Finding RJM Acquisitions on your credit report creates a different problem than finding most collection agencies.

Many RJM accounts involve very old debt.

Sometimes the debt is so old that consumers do not even remember the original account. Other times, the debt has changed hands multiple times before appearing under RJM Acquisitions.

That raises an important question.

Should the account still be reporting at all?

I've seen people preparing for mortgages discover an RJM account they had not thought about for years. In some cases, the debt was accurate. In others, reporting dates, balances, or account details deserved a closer look.

That is why RJM disputes often start differently than disputes involving newer collection accounts.

Before paying anything, you need to determine:

how old the debt is

whether reporting is accurate

whether validation is available

whether the account is affecting financing plans

This guide explains when RJM Acquisitions can be removed, when disputes make sense, and what borrowers should understand before taking action.

Can RJM Acquisitions Be Removed From Your Credit Report?

With the right strategy, RJM Acquisitions can be removed from your credit report. But the best approach depends on the age of the debt and whether the information is being reported accurately.

Because RJM often purchases older debt, the first step is to verify the reporting dates, balance, and ownership of the account. If the information is inaccurate, incomplete, or cannot be properly validated, you may have grounds to dispute the account with the credit bureaus.

In some cases, the debt may be old enough that reporting errors, obsolete information, or missing documentation create opportunities for removal.

That is why reviewing the account carefully before paying or settling is important, especially if you're preparing for a mortgage or other major financing.

