Getting approved for a car loan isn't just about walking into a dealership and picking out a car.

Lenders look at specific requirements before they hand over thousands of dollars for your vehicle purchase.

Understanding these requirements before you start shopping can save you time, discouragement, and help you secure the best possible deal on your dream car.

Essential Car Loan Credit Score Requirements

What Credit Score Do You Actually Need?

A credit score of 661 or above is considered a prime VantageScore® credit score. This will generally improve your chances of getting approved with favorable terms. For the FICO® Score, a good credit score is 670 or higher. However, the reality is more nuanced than a single number.

Most borrowers need a FICO score of at least 600 to get a competitive rate on an auto loan. Think of this as the threshold where you stop paying penalty rates and start getting deals that make financial sense. Below 600, you're in subprime territory where interest rates climb steeply.

When purchasing a car, the minimum credit score requirement may be around 500. Those with average credit scores lower than 500 can still get financing, but they may have higher rates. This means even people with poor credit can get car loans, but the cost becomes prohibitive quickly.

The Real Impact of Your Credit Score on Interest Rates

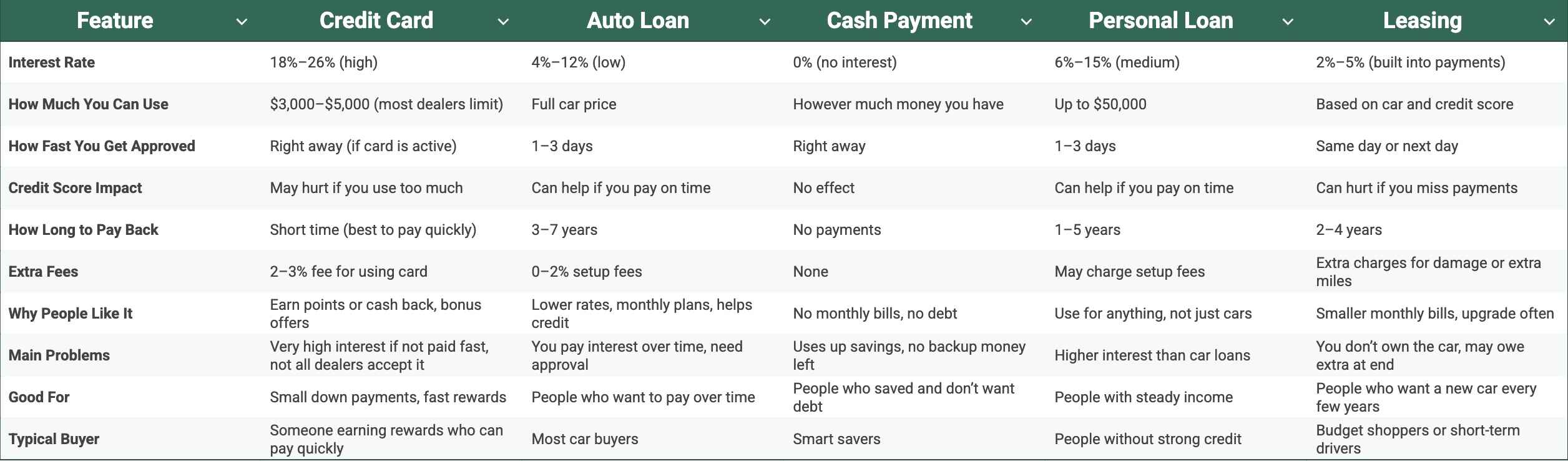

Here's what your credit score actually costs you. A borrower with a 750 credit score might get a 4% interest rate on a $25,000 car loan. That same loan with a 550 credit score could carry an 18% interest rate. Over a 5-year loan term, the difference is about $8,500 in additional interest payments.

Credit score ranges and typical car loan rates break down like this:

- Excellent credit (750+): 3-5% interest rates

- Good credit (670-749): 5-8% interest rates

- Fair credit (580-669): 8-15% interest rates

- Poor credit (300-579): 15-25% or higher interest rates

Understanding these ranges helps you know whether to shop for a car now or spend a few months improving your credit score first.

When Your Credit Score Isn't Everything

A new lender may consider your debt-to-income ratio. The credit union you bank with may consider how long you've been a member. This is important because it means you have options even if your credit score isn't perfect.

Credit unions often offer better rates to members, especially long-term members with established relationships. Some online lenders focus more on income stability than credit scores. Understanding these alternatives can help you find better deals than traditional bank financing.

