Good credit building credit cards can help raise your score faster than most people expect. But not every card helps in the same way.

My credit repair company is operating for almost 20 years, and I’ve seen people open the wrong cards just because they were easy to get approved for. A few months later, they are stuck with high fees, tiny limits, and credit scores that barely moved.

That is where a lot of people get frustrated.

Building credit is not only about getting approved for a card. It is about building a credit profile lenders actually trust. That means on-time payments, low balances, and accounts that report correctly to all three credit bureaus.

I’ve seen people gain 50 to 100+ points from one secured card used the right way. I’ve also seen people hurt their scores because they maxed out a $300 limit thinking small cards do not matter.

They do.

Credit cards affect utilization, payment history, account age, and overall lender risk. Those are some of the biggest things that shape your score.

The good news is that you do not need expensive cards or perfect credit to start building momentum. You just need the right setup and the right habits early on.

Good Credit Building Credit Cards That Can Help Raise Your Score

Best Types of Credit Building Cards

The best credit building card depends on where your credit stands right now.

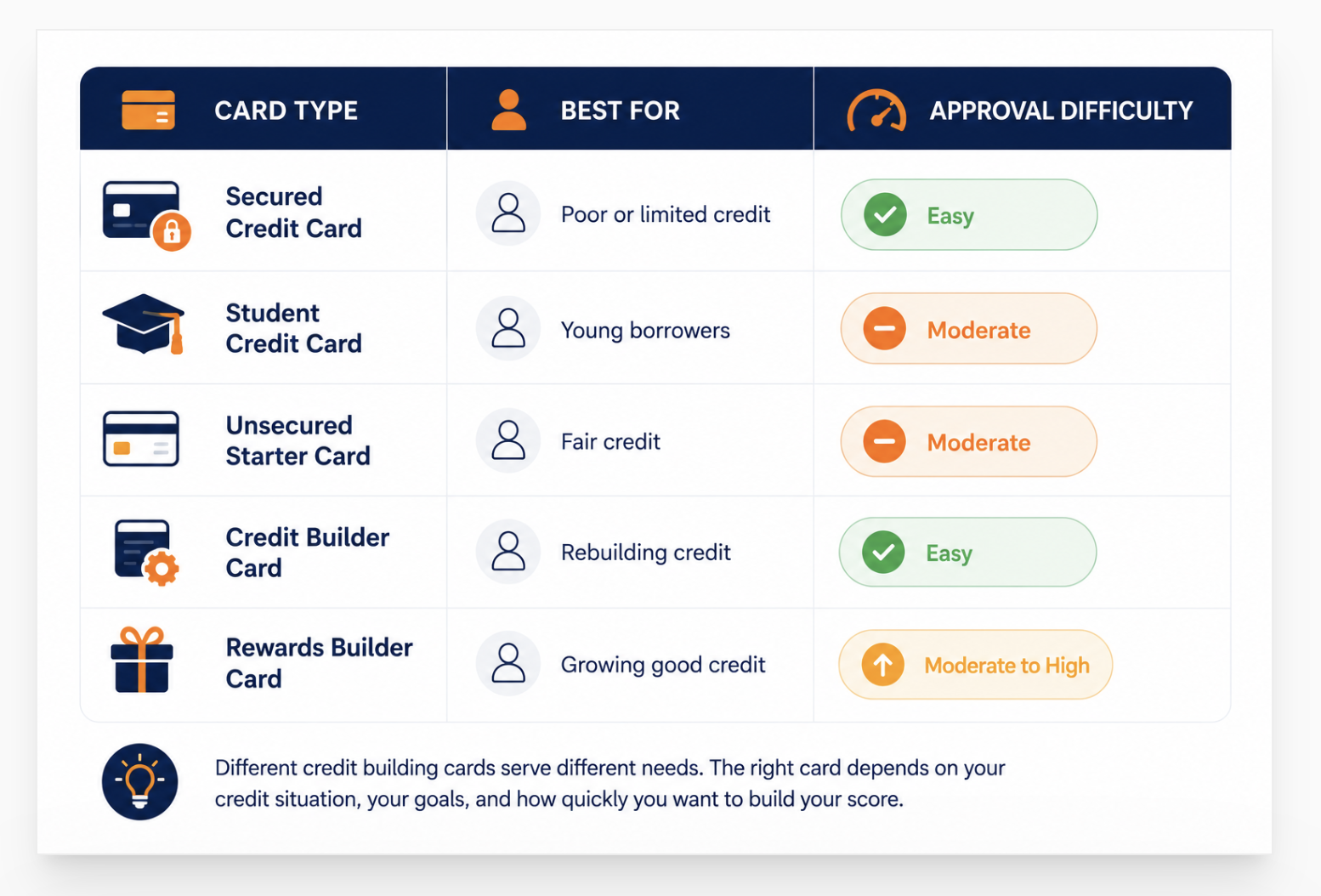

If your score is low or you are starting from scratch, secured cards are usually the easiest way in.