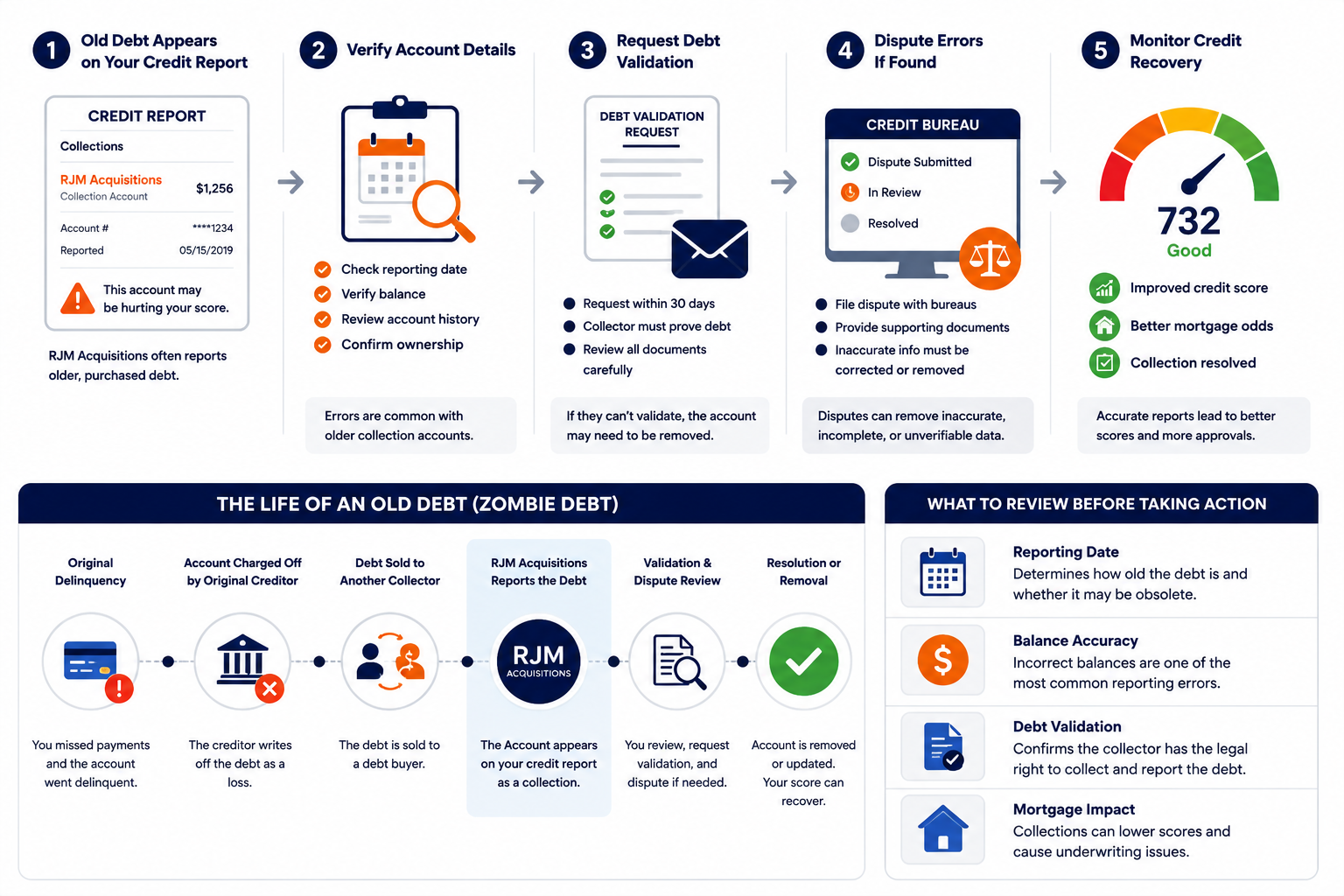

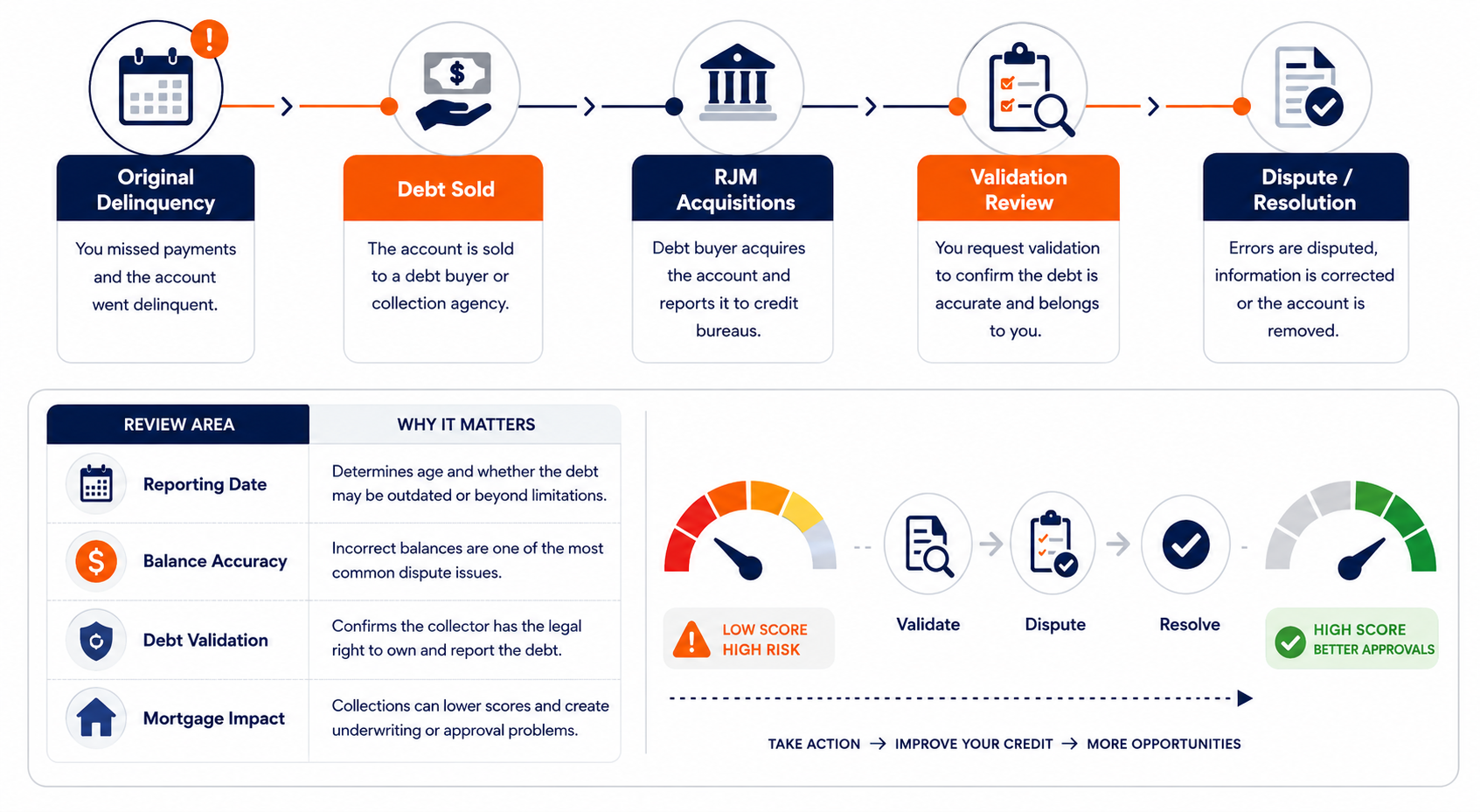

How Old Debt Can End Up on Your Credit Report

An older collection account can create problems during mortgage underwriting.

The timeline above shows the path from original delinquency to validation, dispute review, and potential credit recovery.

Who Is RJM Acquisitions

RJM Acquisitions LLC is a debt buyer that purchases old, charged-off consumer accounts , primarily credit card debt , and attempts to collect the stated balance. What distinguishes RJM from most debt buyers is their focus: they specifically target accounts that are often past the statute of limitations. The Federal Trade Commission investigated RJM in 2012 for collecting on legally unenforceable debt. After that investigation, RJM now discloses in their letters that consumers cannot be sued on the debt.

RJM does not operate like Portfolio Recovery Associates or Midland Credit Management.

They do not make outbound phone calls. They send letters. They wait for consumers to call them back. Credit bureau reporting is their collection tool. Lawsuits are not an option for them.

This matters because the entire RJM collection model depends on consumers not knowing two things. First: the debt is probably past the statute of limitations. Second: the account may be approaching or past the seven-year FCRA reporting limit.

Keep both of those numbers in mind before taking any action on an RJM account.

Why RJM Acquisitions Appears on Credit Reports

RJM Acquisitions appears on credit reports because they purchased a charged-off account from an original creditor or another debt buyer. The original account defaulted years earlier. The original creditor sold the debt at a deep discount. The debt may have changed hands multiple times before RJM acquired it. RJM then reports the account to credit bureaus under their name , which is how consumers first discover them.

The discovery is often a surprise.

