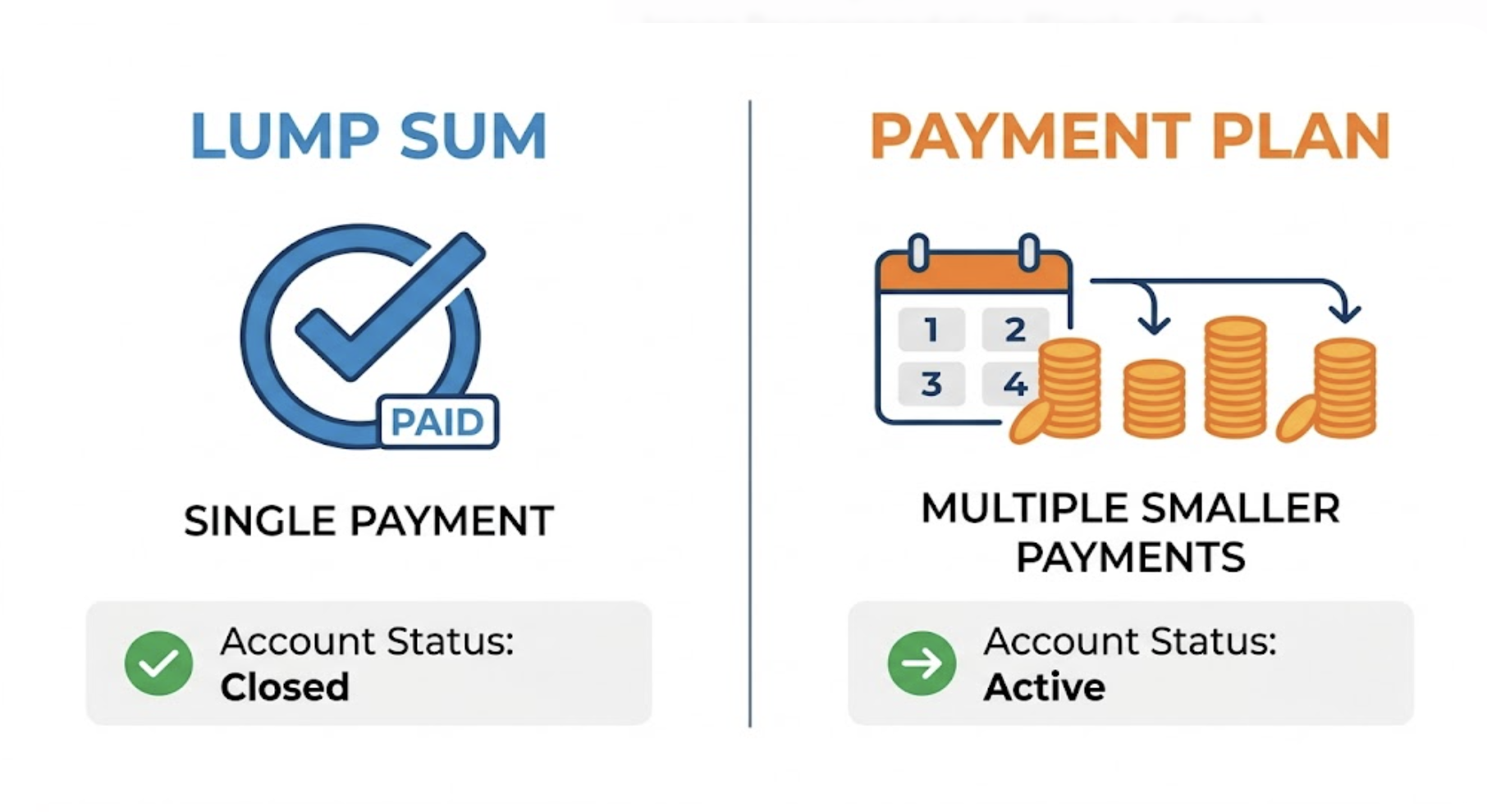

There are two common ways to pay a collection account: a lump sum settlement or a payment plan. Both reduce the balance, but they affect cost, timeline, and credit differently.

A lump sum usually closes the account faster and may reduce the total amount owed. A payment plan spreads the balance over time but keeps the account active until it is fully paid.

Under the Fair Credit Reporting Act, both settled and paid accounts can remain on your credit report for up to seven years. That means the structure of the payoff matters as much as the outcome.