Cards like OpenSky Secured or First Progress are popular because approval is easier and they report to the major credit bureaus. Most only require a small deposit to open.

For people rebuilding after collections, charge-offs, or late payments, installment-style builder accounts can help create positive payment history faster. Programs like Kikoff, Kovo, Self, and CreditStrong are designed for that. Some focus on low monthly cost while others focus on larger installment reporting or savings growth over time.

That difference matters more than people think.

A revolving account helps utilization. An installment account helps payment history mix. Having both can strengthen a credit profile faster than relying on one type alone.

Start with the type your current score qualifies for. Move up as the score improves.

What Are Good Credit Building Credit Cards

Good credit building credit cards are designed for people with no credit, thin files, or damaged credit. They typically approve more easily than standard cards, report monthly to all three bureaus, and help establish positive payment history. The two main types are secured cards (require a deposit) and unsecured starter cards (no deposit, usually for fair credit).

Not every card that approves you is a credit building card.

Some cards charge high annual fees, monthly maintenance fees, and application fees before you even use them. Those fees eat into your available credit, spike utilization, and produce debt without producing credit growth. Avoid them.

A real credit building card has three things.

- Reports to all three bureaus. If the card does not report to Equifax, Experian, and TransUnion, it does not build credit regardless of how responsibly you use it.

- Low or zero annual fee. A $99 annual fee on a $200 limit card immediately uses 49.5% of your credit line on the day it posts. That crushes utilization before you spend a dollar.

- Upgrade path. The best starter cards offer an automatic review for unsecured credit after 6-12 months of responsible use. That upgrade keeps the account age intact and increases your available credit.

How Credit Building Cards Improve Your Score

Credit building cards improve your score through two of the five FICO factors that together control 65% of the score. Payment history (35%) grows with each on-time payment. Utilization (30%) improves when you keep the balance low relative to the limit. A card also adds account age over time and contributes to credit mix. All four benefits come from one card used correctly.

The payment history effect starts immediately. Every statement cycle that closes with a zero or low balance and a confirmed on-time payment posts a positive mark to all three bureaus. Over 12 months, that is 12 positive marks per bureau , or 36 total positive entries from a single card.

Utilization works even faster. Keeping utilization low boosts your score in the same billing cycle where the change occurs. Pay the balance down before the statement closes and the improvement shows up in the next score update within days.

Secured vs Unsecured Credit Building Cards

Secured cards require a refundable deposit , usually $200 , that becomes the credit limit. They are easier to approve because the deposit reduces the lender's risk. Unsecured starter cards require no deposit but usually need fair credit (580-670) to qualify. Both types report to the bureaus the same way. Both build credit through the same FICO mechanics. Choose based on your current score, not preference.

The deposit on a secured card is not a fee , it is collateral.

You deposit $200. Your limit is $200. You use the card, pay it off, and the deposit sits untouched in an account. When you close or upgrade the card, the full deposit returns. It is more like a rental deposit than a cost of doing business.

As Experian's secured vs unsecured credit card guide explains, the credit-building mechanics are identical between the two types. What differs is the approval threshold. Secured cards approve almost anyone with income and a bank account. Unsecured starter cards typically want a fair credit score of at least 580-620 before approving.

| Feature | Secured Card | Unsecured Starter Card |

|---|---|---|

| Deposit required | Yes , typically $200+ | No |

| Credit score needed | None or poor credit accepted | 580-620+ typically |

| Credit building effect | Same as unsecured | Same as secured |

| Annual fees | $0-$25 on best cards | $0-$75 range; some high-fee traps |

| Upgrade path | Most good secured cards offer it | Starts unsecured already |

| Starting credit limit | Equals your deposit | $200-$1,000 typical range |

| Best for | No credit or bad credit | Fair credit (580-669) |

Best Credit Cards for Building Credit

We recommend these accounts for ASAP Credit Repair clients. Use one installment account and one revolving card together for the fastest credit mix improvement.

💰 Installment Credit Builder AccountsAs NerdWallet's 2026 best credit cards for building credit confirms, the strongest options share a common theme , low fees, full three-bureau reporting, and an upgrade path to better products once the credit file shows consistent responsible behavior.

Understanding how your credit limit directly affects your utilization ratio matters especially with secured cards that start at $200. The lower the limit, the faster normal spending can spike utilization past the 30% threshold where score suppression begins.

