Debt Validation is the formal process that allows consumers to request written proof of a debt through a Debt Validation Letter before making any payment.

Let’s imagine a scenario.

You open your mailbox, and there's a letter from a collection agency. Say, for example, NCB Management, a company you're not familiar, or you have never had any transaction with. Now your phone rings, and someone on the other end tells you that you owe $1,400, and they want it now.

Your first instinct might be to panic. Your second might be to just pay it and make the whole thing go away.

Don't do either one.

Before you hand a single dollar to any debt collector, you have a legal right to ask them to prove the debt is real, the amount is accurate, and they have the legal authority to collect it. That process is called debt validation. As a credit repair expert in Texas, I’d say it's one of the most powerful tools a consumer has when dealing with collections.

Most people have never heard of it. And debt collectors are counting on that.

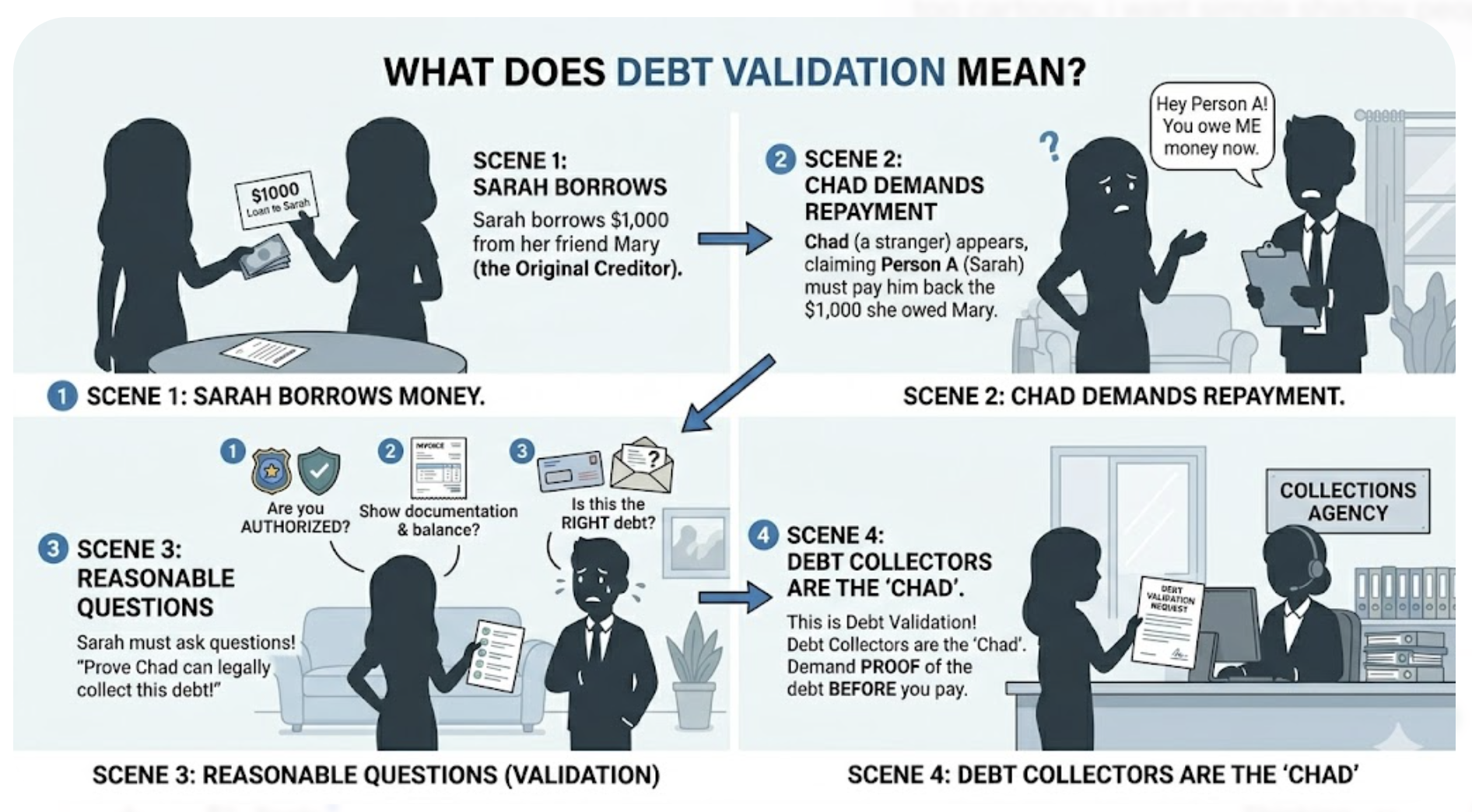

What Does Debt Validation Mean?

