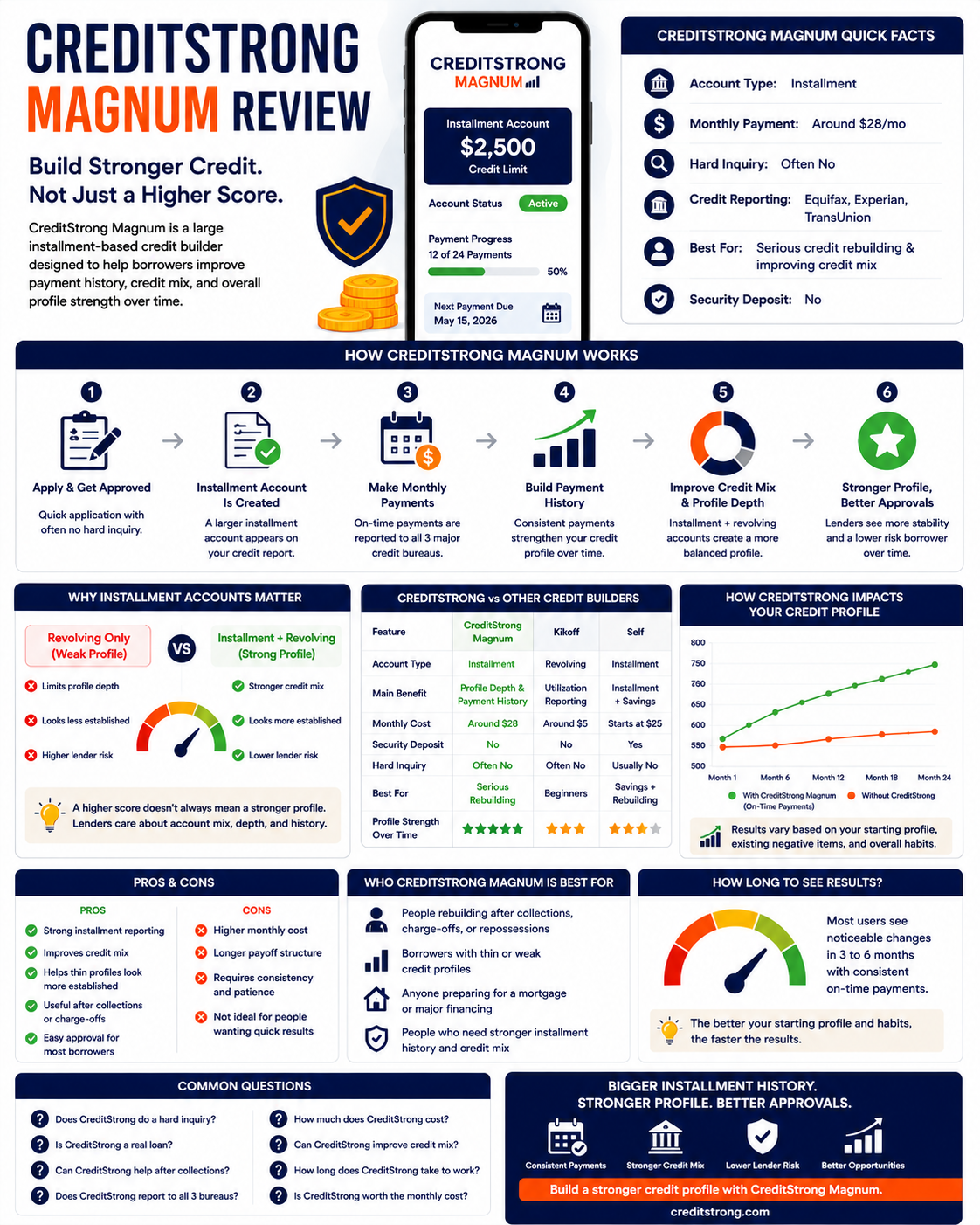

CreditStrong Magnum is a large installment-based credit builder account designed to help users improve payment history, strengthen credit mix, and build a more established credit profile through long-term installment reporting.

