Paying a settlement does not automatically stop a lawsuit. A case only ends when the creditor agrees to the terms and files a dismissal with the court. Without that step, the lawsuit can still move forward even if payment has been made.

Under civil procedure rules, both parties must formalize the resolution. In practice, this is where problems occur. In cases we handle, some defendants pay a settlement based on verbal terms or informal agreements, expecting the case to close. If the agreement is not documented and filed, the court record does not change, and the case can proceed toward judgment.

A proper settlement includes written terms, confirmation of payment conditions, and a filed dismissal or stipulation with the court. The timing also matters. If the case is close to a hearing or default stage, delays in filing can still lead to adverse outcomes.

This article explains when a settlement stops a lawsuit, what documents are required, and how to make sure the case is formally closed.

Will Paying a Settlement Stop a Lawsuit Immediately?

No. Paying a settlement does not stop a lawsuit immediately.

Payment and dismissal are two separate legal steps. After you pay, the creditor must still file a formal dismissal with the court. Until that document is filed, the case stays open. If the creditor's attorney does not file the dismissal, the lawsuit continues even after your money has cleared. This is why you get the settlement in writing before you pay - not after.

Key Takeaways

Payment alone does not end a lawsuit. The creditor must separately file a dismissal with the court after receiving payment.

Require dismissal with prejudice in writing before you pay. This prevents the creditor from filing the same lawsuit again.

In California, the creditor may file a Notice of Settlement (form CM-200) and has up to 45 days to file the Request for Dismissal (form CIV-110). Other states have different timelines.

If the creditor does not file the dismissal as agreed, you have a written settlement agreement to enforce. Without that document, you have no legal recourse.

As CBS News reports, creditors often accept 30% to 60% of the balance to avoid litigation costs, even after a lawsuit is filed.

File an Answer to the lawsuit first before entering settlement talks. The Answer prevents a default judgment while you negotiate.

My Perspective: The most common and costly settlement mistake I see: the person pays, assumes the lawsuit is over, and finds out months later that the case never closed. The creditor's attorney never filed the dismissal. The judgment was entered. Wages got garnished. All of it preventable with one document signed before the money moved. This article explains exactly what has to happen for a lawsuit to actually stop, what dismissal with prejudice means, and the sequence of steps that protects you.

Why Paying a Settlement Does Not Automatically Stop a Lawsuit

A lawsuit is a court proceeding. Paying money to the other side is a financial transaction. Courts are not notified when money changes hands between two parties. The court only knows the case is resolved when the plaintiff files a formal dismissal document. Until that filing happens, the case remains active on court records. The judge has no way to know you paid.

This distinction matters because a lot of people assume a settlement is the same as a case resolution. It is not. A settlement is an agreement between two private parties. A lawsuit is a matter of public court record. Those two things operate on separate tracks, and bridging them requires a specific legal filing: the dismissal.

As the California Courts self-help guide states clearly: "Your case won't be dismissed automatically if you settle. The plaintiff should dismiss the case as part of your agreement." This applies in every state, not just California. Courts across the country operate the same way. Payment does not trigger automatic case closure.

"I settled with the debt collector for $1,800 on a $3,400 balance. Paid by cashier's check. Thought it was done. Six weeks later I got a notice that a judgment had been entered against me. Turns out their attorney never filed the dismissal. I had no written agreement requiring it. Took another three months and a lawyer to get the judgment vacated. Cost me more than I saved on the settlement." Reddit r/personalfinance · Debt settlement without dismissal requirement, 2025Settled $3,400 debt for $1,800. No written dismissal requirement. Judgment entered 6 weeks later. Required attorney to vacate. Outcome worse than the original debt.

That outcome is common and preventable. The fix is simple: the settlement agreement must include a written requirement that the creditor file a dismissal with the court as a condition of receiving payment. No written requirement, no protection. The creditor keeps your money and keeps the lawsuit.

What Has to Happen for a Lawsuit to Stop After Settlement

Settlement Agreement Signed: Both parties sign written agreement including dismissal requirement. You keep a copy.

Payment Made: You pay the agreed amount by traceable method. Get written receipt.

Creditor Files Dismissal: Creditor's attorney files dismissal with prejudice with the court. This step is NOT automatic.

Court Processes Filing: Court records the dismissal. Timeline: days to weeks depending on state and court.

Case Closed: Case appears as dismissed on public court records. Creditor cannot refile for same debt.

What Is Dismissal With Prejudice and Why It Matters

Dismissal with prejudice permanently ends the lawsuit and bars the creditor from filing the same claim again. Dismissal without prejudice ends the current case but allows the creditor to refile later. When settling a debt lawsuit, always require dismissal with prejudice. If the creditor only offers dismissal without prejudice, you are paying to pause the lawsuit, not end it.

