Is gross income after taxes? No. Gross income is what you earn before taxes are removed. Net income is what you keep after taxes come out. Most people mix these two up. That one mistake leads to bad budgets, loan denials, and tax errors.

I run a credit repair company. One client came to me after her finances fell apart fast. She built her monthly budget using her gross income. She thought it was her take-home pay. Within three weeks, she overdrafted her account. She missed a credit card payment. Her credit score dropped 40 points from that single error.

According to the IRS, 165.8 million tax returns were filed in 2025. Every one of them started with gross income as the base number. That number is always pre-tax. The Bureau of Labor Statistics found that the median weekly gross income for full-time U.S. workers hit $1,214 in Q3 2025, which works out to about $63,128 per year before any deductions.

Gross income is where the math starts. Net income is what you actually live on. Knowing the answer to "is gross income after taxes" changes how you read every paycheck, tax form, and loan application you will ever sign.

Is Gross Income After Taxes? Here Is the Direct Answer

People ask, "Is gross income after taxes more than you might think? The answer is always no.

Gross income is your total earnings before anything is taken out. Taxes have not touched it yet. Net income is the amount left after taxes and all other deductions are removed.

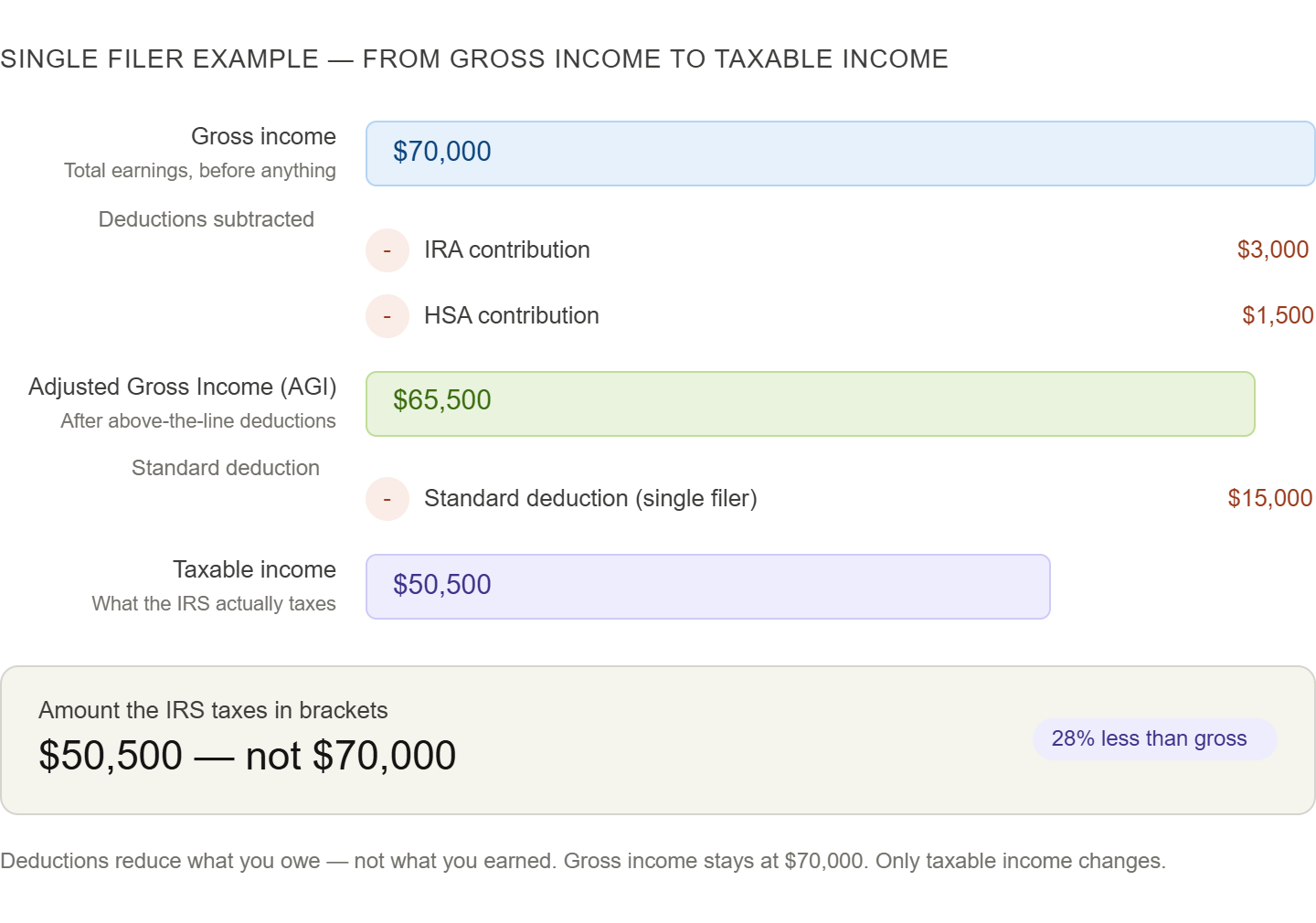

Here is a simple example. You sign a job offer for $70,000 per year. That $70,000 is your gross income. After federal tax, state tax, Social Security, and Medicare are removed, your take-home pay drops to around $50,000. That $50,000 is your net income.

The IRS defines gross income as "all income from whatever source derived." Taxes reduce that amount. They do not define it.

What Is the Difference Between Gross Income and Net Income?

Gross income is your total earnings before any deductions. Net income is what lands in your bank account after taxes and withholdings come out.

