Missing payments on your Comenity Bank credit card feels scary. You're not alone. Over 70 million Americans have dealt with debt collectors, and credit card defaults hit a 14-year high in 2024.

If you've missed payments on your Victoria's Secret card, Ulta Beauty account, or any other Comenity card, you need to understand what happens next.

This guide breaks down exactly what Comenity Bank does when you default. How it damages your credit, and what steps you can take right now to bring your credit score back up.

What Is Comenity Bank?

Comenity Bank issues credit cards for over 100 major retailers. You might not recognize the Comenity name, but you probably recognize these stores:

- Victoria's Secret

- Ulta Beauty

- Belk

- Express

- American Eagle Outfitters

- Zales

- Lane Bryant

- Ann Taylor

Comenity used to go by World Financial Network National Bank (WFNNB) until they changed its name in 2012. They now manage credit programs for more than 31 million customers.

The Problem: Comenity cards typically come with high interest rates. Many cardholders carry high balances and struggle to make payments when financial problems hit.

When Does Default Actually Happen?

Default doesn't happen overnight. You move through specific stages before Comenity closes your account and sends you to collections.

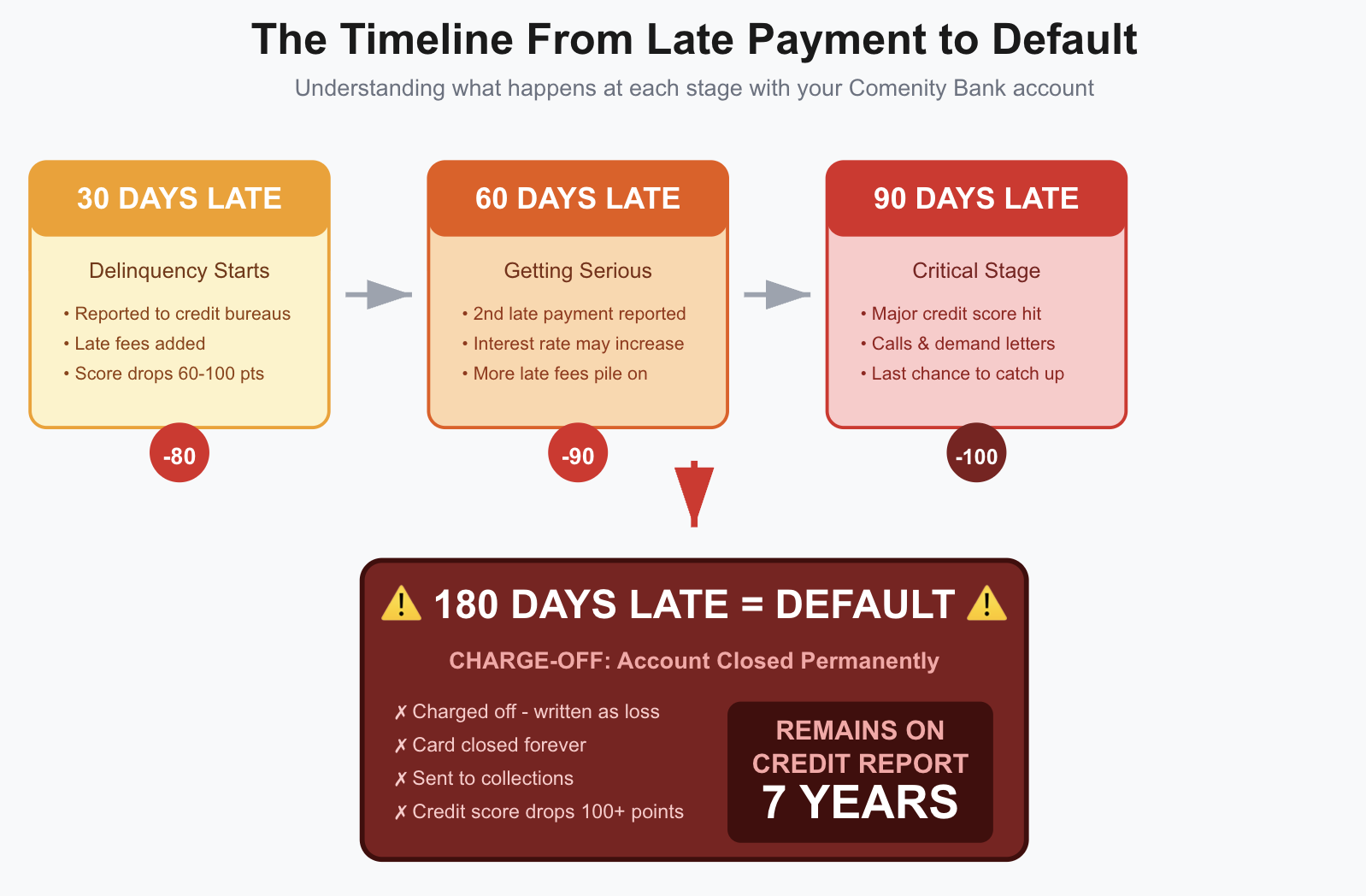

The Timeline From Late to Default

30 Days Late (Delinquency Starts)

- Comenity reports your missed payment to the credit bureaus

- Late fees get added to your balance

- Your credit score drops 60-100 points

60 Days Late

- Another late payment hits your credit report

- Comenity may raise your interest rate significantly

- More late fees pile on

90 Days Late

- Your credit score takes a major hit

- Comenity starts calling and sending demand letters

- You still have time to catch up

180 Days Late (Default)

- Comenity charges off your account

- They close your card permanently

- Your debt goes to collections

- Your credit score can drop 100+ points

This charge-off stays on your credit report for seven years from the date of your first missed payment.

What Comenity Bank Does After You Default

Once you hit 180 days without payment, Comenity takes aggressive action to recover its money.

They Close Your Account Permanently