Most people don’t look into CreditStrong until smaller credit builder accounts stop helping.

That usually happens after the same frustrating pattern repeats:

the score barely moves

approvals still fail

lenders still hesitate

the profile still looks weak

A lot of borrowers think adding one small revolving account automatically creates a strong credit profile.

It doesn’t.

I’ve seen people with decent scores still struggle during underwriting because the overall profile lacked depth. One tiny secured card or starter builder account often isn’t enough to offset collections, charge-offs, repossessions, or thin reporting history.

That is where CreditStrong enters the conversation differently.

The Magnum plan focuses on larger installment reporting designed to strengthen payment history, improve credit mix, and make the overall profile look more established over time.

Not fast hacks.

Not rewards.

Not “easy points.”

More like long-term profile rebuilding for people trying to recover from real credit damage.

This guide breaks down:

how CreditStrong Magnum works

why installment depth matters

why some builder accounts stop helping

where CreditStrong actually helps

where it becomes expensive

and who should avoid it completely

Why CreditStrong Magnum Helps Some Borrowers More Than Small Credit Builders

Small credit builder accounts can help beginners. But they often do not add enough depth for borrowers rebuilding after collections, charge-offs, or denied loan applications.

CreditStrong Magnum focuses on larger installment reporting. Which can make a credit profile look more established to lenders over time.

What Is Magnum by CreditStrong

Magnum is CreditStrong's largest installment credit builder loan. CreditStrong is a brand of Austin Capital Bank, an FDIC-insured institution. The loan principal , from $2,000 to $25,000 , is held in a locked FDIC-insured savings account while you make monthly payments. Each payment reports to Equifax, Experian, and TransUnion. At the end of the term, the savings are released to you. You pay interest over the term. The net effect: a large positive installment tradeline on all three bureau files plus forced savings returned at the end.

Magnum is fundamentally different from Kikoff and Kovo in one critical way.

Kikoff and Kovo are subscription services. You pay a monthly fee. There are no funds held in your name. Nothing is returned at the end.

Magnum is a real bank loan. You borrow money from Austin Capital Bank. The bank holds it for you in a CD. You pay the loan back over 60-120 months. When the loan is paid off, the CD releases your savings. You pay interest along the way , but you also get principal back. The credit building benefit comes from 60 to 120 months of on-time installment payments on a large balance reported to three bureaus.

How Magnum Works

CreditStrong runs a soft credit check only. Approval is based primarily on income and ability to repay , not your existing credit score.

Austin Capital Bank deposits the loan amount into a locked FDIC-insured CD in your name. You cannot access it yet. This collateral is what allows the loan without a hard credit check.

Fixed monthly payments from $28 auto-draft each month. Each payment is reported to Equifax, Experian, and TransUnion as on-time installment activity.

When all payments complete, the CD releases. You receive the loan principal back minus the interest and fees paid. Net savings depends on term length and APR.

The reporting mechanic is what builds the credit. Every on-time payment adds a positive installment mark to three bureaus. At the end of 24 months (for a 24-payment term), that is 24 positive payment marks per bureau , and a $2,000+ installment account with a clean payment record on your file.

What Makes Magnum the Largest Credit Builder

Magnum reports installment loan balances from $2,000 to $25,000 on your credit report. Most credit builders report $250-$3,000. Larger reported balances create more credit depth. This matters to lenders evaluating not just your score but your demonstrated ability to manage large installment debt responsibly. A $25,000 installment account paid on time for 24 months says something a $240 account cannot.

Why does the balance size matter?

Credit scores measure payment behavior. But lenders look at more than just the score. They evaluate the depth of your credit history. A borrower who has successfully managed a $25,000 installment loan over two years demonstrates significantly more repayment capacity than one who managed a $240 subscription plan.

This distinction shows up most clearly in mortgage underwriting. Underwriters review the actual accounts in the credit file , not just the score. A large, clean installment tradeline from a real bank loan tells a different story than a series of small subscription accounts.