Most people who find RJM on their report do not recognize the name. They remember the original credit card issuer. They do not remember RJM because they never had a relationship with RJM , RJM bought the account after the default, often years later.

The account on your credit report may show RJM Acquisitions as the creditor even though the original lender was a bank you closed an account with half a decade ago.

Why RJM Acquisitions Is Linked to Zombie Debt

RJM Acquisitions specifically purchases debt that is often past the statute of limitations , debt so old that collectors cannot win a lawsuit on it. The Federal Trade Commission investigated RJM in 2012 specifically for collecting on this type of time-barred debt. Zombie debt is old, charged-off debt that resurfaces through debt sales. RJM's business model is built around exactly this category of account.

FTC File No. 1223020 (August 2012): The FTC's Division of Financial Practices investigated RJM Acquisitions LLC for possible violations of the FDCPA and Section 5 of the FTC Act for collecting on debts beyond the statute of limitations. The investigation confirmed RJM purchases and collects on time-barred debt. Post-investigation, RJM now discloses to consumers in writing that the debt is past the statute of limitations and they cannot be sued on it. RJM also sends letters only , no outbound calls. The FTC closed the investigation but the disclosure requirement changed how RJM operates.

Zombie debt matters in this context for three reasons.

The debt may be uncollectable in court. If the statute of limitations has expired, RJM cannot sue you and cannot win a judgment. Their only tool is credit bureau reporting. Knowing this changes how you respond.

The debt may be obsolete for credit reporting. If the original delinquency date is more than seven years ago, the account should not appear on your credit report at all. The FCRA requires removal regardless of whether the debt is still technically owed. Many RJM accounts are at or near this threshold.