What Credit Score Do You Need

Most secured credit cards have no minimum score requirement. They approve based on income and the ability to fund the deposit. Unsecured starter cards typically need 580+. Some, like Petal 1, use income and cash flow instead of the score. No score or poor credit starts with secured. Fair credit (580-669) opens both secured and unsecured options.

| Credit Situation | Best Starting Card Type | Approval Note |

|---|---|---|

| No credit history | Secured card or Chime Credit Builder | No score required for most secured cards. Income verification needed. |

| Poor credit (300-579) | Secured card | OpenSky and Chime do not require credit checks. Capital One Platinum Secured accepts poor credit with income. |

| Fair credit (580-669) | Secured or unsecured starter | Both options accessible. Chase Freedom Rise, Petal 1, and Capital One Quicksilver Secured are common choices. |

| Good credit (670-739) | Unsecured rewards cards | Most major unsecured cards now accessible. Focus shifts from credit building to credit optimization. |

One thing to check before applying for any card: whether outstanding collections on your credit report affect the application. Some issuers deny applicants with open collection accounts regardless of score. Removing collections from your credit report before applying can improve approval odds and the terms offered on a new card.

How to Use a Credit Card to Build Credit Fast

Use the card for one small recurring purchase monthly. Pay the full balance before the statement closes , not on the due date, before the closing date. Keep the balance below 10% of the credit limit at statement time. Set autopay to cover the minimum as a backup. Never apply for a second card until 6 months of clean history shows on the first.

The balance on your statement close date is what the bureau receives , not the balance after you pay on the due date. Log into your account and find the statement close date. It is typically 21-25 days before the due date. Every payment strategy should target this date, not the due date.

This is the single most important date on your cardA streaming subscription, a phone bill, a regular gas fill-up. One small, predictable charge. This keeps the balance minimal and the statement report clean. Avoid using the card for groceries, dining, or impulse spending until the credit building habit is completely automatic.

Small and predictable prevents accidental high utilizationThis produces two wins simultaneously. The bureau receives a near-zero balance , perfect utilization. And the on-time payment mark posts for that billing cycle. Both the utilization and payment history factors move in your favor from one action taken before the close date.

Near-zero utilization at statement close + on-time mark = maximum scoring benefitEven with the best intentions, a manual payment can be forgotten. Set autopay to the minimum payment as a backup. If you forget the manual payment before the statement closes, the autopay prevents a 30-day late mark. A single late payment costs 60-110 points and stays for seven years. The backup protects against the worst-case outcome.

Autopay is insurance , not the strategy, but essential protectionEach application generates a hard inquiry costing 5-10 points. Multiple applications early in the credit building process also lower average account age on a thin file. Wait 6 months. Let the first card age and report. Then evaluate whether a second card fits the plan based on your goal and current score.

Patience compounds credit the same way interest compounds debtMistakes That Hurt Your Credit Score

Opening a credit building card helps. Doing these things with it undoes the benefit.

- ✗ Maxing out the limit. A $200 secured card with a $190 balance sits at 95% utilization. That suppresses the score even with perfect payment history. Never go above 30% at statement close. Aim for under 10%.

- ✗ Missing a payment. One 30-day late mark costs 60-110 points and stays on the report for seven years. This is the single most damaging action available on a credit building card.

- ✗ Applying for multiple cards at once. Multiple applications in a short period stack hard inquiries and lower average account age. Both hurt the score you are trying to build.

- ✗ Closing the card early. Closing the first card removes its account age from the average and reduces available credit. Keep it open. A card with a $0 balance and zero activity costs nothing and grows older every month.

- ✗ Carrying a balance to "show activity." This myth costs borrowers interest with zero credit benefit. The card reports activity as long as a statement generates , even if you pay in full every month.

- ✗ Ignoring existing collections. A new credit card cannot offset an active collection dragging the score. Addressing collections in the credit file produces faster results than opening new accounts alone.

How Long Does It Take to Build Credit

Most people see the first meaningful score movement within 3-6 months of opening and using a credit building card correctly. Reaching a 670 score from a thin file typically takes 12-18 months. From poor credit (500-580), getting to 620 usually takes 6-12 months of consistent on-time payments and low utilization. From there, each 10-20 point gain comes from time and account aging.

The timeline depends on what the starting file looks like.

A borrower with no credit at all and a clean history (no negatives) progresses fastest. There is nothing pulling the score down , only positive information being added. These borrowers often hit 650-680 within 12-18 months.

