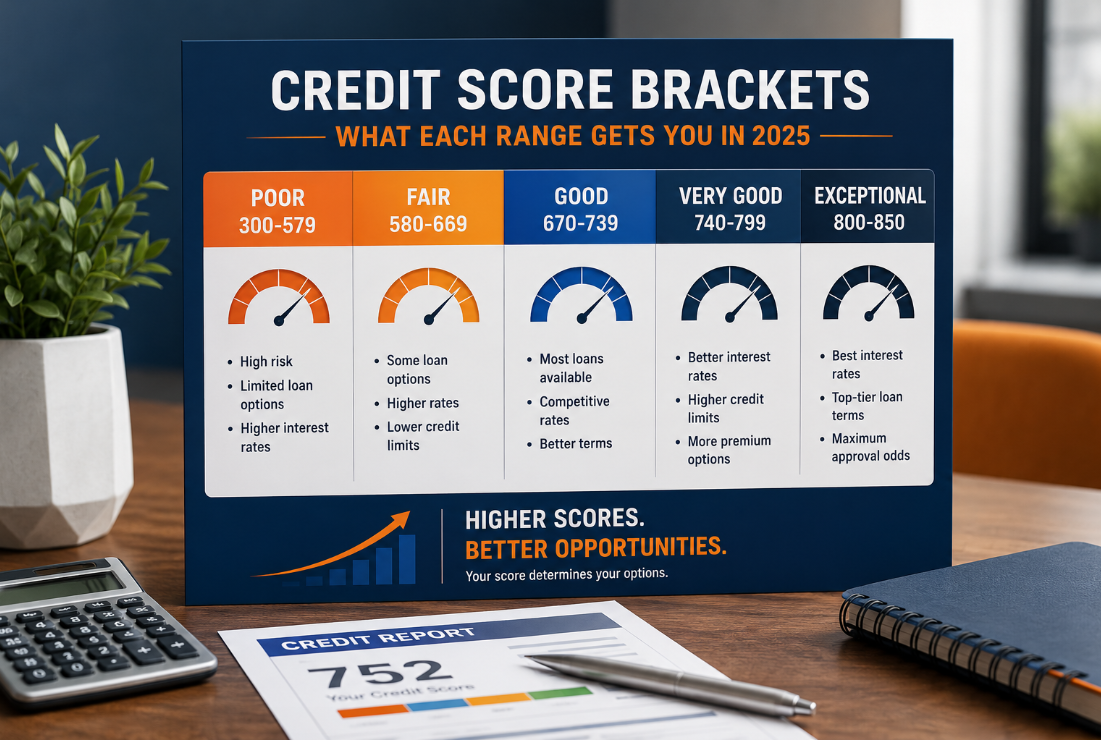

Credit score brackets are the five ranges that lenders use to classify borrowers from highest to lowest risk. The FICO scale runs from 300 to 850, divided into Poor (300–579), Fair (580–669), Good (670–739), Very Good (740–799), and Exceptional (800–850). Where you land on that scale directly determines the rates you pay, the loans you qualify for, and how much the entire process costs you.

Running a credit repair company, I see the same pattern repeat itself. A client comes in right after a loan denial, frustrated, saying their score "seemed fine." One of the most unforgettable accounts this past year came from a client who had a 671 and thought she was in solid shape for a mortgage. She was in the Good bracket. But her lender was using a stricter internal cutoff. Eight points lower, and she would have missed even that window. Understanding the brackets is not just useful trivia. It determines real money.

According to FICO's inaugural Score Credit Insights report, the middle score range of 600–749 shrank from 38.1% of the U.S. population in 2021 to 33.8% in 2025, while more consumers moved toward both the highest and lowest brackets. Credit scores are splitting, not averaging out.

What Are Credit Score Brackets?

Credit score brackets are groupings that credit scoring companies create to categorize borrowers by risk level. FICO and VantageScore both use the 300–850 range, but they draw the bracket lines differently.

Lenders use these groupings to make fast decisions. A score of 720 and a score of 790 may look similar to a consumer. To a lender, one is Good, and the other is Very Good, and that difference can affect the interest rate by as much as a full percentage point.