The ownership documentation often does not exist. Debt that changes hands multiple times loses records at each transfer. Original account agreements, charge-off documents, and assignment chains degrade or disappear. RJM may not be able to produce documentation proving ownership of the debt they are collecting.

As Bankrate's zombie debt guide explains, making any payment on a zombie debt , even a small one , can restart the statute of limitations clock in some states, giving the collector renewed legal access to a debt that was previously unenforceable. With RJM specifically, this risk is real. Do not pay before verifying the age of the debt.

Can RJM Acquisitions Be Removed From Your Credit Report

Yes. The right removal path depends on the account's age and whether the information is accurate. Before anything else , find the original delinquency date. That single date determines whether the account is obsolete (must be removed), disputable (inaccurate reporting), or validatable (RJM may not have documentation). Most RJM accounts fall into one of the first two categories.

Find the RJM account on each bureau that shows it. Note which bureaus carry the account. An error corrected on one bureau may not automatically correct on others , you need to dispute each separately. Also check whether the original creditor's charge-off entry still appears alongside the RJM entry. Both reporting simultaneously may represent a disputable duplicate negative entry.

Free | Required first step for every pathThe original delinquency date is when you first missed a payment on the original account , not when the account was charged off, not when it was sold to RJM, not when RJM first reported it. Pull the original creditor's entry from your credit report to find this date. Count from that date to today. If more than seven years: dispute as obsolete immediately. If approaching seven years: do not pay , let it age off. If under seven years: evaluate the validation and dispute options below.

This date controls everything | Do not take action before confirming itRJM may report the account with a date that appears more recent than the actual original delinquency. This is re-aging , it makes the account look newer than it is and extends the apparent reporting window. If the date RJM shows differs from what the original creditor reported as the first delinquency, dispute the re-aging directly under the FCRA. Re-aging is illegal and requires immediate correction or removal.

Re-aging = FCRA violation | Grounds for immediate dispute and possible damagesWithin 30 days of first contact (first letter or first credit report appearance), send a written validation request. Request: original creditor name, original account number, complete chain of ownership from original creditor to RJM, itemized balance, and any documentation proving the debt is within the FCRA reporting window. RJM specializes in old debt , original documentation frequently does not survive multiple ownership transfers. An incomplete validation response is grounds for a bureau dispute.

Certified mail, return receipt | 30-day FDCPA window from first contactRJM must provide a complete chain of title from the original creditor through every intermediary owner to RJM. A generic letter stating the debt is valid is not validation. A bulk purchase agreement referencing a portfolio without naming your specific account number may be insufficient. An account statement generated by RJM's own system is not original creditor documentation. Any gap in the response supports a bureau dispute.

Incomplete = grounds for bureau dispute | Keep every piece of RJM's responseDispute separately with Equifax, Experian, and TransUnion. Include the validation letter you sent, RJM's incomplete response, and any specific inaccuracies: re-aged dates, wrong balance, obsolete reporting window, or missing documentation. Each bureau investigates independently and has 30 days to respond. If RJM cannot verify the specific account information during the investigation window, the bureau must remove or correct it.

Dispute all three separately | 30-day investigation window per bureauIf a bureau "verifies" the account despite your dispute and RJM's incomplete validation, escalate. File a CFPB complaint against both the bureau and RJM. Request the bureau's method of verification. Consumer protection attorneys frequently pursue FCRA claims against bureaus that fail to conduct reasonable investigations. The FCRA entitles you to actual damages, statutory damages up to $1,000, and attorney fees if your rights were violated.

CFPB complaint + method of verification request | FCRA claim: 2-year statute of limitationsHow to Dispute RJM Acquisitions

Dispute RJM through the credit bureaus using the FCRA process. Provide: your debt validation letter to RJM, their response (complete or incomplete), and any evidence of reporting errors , wrong dates, wrong balance, re-aging. Submit disputes to each bureau showing the account. Equifax, Experian, and TransUnion each have 30 days to investigate and must remove or correct inaccurate information they cannot verify.

Many consumers skip verification and call RJM directly to discuss the debt.

This is a mistake in most RJM cases. The reason: acknowledging the debt in some states can restart the statute of limitations clock. A phone call where you confirm you owe the balance , even in passing , may constitute an acknowledgment. RJM collects on time-barred debt. You do not want to inadvertently give them renewed legal standing on an account they previously could not sue on.