In accounts we handle, the decision often comes down to control. Some clients prefer to resolve the debt at once and stop the reporting cycle. Others need time and choose structured payments to stay current. The results differ depending on how the account is reported during and after repayment.

This article explains when a lump sum makes sense, when a payment plan works better, and how each option affects your credit and total cost.

Lump Sum Settlement · Debt Settlement vs Payment Plan · How Much to Offer · Credit Score Impact · Settlement Negotiation Strategy · Creditor Negotiation

Updated April 2026 · Sources: American Association for Debt Resolution settlement data, CBS News debt negotiation reporting, NerdWallet debt settlement guide, CFPB debt settlement guidance, Federal Reserve Bank of New York consumer debt data 2025

- The average lump sum settlement resolves debt at 50.7% of the original balance, per the American Association for Debt Resolution. Most successful offers land between 40% and 60% of what is owed.

- Creditors strongly prefer lump sums because they eliminate the risk of future missed payments. That preference is your leverage to negotiate a lower amount.

- A settled account is reported as "settled" rather than "paid in full" on your credit report and stays there for 7 years. It does damage your score. But it damages it less than a defaulted unpaid account.

- Payment plans rarely reduce the principal. They stretch repayment, sometimes with reduced interest, but you typically pay the full amount owed over time.

- Any forgiven debt above $600 may be taxable as income. The creditor may send a 1099-C. This is often overlooked and creates a surprise tax bill.

- Never pay a lump sum before getting the settlement agreement in writing. The written agreement must confirm the amount, that it resolves the account, and what status will be reported to the credit bureaus.

Lump Sum Settlement vs Payment Plan: The Core Difference

| Factor | Lump Sum Settlement | Payment Plan | Winner |

|---|---|---|---|

| Amount paid | 40% to 60% of balance (avg 50.7%) | 100% of balance, usually | Lump Sum |

| Speed to resolution | Days to weeks once agreed | Months to years | Lump Sum |

| Creditor preference | Strongly preferred (certain payment) | Accepted but riskier for creditor | Lump Sum |

| Negotiating power | High - immediate payment = leverage | Low - no urgency for creditor | Lump Sum |

| Credit report notation | "Settled" - negative but shows resolution | "Paid in full" if full amount paid | Payment Plan |

| Cash required upfront | Yes - full agreed amount at once | No - spread over time | Payment Plan |

| Interest/fees during plan | Stops at settlement | May continue to accrue | Lump Sum |

| Tax implications | Forgiven amount may be taxable (1099-C) | None (paying full amount) | Payment Plan |

| Lawsuit risk | Ends when settled | Continues until last payment | Lump Sum |

The table makes the case clearly. Lump sum wins on amount saved, speed, leverage, interest costs, and lawsuit risk. Payment plan wins only on cash flow (no large upfront requirement) and credit report notation (paid in full instead of settled). If you have the money, or can raise it, lump sum is the smarter choice almost every time.

That experience is not unusual. Debt buyers who purchased the account at a steep discount from the original creditor have much more room to negotiate than the original creditor ever did. If a debt buyer paid 8 cents per dollar for your account, accepting 40 to 50 cents is still a huge profit for them. That economics math is your leverage.

How Much Should You Offer for a Lump Sum Settlement?

As CBS News reports in its debt settlement guide, most successful settlements result in paying 30% to 50% less than the original balance. The closer the debt is to the statute of limitations in your state, the more leverage you have, because a lawsuit filed after the SOL expires cannot be won by the creditor. That fact alone can move a creditor from refusing to settle to accepting 30 to 40 cents on the dollar.

Two things creditors and debt buyers respond to most consistently: a lump sum payment available immediately, and documented proof that you cannot pay more. If you can show both, you are in the strongest negotiating position possible. If the debt is already delinquent and the creditor sees a real risk you may file for bankruptcy, they often prefer 40 cents today over zero cents from a bankruptcy discharge later.

Does a Lump Sum Settlement Hurt Your Credit?

The chart shows the key insight most people miss. A lump sum settlement does drop your score temporarily. But it starts recovering almost immediately because the account balance goes to $0 and the delinquency clock resets. Payment plan recovery is slightly better long-term because "paid in full" reads better than "settled." But the gap is not enormous. Both paths dramatically outperform ignoring the debt, which produces a continuous decline as interest accrues, judgment risk increases, and the delinquency ages without resolution.