Comenity charges off your account. This means they write it off as a loss on their books. But this doesn't erase your debt; you still owe the money.

Your card has been closed permanently. You can't use it again, even if you later pay off the balance.

They Report The Charge-Off To Credit Bureaus

Comenity reports the charge-off to Equifax, Experian, and TransUnion. This appears as a "charge-off" on your credit report, one of the worst marks you can have.

The charge-off entry shows:

- The original creditor (the retail store)

- Comenity Bank as the account holder

- The amount you owed when they charged it off

- The status as "charged off"

This entry damages your credit for seven full years.

They Send Your Debt To Collections

Comenity follows one of two paths with your charged-off debt:

Path 1: They assign your debt to a collection agency

- Comenity still owns your debt

- They hire collectors to pursue payment on their behalf

- Collectors earn a percentage of what they collect

- Your credit report still shows Comenity as the creditor

Path 2: They sell your debt to a debt buyer

- Comenity sells your account for pennies on the dollar

- The debt buyer now owns your debt completely

- Comenity updates your credit report to show a zero balance

- The debt buyer may appear as a new collection account on your credit report

Collection Agencies Start Calling

Once collectors get your account, they will:

- Call you multiple times per week

- Send demand letters to your home

- Contact you about settling the debt

- Threaten legal action if you don't pay

According to the Consumer Financial Protection Bureau, 25% or 1 out of 4 people dealing with debt collectors felt uncomfortable, harassed, or threatened during collection calls.

They May Sue You

If you continue not paying, Comenity or the collection agency may file a lawsuit against you. This is more common for larger balances, typically over $1,000.

If they sue you and win, they can:

- Garnish your wages (take money from your paycheck)

- Levy your bank account (freeze and withdraw funds)

- Place liens on property you own

- Add court costs and attorney fees to what you owe

Critical: If you get sued, you must respond. Ignoring a lawsuit from TSI or Comenity, leads to a default judgment, which gives collectors powerful enforcement rights.

How Default Destroys Your Credit Score

Defaulting on a Comenity card causes severe, long-lasting credit damage.