The bracket you sit in at the time of application matters more than your score history. Lenders pull a current snapshot. A score that moved three points in the wrong direction before application day can push you into a lower bracket and change your offer entirely.

FICO Credit Score Brackets: The Full Breakdown

FICO scores are used in 90% of top U.S. lending decisions. These are the five official ranges:

Poor: 300–579

Scores in this range signal high risk to lenders. Most traditional banks will not approve a mortgage, personal loan, or standard credit card at this level. Borrowers in this bracket often face secured credit card requirements, sky-high APRs, or flat denials.

Common reasons a score lands here include charge-offs, active collections, multiple missed payments, bankruptcy, or foreclosure. In 2025, the percentage of Americans in the poor range grew to 15%, up from prior years, driven in part by the resumption of federal student loan delinquency reporting (FICO, 2025).

Fair: 580–669

Fair credit opens more doors, but none of them are cheap. FHA home loans are available with a score of 580 or higher, requiring as little as 3.5% down. Auto loans are possible, but expect rates between 10% and 15%, depending on the lender. Credit cards in this range typically carry annual fees and low limits.

The real cost shows up over time. A borrower with a 620 FICO score taking out a $350,000 mortgage can pay nearly $50,000 more in interest over 30 years than a borrower with a 700 score, according to Experian data. That gap comes from a difference of less than two brackets.

Good: 670–739

Good credit is where most Americans sit. The national average FICO score was 713 in 2025, which places the average U.S. borrower solidly in the Good bracket. At this level, most mainstream loans and credit cards are available. Interest rates are competitive, though not the lowest on the market.

Borrowers here are typically called prime borrowers by lenders. Getting from Good to Very Good can still save thousands in interest, especially on large loans. The gap between 739 and 740 is one point on a scale, but it is a full bracket change that lenders recognize.

Very Good: 740–799

Very Good credit gives borrowers access to most lenders' best-advertised rates. Mortgage, auto loan, and credit card approvals become straightforward. Lenders view this range as low risk. Premium credit cards with strong rewards programs become available here.

In 2025, 48.1% of U.S. consumers held scores of 750 or higher, up from 43.3% in 2019, according to FICO's Score Credit Insights report. That is a meaningful shift. Nearly half of American consumers are now in the Very Good bracket or above, which tells you how competitive lending has become at these tiers.

Exceptional: 800–850

Exceptional credit gives borrowers the best terms available. Lenders rarely deny applications in this range. Interest rates sit at or near their floor. Credit card issuers compete for borrowers with these scores.

As of March 2025, 1.76% of U.S. consumers held a perfect 850 FICO score, according to Experian. Reaching 850 is not necessary to get top-tier rates. Most lenders treat scores above 800 identically. The practical benefits of 800 and 850 are the same. Getting from 800 to 850 is a point of personal achievement, not a financial necessity.

VantageScore Brackets vs. FICO Brackets

Most free credit monitoring tools, including Credit Karma and many bank apps, display VantageScore 3.0. Mortgage lenders typically use FICO 2, 4, or 5. Auto lenders often use the FICO Auto Score. The score you check and the score your lender pulls are often different models. Checking the wrong one before a major application is one of the most common mistakes borrowers make.

In our office alone, we review cases regularly where a client's VantageScore and FICO score differ by 40 to 60 points. That difference can mean landing in entirely different brackets depending on which model the lender uses.

What Credit Score Do You Need for a Mortgage?

The minimum FICO score for an FHA loan is 580, with a 3.5% down payment. Dropping below 580 requires a 10% down payment to qualify. Conventional loans through Fannie Mae and Freddie Mac typically require a minimum of 620.

Better brackets unlock better rates. In Q4 of 2025, mortgage approvals for scores between 620 and 679 dropped by 18% compared to 2023, based on tracked application data. Lenders tightened standards as interest rates stayed elevated. Borrowers on the edge of a bracket had less margin for error.

