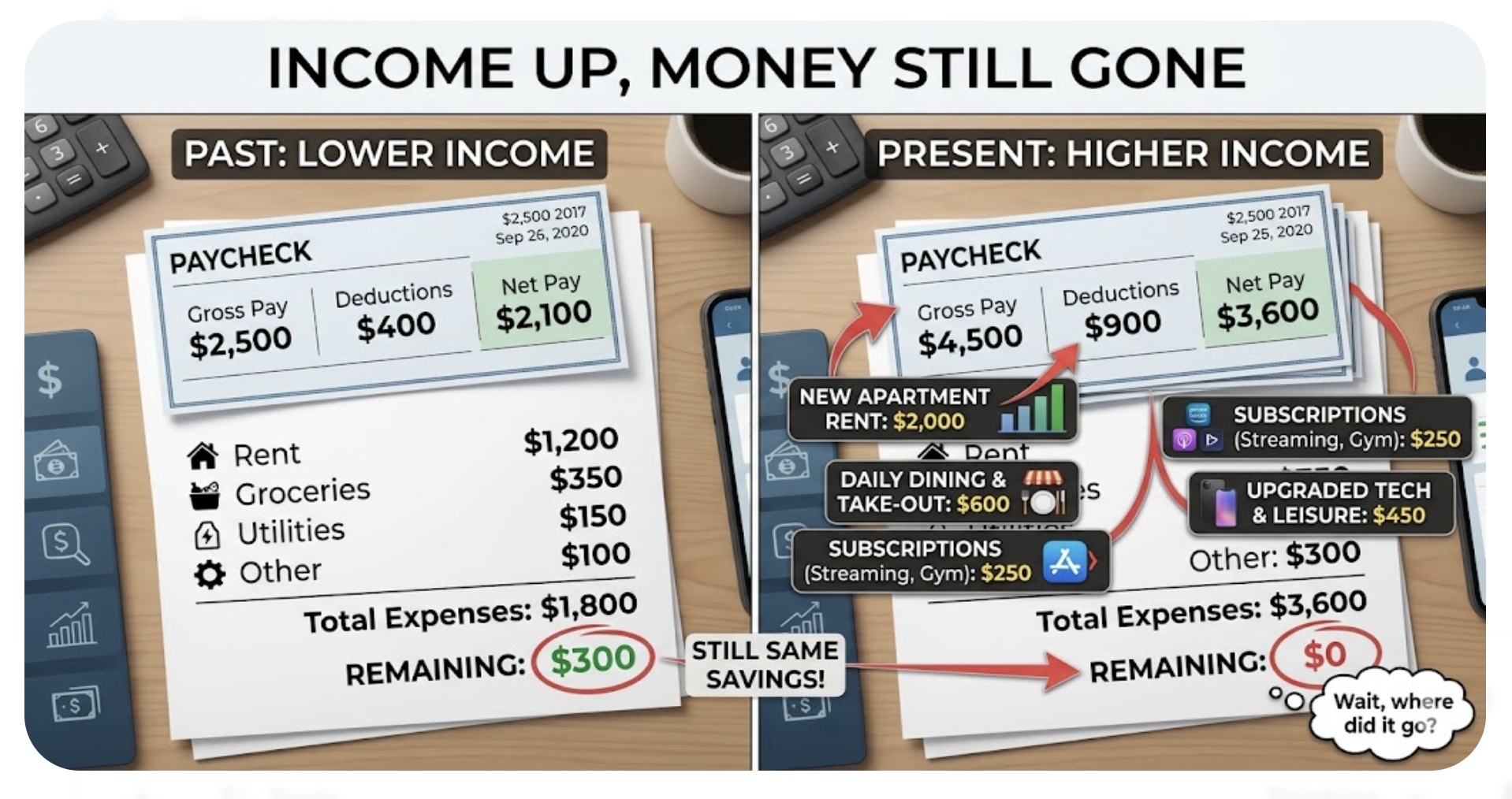

There is a pattern where income increases, but financial pressure stays the same. This is known as lifestyle inflation, or lifestyle creep. As earnings go up, spending tends to rise at the same pace, which limits savings and keeps cash flow tight.

Data from the Bureau of Labor Statistics shows that household spending increases alongside income across most categories, including housing, transportation, and discretionary expenses. The result is that higher income does not always lead to better financial stability.

In the credit files and budgets we review, this shows up clearly. People earning more than they did a few years ago still carry balances, miss savings targets, or rely on credit during gaps. The issue is not income alone. It is how spending adjusts to match it.

This article explains why lifestyle inflation happens, how it affects your finances, and what to change if you want income growth to translate into real progress.