The phrase "with prejudice" is legal shorthand for permanent. It means the cause of action is extinguished. The creditor accepted your payment as full resolution, and the court record reflects that. They cannot come back a year later claiming you still owe the same debt.

Dismissal without prejudice is used when a case is temporarily dropped, often so it can be refiled later. Some creditors try to offer this when they are uncertain about their documentation or want to keep pressure on you during payment plan negotiations. Do not accept it as a final resolution.

As CBS News reports in its debt lawsuit settlement guide, when negotiating a settlement you should "ask for a settlement that includes dismissal of the lawsuit with prejudice, meaning they cannot sue you again for the same debt. And, get everything in writing before making any payments." That sequence matters: writing first, payment second.

Can You Settle a Debt Lawsuit After You Have Been Served?

Yes. You can settle a debt lawsuit at any stage after being served, including before the response deadline, after filing your Answer, and even during trial preparation. Filing an Answer does not prevent settlement - it makes settlement more likely. Creditors become more willing to negotiate once they know you will contest the case rather than default. Most debt lawsuits settle before going to trial.

The moment you are served is not the moment to panic or to pay immediately. It is the moment to assess. Creditors and debt collectors file lawsuits, partly betting that you will not respond. When you file an Answer, that bet fails. The creditor now faces the time and cost of actual litigation. That changes their incentive toward settlement.

Filing your Answer before negotiating also protects you during settlement talks. If the creditor's attorney contacts you about settlement while your response deadline is still open and talks break down, you still have time to file your Answer. If you let the deadline pass while negotiating in good faith, the creditor can obtain a default judgment before any agreement is reached. File first, negotiate second.

"Debt collector sued me for $4,100. Filed my Answer myself using the court's online form. Three days later their attorney called me. We settled for $1,850. They sent a settlement agreement that said dismissal with prejudice. I paid. Confirmed the dismissal was filed on the court's website 10 days later. The whole thing from summons to closed case took about 6 weeks. Filing the Answer is what started the conversation." Reddit r/debtfree · Post-service settlement thread, 2025$4,100 sued, settled for $1,850. Answer filed first. Dismissal with prejudice in written agreement. Case confirmed closed via court website within 10 days of payment. Filing the Answer triggered settlement contact.

That pattern repeats across thousands of debt lawsuits annually. The Answer signals you are a prepared defendant. It does not guarantee a settlement, but it dramatically increases the odds the creditor contacts you rather than proceeding to trial.

What a Settlement Agreement Must Include to Stop the Lawsuit

The written settlement agreement is the document that bridges your payment and the court dismissal. If it does not specifically require the creditor to file a dismissal with prejudice, you have no enforceable obligation on their end. The agreement must be signed by both parties. You receive a copy. You pay after signing, not before.

File your Answer with the court before negotiating. Do not let the response deadline pass. Filing an Answer protects you from a default judgment during negotiations and signals to the creditor you will contest the case.

Make your settlement offer directly to the creditor's attorney. The law firm named in the summons is handling the case. Start at 25 to 35 percent of the balance. As CBS News confirms, creditors often settle at 30 to 60 cents on the dollar to avoid litigation costs. Do not reveal your ceiling in the first call.

Once both sides agree, request the written settlement agreement before paying. The agreement must include: the exact settlement dollar amount, the account number and original creditor name, a statement that this amount fully resolves the debt, a requirement that the creditor files a dismissal with prejudice within a specified number of days, and the credit bureau reporting status. Both parties sign it. You keep a signed copy.

Pay by traceable method after receiving the signed agreement. Cashier's check, certified check, or documented electronic transfer. Never pay in cash. Keep the payment confirmation and all correspondence from the creditor's attorney.

Verify the dismissal was filed with the court. Most state courts have online case lookup tools. Check 10 to 14 days after payment. If the dismissal has not been filed by the deadline in your agreement, send a certified letter to the attorney demanding they complete the filing. Keep that letter as evidence.