Debt validation is your legal right. It is protected under the Fair Debt Collection Practices Act (FDCPA), and the purpose is to demand that a debt collector prove a debt is legitimate before you pay it.

Here's the simplest way to understand it.

Let's say you borrowed money from your friend Mary a few years back. Mary is the original creditor. Time passes, life gets complicated, and one day a stranger named Chad shows up, saying you owe him the money, not Mary.

You've never met Chad. You have no agreement with Chad. So why would you just hand over money based on his word alone?

You probably wouldn't. And you'd have some very reasonable questions first:

- Is Chad legally authorized to collect this debt?

- Does Chad have documentation showing the exact balance owed? Including all interest and fees added since the original debt?

- Is this even the right debt? You remember owing money to two different people around the same time. Did you already pay one of them?

This is exactly the thought process you should apply every time a collection agency contacts you. Debt collectors are the "Chad" in this scenario. And just like you'd question Chad before paying, you have every right, and every reason, to question them too.

The bottom line of debt legitimacy is that the debt is accurate, legally enforceable, correctly calculated, and that the collector has the legal authority to collect it.

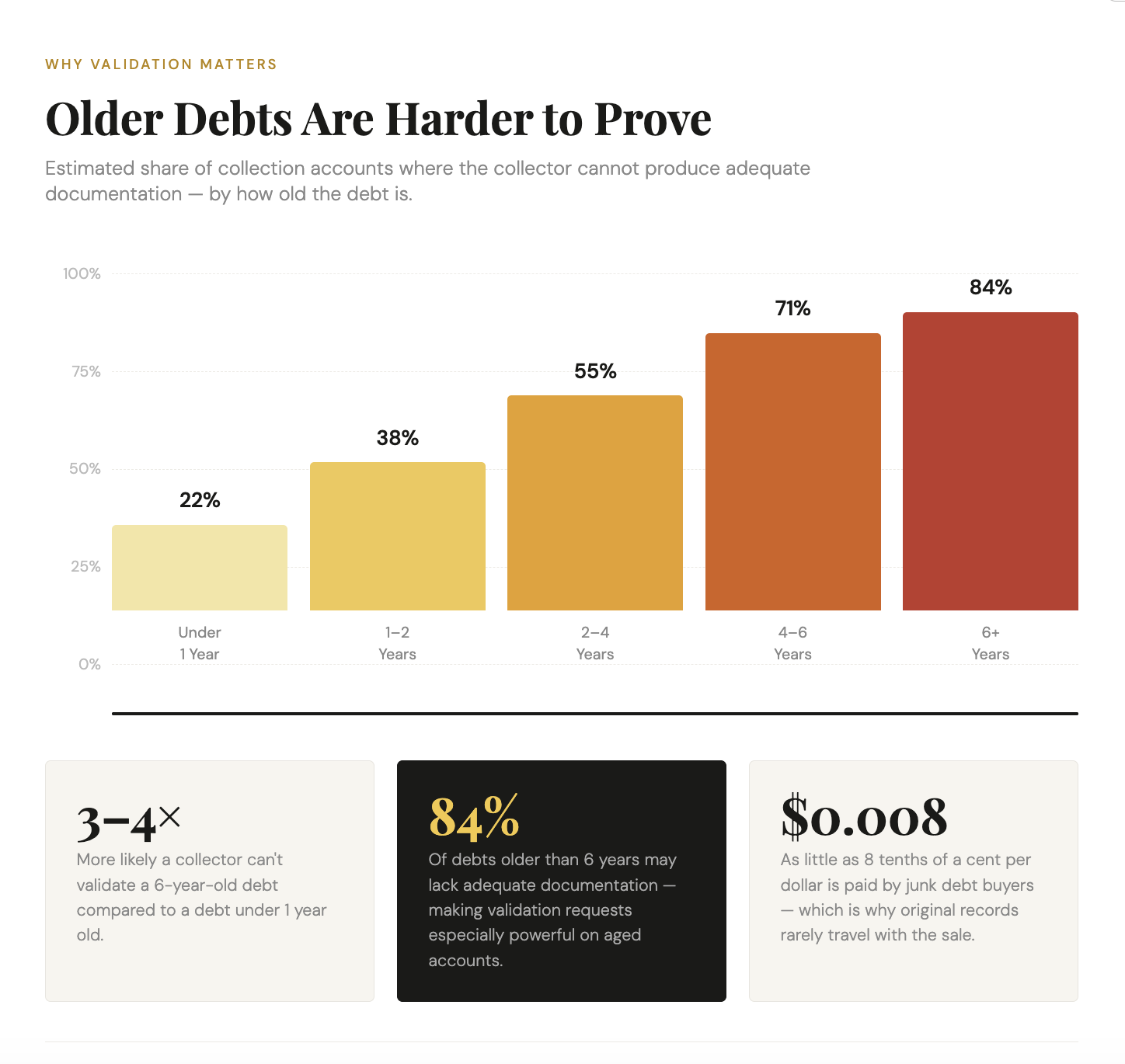

Why Debt Collectors Can't Always Prove What You Owe

This is the part that surprises most people.