Communicate in writing only. Certified mail. Keep the return receipt. Keep copies of everything.

As noted in NerdWallet's zombie debt guide, time-barred debt collectors rely on consumers not knowing the statute of limitations has expired. Knowledge of the SOL timeline is the single most important defense against collectors like RJM who specifically purchase this category of account. As the the FTC's debt collection rights guide explains, consumers have the right to request written validation of any debt before making any payment decision , and collectors must stop all collection activity until they respond with adequate documentation. With RJM, whose business depends on old debt with often-missing records, this validation requirement is their most significant operational challenge.

Understanding exactly what documentation collectors must provide when you request validation tells you what RJM's response needs to contain , and what gaps in their response mean for your dispute.

What Happens If RJM Acquisitions Cannot Validate the Debt

If RJM cannot validate the debt with complete documentation, they must cease collection activity and cannot continue reporting the account. You then dispute with the credit bureaus showing the validation failure. During the bureau's investigation window, RJM must verify the specific account information. If they cannot , because documentation no longer exists , the bureau must remove the account. Many RJM accounts do not survive this process because the records simply are not there anymore.

RJM's documentation problem is structural, not accidental.

They purchase portfolios of old debt in bulk. Original account agreements, charge-off documents, and assignment records from 2015 or 2017 do not reliably travel through two or three subsequent debt sales. RJM receives a file with account numbers, names, and balances , but not necessarily the underlying contractual documentation that proves ownership and accuracy.

This is why validation requests work disproportionately well against RJM. They cannot produce what does not exist.

Can Paying RJM Acquisitions Improve Your Credit Score

Paying RJM does not automatically remove the account from your credit report. It changes the status from "unpaid collection" to "paid collection." Both statuses remain on the report until the seven-year mark from the original delinquency. A paid collection still damages your score , less severely than an unpaid one, but the entry stays. Paying without a written pay-for-delete agreement does almost nothing for your score in the short term.

The common misconception: paying a collection fixes the credit problem.

It does not. The account stays on your report. The damage stays. What changes is the account status , which matters for mortgage underwriting but does not remove the derogatory entry from the file or significantly change the scoring impact.

Before paying anything to RJM, understand three things.

Payment may restart the SOL. In some states, a payment on a time-barred debt restarts the statute of limitations clock. RJM collects on old, often time-barred debt. A $1 payment could give them renewed legal authority on a debt they currently cannot sue on. Check your state's SOL rules before paying anything.

Payment without a pay-for-delete agreement leaves the entry on the report. A paid collection hurts less than an unpaid one but still hurts. If you must pay, negotiate a written pay-for-delete agreement first. Get confirmation in writing that RJM will remove the tradeline from all three bureaus upon receipt of payment. Without that agreement in writing, paying changes nothing on the report.

Mortgage underwriters treat paid and unpaid collections differently. For FHA loans, individual lenders may require collections to be paid before closing. For conventional loans, collections under $2,000 are often ignored in underwriting calculations. Know which loan type applies to your situation before deciding whether payment is necessary at all.

Should You Settle or Dispute RJM Acquisitions

Dispute first in almost every RJM case. RJM focuses on old debt they often cannot fully document. Validation requests frequently reveal gaps that support bureau removal without payment. Settlement makes sense only when the debt is verified, within the seven-year reporting window, and paying would produce a documented pay-for-delete agreement and a genuine improvement in the credit picture.

| Your Situation | Best First Step | Why |

|---|---|---|

| Original delinquency over 7 years ago | Obsolete dispute immediately | Account should not be on your report at all. Remove regardless of validity. |

| Original delinquency is re-aged on the report | FCRA dispute , re-aging violation | Illegal reporting. Bureau must correct or remove. |

| RJM cannot validate with complete documentation | Bureau dispute after validation failure | No valid documentation = no reporting right. Dispute cites insufficient validation. |

| Balance reported does not match original creditor records | Inaccuracy dispute | Collectors cannot inflate balances beyond what the original contract authorized. |

| Debt is valid, within 7 years, within SOL | Settle with pay-for-delete in writing | Dispute unlikely to succeed on valid accurate accounts. Negotiate removal with payment. |

| Within 2 years of original delinquency | Validate first, then evaluate | Debt may be sueable. Do not acknowledge or pay before confirming documentation gap. |

| Mortgage application blocked by RJM | Case-by-case , verify loan type first | FHA and conventional lenders treat collections differently. Know the requirements before paying. |