VA loans have no official minimum credit score, but most VA lenders set their own internal floor at 580 to 620. USDA loans typically require at least 640.

The practical target for the best mortgage rates is 760 or above. Below that, even within the Very Good bracket, rates can vary by lender.

What Credit Score Do You Need for a Car Loan?

Auto lenders use a tiered system. Each tier carries a different interest rate, and the brackets map closely onto the FICO model.

Scores of 750 or higher get the best auto loan rates, often called super-prime. Scores from 700 to 749 land in the prime tier. The near-prime range runs from 650 to 699. Subprime auto loans cover 600 to 649, and deep subprime covers anything below 600.

Auto loan delinquencies rose 24% since 2021, according to FICO's 2025 Credit Insights report. Lenders in this market moved cautiously. Borrowers in the subprime and near-prime range paid materially higher rates in 2025 than they would have in 2022 for the same vehicle.

How Credit Score Brackets Affect Interest Rates

The bracket you sit in at loan application time has a direct, measurable dollar impact. Rate differences between brackets are not minor rounding errors. They translate into real money over the life of a loan.

For mortgages, the rate difference between a 620 score and a 760 score can reach 1.5 percentage points or more. On a $350,000 30-year fixed mortgage, that difference equals roughly $138 more per month and nearly $50,000 more over the life of the loan, according to Experian.

For auto loans, the spread between a prime and deep-subprime rate can exceed 10 percentage points. A $25,000 car loan at 7% costs the borrower about $495 per month. The same loan at 17% costs $627 per month. Over five years, that is over $7,900 in additional interest, all tied to a bracket difference.

Bankcard delinquencies rose 48% since 2021 in the U.S., with average credit utilization climbing to 35.5% according to FICO's Credit Insights data. Rising utilization pushes consumers down brackets. A consumer who was solidly in Very Good territory in 2022 may now sit in Good territory simply from carrying higher balances on the same cards, with no missed payments.

How to Move from One Bracket to the Next

Moving up one bracket does not require years of perfect credit. In most cases, two or three targeted changes produce the biggest score gains in the shortest time.

Credit utilization is the fastest lever. Utilization above 30% actively holds scores down. Paying down balances to below 10% of the available limit can move a score by 20 to 40 points within one to two billing cycles. That single change moves many consumers from Fair into Good, or from Good into Very Good.

Disputing errors is the second lever. The FTC found that one in five Americans has at least one error on their credit report, and one in ten has an error material enough to lower their score. In this office, more clients than I can count moved up a full bracket after a single error removal. The process takes 30 to 45 days. It costs nothing.

Payment history is the third lever. Even one 30-day late payment can remain on a credit report for seven years. Bringing all current accounts to current status and keeping them current prevents further bracket damage and starts the long recovery. On-time payments compound over time, and their weight in the score grows as the derogatory mark ages.

Applying for new credit in large amounts right before a major loan application is the most common self-inflicted bracket drop. Multiple hard inquiries in a short window lower the score temporarily. Give your score 90 days of clean inactivity before applying for anything large.

Not Happy With Your Credit Score Bracket?

Moving from Fair to Good or from Good to Very Good could save you thousands on loans, credit cards, and mortgage interest rates. Get a personalized credit analysis and see what may be holding your score back.

No obligation. Find out what may be hurting your score and what steps could help improve your credit score faster.

Where Americans Stand in the Brackets Right Now

The 2025 credit landscape shifted in two directions at once. Scores at the top kept rising. Scores at the bottom fell further. The middle got smaller.

The national average FICO score declined to 713 in 2025, the first annual drop since 2013. Baby boomers averaged 747 and improved. Gen Z averaged 678 and fell three points in a single year. Millennials averaged 689, also down two points from 2024.

The data reflects a K-shaped recovery. Consumers with strong credit and stable incomes held ground or improved. Consumers carrying student loan debt, high-utilization balances, or adjustable-rate loans faced real bracket pressure in 2025.

Checking your score is no longer enough. Knowing which bracket you sit in, which scoring model your lender will use, and how close you are to the next tier is the information that actually shapes your financial outcomes.