The Credit Score Drop

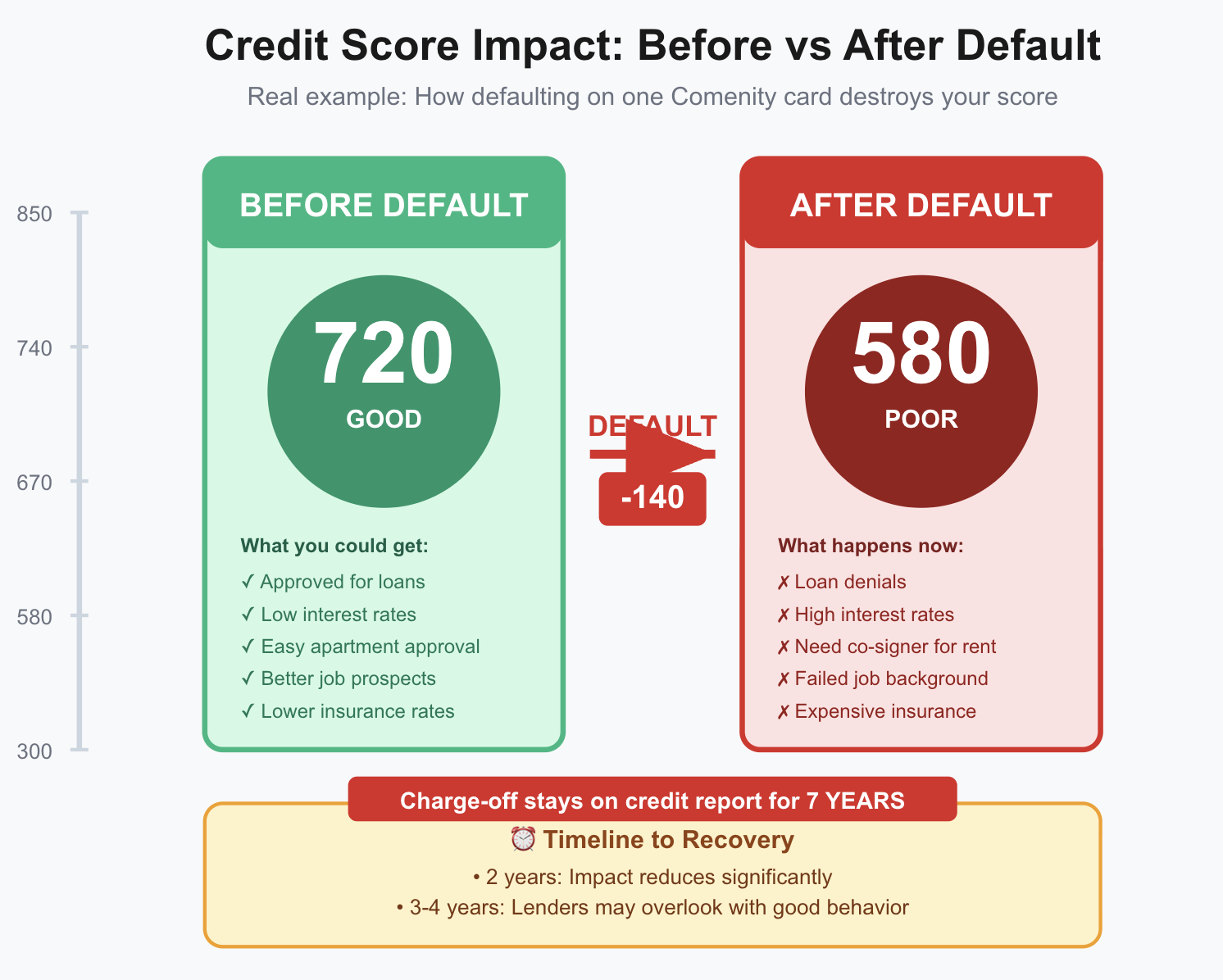

Research shows that missing even one payment drops your credit score by 60-100 points. When you reach default after six months of non-payment, your score can plummet by 100 points or more.

Example: If you start with a 720 credit score and default on your Comenity card, you could end up with a score in the low 600s or worse.

The Seven-Year Impact

The charge-off stays on your credit report for seven years from the date of your first missed payment. During this time:

- Loan denials: Lenders see the charge-off and deny your applications

- Higher interest rates: If you do get approved, you will pay much higher rates

- Harder to rent: Landlords check credit and may reject your application

- Job difficulties: Some employers check credit during hiring

- Higher insurance rates: Auto and home insurance companies charge more

Even after you pay the debt, the charge-off remains on your credit report for the full seven years.

It will simply update to show "paid charge-off" instead of "unpaid charge-off."

