Why Credit Repair Is Better Than Settling Debt in 2026, because it fixes your credit report without forcing you to miss payments, owe taxes on forgiven debt, or risk a lawsuit from a creditor. Credit repair and debt settlement solve two different problems, and only one of them protects your credit score while you rebuild your finances. This distinction matters even more in 2026, as lenders tighten approval standards and credit reporting errors keep climbing across the industry.

I own ASAP Credit Repair, and I have worked inside this industry for more than 15 years. My team has helped over 22,000 clients clean up their credit files. This topic is one of my favorites to write about because I watch the debt settlement decision split people's confidence in half almost every week. Someone calls us, convinced that settling their debt will fix their credit. It rarely does.

The Consumer Financial Protection Bureau warns that debt settlement may leave you deeper in debt than when you started, since unpaid balances build penalties and interest while you save toward a lump-sum offer. The CFPB also confirms that debt settlement can damage your credit score and your ability to get credit later (consumerfinance.gov). That warning comes straight from the federal agency that tracks these complaints, not from a credit repair company trying to sell you something.

What Credit Repair Actually Does to Your Credit File

Credit repair targets your credit report, not your debt balance. A credit repair company reviews your reports from Equifax, Experian, and TransUnion, then looks for items that are inaccurate, outdated, duplicated, or unverifiable. The Fair Credit Reporting Act gives every consumer the right to dispute those items directly with the bureaus.

Credit repair does not erase real debt. It removes reporting errors that hurt your score without cause. A collection account listed twice, a paid balance still showing as open, or a late payment reported past the seven-year limit are all common targets. Once a bureau cannot verify an item, the law requires the item to come off your report.

Is Credit Repair Possible for Every Credit Report?

Yes, credit repair is possible for most credit reports, but the results depend on what is actually wrong with the file. Every credit report holds dozens of data points pulled from lenders, collectors, and public records. Errors show up more often than people expect.

Credit repair works best in these situations:

A collection account lists the wrong balance or wrong date.

A closed account still reports as open.

The same debt appears more than once from different collectors.

A late payment stays on the report after the legal reporting window ends.

An account belongs to someone else due to a mixed credit file.

Credit repair cannot remove accurate negative information just because it hurts your score. A company that promises to erase all negative items, regardless of accuracy, is breaking federal law under the Credit Repair Organizations Act.

Credit repair fixes what is wrong with your report. Debt settlement, by contrast, tries to change what you owe, and that process comes with a very different set of risks.

What Debt Settlement Actually Does to Your Debt and Your Score

Debt settlement means negotiating with a creditor to accept less than the full balance you owe. Most debt settlement companies ask you to stop paying your creditors first. You deposit money into a separate account instead, and the company uses those funds to negotiate a lump-sum payoff once enough has accumulated.

That strategy sounds simple, but it carries real consequences. Missed payments show up on your credit report immediately. Late fees and interest keep growing on the unpaid balance. Creditors can still sue you for the full amount while you wait for a settlement offer, since a settlement happens outside the legal system.

Debt settlement also creates a tax bill in many cases. Forgiven debt over $600 usually counts as taxable income, and the creditor reports it to the IRS on a 1099-C form. A consumer who settles $8,000 in credit card debt could owe income tax on that forgiven amount the following year.

Why 2026 Raises the Stakes for Debt Settlement

Lenders in 2026 rely more heavily on automated underwriting, which flags settled accounts and charge-offs faster than manual review ever did. A settled account can sit on your credit report for seven years from the date of first delinquency, even after the balance reaches zero.

Last quarter alone, ASAP Credit Repair reviewed credit files for more than 900 clients who had already gone through a debt settlement program. Most of them expected their score to recover once the debt was settled. Instead, their reports still carried the delinquency history, the settled-for-less notation, and in several cases, a fresh collection account from an unpaid remainder.

Debt settlement addresses your balance. It does nothing to fix reporting errors, and it often adds new negative marks to your file. Credit repair addresses the report itself, which is the document lenders actually pull when they decide whether to approve you.

Both strategies solve different problems, but debt settlement carries a much higher cost to your credit score and your tax return. Credit repair works within the report you already have, without adding new damage to it.