An important nuance: if your account is already deeply delinquent, the lump sum settlement may produce almost no additional credit score damage because the delinquency already scored against you. As one FICO expert put it, the floor effect means you cannot fall off the floor. If your score is already at 530 from 180 days of missed payments, settling that account for 50 cents on the dollar may move your score by just a few points in either direction. The bigger movement comes from what you do after the settlement.

One of the fastest ways to confirm whether a settlement was reported correctly to your credit bureaus is to request your free reports from AnnualCreditReport.com within 45 days of paying. If the creditor is reporting the wrong balance, wrong date, or wrong status, you have immediate grounds for a dispute. Our detailed guide on how to settle credit card debt after a judgment covers the specific steps for post-judgment settlements, including how to vacate a judgment in some states, what the written settlement must include, and how to get the court record updated after the settlement is paid.

When Is a Payment Plan Smarter than a Lump Sum?

The key question is: what is the account's current status? If the account is current with no late payments, a payment plan that achieves "paid in full" status is worth more to your credit than a settlement. If the account is already in collections, the damage is done and settlement becomes a cleaner, faster path.

When a collection agency contacts you about a debt, the first phone call is not the moment to negotiate. It is the moment to verify. Ask for written debt validation before you discuss any payment or settlement. Under the FDCPA you have 30 days from first written contact to request validation. The agency must stop collection activity until it provides proof the debt is yours and the amount is correct.

Our guide on how to respond when Gulf Coast Collection contacts you walks through the exact FDCPA process for responding to a collection agency, what debt validation must include, and how to protect yourself from paying a debt that has errors, is past the SOL, or may not even be legally yours to pay.

How to Negotiate a Lump Sum Settlement: Step by Step

- Verify the debt and check your state's statute of limitations before calling. Pull your credit report. Note the date of first delinquency. Look up your state's SOL for credit card or written contract debt. If the SOL has expired, you have significant leverage - the creditor cannot win a lawsuit. If the SOL is approaching, they have urgency to settle. If it is fresh, they have more time and leverage. Know this before any conversation.

- Determine your real maximum lump sum before you dial. Total the money you can realistically pull together: savings, tax refund, borrowed from family with a written repayment plan, or proceeds from selling something. This is your ceiling. Your opening offer is 25% to 35% of the balance. Never reveal your ceiling in the opening call. If they ask "how much can you pay," say "I need to hear what you're willing to accept first."

- Call the settlements or hardship department directly. Ask for the settlements department, not general customer service. State your situation briefly: job change, medical issue, reduced income. Explain you are trying to resolve the account but cannot pay the full balance. Make your opening offer. Be calm and specific with the dollar amount, not a percentage. "I can offer $1,800 as a lump sum to resolve this account today" sounds more credible than "I can pay about 30%."

- Negotiate over multiple calls, not one. Most creditors will not accept your first offer. When they counter, do not immediately accept or reject. Say you need to think about it and call back. This signals you are serious but not desperate. Being too quick to accept suggests you had more available. Space calls 24 to 48 hours apart. This is not unusual and does not harm the negotiation.

- Require a written settlement agreement before you pay anything. Once both sides agree on an amount, ask them to send the agreement in writing to your email or mail address. The written agreement must state: the exact settlement dollar amount, that it fully resolves the account, the account number, and that they agree to report the account as "settled" or "paid in full for less than full balance" to all three credit bureaus. No writing, no payment. Period.

Knowing what to say, when to say it, and how to handle counter-offers is the difference between a good settlement and a stalled one. Our resource of creditor negotiation scripts provides specific word-for-word language for the opening call, the hardship explanation, responding to a counter-offer, and asking for written confirmation - all the parts of the conversation where most DIY negotiators stumble.

The Tax Trap: What Happens to Forgiven Debt

As NerdWallet's debt settlement guide details, debt forgiven through a settlement is considered "canceled debt" by the IRS and is generally taxable unless you qualify for an insolvency exemption. The insolvency exemption applies if your total debts exceeded your total assets at the time of the settlement. In that case, you can exclude the forgiven amount from taxable income up to the amount of your insolvency. Consult a tax professional before settling a large balance, especially if you have multiple accounts.

Also note: as CNBC Select's reporting on debt relief and settlement options confirms, debt settlement companies charge 15% to 25% of the enrolled debt as fees. On a $10,000 debt, that is $1,500 to $2,500 in fees on top of the settlement payment. For most people, negotiating directly produces the same or better outcome without the fee. Use a settlement company only if you are dealing with many accounts simultaneously and lack the time or confidence to negotiate each one individually.