Other Credit Cards Get Affected

Defaulting on your Comenity card can trigger consequences on your other cards:

- Other issuers may lower your credit limits

- Your other cards may increase their interest rates

- You become a higher risk to all creditors

- Lower credit limits increase your credit utilization ratio, further damaging your score

Real-World Example

Sarah had a $3,000 balance on her Ulta Beauty card issued by Comenity. After losing her job, she couldn't make payments. Within six months, Comenity charged off her account.

The Damage:

- Her credit score dropped from 680 to 580

- She got denied for a car loan she desperately needed

- Her other credit card company lowered her limit from $5,000 to $2,000

- When she applied to rent an apartment, the landlord required a co-signer

Sarah's default on one retail card created a domino effect that affected her entire financial life.

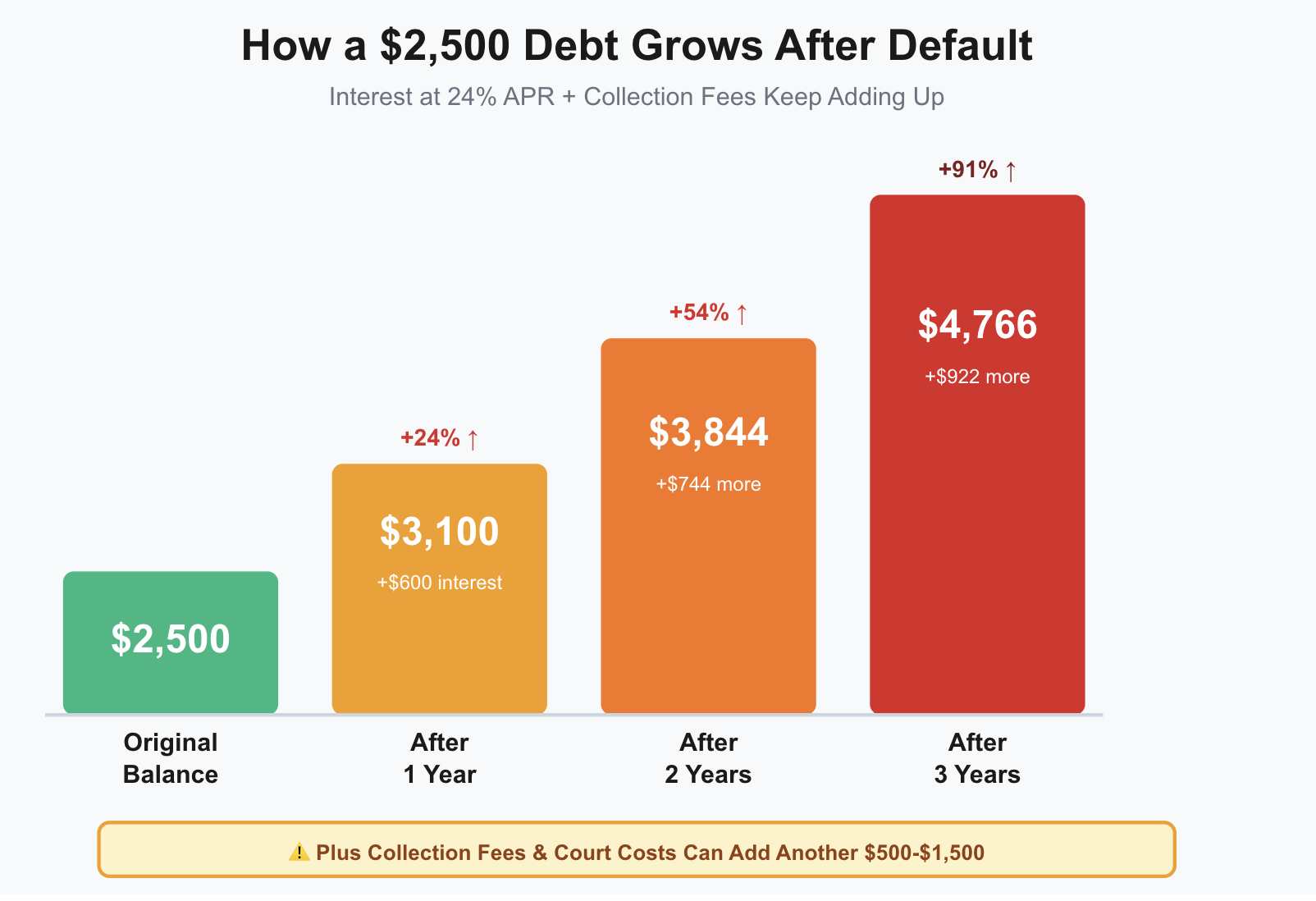

The Growing Debt Problem

Your debt doesn't stop growing after default. It actually gets worse.