Income Requirements That Actually Matter

Minimum Income Thresholds

The gross income requirement for a bad credit car loan is typically a minimum of $1,500 to $2,500 a month. This income needs to be taxable – meaning tips or side hustles that aren't reported won't count toward your qualifying income.

Most lenders want to see consistent income for at least two years. If you're self-employed, you'll typically need two years of tax returns to prove income stability. Recent job changes can complicate approval, even if your new job pays more than your old one.

We'll ask to see bank statements, as well as proof of other income sources like social security, alimony, child support, pay stubs, and legal settlements. This means lenders count various income sources, not just employment income.

Understanding Debt-to-Income Ratios

Your debt-to-income ratio (DTI) might be more important than your credit score for car loan approval. Ideally, lenders want to see a DTI ratio at or below 35%, as this means there is plenty of room in your budget to make your new monthly auto payment.

Typically, lenders like to see a DTI ratio of no more than 45%-50% after factoring in your estimated car loan payment. This is your maximum threshold. Above 50% DTI, most lenders will deny your application regardless of your credit score.

Here's how to calculate your DTI ratio: Add up all your monthly debt payments (credit cards, student loans, mortgage, other loans) and divide by your gross monthly income. For example, if you have $2,000 in monthly debt payments and earn $5,000 per month, your DTI is 40%.

When it comes to your debt-to-income ratio, lenders place a cap of 45% to 50% on bad credit borrowers. This means that if more than half your income is already being used for bills, you likely won't get approved.

Required Documentation Checklist

Identity and Residency Proof

Every lender needs to verify who you are and where you live. You'll need a valid driver's license or state ID, and proof of residence such as a utility bill, lease agreement, or mortgage statement from the past 30 days. Some lenders accept bank statements as proof of residence if they show your current address.

Income Verification Documents

The documents you need for an auto loan verify that you can afford to pay back what you borrow. For employed borrowers, this typically means your most recent pay stub and your previous year's W-2 or tax return.

Self-employed borrowers face more complex requirements. You'll need two years of tax returns, profit and loss statements, and possibly bank statements showing business income deposits. Some lenders want to see quarterly tax payments as proof of ongoing business income.

If you receive income from multiple sources, gather documentation for each. Social Security recipients need their award letter, retirees need pension statements, and people receiving alimony need court documents or divorce decrees showing the payment amounts.

Banking and Asset Information

Lenders want to see your banking history, typically requiring three months of bank statements. They're looking for consistent income deposits, reasonable spending patterns, and sufficient funds for a down payment.

Avoid large unexplained deposits in your bank account before applying for a car loan. Lenders investigate these deposits to ensure they're not borrowed funds, which could indicate you're taking on debt they don't know about.

Insurance Requirements

You cannot drive your new car off the lot without insurance. Most states require liability insurance at minimum, but lenders require comprehensive and collision coverage to protect their investment. Get insurance quotes before shopping for your car so you know the total monthly cost of ownership.

When You're Ready to Buy vs. When You Should Wait

Green Light Indicators

You should move forward with your car purchase when your financial foundation is solid. This means having a credit score above 600, stable employment for at least two years, and a debt-to-income ratio below 40%.

You're also ready when you have a real down payment, not just the minimum required. A down payment of 10-20% shows lenders you're serious about the purchase and reduces their risk. This often translates to better interest rates and terms.

Having an emergency fund separate from your down payment indicates you're financially prepared for car ownership. Cars require maintenance, repairs, and insurance costs beyond the monthly payment.

Red Flag Warning Signs

Wait to buy a car if you're struggling with existing debt payments. Adding a car payment when you're already stretched thin often leads to financial problems that damage your credit further.

Recent job changes, even positive ones, complicate loan approval. If you started a new job within the past six months, consider waiting until you have more employment history with your current employer.

Don't buy a car if you're planning other major purchases like a house within the next year. Car loans affect your debt-to-income ratio, which impacts mortgage approval. The sequence of major purchases matters for your overall financial health.

If your only option is a car loan with an interest rate above 15%, seriously consider waiting. These high-rate loans often trap borrowers in negative equity situations where they owe more than the car is worth.

The Right Time to Strike

The best time to buy a car is when you can afford more than you actually need. If you can qualify for a $30,000 car loan but only need a $20,000 car, you're in a strong negotiating position and won't be overextended financially.