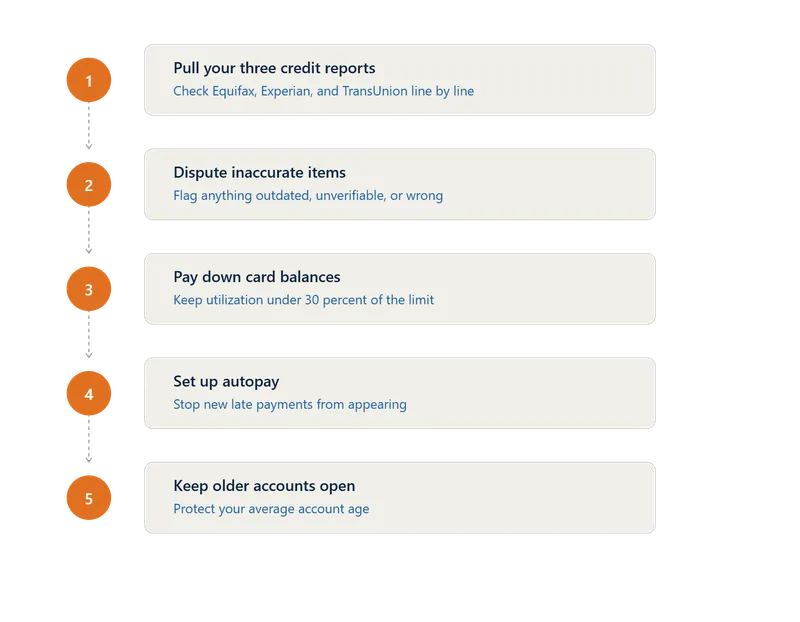

Can a Low Credit Score Be Repaired?

Yes, a low credit score can be repaired, and the fastest path usually starts with a full credit report review. A low score almost always traces back to a handful of causes: missed payments, high credit card balances, collection accounts, or reporting errors.

Repairing a low score follows a clear order:

A score built on real, accurate history takes longer to change than one weighed down by errors. That difference is why the report review always comes first.

Can a Damaged Credit Score Be Repaired After Collections or Charge-Offs?

Yes, a damaged credit score can be repaired even after collections or charge-offs, as long as you work through each account individually. A charge-off means the original creditor wrote off the debt as a loss, but that does not mean the entry has to stay on your report forever or stay inaccurate.

Last quarter, our team disputed more than 1,400 collection accounts on behalf of clients, and a large share of those disputes involved missing documentation, wrong balances, or debt collectors who could not verify the original agreement. When a collector cannot prove the debt is accurate and belongs to you, the bureau must remove the listing.

A charge-off that is accurate and fully documented will likely stay on your report for its full seven years. Credit repair still helps in that situation, since it clears out any duplicate or exaggerated entries tied to the same account, which often inflate the damage beyond what the original debt caused.

How a Good Credit Score Improves Over Time

A good credit score improves over time through consistent habits, not quick fixes. Your score responds to the same five factors every month: payment history, credit utilization, account age, credit mix, and new credit inquiries.

Building toward a stronger score takes these steps:

Pay every account on time, every month, without exception.

Keep credit card balances under 10 percent of the limit for the strongest score impact.

Avoid closing your oldest credit card, since it protects your average account age.

Space out new credit applications instead of applying for several at once.

Check your reports twice a year for new errors before they compound.

A score that climbs through these habits tends to stay higher, since the improvement reflects real financial behavior instead of a temporary dispute win.

When Debt Settlement Still Makes Sense

Debt settlement fits a narrow set of situations. It can help someone with a large amount of unsecured debt who has already fallen behind and has no realistic way to pay the full balance. In that scenario, a reduced payoff may beat years of collection calls and growing interest.

Debt settlement makes less sense for someone current on payments and simply wants a lower balance, since voluntarily stopping payments to qualify for settlement causes damage that did not exist before. Last quarter, our team referred more than 300 callers to nonprofit credit counseling instead of debt settlement, once we confirmed their accounts were still current and their goal was a lower interest rate, not debt forgiveness.

Credit repair and debt settlement answer different questions. Debt settlement asks how to pay less on debt you cannot afford. Credit repair asks how to make your credit report reflect the truth. For most people trying to qualify for a mortgage, a car loan, or a lower interest rate in 2026, the report is the document that decides the outcome, which is exactly why credit repair carries less risk and delivers a cleaner path forward.