Credit Score to Buy a House in Texas (2026) starts at 500 for FHA loans and 620 for conventional mortgages. But the number that gets you approved is not the same number that gets you a good rate. Knowing the difference saves you thousands.

At our credit repair company, we see this situation almost every week. One of the most unforgettable cases came from a Houston client who had a 592 score. Three lenders told him no. A fourth matched him to a USDA rural loan, and he closed on his first home 60 days later. The score alone never tells the full story.

Real buyers share this frustration, too. In r/FirstTimeHomeBuyer on Reddit, a thread with over 400 upvotes showed buyers with scores between 580 and 620 getting approved in Texas through FHA, while others with 640 scores got denied because of high debt-to-income ratios. (Source: reddit.com/r/FirstTimeHomeBuyer) The pattern is clear: credit score is just one piece of the puzzle.

According to the Texas Real Estate Research Center, the median home price in Texas was $330,000 as of December 2025, with home sales showing a 6.1% year-over-year gain. That means more Texas buyers are entering the market, and more of them are asking what score they actually need.

What Is a Good Credit Score to Buy a House?

A good credit score to buy a house is 670 or higher on the FICO scale. At that level, most lenders approve you. You also qualify for competitive interest rates on most loan types.

Here is how FICO score ranges break down for home buyers:

800 to 850: Excellent. You qualify for the best rates and lowest fees.

740 to 799: Very good. Strong approval odds and low mortgage insurance costs.

670 to 739: Good. You qualify for standard loan products at solid rates.

580 to 669: Fair. Approval is possible, but rates will be higher.

500 to 579: Poor. FHA with 10% down is your main option.

Below 500: Most lenders decline entirely.

The average credit score in Texas sits around 680, according to data from Experian. That puts most Texas buyers in the "good" range. But average does not mean easy. A 680 with high credit card balances and missed payments in the last 12 months can still fail lender review.

The target score for the best mortgage rates is 740 or above. At that level, lenders compete for your business. Below 620, your options shrink fast.