Interest Keeps Piling Up

Even after a charge-off, interest continues to accrue on most accounts. Your balance grows larger every month you don't pay.

Comenity may also increase your interest rate after you miss payments. Some retail cards have penalty rates as high as 29.99% APR.

Collection Fees Get Added

Collection agencies often add their own fees to your debt:

- Collection costs

- Attorney fees if they sue

- Court costs if they win a judgment

A $2,000 debt can balloon to $3,000 or more by the time collectors finish adding fees.

The Math Gets Ugly Fast

Let's say you defaulted on $2,500 at 24% APR:

- After 1 year: $3,100

- After 2 years: $3,844

- After 3 years: $4,766

This doesn't include collection fees or court costs if they sue you.

What You Can Do Right Now

If you've defaulted or you're heading toward default, you have options. Taking action now prevents further damage.

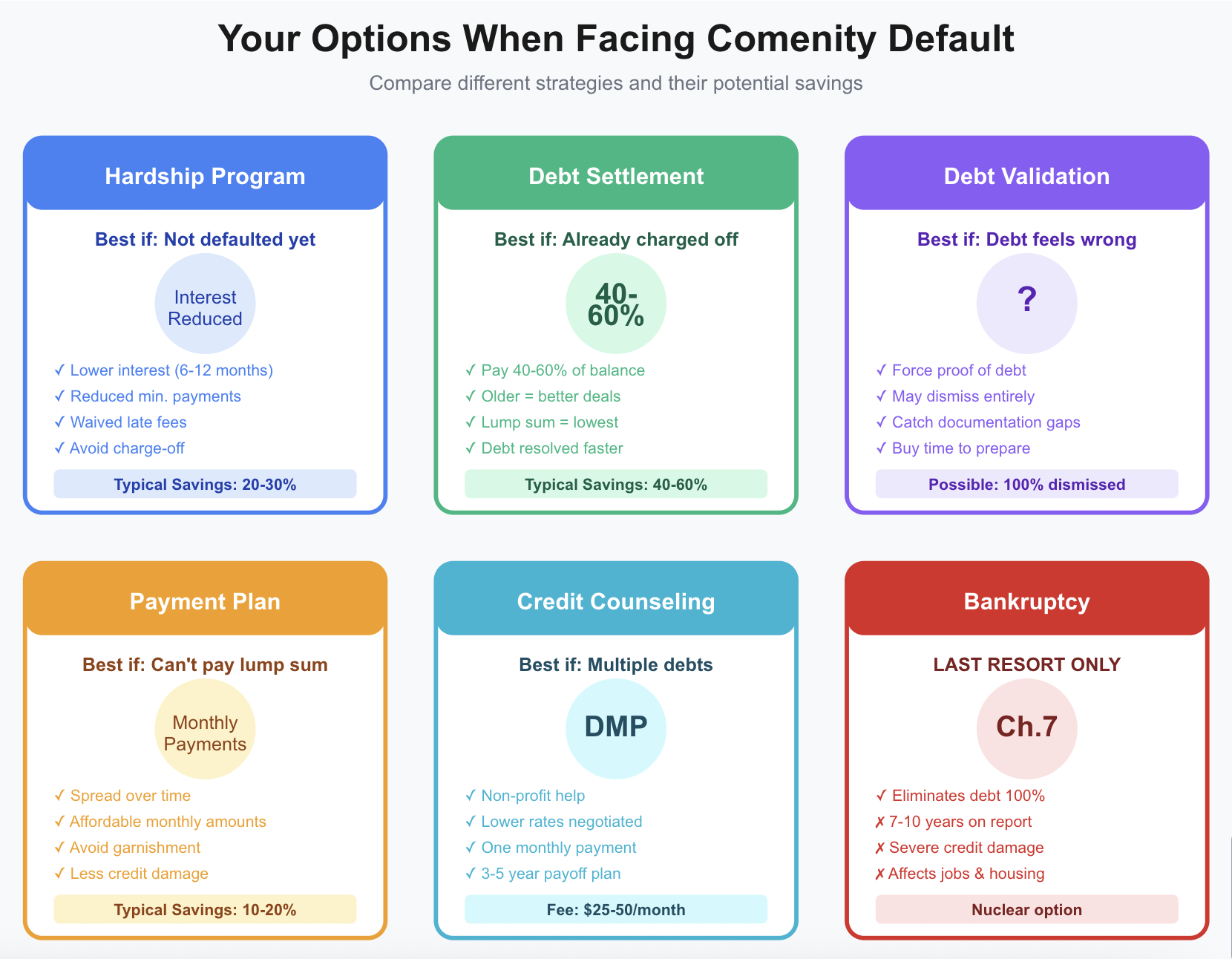

Option 1: Contact Comenity Immediately

If you haven't hit 180 days yet, call Comenity before they charge off your account. They offer hardship programs that can help:

Hardship Plans Include:

- Temporarily lower interest rates (usually 6-12 months)

- Reduced minimum payments

- Waived late fees

- Deferred payments in extreme cases

You must have a legitimate hardship to qualify:

- Job loss

- Medical emergency

- Natural disaster

- Death in the family

- Serious illness

Call Comenity's customer service and explain your situation clearly. Have your budget ready to show your income and expenses.

Warning: Comenity may close your card or lower your credit limit when they put you on a hardship plan.

Option 2: Negotiate A Settlement

If Comenity has already charged off your account, you can negotiate to settle for less than you owe.

How Comenity Settles:

- They typically accept 40-60% of the balance

- Older debts settle for less (sometimes 25-40%)

- Lump-sum payments get better deals than payment plans

Settlement Process:

- Contact Comenity or the collection agency

- Explain that you want to settle the debt

- Start with a low offer (30-40% of balance)

- Negotiate up from there

- Get everything in writing before paying

- Pay only after you have written confirmation

Critical: Never give collectors access to your bank account. Pay by money order or certified check only.