After You Settle: Make Sure It Reports Correctly

The most common post-settlement problem we see: the creditor reports the wrong balance, the wrong date, or fails to update the account status after payment. A free 3-bureau audit shows exactly what Experian, TransUnion, and Equifax are reporting on every settled account - including whether the date of first delinquency is correct and whether the account status matches your written settlement agreement. Inaccurate reporting after a settlement is disputable under the FCRA.

Get My Free Credit Audit → Secure · 2 minutes · No credit card requiredFrequently Asked Questions

Is a lump sum settlement better than a payment plan?

Almost always yes, if you can raise the money. A lump sum settlement typically reduces your balance by 40% to 60%. A payment plan rarely reduces your principal - it just spreads full repayment over time. Creditors prefer lump sum because they get certainty of payment, which gives you negotiating leverage to offer less. The trade-off is that a lump sum settlement is reported as "settled" rather than "paid in full," which is slightly worse for your credit than a completed payment plan, but much better than an ignored or defaulted account.

How much should I offer for a lump sum settlement?

Start at 25% to 35% of the total balance. Most successful settlements land between 40% and 60% of the original amount. The average per industry data is 50.7% of the balance. Always start below your ceiling so you have room to negotiate. Have the money ready before you call. If the creditor knows payment is immediate, they are more likely to accept a lower offer. Get every agreement in writing before sending any money.

Does a lump sum settlement hurt your credit?

Yes. The account is reported as "settled" rather than "paid in full," which signals that you did not repay the full amount. Credit scores can drop 60 to 125 points depending on your starting profile. The settled notation stays on your credit report for 7 years. However, if the account was already delinquent or in collections, much of the credit damage already occurred before the settlement. Settling stops the damage from worsening and starts the recovery clock. Both a settlement and a completed payment plan are significantly better for your long-term credit than ignoring the debt.

Can a creditor refuse a lump sum settlement?

Yes. Creditors have no legal obligation to accept any settlement offer. Original creditors (your bank or card issuer) are more likely to refuse settlement and require full repayment. Debt buyers who purchased your account at a steep discount are much more likely to settle, sometimes for 25% to 50% of the original balance, because any amount above their purchase cost is profit. Factors that improve your acceptance odds: the account is delinquent, you can document financial hardship, the debt is near the statute of limitations, and you can pay immediately in a single lump sum.

Is forgiven debt taxable?

Yes, in most cases. If a creditor forgives $600 or more through a settlement, they must report it to the IRS and send you a 1099-C form. The forgiven amount is treated as ordinary income in the tax year the settlement occurred. However, if your total debts exceeded your total assets at the time of the settlement (you were insolvent), you may be able to exclude the forgiven amount from taxable income. Consult a tax professional, especially before settling a large balance, to understand your specific tax exposure.

What should a lump sum settlement agreement include?

The written settlement agreement must include: the exact settlement dollar amount you are paying, the account number, a statement that this payment fully resolves the account and the creditor will not pursue any remaining balance, and the credit bureau reporting status (that the account will be reported as "settled" or "paid in full for less than full balance" rather than remaining open and delinquent). Never send payment before receiving this written confirmation. If the creditor will only communicate verbally, ask them to follow up with written confirmation and wait for it before paying.

- Lifestyle Inflation: Why You Still Feel Poor If debt settlement is where you are now, lifestyle inflation may be part of what got you here. This covers the patterns that cause spending to outpace income, the psychology behind it, and the specific habits that break the cycle so debt does not rebuild after you settle.

- California Credit Card Debt Collection: What You Need to Know California has some of the strongest consumer debt protections in the country, including a shorter statute of limitations on credit card debt and restrictions on wage garnishment. If you are settling or negotiating debt in California, understanding these rules changes your leverage and your strategy.

- What to Do When Alltran Financial Contacts You Alltran Financial is a healthcare and consumer debt collector. If they have contacted you, this covers your FDCPA rights, how to request debt validation, and how to evaluate whether a lump sum settlement or payment plan makes more sense based on what they are collecting and the account's current status.

Lump Sum vs Payment Plan

A lump sum and a payment plan both resolve the debt, but they do not produce the same outcome. A lump sum ends the account faster and can reduce what you pay. A payment plan gives more flexibility but keeps the account open longer.

The decision comes down to cash flow and timing. If the funds are available, a lump sum usually limits cost and stops the cycle. If not, a payment plan can work as long as it is consistent and does not fall behind.

What matters is not just paying the debt. It is how the account is reported while you do it.