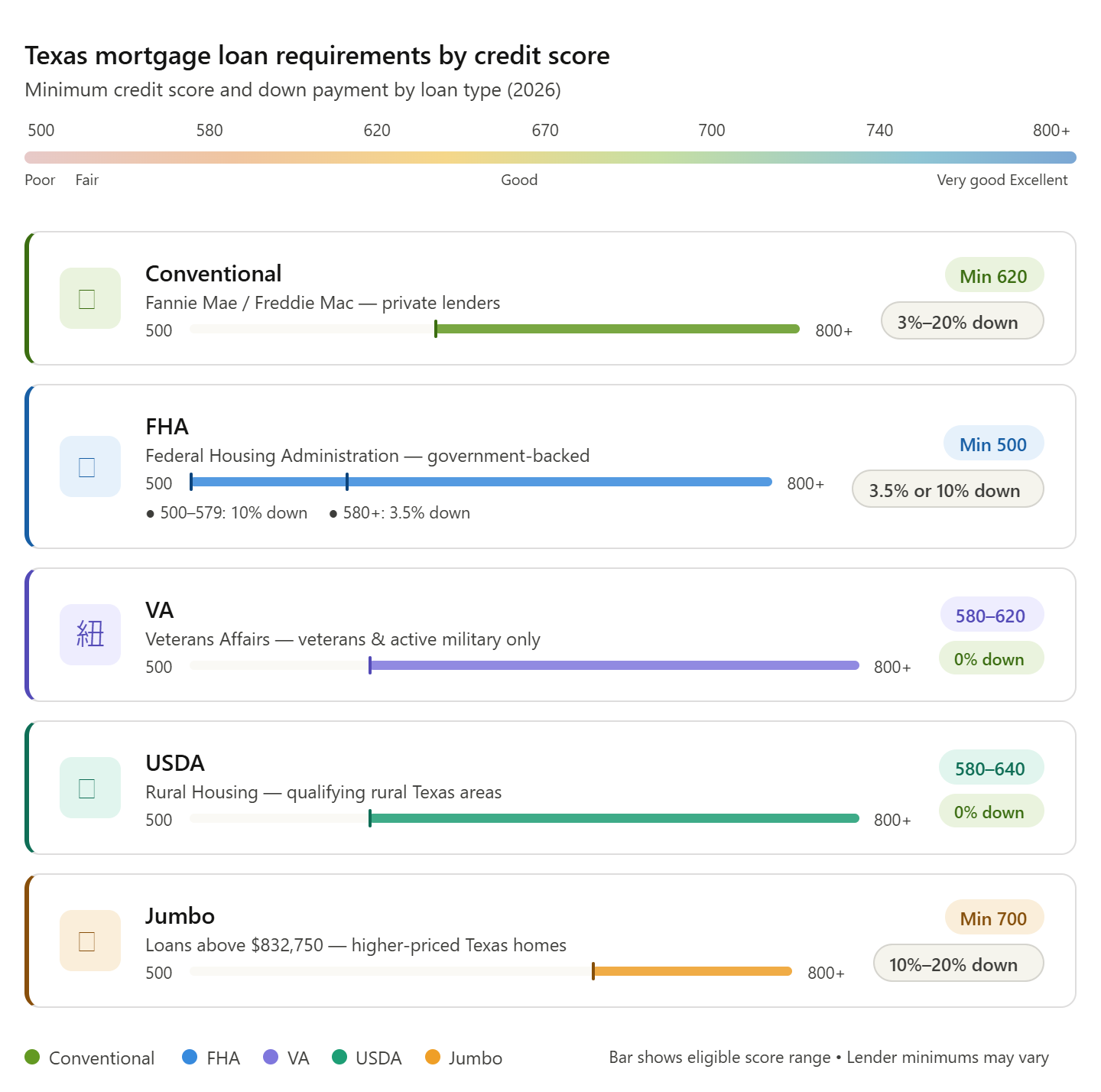

Credit Score Requirements by Loan Type in Texas

Each loan program sets its own minimum credit score. Here is a clear breakdown for Texas buyers in 2026:

One important 2026 update: Fannie Mae removed its hard minimum score requirement for certain conforming loans in late 2025. Lenders now have more room to look at your full financial picture, including income, reserves, and debt levels. But most Texas lenders still apply their own internal minimum of 620. Do not count on this change as a shortcut.

Your score also directly affects your interest rate. A buyer with a 700 score might qualify for a 6.5% mortgage rate. A buyer with a 640 score may face 7.5%. On a $350,000 loan, that difference adds up to over $200 per month — and more than $72,000 over a 30-year term.

What Is the Minimum Credit Score for an FHA Loan?

The minimum credit score for an FHA loan is 580 to qualify with a 3.5% down payment. If your score falls between 500 and 579, the FHA still allows you to borrow, but you need at least 10% down.

FHA loans are backed by the Federal Housing Administration. Because of that government backing, lenders accept lower scores and higher debt levels than they would for conventional loans.

In 2024, over 29% of homebuyers nationally chose FHA loans, largely because of these flexible credit rules. In Texas, FHA loans are especially popular in Dallas and Houston, where first-time buyers use them to get in with smaller down payments.

Key facts about FHA loans in Texas:

FHA loan limits for 2025 start at $524,225 for single-family homes in standard counties.

All FHA loans require mortgage insurance premiums (MIP), both upfront and annual.

FHA allows debt-to-income ratios up to 57% in some cases, much higher than conventional limits.

Scores below 500 do not qualify for FHA at all.

The FHA is often the right path for buyers with scores between 580 and 619. Just know that you will pay for mortgage insurance until you refinance or sell.

Can You Get a Mortgage with Bad Credit in Texas?

Yes. A credit score below 620 does not automatically disqualify you in Texas. Several loan programs and lenders specifically serve buyers with lower scores.

Options available to Texas buyers with bad credit:

FHA loans accept scores from 500 to 579 with 10% down. A score of 580 or higher only requires 3.5% down.

VA loans have no official minimum score. Most VA lenders prefer 620, but some approve buyers at 580. Veterans and active-duty service members should apply here first.

USDA loans serve rural Texas buyers with no down payment required. Lenders typically want 580 to 640. Rural areas like the Texas Hill Country and Foard County often qualify.

Texas state assistance programs also have flexible options. The Texas Department of Housing and Community Affairs (TDHCA) runs the My First Texas Home program, which accepts scores as low as 620 and provides up to 5% down payment assistance. (Source: welcomehome.tdhca.texas.gov)

Last year alone, our office handled 47 cases where clients came in believing homeownership was impossible because of credit. In 31 of those cases, we helped them qualify within six months through FHA or TDHCA programs.

Subprime lenders also operate in Texas. They evaluate employment history and income more heavily than credit scores. But subprime mortgages carry higher rates and fees. Use them only as a last resort after exhausting government-backed options.