A borrower with poor credit from past late payments or collections builds more slowly because positive new behavior gets weighed against existing negative marks. The negatives age and lose impact every year, but they do not disappear immediately. Patience and consistency win here.

| Starting Situation | Expected Timeline | Key Driver |

|---|---|---|

| No credit history | 12-18 months to 670 | Consistent on-time payments and account aging |

| Poor credit (500-579) | 6-12 months to 620 | Lower utilization and clean post-start payment history |

| Fair credit (580-669) | 6-12 months to 700 | Utilization reduction and no new negative accounts |

| Rebuilding with old negatives | 18-36 months to 700 | Negatives aging off + positive history stacking |

What Lenders Want to See

Lenders do not just look at the score. They want a pattern. Consistent on-time payments. Low balances relative to limits. No recent applications. Stable account history. No open collections. A credit building card managed correctly for 12-24 months creates that pattern. The score is the summary , the payment and utilization behavior is what lenders actually read when they review a file.

A 680 score with one secured card, 24 months of on-time payments, and 8% utilization tells a very different story than a 680 score with four accounts, missed payments, and high balances that happened to average out.

The first file signals control. The second signals chaos that temporarily stabilized.

What lenders want to see:

- 12-24 months of on-time payment history on every open account

- Low utilization across all revolving accounts , under 30% total, under 10% per card

- No recent hard inquiries that suggest active new borrowing

- No open collections that remain unresolved

- Account age that demonstrates a track record, not a brand new file

- Income and DTI that show the new loan payment fits the budget

A credit building card is one tool. It builds payment history and utilization management habits. But it works best alongside a clean file , no outstanding collections pulling the score down while the card works to push it up. As Bankrate's secured credit card guide notes, keeping the balance low and paying off the card each month is the most effective strategy , not just for the score, but for the financial habits lenders want to see in any borrower they approve for a major loan.

What is the best credit card for building credit?

The best credit card for building credit depends on your starting point. For no credit or poor credit, Capital One Platinum Secured, Discover it Secured, and Chime Credit Builder are consistently recommended for their low fees, full three-bureau reporting, and upgrade paths. For fair credit, Chase Freedom Rise and Petal 1 Visa offer unsecured access. The card itself matters less than using it correctly , low utilization, on-time payments, and keeping the account open.

How many cards should beginners have?

Start with one. Get the first card fully under control , statement close date tracked, payments timed, utilization managed. After 6-12 months of clean history, evaluate whether a second card makes sense. A second card can help utilization math by increasing total available credit. But multiple applications in the early months stack hard inquiries and slow the score growth you are trying to build.

Does utilization still matter with a $200 limit card?

Yes , more than with any other card. A $200 limit means $20 puts you at 10% utilization. $60 puts you at 30%. $100 puts you at 50%. Every dollar of spending creates a larger utilization impact than it would on a higher-limit card. This is why paying the balance before the statement closes is especially important on secured starter cards. The scoring model does not know the limit is only $200 , it just reads the utilization percentage.

How long should you keep your first credit building card?

Keep it open indefinitely. The first card becomes the oldest account in your credit file, which contributes to average account age (15% of FICO). Closing it reduces both account age and available credit simultaneously. Even if you upgrade to better cards later, keep the first one open with a small recurring charge and autopay to maintain the account age and reporting without any effort or carrying risk.

Can one credit card build good credit?

Yes. One card used correctly builds payment history, establishes a positive utilization pattern, adds account age, and contributes to credit mix. Many borrowers go from no credit to 670+ with a single secured card used responsibly for 12-18 months. A second card can accelerate the process by improving the total utilization ratio , but it is not required. Consistency on one card beats inconsistency on three.

Starting a Credit Card on a Damaged File? Fix the File First.

A new credit building card works best on a clean file. If collections, inaccurate entries, or outdated negatives are suppressing your score, a free 3-bureau audit shows exactly what is there so you can address the right things before opening a new account.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card required-

How to Cancel a Credit Card Without Hurting Your Score The instinct to close a credit card you are not using can backfire. This covers the exact impact of closing a card on account age and available credit, which cards are safer to close, when closing makes financial sense despite the score impact, and how to cancel a card correctly if you decide the fee or terms no longer justify keeping it open.

-

Is Gross Income Before or After Taxes , What Credit Applications Ask For Every credit card application asks for income. Most applicants are unsure whether to enter gross or net income , and entering the wrong number can affect both approval odds and credit limit offers. This covers what gross income means, what credit card issuers use it for in underwriting, and why income reporting accuracy matters for the best available credit limit on a first credit building card.

-

Can You Buy a House With a Repo on Your Credit A credit building card is often the first step toward qualifying for a mortgage after a major derogatory event. This covers how a repossession affects mortgage underwriting, which loan programs remain open after a repo, and the credit recovery timeline that moves a post-repo file from the Fair tier into the Good and Very Good tiers where mortgage approval becomes consistently accessible.