Magnum Plans and Pricing

Magnum plans start at approximately $28 per month for the entry-level tier. Monthly payments increase with higher loan amounts. Terms run 60, 84, 96, or 120 months. Interest is charged on each plan. The total interest paid depends on the loan amount, APR, and term selected. At term end, the principal is returned. Longer terms mean lower monthly payments but more total interest paid over time.

| Loan Amount | Est. Monthly | Term Options | Key Benefit |

|---|---|---|---|

| $2,000 | ~$28/mo | 60-120 months | Entry point , $28/mo affiliate plan. Adds $2,000 installment tradeline to all 3 bureaus. |

| $5,000 | ~$50-70/mo | 60-120 months | Mid-tier. Larger reported balance. Stronger credit depth signal for lenders. |

| $10,000 | ~$80-110/mo | 60-120 months | High impact. $10K installment account with clean history is meaningful for mortgage prep. |

| $25,000 | $100+/mo | 84-120 months | Maximum builder. 33x larger than Self's max plan. For serious credit depth goals. |

Does Magnum Build Credit

Yes. Magnum builds credit through payment history (35% of FICO), credit mix (10%), and account age (15%). The large reported balance also gives lenders a more substantial installment history to evaluate. CreditStrong's own data shows an average +88 FICO Score 8 increase in the first year for users starting below 550 with 12 consecutive on-time payments.

Three FICO factors move with Magnum.

Payment history (35%). Every on-time monthly payment adds a positive installment mark to three bureaus. Missed payments report to all three. The payment consistency over 60-120 months builds the most durable payment history record of any product in the credit builder category.

Credit mix (10%). Borrowers who only have revolving accounts (credit cards) see score improvement when they add a legitimate installment account. Magnum adds a real bank installment loan to the file , not a subscription plan but an actual loan product with an Austin Capital Bank loan number.

Account age (15%). Magnum's 60 to 120 month terms are significantly longer than Kikoff (open-ended) or Kovo (24 months). Keeping a 5-10 year installment account open contributes to average account age over a long horizon.

As Experian's credit builder loan guide explains, a credit builder loan reports your payment history to the bureaus , and the discipline of making consistent on-time payments over a long term is exactly what builds durable credit scores. As LendEDU's 2026 CreditStrong review notes, CreditStrong's Magnum tier produces meaningful score movement specifically because the large loan amount creates more substantial credit depth than typical credit builder products , which is especially impactful on thin files and files with no prior installment history.

Magnum Features That Actually Matter

The amount reported on your credit file is the primary differentiator. A $25,000 installment account with a clean payment history tells a fundamentally different story to lenders than a $240 subscription account. Choose your loan amount based on what you can sustain with consistent monthly payments.

Unlike Kikoff or Kovo, your money comes back. The loan principal held in the FDIC-insured CD is released to you when all payments complete. You pay interest for the credit building benefit, but the core funds are not lost. This makes Magnum closer to a forced savings + credit building program than a pure subscription.

Every payment posts to Equifax, Experian, and TransUnion. No partial bureau coverage. Mortgage lenders pull all three. All three show the same clean installment payment history from a bank-issued loan with a significant balance.

Long terms mean lower monthly payments for the same loan amount. A $10,000 Magnum loan over 120 months costs roughly the same monthly as a $2,000 loan over 24 months , but reports ten times the balance for ten times as long. Longer terms build more account age over time.

Your savings are in a real FDIC-insured bank CD. The loan is a real bank loan product with regulatory oversight. This is not a startup subscription. Lenders who pull your report see a real bank installment loan , not a fintech credit building product. That distinction can matter in manual underwriting reviews.

CreditStrong's own 2024 data: average first-year FICO Score 8 increase of +88 points for users starting below 550 with 12 consecutive on-time payments. Independent reviews estimate 25-70 points in 12 months for most user profiles. Forum reports frequently mention 40+ point gains within four months.