Quick Recap: Score Requirements and Loan Options

To summarize where you stand: FHA covers buyers from 500 to 619, conventional starts at 620, and VA and USDA offer zero-down paths for eligible buyers. Texas state programs layer on top of all of these, adding down payment help when your score hits 620.

Are You Financially Ready to Buy a Home in Texas?

A credit score alone does not tell you if you are ready to buy. Lenders also review your debt-to-income ratio, employment history, down payment, and savings.

Here are the key financial checkpoints:

Debt-to-income (DTI) ratio. Most conventional lenders want your total monthly debts to stay below 43% of gross income. FHA allows up to 57% in some cases. For a $5,000 monthly income, that means total debt payments, including your new mortgage, should not exceed $2,150 for conventional and up to $2,850 for FHA.

Income. To comfortably afford a $300,000 home in Texas, most lenders want to see $75,000 to $85,000 in annual household income. Dallas buyers typically need $64,000 or more for a median home in that market.

Down payment. The typical first-time buyer in 2025 put down 10%, according to the National Association of Realtors. FHA requires just 3.5% with a 580 score. USDA and VA require zero.

Employment history. Lenders want two years of steady employment in the same field. Self-employed buyers need two years of tax returns showing consistent income.

Savings after closing. Many lenders want to see one to two months of mortgage payments in reserve after you close.

If your DTI is above 50%, work on paying down existing debt first. If your down payment is under 3.5%, explore Texas state assistance programs before applying.

Texas First-Time Homebuyer Programs That Work With Low Credit Scores

Texas offers two primary programs that help buyers with limited credit or savings:

TDHCA My First Texas Home is available to first-time buyers and veterans. It offers a 30-year fixed-rate mortgage with up to 5% down payment and closing cost assistance. The minimum credit score is 620. The program works with FHA, VA, and USDA loans. Income and purchase price limits apply by county.

TSAHC Home Sweet Texas is run by the Texas State Affordable Housing Corporation. It provides grants or second-lien loans up to 5% of the loan amount. The minimum credit score is usually 620. FHA, VA, and USDA loans are eligible. Some counties offer higher income limits.

TDHCA My Choice Texas Home mirrors the My First Texas program but does not require first-time buyer status. Repeat buyers can use it with a 620 score.

Buyers can stack these programs with other incentives. Some employers, municipalities, and school districts offer matching grants or employer-assisted housing funds on top of state programs.

In our experience, most Texas buyers with scores between 620 and 660 qualify for at least one of these programs. The difference in upfront cost, compared to going it alone, can reach $10,000 to $17,000 on a median Texas home.

Ready to Buy a House in Texas?

Your credit score could determine your mortgage approval, interest rate, and down payment options. Get a professional credit analysis before you apply and discover how to qualify for the best Texas home loan programs.

No pressure. No hard inquiry. Find out what loan programs you may qualify for today.

How to Raise Your Credit Score Before Applying for a Texas Mortgage

Raising your score by 40 to 60 points can move you from FHA territory into conventional loan territory. That shift removes mandatory mortgage insurance and often cuts your rate.

Here is what actually moves the needle:

Pay every bill on time for six consecutive months. Payment history drives 35% of your FICO score.

Bring credit card balances below 30% of your credit limit. Below 10% is ideal. Utilization drives another 30%.

Dispute errors on your credit report at AnnualCreditReport.com. Errors appear on roughly 1 in 5 reports.

Avoid applying for new credit cards or loans in the six months before your mortgage application. Each hard inquiry can drop your score by 5 to 10 points.

Keep old accounts open. Closing a paid-off card can reduce your available credit and raise your utilization ratio.

Consistent on-time payments and debt reduction can raise scores within six to twelve months. Correcting errors and lowering utilization can produce results even faster, sometimes within 30 to 60 days after the bureau updates.

If you are not sure where to start, pull all three credit reports (Equifax, Experian, TransUnion) and compare them. Lenders use the middle score of the three. Improving the weakest report often has the biggest impact on your mortgage qualification.

Credit score requirements in Texas are straightforward once you match the right loan to your situation. FHA opens the door at 580. Conventional starts at 620. Texas state programs add down payment help at 620. And for veterans and rural buyers, VA and USDA loans create paths that credit score alone rarely blocks.

The buyers who succeed are the ones who understand the full picture score, DTI, income, and available programs before they apply.