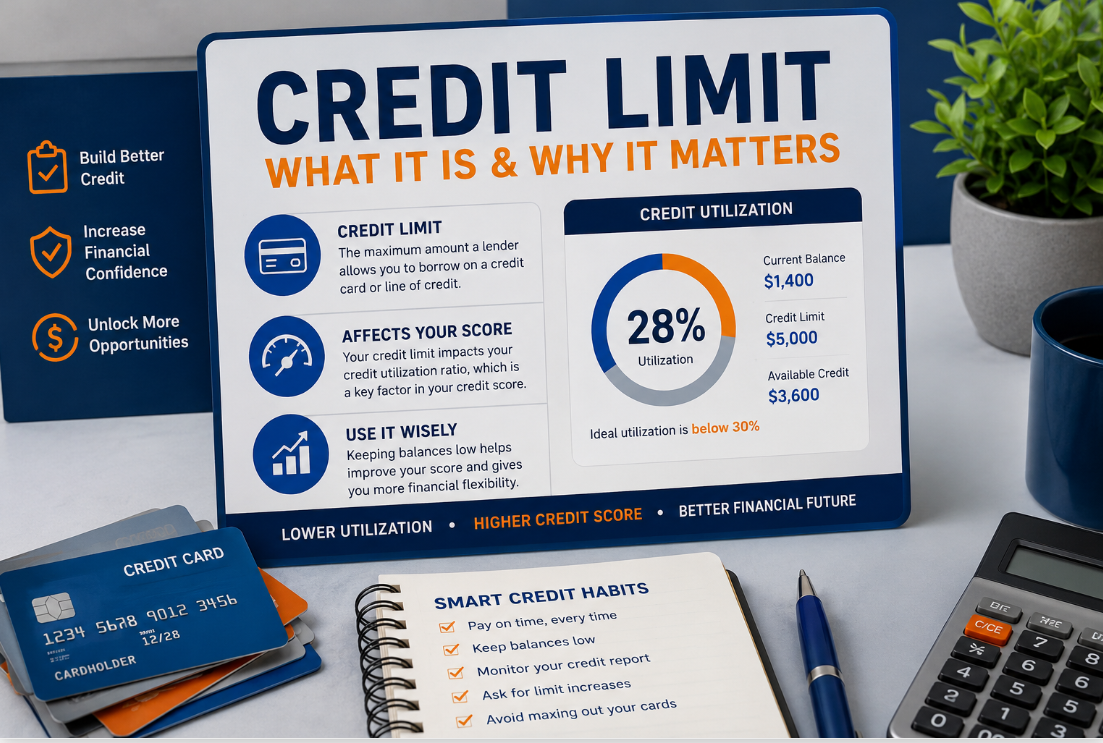

A credit limit meaning is the maximum dollar amount a lender allows you to borrow on a credit card or line of credit at any given time. What does credit limit mean in practice? It means you cannot charge more than that cap without facing a declined transaction, a penalty fee, or damage to your credit score. Your limit also ties directly to your credit utilization ratio, which is one of the biggest factors in your credit score calculation.

Running a credit repair company, I see this confusion almost daily. One case that stands out: a client came in with a 580 credit score and genuinely believed her $500 credit limit was her total "spending budget" for life. She had been paying off the card and not using it, thinking that was the right move. She did not know that responsible use, not avoidance, is what moves the needle.

The confusion is widespread. According to a 2024 NPR report, credit card balances reached $1.11 trillion, and nearly 1 in 5 cardholders are at or near their credit limit. That number signals a major gap in how people understand and manage their available credit.

What Is a Credit Limit and How Does It Work?

A credit limit is the ceiling on how much you can borrow from a lender through a revolving credit account. Credit cards and lines of credit both carry credit limits. Once approved, you can spend up to that amount, pay it down, and borrow again. That cycle repeats for the life of the account.

Here is a simple example. Your card has a $3,000 credit limit. You spend $1,200. Your remaining borrowing power drops to $1,800. Pay off the $1,200, and your full $3,000 limit returns.

Credit limits apply to three main credit types:

Secured credit — You deposit cash as collateral. That deposit amount usually becomes your credit limit.

Unsecured credit — No deposit required. The lender sets your limit based on your credit profile and income.

Open credit — Used for variable bills like utilities. No fixed credit limit applies.

Credit limits are not static. Lenders review accounts regularly and can raise or lower your limit based on how you use the card.

Credit Limit Meaning: How It Works and Affects Your Score?

A credit card limit is the specific cap your card issuer places on a single credit card account. It differs from an overall line of credit because it applies only to that one card.