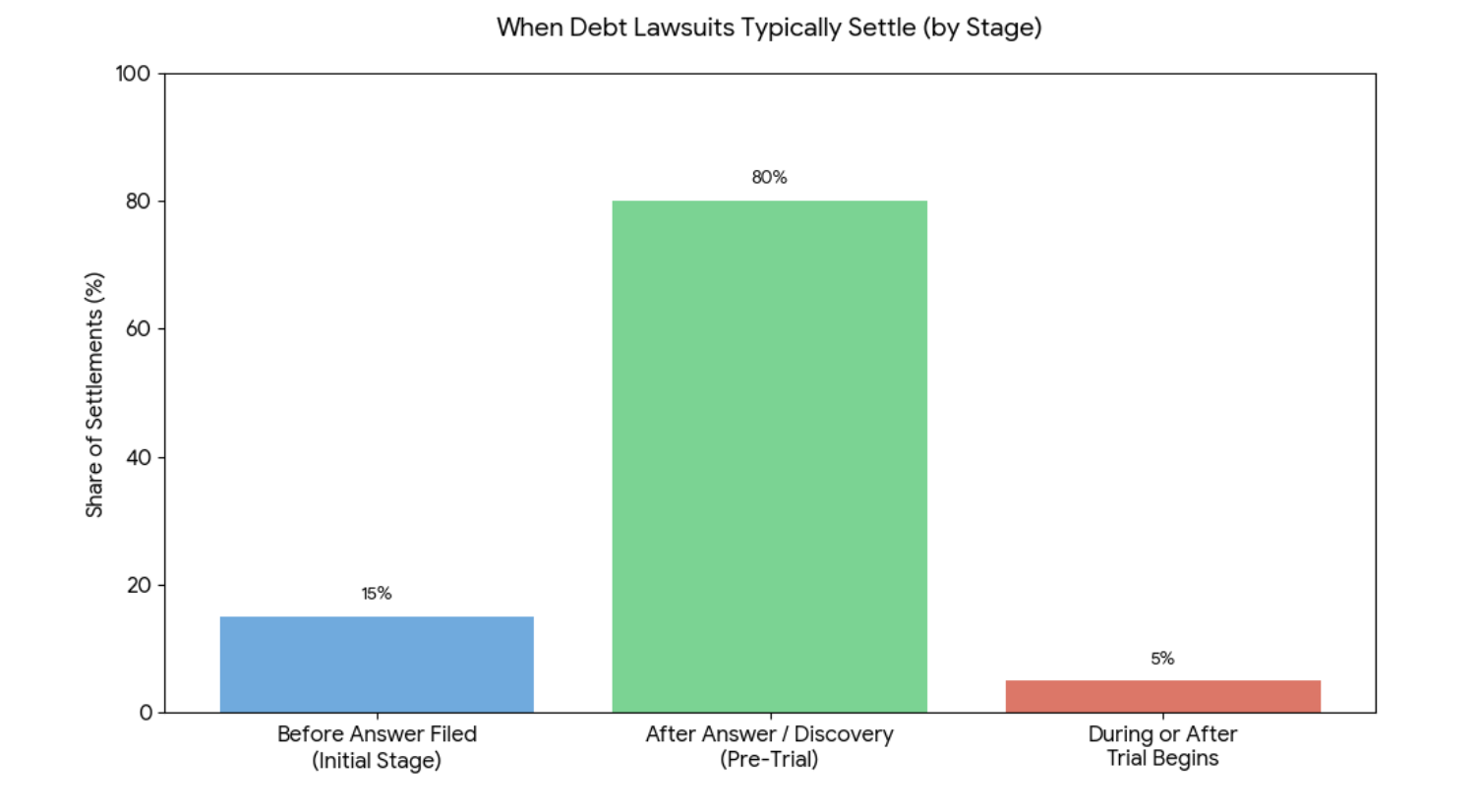

When Debt Lawsuits Typically Settle (by Stage) Industry pattern data

The chart shows why filing an Answer is critical. The largest settlement window is after the Answer is filed but before trial. That is when both sides are facing real cost. The creditor faces litigation expenses and the defendant faces an actual court date. That mutual cost pressure is what drives most settlements to a resolution both sides can accept.

Compare your options before settling. Settlement is not always the right move. If the debt is past the statute of limitations, the creditor may not have a valid case at all. If Velocity Investments, Midland Credit, or another debt buyer filed suit with incomplete chain-of-title documentation, that is a defense that may dismiss the case without payment. Our comparison of credit repair versus debt settlement covers which option applies to which type of account, how each affects your credit report, and the cases where repairing the report first produces a better outcome than settling the debt.

What Happens If You Settle Without a Written Agreement

If you pay without a written settlement agreement that requires dismissal, the creditor keeps your money and the lawsuit stays open. They can continue to seek a judgment for whatever balance they claim you still owe, including accrued interest and attorney fees. Payment without a written agreement is treated as a voluntary partial payment, not as a settlement. It does not stop the case and it does not protect you from a judgment.

Three things that happen when you pay without a written agreement: The creditor treats your payment as a credit on the account but the case stays active. They can continue toward a judgment for the remaining claimed balance. Any judgment entered after you paid does not automatically offset your payment - you may owe court costs and attorney fees on top of what you already paid. And you have no written proof of what was agreed, making it hard to dispute what the creditor later claims.

As CBS News explains in its debt lawsuit dismissal guide, when negotiating a settlement you must ensure it "includes a clause requiring the lawsuit to be dismissed before agreeing to it." The clause does not have to be complex. It just has to be in the document, signed, and returned to you before payment clears.