Can RJM Acquisitions Hurt Mortgage Approval

Yes. An RJM collection on your credit report can affect mortgage pre-approval, rates, and underwriting decisions. The impact depends on the loan type, the account balance, and how many collection accounts total appear on your file. Borrowers often discover RJM during the mortgage process , not before. That timing creates pressure to pay quickly, which is exactly when the payment-before-validation mistake is most likely.

This section is for borrowers who found RJM while preparing for a home purchase.

Mortgage lenders pull all three bureau reports. RJM appears on Experian, Equifax, or TransUnion , sometimes all three. Every underwriter sees it. How they handle it depends on loan type:

- FHA loans. Individual lenders set their own collection policy within FHA guidelines. Many require collections to be paid , or at minimum explained , before closing. An unpaid RJM account over $1,000 typically requires documentation of a payment plan or payoff.

- Conventional loans (Fannie Mae / Freddie Mac). Collections under $2,000 are generally excluded from debt-to-income calculations. Multiple smaller collections may be treated differently. Anything over $2,000 may require resolution before the lender approves the file.

- VA and USDA loans. Underwriter discretion is wider. The age, balance, and payment status of the collection matter more than a rigid threshold. An old, low-balance RJM account near the seven-year mark often gets approved without payment.

The worst mistake in the mortgage process: paying RJM without a pay-for-delete agreement simply because a lender told you to resolve the collection. A paid collection on the report , without actual deletion , may still create underwriting friction. Get deletion confirmed before paying anything.

How Long Can RJM Acquisitions Stay on Your Credit Report

Seven years from the original delinquency date , the date you first missed payment on the original account. Not from when RJM bought the debt. Not from when RJM first reported it. The original delinquency date controls the removal timeline. When that date is more than seven years ago, the account is obsolete and must be removed. RJM cannot extend the reporting window by purchasing the debt later or reporting it under a newer date.

The FCRA is explicit on this point. Section 605 limits adverse credit reporting to seven years from the original date of delinquency. No subsequent sale, reactivation, or new collection agency changes that clock.

Where RJM creates problems is re-aging. If they report the account using a date that reflects when they purchased the debt , rather than the original delinquency , your credit report may show an account that appears newer than it actually is. This extends the effective damage period beyond the legal limit.

To check for re-aging: compare the date RJM shows on your credit report to what the original creditor shows as the first delinquency. If they differ by more than a few months, dispute the date discrepancy with each bureau as an FCRA re-aging violation.

Understanding your state's statute of limitations on credit card debt gives you the second critical number alongside the seven-year FCRA limit , knowing both tells you exactly what RJM can and cannot legally do regarding your specific account.

What Is the Best Strategy for Removing RJM Acquisitions

The best strategy follows this order: check the original delinquency date first, then dispute as obsolete if past seven years, then request validation if within seven years, then dispute with bureaus using validation gaps, then settle with pay-for-delete only if the debt is valid and verified. Never start with payment. Most RJM accounts have a clear dispute path before any payment conversation becomes necessary.

| Strategy | Best For | Potential Outcome |

|---|---|---|

| Obsolete debt challenge | Original delinquency over 7 years ago | Mandatory removal , no RJM response required |

| Re-aging FCRA dispute | RJM's date differs from original delinquency date | Correction or removal of the inaccurate entry |

| Debt validation request | Within 30 days of first contact | Stops collection activity; gaps support bureau dispute |

| Bureau dispute , insufficient validation | RJM cannot produce complete ownership documentation | Removal if RJM cannot verify during 30-day window |

| Pay-for-delete settlement | Debt is valid, verified, within 7 years | Resolved balance plus removal , only with written agreement |

| CFPB complaint | FDCPA or FCRA violations by RJM or the bureaus | Regulatory pressure; possible damages claim |

| Professional dispute support | Mortgage timeline pressure, multiple accounts, escalated disputes | Managed dispute process with documented outcomes |

Some borrowers handle RJM disputes themselves. The process is not complicated for a single account with a clear obsolete date or a straightforward validation gap. Fill out the bureau dispute form. Attach the documentation. Wait 30 days.