Gross income includes:

Wages, salaries, and hourly pay

Bonuses, commissions, and tips

Rental income

Dividends and capital gains

Freelance or business income

Retirement distributions

Net income is what remains after these are subtracted:

Federal income tax

State income tax

Social Security tax (6.2%)

Medicare tax (1.45%)

Health insurance premiums

Retirement contributions

For most middle-income earners, the gap between gross and net pay runs between 25% and 35%. That is a large cut when you are building a monthly budget.

Last year, our credit repair team reviewed over 300 client financial profiles. Each person had used gross income to estimate loan payments. In nearly 40% of those cases, lenders flagged a debt-to-income ratio that was too high. The clients had not accounted for what taxes would remove first.

What Is the Difference Between Gross Income Before and After Taxes?

"Gross income before taxes" is simply your gross income. There is nothing else to add. "Gross income after taxes" is not a standard financial term. When people say "income after taxes," they mean net income.

Gross income does not change based on taxes. It stays fixed at your total earned amount. Taxes are subtracted from it to create net income.

Here is the full income flow from top to bottom:

Gross income: All earnings before anything is removed.

Adjusted Gross Income (AGI): Gross income minus specific IRS-approved deductions.

Taxable income: AGI minus your standard or itemized deduction.

Net income: Your take-home pay after all taxes and payroll deductions.

Each step moves further from what you earn and closer to what you keep. Use net income for budgeting. Use gross income for loan paperwork and tax filing. That is the clearest way to answer "is gross income after taxes": gross income comes first, taxes come second.

What Is Considered Gross Income?

Gross income covers far more than just your paycheck. The IRS says gross income is all income from whatever source, unless the law cuts it out.

These sources count toward gross income:

Wages, salaries, and hourly pay

Bonuses, commissions, and tips

Rental income from properties you own

Investment income and dividends

Freelance or self-employment earnings

Business profits

Retirement distributions from a 401(k) or IRA

Gambling winnings

Canceled debt, in most cases

Cryptocurrency gains

These do not count:

Gifts up to the annual exclusion limit, most inheritances, life insurance payouts, and certain municipal bond interest are all excluded from gross income.

One thing surprises many people. Canceled credit card debt counts as gross income. The IRS already receives 1099-C forms reporting those amounts. Not reporting canceled debt is one of the top reasons people receive IRS notices.

This is also where the question "is gross income after taxes" gets more nuanced. Some income never gets taxed at all. But that does not mean it skips the gross income line. It still starts there.

Is Gross Income Taxable?

Gross income is the base for tax calculations. But the IRS does not tax every dollar at the same rate.

Taxes move through this chain:

Gross income is reduced by above-the-line deductions to produce AGI.

AGI is reduced by the standard or itemized deduction to produce taxable income.

Tax rates apply only to taxable income, not to the full gross income.

Some income avoids tax entirely. Qualified Roth IRA distributions carry no tax. Certain municipal bond interest is tax-free. Part of Social Security income may be excluded, too.

Gross income sets the ceiling. Deductions and credits pull the taxable amount down from there. When you ask, "Is gross income after taxes?" the answer is still no, even at this stage. Taxes work on taxable income, which is always lower than gross income.

How to Calculate Your Gross Income

Add every source of income together before any deductions are taken. That total is your gross income.

For a salaried employee: Box 1 on your W-2 is not your full gross income. Pre-tax items like 401(k) contributions and health premiums are already removed from Box 1. Boxes 3 and 5 are closer to your true gross pay.

For a self-employed person: Gross income is total revenue before business expenses. Use IRS Schedule C to track it.

Quick estimates:

Multiply your hourly rate by 2,000 to get a yearly gross income estimate. Multiply your weekly gross pay by 52 to reach the same result.

Gross income matters in three main ways. Mortgage lenders cap housing costs at 28% of your gross monthly income, per the Consumer Financial Protection Bureau. Loan and credit applications require gross income, not net. Tax returns start with gross income and reduce it from there.

Why Gross Income Matters for Credit and Loans

Lenders ask for gross income, not net income. That number gives them a clean, pre-tax benchmark. It removes the variable of personal spending choices.

At our credit repair firm, we saw several cases in just the first quarter of this year where clients wrote their net income on mortgage applications. Underwriters caught the discrepancy during income checks. One client had their loan held up for three weeks while they gathered the right documents.

Gross income also controls eligibility for government programs. Medicaid, income-driven student loan repayment, and the Earned Income Tax Credit all use gross income thresholds to determine eligibility.

Use net income for your daily spending plan. Use gross income for loan paperwork, benefit applications, and tax returns.

Confused About What Income Lenders Actually Count?

Your gross income, net income, and credit profile all affect how lenders view you. If old collections, late payments, or credit report errors are holding you back, we can help you review your credit and build a plan.

Get Your Free Credit Report ReviewSee what may be hurting your credit before you apply for a loan, mortgage, or credit card.

Gross Income vs. AGI vs. Taxable Income: Which Number Matters?

All three numbers matter. Each one answers a different question.

Gross income tells you what you earned in total before any adjustments.

AGI is gross income minus above-the-line deductions. It appears on Line 11 of Form 1040. The average AGI in the U.S. fell between $75,000 and $80,000 in 2023, based on the latest IRS data. Benefit programs and financial aid offices often use AGI to check eligibility.

Taxable income is AGI minus your standard or itemized deduction. This is the number the IRS uses to calculate your actual tax bill. It is nearly always lower than your gross income.

Use gross income when applying for loans, checking income filing thresholds, or filling out lender forms.

Use AGI when: checking tax credit eligibility, filing your return, or applying for financial aid.

Use taxable income when: figuring out your actual tax owed or choosing between the standard deduction and itemizing.

So, is gross income after taxes? No. Gross income is always before taxes. Net income is after. AGI sits between the two. Knowing where each number fits keeps your budget accurate, your loan applications clean, and your tax return correct.