Option 3: Request Debt Validation

By law, you have the right to request proof that you owe the debt. This is especially important if a collection agency bought your debt.

Send a debt validation letter within 30 days of the collector's first contact. Demand that they prove:

- You owe the debt

- The amount they claim is accurate

- They have the legal authority to collect it

- The debt is within the statute of limitations

Send your letter by certified mail with return receipt. Collections must stop while they validate the debt.

Why This Matters: Collection agencies often can't produce proper documentation. If they can't validate the debt, they must remove it from your credit report.

Option 4: Set Up A Payment Plan

If you can't settle in a lump sum, ask about payment arrangements. Comenity and collection agencies will often accept monthly payments.

Tips For Payment Plans:

- Only commit to amounts you can actually afford

- Get the payment agreement in writing

- Make sure it states they'll report to credit bureaus as agreed

- Set up auto-pay so you don't miss payments

- Keep proof of every payment you make

Option 5: Consider Debt Counseling

Non-profit credit counseling agencies can help you manage Comenity debt through a debt management program (DMP).

What DMPs Do:

- Consolidate multiple card payments into one monthly payment

- Negotiate lower interest rates with Comenity

- Get late fees waived

- Create a 3-5 year payoff plan

Comenity's DMP Terms:

- Monthly payment of at least 2% of your balance

- Interest rate of at least 6% (they raise rates below 6%)

- They may close your account

Credit counseling agencies are non-profit and charge minimal fees (usually $25-50 per month).

Option 6: Bankruptcy (Last Resort)

If your debt is overwhelming and you have no way to pay, bankruptcy might make sense. Chapter 7 bankruptcy can eliminate credit card debt completely.

The Consequences:

- Bankruptcy stays on your credit report for 7-10 years

- You'll struggle to get new credit for several years

- It affects job applications and housing

- Some debts can't be discharged (student loans, taxes)

Only consider bankruptcy after exploring all other options. Consult with a bankruptcy attorney to understand if it's right for your situation.