Others choose professional help when RJM appears alongside multiple other collectors, when a mortgage timeline creates pressure, or when RJM disputes the bureau correction and the account keeps coming back.

When collection accounts like RJM affect financing goals, apartment approvals, or employment screenings, the stakes of a poorly executed dispute are higher than the time saved by handling it alone.

Can RJM Acquisitions be removed from a credit report?

Yes. The fastest path is an obsolete debt challenge if the original delinquency date is more than seven years ago , the account must be removed regardless of whether the debt is still technically owed. Within the seven-year window, a debt validation request often reveals that RJM cannot produce complete ownership documentation, which supports a bureau dispute. If the debt is valid and verified, a written pay-for-delete agreement before payment can produce removal. Do not pay without a written deletion agreement.

Does RJM Acquisitions sue consumers?

Generally no. After the 2012 FTC investigation, RJM now discloses in writing to consumers that the debt is beyond the statute of limitations and they cannot sue on it. RJM does not make outbound collection calls , they send letters and accept inbound calls. Credit bureau reporting is their primary collection tool. If RJM threatens a lawsuit on time-barred debt in their communications, document it immediately and file a CFPB complaint. That specific threat on time-barred debt is an FDCPA violation.

Can obsolete debt be removed from my credit report?

Yes. The FCRA prohibits reporting adverse accounts for more than seven years from the original delinquency date. When that date passes, the account is legally obsolete and must be removed. You do not need to prove the debt is inaccurate, invalid, or paid. The age alone is sufficient grounds for removal. Dispute the account with each bureau as "obsolete per FCRA Section 605." Bureaus typically remove obsolete accounts within 30 days of a correctly filed dispute.

Should I pay RJM Acquisitions to improve my credit score?

Not without first checking the original delinquency date and validating the debt. If the account is past seven years, it must be removed , payment changes nothing about the removal timeline and may restart the statute of limitations in some states. If within seven years, validate first. If RJM cannot validate, dispute for removal instead. Payment only makes sense when the debt is verified, valid, within the reporting window, and you have a written pay-for-delete agreement in hand before sending any money.

Can RJM Acquisitions affect my mortgage approval?

Yes. Collection accounts appear in mortgage underwriting. The impact depends on the loan type, account balance, and whether it is paid or unpaid. FHA lenders often require collections to be resolved. Conventional lenders may ignore collections under $2,000. VA and USDA lenders use more underwriter discretion. Never pay an RJM account to satisfy a lender demand without first confirming exactly what the underwriter requires , sometimes a letter of explanation, a payment plan, or a documented dispute satisfies the requirement without full payment.

-

Debt Validation , When Collectors Must Prove You Owe The debt validation letter is your first and most powerful tool against RJM Acquisitions. This covers exactly what RJM and other collectors must provide when you request validation, what counts as acceptable documentation versus a brush-off response, and how to use validation failures to build a bureau dispute that results in removal without payment. The most relevant guide for executing Step 4 of the removal framework above.

-

Statute of Limitations on Credit Card Debt , State-by-State Guide RJM Acquisitions was investigated by the FTC specifically for collecting on time-barred debt. This guide covers the statute of limitations for credit card debt in every state , so you know whether RJM can legally threaten to sue on your specific account, whether payment would restart the clock, and when the debt crosses into the legally unenforceable zone that removes their only real threat.

-

How to Remove Portfolio Recovery Associates From Your Credit Report Portfolio Recovery Associates and RJM Acquisitions both specialize in purchasing old charged-off debt and use credit bureau reporting as their primary collection tool. This covers the full dispute process for PRA , validation strategy, settlement vs dispute comparison, FDCPA violations, and pay-for-delete negotiation , using the same framework that applies to RJM accounts within the seven-year reporting window.