes-based loans evaluating your earning potential and major rather than requiring traditional credit checks or cosigners.

Funding U: Provides loans to high-achieving students without credit checks or cosigners, though availability is limited in some states.

MPOWER Financing: Specializes in loans for international students and DACA recipients, with no cosigner required.

How Student Loans Affect Your Credit

Building Credit Through Loans

Making consistent on-time payments helps establish positive credit history. Federal and private student loans appear on credit reports and demonstrate responsible borrowing.

Credit Score Impact

- Hard inquiries: Private loan applications cause temporary score dips (usually 5-10 points)

- On-time payments: Build positive payment history over time

- Missed payments: Damage your score significantly

- Default: Severely impacts credit and triggers collection actions

Red Flags to Avoid

Watch out for:

- Lenders requiring upfront fees before approval

- Guaranteed approval claims without credit checks

- Pressure to borrow more than you need

- Confusing or hidden terms and conditions

Tips for Managing Student Loans with Bad Credit

- Borrow only what you need: Calculate actual costs, including tuition, fees, room, board, and books.

- Explore all federal options first: Exhaust subsidized and unsubsidized loans before considering private borrowing.

- Compare multiple private lenders: Prequalification lets you check rates without hard credit pulls.

- Understand repayment terms: Know when payments start, how much you'll owe monthly, and total repayment cost.

- Create a repayment strategy: Plan how you'll manage payments after graduation before borrowing.

- Monitor your credit: Regular monitoring helps you track improvement and catch errors early.

Frequently Asked Questions

Q: Can I get student loans with a 500 credit score? Yes. Federal loans don't consider credit scores. Private loans will be challenging, but outcomes-based lenders or using a cosigner makes approval possible.

Q: Will applying for student loans hurt my credit? Federal applications don't affect credit. Private loans require hard inquiries, though prequalification checks don't impact scores.

Q: What if I don't have any credit history? Most federal loans require no credit history. Private lenders may offer first-time borrower programs or outcomes-based options.

Q: How long does bad credit affect student loan eligibility? Bad credit permanently affects federal loan eligibility for undergraduates minimally. Private lenders typically require 12-24 months of credit rebuilding for better rates.

Q: Can I refinance student loans with bad credit later? Refinancing typically requires good credit (670+ FICO score). Focus on building credit through on-time payments before refinancing.

Next Steps

- Complete the FAFSA: Start with federal aid applications immediately

- Accept federal loans first: Maximize lower-cost federal borrowing

- Research private options: If needed, compare lenders accepting bad credit

- Consider credit building: Work on improving your score for future borrowing

- Create a budget: Plan how you'll manage repayment after graduation

Building Your Financial Future

Bad credit doesn't have to derail your educational goals. With federal loans as your foundation and strategic use of private loans when necessary, you can finance your education successfully.

Focus on making consistent payments once repayment begins. This establishes positive credit history and opens doors to better financial opportunities after graduation.

Ready to improve your credit? Contact ASAP Credit Repair to build a strong financial foundation for your educational journey and beyond.