People Also Ask

What is lifestyle inflation?

Lifestyle inflation is the increase in spending that happens as income rises, often preventing savings from growing.

Why do I feel broke even after getting a raise?

Spending often increases with income, which can offset the financial benefit of the raise.

Is lifestyle creep bad?

It becomes a problem when increased spending replaces saving or leads to higher debt.

How do you stop lifestyle inflation?

By controlling spending increases, setting fixed savings targets, and avoiding automatic upgrades in lifestyle.

Lifestyle Inflation · Lifestyle Creep · Why You Feel Poor Making More Money · Spending vs Income Gap · How to Stop Lifestyle Inflation

Updated April 2026 · Sources: Federal Reserve Survey of Household Economics 2024, USAFacts personal savings rate data 2025, CNBC high-earner financial stress survey, Investopedia lifestyle creep analysis, Bureau of Economic Analysis

- The Federal Reserve found that in 2024, 37% of adults increased monthly spending while only 32% increased monthly income. More people spent more than they earned, not less.

- The U.S. personal savings rate was just 4.4% in 2024. In the 1970s it averaged 11.7%. Americans earn more and save less proportionally than any prior generation.

- 36% of Americans earning over $100,000 live paycheck to paycheck. High income does not protect you from lifestyle inflation. It just raises the ceiling of what you can waste.

- The average American household now spends $273 per month on subscriptions alone - up 435% from 2018. That is $3,276 per year on recurring charges most people could not name off the top of their head.

- Lifestyle inflation is a pattern, not a character flaw. The human brain is wired to normalize comfort quickly (called hedonic adaptation). Understanding that makes it easier to fight.

What Is the Meaning of Lifestyle Inflation?

The term "lifestyle creep" captures how this happens. It is not a sudden decision to blow your raise. It is gradual. A slightly better apartment here. A car payment you now can "handle" there. A few streaming services. More dining out because you are busy and you "deserve" it. Each choice feels justified. Together they erase the raise entirely.

As Investopedia's lifestyle creep explainer documents, the core problem is that luxuries become baseline expectations. What felt like a treat becomes your new normal. What once felt like a splurge becomes something you cannot imagine giving up. That shift in expectations is what makes lifestyle inflation so hard to notice from the inside.

The Federal Reserve's 2024 Survey of Household Economics confirmed the spending-outpacing-income pattern for the third consecutive year in a row. More adults increased their monthly spending than increased their monthly income. That is not just inflation in the cost of necessities. That is lifestyle inflation: voluntary spending growing faster than the paychecks that fund it.

That Reddit post gets to the heart of it. A $14,000 raise absorbed almost entirely by upgraded spending. Not reckless spending. No single ridiculous purchase. Just a nicer apartment, a better car, and the spending pattern that follows when you feel like you finally have a little room. That is exactly how lifestyle inflation works.

Lifestyle Inflation Statistics That Show the Real Scale of the Problem

Those numbers do not lie. The average American worker takes home more in real dollars today than workers of the 1970s. Yet they save a smaller fraction of that income. The extra dollars are not going to taxes. They are going into higher monthly expenses - bigger homes, newer cars, premium everything, and subscription services that did not exist a generation ago.

As reported by CNBC's investigation into why high earners feel broke, nearly two-thirds of Americans earning over $300,000 per year struggle with credit card debt. The survey found that the feeling of financial stress does not disappear as income rises - it follows you upward because spending adjusts to each new level. As psychologist Sabrina Romanoff put it in the same report: earning more does not make you feel rich. Spending less does.

The chart makes the pattern visual. Real wages climbed through every decade. Savings rates fell in almost a mirror image. The more Americans earned, the less they kept. That is lifestyle inflation at a macro scale. What happens in the national data is happening in individual households right now.

Debt is the outcome when lifestyle inflation runs long enough. The spending patterns that lifestyle creep builds often outlast the income that funded them. When a job loss, a health crisis, or an economic shift happens, the inflated expenses do not shrink automatically. That is when collections accounts start appearing, credit scores fall, and people find themselves in genuine financial crisis despite having earned good salaries. Our guide on why so many people are struggling with debt covers the structural patterns we see in client cases, including how lifestyle-driven spending decisions translate into credit report damage years later.

What Are Some Examples of Lifestyle Inflation?

Add those six examples together: $5,400 + $6,600 + $7,680 + $3,276 + $4,000 + $5,544 = roughly $32,500 per year in lifestyle inflation on a moderate estimate. For someone who got a $20,000 raise, that is not just the raise gone. That is the raise plus $12,500 more in annual spending than before the promotion.