Magnum vs Other Credit Builders

| Feature | Magnum | Kovo | Kikoff Basic | Self |

|---|---|---|---|---|

| Monthly cost (entry) | ~$28 | $10 | $5 | $25+ |

| Account type | Installment (real loan) | Installment (subscription) | Revolving (credit line) | Installment (real loan) |

| Reported balance | $2K-$25K | $240 total plan | $750 credit line | Up to ~$3,000 |

| Bureaus reported | Equifax, Experian, TransUnion | All 4 (incl. Innovis) | Equifax + Experian only | All 3 standard |

| Hard inquiry | No (soft pull) | No | No | No |

| Interest charged | Yes (bank loan) | No | No | Yes (APR applies) |

| Money returned at end | Yes (principal) | No | No | Yes (minus interest) |

| Institution type | FDIC-insured bank | Fintech startup | Fintech startup | Partner bank |

| Term length | 60-120 months | 24 months | Open-ended | 12-24 months |

| Avg first-year score gain (sub-550) | +88 pts (official) | Not published | +86 pts (official) | +47 pts (3rd party) |

Magnum wins on reported balance size, institution backing, and savings return. Kovo wins on four-bureau coverage and lower cost. Kikoff wins on lowest cost and utilization management. Self sits between Magnum and Kovo on most metrics.

The optimal credit building stack for most borrowers preparing for a mortgage: Magnum for large installment history depth, Kikoff for revolving utilization management. Together they cost under $35 per month and address five FICO factors , payment history, utilization, credit mix, account age, and credit depth , across three to four bureaus.

For the full breakdown of every recommended credit building account and how they stack together, the complete guide to credit building cards and accounts covers the entire lineup side by side.

Does Magnum Hurt Your Credit

Applying does not hurt your credit , no hard inquiry. Missing a payment can hurt significantly. Magnum reports to all three standard bureaus. A missed payment that posts to three bureaus simultaneously costs 60-100 points and stays on the file for seven years. Closing the account early may also come with a small fee and stops the positive reporting. The longer the term, the longer you benefit , but also the longer you must maintain consistent payments.

Is CreditStrong Legit

Yes. CreditStrong is a brand of Austin Capital Bank, an FDIC-insured financial institution. The savings account holding your loan principal is FDIC-insured up to applicable limits. CreditStrong reports to all three major bureaus. LendEDU, NerdWallet, Finder, and multiple independent sites. The product is a real bank loan , not a fintech subscription , which makes it one of the most institutionally credible products in the credit builder category.

The most common complaint in CreditStrong reviews is not about the product failing , it is about users who close accounts early, forfeiting some of the savings and the ongoing score-building momentum. Understand the term commitment before starting.

As Firstcard's April 2026 Magnum review states, common user forum themes about Magnum include significant score gains and satisfaction with the forced savings mechanic. The most frequent complaint is locked funds for users who unexpectedly needed liquidity from the savings account , which is not accessible until the term ends.

Who Should Use Magnum

Magnum is strongest for borrowers preparing for a mortgage or large loan within 12-36 months, thin-file borrowers who want maximum credit depth, and anyone who wants the forced savings return at term end. It is less suited for borrowers on tight monthly budgets, people who need liquidity from savings, and beginners who should start with Kikoff or Kovo before committing to a multi-year bank loan.

Use Magnum when:

- You are preparing for a mortgage application in the next 1-3 years and want lender-visible installment depth on your credit file

- Your credit file has no or thin installment history , a $5,000-$25,000 bank installment loan creates the most significant single addition available

- You want forced savings , monthly payments that build credit and return as savings when the term ends

- Budget allows $28+ per month consistently for 60-120 months without financial stress

- You want a real bank loan on your report , not a subscription service , which shows up differently in manual underwriting reviews

Start with Kikoff or Kovo instead when:

- Monthly budget is tight , $5 or $10/month is the limit

- You have no credit at all and need a starter account before committing to a multi-year loan

- You anticipate needing the savings funds before the term ends

- You are early in the credit building process and want to establish payment history before taking on a larger commitment

$15/month: Kikoff ($5) + Kovo ($10) , revolving + installment, 2-4 bureau coverage, no savings return

$33/month: Kikoff ($5) + Magnum entry ($28) , revolving + large installment, 3 bureau coverage, savings return at end

$38/month: Kikoff ($5) + Kovo ($10) + Magnum ($28) minus Kovo after 24 months , maximum early coverage then consolidate to Magnum for long-term depth

What is Magnum by CreditStrong and how does it work?