One more protection worth building into the agreement: request that the creditor report the account as "settled" rather than leaving the status as "charged off and unpaid." This is negotiable. Most creditors will agree because it is a small concession for them and it matters to your score. Our breakdown of lump sum settlement versus payment plan covers the exact language that goes into a settlement agreement for credit reporting purposes, what "settled" versus "paid in full for less than full balance" means on your report, and which notation is more likely to be accepted by future lenders.

"Creditor's attorney called me out of nowhere offering to settle for 50 percent. I said yes on the phone and sent them a check the next week. No written agreement. They cashed the check and then filed for a judgment on the remaining balance two months later. Judge said a verbal agreement is not enforceable in a debt case. I learned the hardest way: nothing matters until it is in writing and signed." r/legaladvice · Debt settlement phone agreement dispute, 2024Verbal-only settlement. Check cashed. Judgment filed on remaining balance 2 months later. Verbal agreements not enforceable in debt cases. Written signed agreement is mandatory before payment.

How Long Does It Take for a Case to Be Dismissed After Settlement?

The creditor's attorney must take action to file the dismissal. Courts do not close cases automatically. The timeline depends on the state, the attorney's speed, and court processing times. Most dismissals are filed within 10 to 30 days of payment. In California, the creditor may file form CM-200 (Notice of Settlement) and then has up to 45 days to file the actual dismissal via form CIV-110. Specify a deadline in your written agreement so you have something to enforce if they delay.

If you have paid and weeks pass without a filed dismissal, here is your next move. Send a certified letter to the law firm referencing the settlement agreement, the payment date, the payment amount, and the dismissal requirement they agreed to. Ask them to confirm in writing when they will file the dismissal. Keep that letter and any response as evidence. If they still fail to act, you may need to file a motion to enforce the settlement agreement with the court. A consumer law attorney can do this quickly and at low cost compared to the alternative of a judgment on your record.

After a lawsuit is resolved, the impact on your credit report is the next thing to address. A settled account and a dismissed case are two separate credit events. The dismissal affects the public records section of your report. The account status is what affects your score. If you also negotiated how the account will be reported, verify that within 45 days of the settlement by pulling your credit reports. If the status is still showing as unpaid or delinquent, that is a dispute you can file under the FCRA. Our detailed walkthrough of settling credit card debt after a judgment covers what happens to the judgment on your credit report, how to get the judgment noted as satisfied, and how that differs from a pre-judgment settlement.

Settled a debt but the account still looks wrong on your report? A free 3-bureau audit shows exactly what is reporting and whether any entry is disputable.

A free 3-bureau audit shows exactly what is reporting and whether any entry is disputable.

Settled a debt but the account still looks wrong on your report? →Settled a Debt? Make Sure It Shows Correctly on Your Report

A dismissed lawsuit and a settled account are two different credit events. Both need to be verified. A free 3-bureau audit shows exactly what Experian, TransUnion, and Equifax are reporting on every settled or dismissed account, including whether the date, balance, and status are accurate. Errors after settlement are common and disputable under the FCRA.

Get My Free Credit Audit →Secure · 2 minutes · No credit card required

Recommended Reads

Top Credit Cards for Bad Credit in Houston After settling a debt and getting the lawsuit dismissed, the next step is rebuilding. This covers the 10 best secured and unsecured cards available in Houston for scores below 580, with real data on approval rates, fees, and how fast each card moves your score.

How to Settle Midland Credit Without Resetting the Clock Midland Credit Management is one of the most active debt buyers in the country. This covers the specific tactics for negotiating a settlement with Midland, how to avoid accidentally restarting the statute of limitations, and what their standard settlement terms look like.

How to Deal with Capio Partners Capio Partners collects primarily on medical debt. Medical debt has different rules for credit reporting and different negotiating leverage than credit card debt. This covers what Capio can and cannot do, how to validate the debt, and when a settlement makes sense versus a dispute.

Disclaimer: This article is for general educational purposes only and does not constitute legal advice. Debt collection laws, court procedures, and settlement rules vary by state. If you have been served with a lawsuit, consult a licensed consumer law attorney in your state. Many consumer protection attorneys offer free consultations and take FDCPA cases on contingency. ASAP Credit Repair USA is registered under the Credit Repair Organizations Act and is not a law firm.

There's A Way To Stop a Lawsuit

A settlement can end a lawsuit, but only if it is completed and filed correctly. Payment alone does not close the case. The court only recognizes what is documented in the record.

The key step is the dismissal. Without it, the case remains active and can move forward.

Before paying, confirm the terms in writing and make sure the agreement includes how and when the lawsuit will be dismissed.

Ready to improve your credit?

Get Started →