What Causes Lifestyle Inflation? (The Psychology)

Hedonic Adaptation

Your brain is remarkable at normalizing new comfort levels. The new apartment feels amazing for three weeks. Then it is just where you live. The car feels exciting for a month. Then it is just your commute. Research on hedonic adaptation (sometimes called the hedonic treadmill) shows that the emotional return from lifestyle upgrades fades faster than the financial obligation lasts. You stop feeling the pleasure of the upgrade. The monthly payment keeps coming.

Social Comparison

If your coworkers, friends, or Instagram feed normalizes a spending level above yours, you feel pressure to match it. Most people cannot actually see anyone else's net worth, savings rate, or credit card balance. They see what people spend. What people show. Social comparison drives spending toward visible lifestyle markers - the car, the home, the vacation photos - rather than toward the invisible metrics that actually build wealth.

Income Confidence

When money feels less tight, most people stop tracking it closely. That loss of vigilance is itself a lifestyle inflation driver. Budget tracking catches drift early. Stopping it lets the drift accumulate until the next credit card statement shock.

When someone has faced debt collection from a medical provider, landlord, or retailer after a period of inflated spending, the credit damage can persist for years. Agencies like Alltran Financial sometimes surface on credit reports related to healthcare and consumer debt. Our breakdown of what to do when Alltran Financial contacts you explains your FDCPA rights, how to request debt validation, and what to check on your credit report when a collection agency appears - all relevant steps if lifestyle-driven spending has led to debt that is now in collections.

What Is the $1,000 a Month Rule?

| Monthly Lifestyle Addition | Annual Extra Spend | Savings Needed to Sustain It in Retirement | Impact |

|---|---|---|---|

| $500/mo (nicer apartment) | $6,000/yr | $120,000 more required | Moderate |

| $1,000/mo (car + dining upgrade) | $12,000/yr | $240,000 more required | High |

| $2,000/mo (housing + car + subscriptions) | $24,000/yr | $480,000 more required | Severe |

| $500/mo saved instead of spent | $6,000/yr saved | Reduces retirement savings gap by $120,000 | Positive |

The $1,000 a month rule puts lifestyle inflation in concrete terms. Adding $1,000 to your monthly expenses is not just $12,000 per year. It is a $240,000 higher retirement savings target. Most people making lifestyle upgrades do not think in those terms. They think about whether next month's paycheck can cover the new payment. The $1,000 a month rule shows why "I can afford it" is the wrong question. The right question is: "Can I afford the retirement version of this?"

How to Get Out of Lifestyle Inflation: 5 Steps That Actually Work

- Run a 12-month spending audit and find every category that grew. Pull your last 12 months of bank and card statements. Group spending into categories. Compare this year's monthly averages to the year before. Write down every category where spending increased. That list is your lifestyle inflation map. Most people find $300 to $800 per month in growth they cannot immediately explain.

- Automate savings before the money hits your checking account. Set up an automatic transfer the same day as your paycheck. Move your target savings percentage directly to a separate account or into your 401(k). When the savings are automated and invisible, you cannot spend them by default. Start at 10% if 20% is not currently possible. Increase by 1 percentage point every three months.

- Apply the 50/30/20 rule to every raise, not just your current income. When income goes up: 50% to needs, 30% to wants, 20% to savings or debt paydown. The new income should increase the savings number before it increases the wants number. Most people do the reverse - they let the raise flow straight into lifestyle and save whatever is left, which is usually nothing.

- Audit every subscription and cancel anything unused in 30 days. List every recurring monthly charge in your accounts. Note the last time you actively used each one. Cancel anything you have not used in the last 30 days. Do this quarterly. Subscriptions re-accumulate fast. The average household spending $273 per month on subscriptions could free $100 to $150 per month just by cutting unused ones.

- Implement a 72-hour rule on non-essential purchases above $100. Write the item on a list. Wait 72 hours. Revisit. Buy it or decide not to. Most impulse spending fails the 72-hour test. The desire passes. This single habit prevents a large portion of the small lifestyle inflation decisions that add up over months and years.

If a financial emergency is what first revealed that lifestyle inflation had depleted your savings cushion, it helps to know what options exist that do not make the situation worse. Our guide on how to access emergency cash without damaging your credit covers the safest borrowing options ranked by cost and credit impact, including paycheck advance apps, credit union PAL loans, and employer advances - all of which carry far less financial risk than the high-cost emergency debt that typically follows when savings have been consumed by lifestyle spending.