Magnum is a credit builder loan from CreditStrong, a brand of Austin Capital Bank (FDIC-insured). You apply with no hard credit check, the bank deposits the loan amount ($2,000 to $25,000) into a locked FDIC-insured CD in your name, and you make fixed monthly payments starting at approximately $28. Each payment reports to Equifax, Experian, and TransUnion as on-time installment activity. At the end of the 60-120 month term, the CD releases and you receive the loan principal back minus interest and fees paid over the term.

Can you close Magnum early?

Yes, but early closure may come with a small fee and you lose the ongoing reporting benefit of the remaining term. You still receive your savings (principal minus interest paid to date) when you close. The credit building benefit stops when the account closes , any positive payment history that posted before closure stays on your credit report. For maximum benefit, completing the full term is recommended. Do not start a Magnum plan you may need to close early due to liquidity concerns , the savings are not accessible until the loan is paid off.

Is Magnum better than Self for building credit?

Magnum and Self are both real bank-backed credit builder loans that return savings at term end. Magnum offers larger loan balances (up to $25,000 vs Self's ~$3,000 max) which creates more credit depth on the report. Self starts at lower monthly payments and offers a secured credit card add-on. Both report to all three standard bureaus. Choose Magnum if maximizing the reported installment balance is the priority. Choose Self if a lower monthly payment entry point or the secured card option matters more for your situation.

What happens to your Magnum savings if the bank fails?

The savings are held in an FDIC-insured CD at Austin Capital Bank. FDIC insurance protects deposits up to $250,000 per depositor per institution in the event of a bank failure. Your savings principal is protected by the full extent of standard FDIC coverage. This is one of the key reasons CreditStrong's institutional backing matters , the funds are not in a fintech company's account but in a federally insured bank deposit.

How is Magnum different from Kikoff and Kovo?

Three fundamental differences. First: Magnum reports $2,000-$25,000 on your credit file. Kikoff reports a $750 credit line. Kovo's total plan is $240. Second: Magnum returns your principal at the end , Kikoff and Kovo keep all the money. Third: Magnum charges interest like a real bank loan , Kikoff and Kovo have no interest. Magnum is the most expensive and most powerful. Kikoff and Kovo are the lowest-cost entry points. Most borrowers benefit from combining products rather than choosing just one.

Magnum Builds Credit Depth. We Remove What Is Holding the Score Back.

Magnum adds a major positive installment tradeline. But collections, inaccurate entries, and outdated negatives subtract from the score at the same time. A free 3-bureau audit shows exactly what each bureau reports so you know which negative items to address while Magnum builds the positive side of your file.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card required-

Good Credit Building Credit Cards , Best Accounts for 2026 Magnum is the largest installment builder in our full recommended account lineup. This guide covers every installment and revolving credit building account side by side , Kikoff, Kovo, Magnum, OpenSky, Credit Builder Card, CreditStrong, First Latitude, and First Progress , with descriptions, best-for lines, and affiliate links so you can build the right combination for your credit profile and monthly budget.

-

Kovo Credit Builder Review , $10/Month Installment Plan That Reports to 4 Bureaus Kovo is the most common pairing with Magnum in the first 24 months of a credit building stack. At $10/month with four-bureau reporting including Innovis, Kovo covers the installment history gap across all four bureaus while Magnum builds the large balance depth across the three standard bureaus. Running both for 24 months gives you the broadest coverage before transitioning to Magnum-only for the remaining term.