Card issuers set limits that balance two goals. They want the limit high enough that you use the card often. They also want it low enough that you will not borrow more than you can repay. According to the Federal Reserve, the average total credit limit across all cards held by a U.S. consumer is approximately $29,000. That is spread across multiple cards, not just one.

Credit card limits can vary widely. A secured starter card might carry a $200 limit. A premium travel card issued to a high-income applicant might carry $50,000 or more. The card type matters too. Some cards come with preset limits. Others use a range and place you within it based on your credit file.

What Is the Difference Between a Credit Limit and Available Credit?

These two terms are not interchangeable, and mixing them up causes real financial mistakes.

Credit limit is the total amount the lender approved for your account. It does not change when you spend money.

Available credit is how much of that limit you still have left to use. It changes every time you make a purchase or a payment.

Here is the math: if your credit limit is $5,000 and your current balance is $1,500, your available credit is $3,500.

Many people check their available credit and assume it reflects their credit limit. It does not. Your balance, pending charges, interest accrued, and fees all reduce your available credit, even while your credit limit stays the same.

Tracking available credit matters most before large purchases. Running close to zero available credit increases your utilization rate, which can lower your credit score within days of the reporting date.

What Determines a Credit Card's Credit Limit?

Lenders use several data points when setting your credit limit. The Consumer Financial Protection Bureau (CFPB) confirms that credit scores and credit reports play a direct role in both the interest rate and credit limit you receive.

The key factors lenders weigh:

Credit score — A higher score signals lower risk and typically earns a higher limit.

Payment history — Consistent on-time payments show reliability.

Income — Higher income suggests a greater ability to repay.

Debt-to-income ratio — Lenders compare what you owe to what you earn.

Credit utilization — How much of your existing credit you use affects the decision.

Existing credit accounts — The number and age of open accounts factor in.

New applicants with thin credit files often start with low limits, $300 to $500, because the lender has little data to assess risk. Over time, responsible use builds the profile needed for a higher limit.

At this point, you know what a credit limit is, how it differs from available credit, and what drives the number a lender assigns you. Now let's look at how that number affects your actual credit score.

How Does a Credit Limit Affect Your Credit Score?

Your credit limit directly shapes your credit utilization ratio, the second most important factor in your FICO score after payment history.

Credit utilization ratio = (Current Balance / Credit Limit) x 100

If you carry a $2,000 balance on a card with a $4,000 limit, your utilization is 50%. Lenders and scoring models consider anything above 30% a risk signal. The lower your utilization, the better your score.

According to Experian's 2024 consumer data, the average credit utilization rate in the U.S. is 29%, right at the edge of the recommended threshold. That means a large share of American cardholders are one or two purchases away from crossing into territory that can hurt their score.

A higher credit limit helps your utilization ratio even if your spending stays the same. If that same $2,000 balance sits on a card with an $8,000 limit, your utilization drops to 25%.

Your credit limit itself does not hurt your score. How much of it do you use?

Can You Go Over Your Credit Limit?

Yes, but it comes at a cost.

Most card issuers decline transactions that push you over your limit. Some issuers allow small overages, especially if you have a strong history with them. Going over the limit can trigger:

Over-limit fees on cards that permit overages

A reduction in your credit limit

An increase in your interest rate

Account closure in repeated cases

Carrying a balance above your credit limit also signals financial stress to future lenders. It can appear on your credit report and lower your score quickly.

If your card was declined and you are not sure why, check your available credit first. A pending transaction or an interest charge may have pushed your balance closer to the limit than you realized.