Lifestyle Inflation and Your Credit Score: The Connection Most People Miss

This connection is something we see in our credit repair practice constantly. A client comes in with a 550 credit score and several collection accounts. Their income two years ago was $80,000. They had a job change that cut income to $62,000. But the apartment, the car, the subscriptions, and the spending habits were all built for $80,000. The $18,000 income gap could not be absorbed. Cards were maxed trying to bridge it. Then accounts went to collections. Two years later they are trying to repair credit that lifestyle decisions destroyed.

As USAFacts has reported using Bureau of Economic Analysis data, Americans saved only 4.6% of disposable income in 2024 - lower than at any point in the 1960s, 1970s, 1980s, or 1990s despite decades of higher real wages. That thin savings rate means most households have very little buffer when income drops. Lifestyle inflation is the direct cause of that thin buffer.

Credit Damage from Past Overspending Can Be Fixed

If lifestyle inflation led to missed payments, maxed credit cards, or collection accounts, your credit report may have errors on top of the accurate damage. A free 3-bureau audit identifies every negative entry across Experian, TransUnion, and Equifax, and shows which items are disputable, which can be negotiated for pay-for-delete, and what your score could look like after repair work begins.

Get My Free Credit Audit → Secure · 2 minutes · No credit card requiredFrequently Asked Questions

What is the meaning of lifestyle inflation?

Lifestyle inflation, also called lifestyle creep, means your spending grows every time your income grows. A raise brings a nicer apartment, a better car, more subscriptions, and more dining out. The monthly expenses climb to absorb the new income. The savings account stays flat or shrinks. You earn more but feel just as financially constrained as before because the spending adjusted to match the income instead of the savings adjusting to capture it.

What are some examples of lifestyle inflation?

Common lifestyle inflation examples include: upgrading to a more expensive apartment or home after a raise; financing a new or better car; increasing how often you eat out or order delivery; accumulating 8 to 15 streaming or subscription services; buying premium brands instead of store brands; booking business class or premium hotels instead of budget options; and ordering expensive coffee drinks daily instead of brewing at home. Each example feels small or justified in isolation. Together they can absorb a $15,000 to $20,000 raise entirely.

How do you get out of lifestyle inflation?

To get out of lifestyle inflation: run a 12-month spending audit and identify every category where spending grew; automate savings before you can spend the money; apply the 50/30/20 rule (50% needs, 30% wants, 20% savings) and direct raises to savings first; audit and cancel unused subscriptions quarterly; and use a 72-hour waiting rule before any non-essential purchase over $100. These five habits address the pattern at every level: tracking, automation, income allocation, recurring costs, and impulse control.

What is the $1,000 a month rule?

The $1,000 a month rule is a retirement planning guideline that says every $1,000 in monthly income you want in retirement requires approximately $240,000 saved. In the context of lifestyle inflation, every $1,000 per month you add to your spending now is also $240,000 more you need to save before retirement to sustain that spending level. Adding $2,000 per month in lifestyle expenses over the course of a few years could mean you need $480,000 more in retirement savings than if you had stayed at your previous spending level.

What are the main causes of lifestyle inflation?

The three main psychological causes are hedonic adaptation (your brain normalizes new comfort levels quickly, making today's luxury tomorrow's necessity), social comparison (you feel pressure to match the visible spending of people around you or on social media), and income confidence (you stop budgeting because you feel like higher earnings make discipline less necessary). Subscription creep and the "I deserve it" spending mentality are also major drivers, along with life transitions like marriages, promotions, and relocations that create natural spending escalation points.

-

Why Are So Many People Struggling with Debt? The structural reasons why debt accumulates even when income is decent - including how lifestyle-driven spending decisions translate into credit damage, why collections appear years after the original financial stress, and what patterns appear most consistently in credit repair cases.

-

Emergency Cash Options That Won't Destroy Your Credit If lifestyle inflation has left you without a savings cushion and a financial emergency has hit, this covers the safest emergency borrowing options ranked by cost and credit impact - from paycheck advance apps to credit union PAL loans to personal loan prequalification.

-

What to Do When Alltran Financial Contacts You If lifestyle-driven overspending has led to collection accounts, this explains your FDCPA rights when a collection agency contacts you, how to request debt validation, how to check whether the account is being reported accurately, and what your options are for resolving the debt without making your credit situation worse.

Closing

Lifestyle inflation explains why higher income does not always improve your situation. If spending rises with every increase, nothing changes in your financial position.

The difference shows in how income is handled after it comes in. If part of the increase is kept, savings grow, and debt becomes easier to manage. If all of it is spent, the pressure stays the same.

Most people do not feel poor because they earn too little. They feel it because their expenses are adjusted to match their income.