End-of-model-year sales, typically in September through November, offer the best deals on new cars. Dealers need to clear inventory for new models, leading to significant discounts and manufacturer incentives.

For used cars, avoid buying during tax refund season (February through April) when demand and prices peak. Instead, shop during slower periods like late fall and winter when inventory sits longer on lots.

Improving Your Approval Odds

The Down Payment Strategy

While some lenders offer zero-down financing, putting money down improves your approval odds and loan terms significantly. A larger down payment reduces the lender's risk and often qualifies you for better interest rates.

For new cars, aim for at least 10% down. For used cars, 15-20% down is ideal because used cars depreciate faster than new ones. If you're buying a car that's more than five years old, consider putting down 25% or more to avoid being underwater on the loan immediately.

Shopping for Pre-Approval

Getting pre-approved before visiting dealerships gives you negotiating power and prevents surprises. Apply with your bank, credit union, and at least one online lender to compare rates and terms.

Pre-approval applications typically result in hard credit inquiries, but multiple auto loan inquiries within a 14-45 day window count as a single inquiry for credit scoring purposes. This allows you to shop around without damaging your credit score.

The Co-Signer Option

If your credit or income doesn't qualify you for the rates you want, a co-signer with good credit can help. The co-signer becomes equally responsible for the loan, so choose someone who understands this responsibility.

Co-signers help most when you have limited credit history rather than bad credit history. If you have recent late payments or collections, a co-signer might not be enough to secure good rates.

Types of Lenders and What They Require

Traditional Banks

Banks typically offer the strictest requirements but also the best rates for qualified borrowers. They prefer customers with established banking relationships, stable employment, and credit scores above 650.

Banks often require larger down payments than other lenders, typically 10-20% for new cars and 15-25% for used cars. They also have stricter debt-to-income requirements, usually capping DTI at 40-45%.

Credit Unions

Credit unions often provide the best combination of rates and flexible requirements. They consider the whole relationship, not just credit scores and income. Long-term members with good banking history often get approved when banks would decline them.

Credit union car loan rates are typically 1-2% lower than bank rates. Many credit unions also offer longer repayment terms, which can lower monthly payments but increase total interest paid.

Online Lenders

Online lenders often have more flexible requirements than traditional banks. They may approve borrowers with lower credit scores or higher debt-to-income ratios. However, rates are typically higher than banks or credit unions.

The application process is usually faster with online lenders, often providing decisions within hours rather than days. This speed comes at a cost, as you'll typically pay higher rates than traditional lenders.

Dealer Financing

Dealerships work with multiple lenders and can often find financing for borrowers who can't get approved elsewhere. However, dealer financing typically comes with higher rates than direct lending.

Dealers make money on the "rate markup" – the difference between the rate the actual lender charges and the rate they offer you. This markup can add thousands to your loan cost over time.

Special Situations and Requirements

First-Time Car Buyers

First-time buyers face unique challenges because they lack automotive credit history. Even borrowers with good credit scores from credit cards might struggle with auto loans because lenders view different types of credit differently.

Consider starting with a less expensive used car to establish automotive credit history. Successfully paying off your first car loan makes it much easier to qualify for better terms on your next vehicle.

Self-Employed Borrowers

Self-employed borrowers need more documentation and often face higher interest rates because lenders view variable income as riskier. You'll typically need two years of tax returns, profit and loss statements, and bank statements showing business deposits.

Consider working with lenders who specialize in self-employed borrowers. These lenders understand business income patterns and may offer more flexible underwriting than traditional banks.

Military Personnel

Active duty military personnel often qualify for special financing programs with lower rates and reduced requirements. The Military Lending Act also provides protections against predatory lending practices.

Many manufacturers offer military discounts and special financing terms. These programs often provide better deals than standard consumer financing, even for borrowers with excellent credit.

Making Your Final Decision

Understanding car loan requirements helps you approach the buying process strategically rather than reactively. When you know what lenders want to see, you can prepare your finances to meet those requirements and secure the best possible terms.

The key is matching your financial situation to the right type of lender. If you have excellent credit and stable income, banks and credit unions offer the best rates. If your credit needs work, online lenders or dealer financing might be your best options.

Remember that the goal isn't just getting approved, it's getting approved for terms that fit your budget comfortably. A car loan should enhance your life, not create financial stress that affects other areas of your finances.

Take time to improve your credit score, save for a meaningful down payment, and understand your budget before shopping for cars. This preparation often saves you thousands of dollars and makes the entire car buying process much more enjoyable.