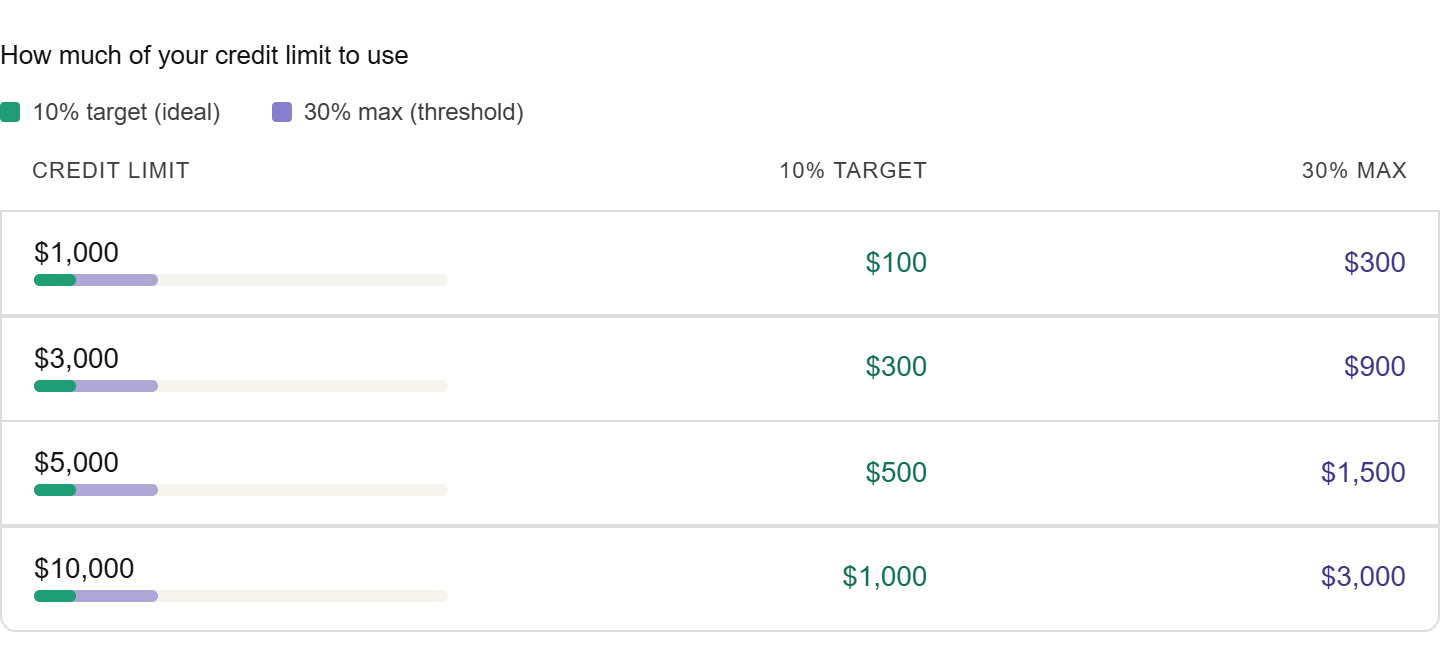

How Much of Your Credit Limit Should You Use?

Keep your credit utilization below 30% of your total credit limit. Most credit experts recommend staying closer to 10% if you want to optimize your score.

Here is a practical target table:

Staying within these ranges matters most in the weeks before applying for a loan, mortgage, or new credit card. Lenders pull your report, and a high utilization rate at that moment can cost you a better rate or approval entirely.

Paying your balance in full each month is the cleanest strategy. It keeps utilization low and avoids interest charges entirely.

How Can You Increase Your Credit Limit?

A higher credit limit gives you more spending flexibility and lowers your utilization ratio without changing your habits. Here is how to request one:

Ask your card issuer directly. Most issuers allow requests through their mobile app, website, or by phone.

Update your income information. Lenders may not have your current income on file. A raise or a new income source can support a higher limit.

Wait for automatic increases. Many issuers review accounts every 6 to 12 months and raise limits for cardholders in good standing.

Open a new card. A new card adds credit to your total available balance, which can lower your overall utilization even before you use it.

Last year, our office worked with over 40 clients pursuing credit limit increases as part of their credit repair plan. In most cases where the client had 12 months of on-time payments, the issuer approved the request without a hard inquiry.

Be aware: some issuers run a hard inquiry when you request an increase. This can temporarily lower your score by a few points. Ask whether the issuer uses a soft or hard pull before submitting the request.

What Happens When a Lender Lowers Your Credit Limit?

Lenders can reduce your credit limit at any time without advance notice. Common reasons include:

Missed or late payments

High utilization on this or other cards

A drop in your credit score

Reduced income on file

Inactivity on the card

A reduced limit can spike your utilization ratio overnight. If you carry a $1,000 balance and your limit drops from $3,000 to $1,500, your utilization jumps from 33% to 67%. That can cause a meaningful credit score drop within the next reporting cycle.

If your limit gets cut, pay down the balance as fast as possible to bring utilization back under control. Then contact the issuer to understand the reason and whether a review is possible.

Need Help Improving Your Credit Limit and Credit Score?

Your credit limit can affect your credit utilization, approvals, and interest rates. If high balances, collections, or credit report errors are holding your score down, ASAP Credit Repair can help you review your report and build a plan.

Get Your Free Credit Report ReviewStart today and see what may be affecting your credit score.

Frequently Asked Questions

Does checking your credit limit affect your credit score? No. Viewing your own credit limit or credit report counts as a soft inquiry and does not affect your score.

Is a higher credit limit always better? A higher limit helps your utilization ratio. The risk is overspending. Only pursue a higher limit if your spending habits are under control.

Can a credit limit be zero? Not on an active card. If a limit drops to zero or the account is suspended, the card is effectively closed for new purchases.

Does a credit limit reset monthly? The limit itself does not reset. Your available credit restores as you pay down your balance.