Comenity Default: What NOT To Do

Avoid these common mistakes when dealing with Comenity default:

Don't Ignore It

Ignoring the debt makes everything worse. The balance grows, collectors become more aggressive, and lawsuits become more likely.

Don't Make Partial Payments Without An Agreement

Small payments restart the statute of limitations in many states. This gives Comenity more time to sue you.

Only make payments as part of a written settlement or payment plan agreement.

Don't Admit The Debt Verbally

When collectors call, don't admit you owe the debt. Don't make promises to pay. Don't give them your bank information.

Instead, say: "Send me written verification of this debt. I'm exercising my rights under the Fair Debt Collection Practices Act."

Don't Fall For Scams

Scammers sometimes pretend to be debt collectors. Verify any collection call before sharing information:

- Ask for their company name, address, and phone number

- Look up Comenity's official number online

- Call back using the verified number

- Never pay via gift cards, wire transfers, or cryptocurrency

Don't Pay With A Debit Card Or Give Bank Access

Never give collectors your debit card number or bank account access. They can withdraw more than agreed.

Pay by:

- Money order

- Certified check

- Credit card (dispute protection)

Your Legal Rights Against Comenity And Collectors

The Fair Debt Collection Practices Act (FDCPA) protects you from abusive collection practices.

What Collectors Cannot Do

Comenity and collection agencies cannot:

- Call before 8 a.m. or after 9 p.m.

- Call you at work after you tell them not to

- Harass you with excessive calls

- Use profane or abusive language

- Threaten violence or arrest

- Lie about how much you owe

- Pretend to be law enforcement

- Tell others about your debt

What You Can Do If They Violate Your Rights

If Comenity or collectors break these rules:

- Document everything (record calls where legal, save messages)

- File a complaint with the Consumer Financial Protection Bureau

- File a complaint with your state attorney general

- Report them to the Federal Trade Commission

- Consult with a consumer rights attorney

You can sue for FDCPA violations and recover up to $1,000 plus attorney fees.

How To Rebuild After Default

Defaulting on a Comenity card damages your credit severely, but you can recover.

Pay Off Or Settle The Debt

Your credit won't fully recover until you resolve the debt. Pay it off or settle it as soon as you can afford to.

Once paid, the entry updates to "paid charge-off," which looks better to lenders than "unpaid charge-off."

Dispute Credit Report Errors

After paying, check your credit reports from all three bureaus. Make sure they accurately reflect the paid status.

If you find errors:

- File disputes with the credit bureaus

- Provide proof of payment

- Follow up until they correct it

Build Positive Credit History

You need new positive information to offset the default:

Get a secured credit card: Put down a deposit (usually $200-500) and use it for small purchases. Pay in full every month.

Become an authorized user: Ask a family member with good credit to add you to their card. Their positive history helps your score.

Pay all other bills on time: Payment history is 35% of your credit score. Perfect payments going forward gradually rebuild your score.

Keep credit card balances low: Use less than 30% of your available credit. Lower is better.

Be Patient

Credit recovery takes time. The default's impact lessens as it ages:

- After 2 years: Impact reduces significantly

- After 3-4 years: Lenders may overlook it with other positive factors

- After 7 years: The entry falls off completely

With consistent positive behavior, your score can recover to the 700s even with a charge-off on your report.

The Bottom Line

Defaulting on a Comenity Bank loan has serious consequences:

✗ Your credit score drops 100+ points

✗ The charge-off stays on your report for 7 years

✗ Comenity sends you to collections

✗ Collectors call constantly and may sue you

✗ Your debt keeps growing with interest and fees

✗ You'll struggle to get approved for loans, apartments, and jobs

But you have options:

✓ Contact Comenity about hardship programs

✓ Negotiate a settlement for 40-60% of the balance

✓ Request debt validation to verify the debt

✓ Set up a payment plan you can afford

✓ Consider credit counseling or bankruptcy as last resorts

✓ Know your legal rights and document violations

Most Important: Don't ignore it. The earlier you take action, the more options you have and the less damage you'll face.

If Comenity or collectors are harassing you, violating your rights, or if you're facing a lawsuit, consult with a consumer rights attorney. Many offer free consultations and can help you understand your options for resolving the debt and protecting your credit.