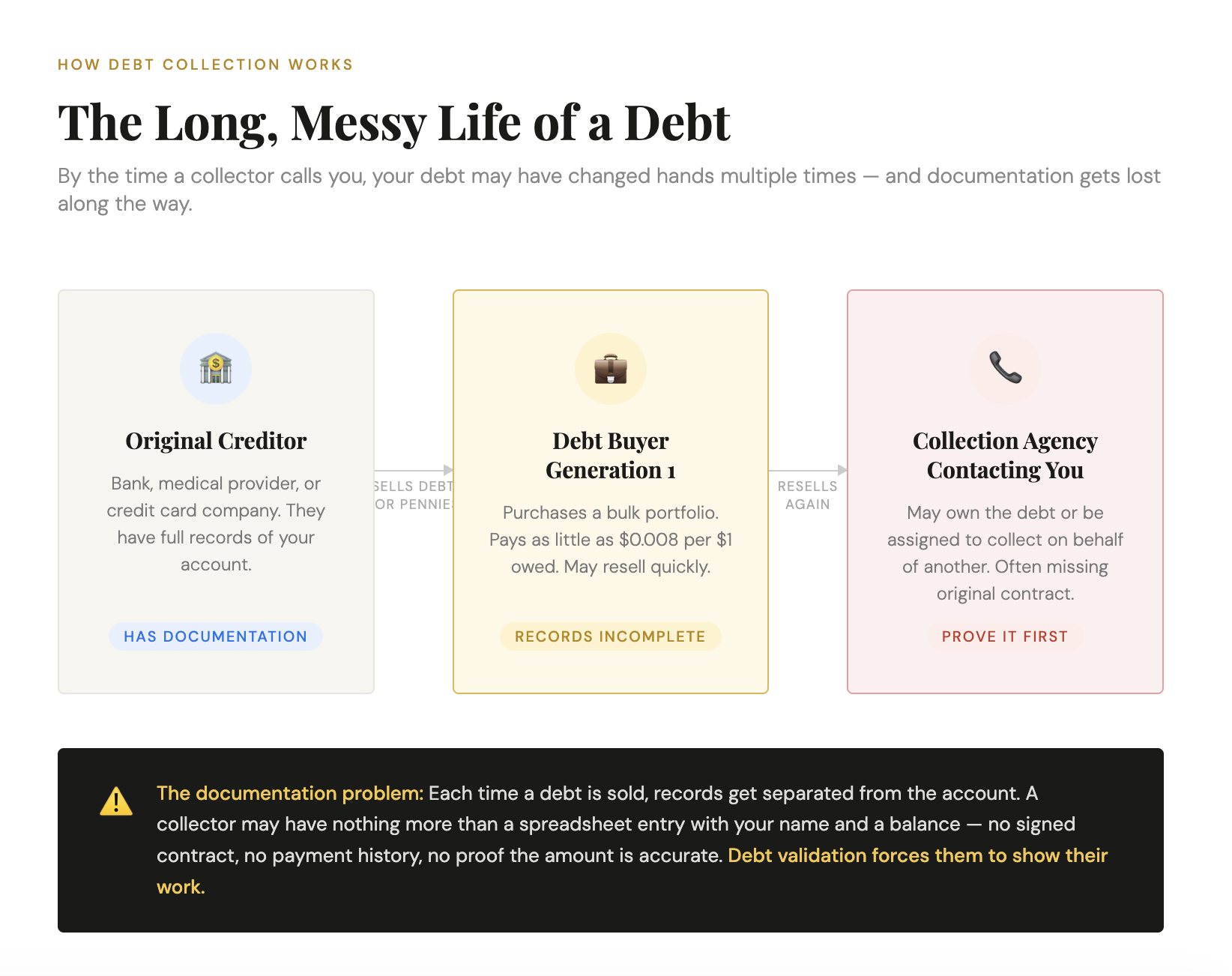

When a debt gets old, it often travels far from its origin. Original creditors, like the bank, the medical provider, or the credit card company, frequently sell old unpaid accounts to third-party companies called junk debt buyers. These companies purchase portfolios of delinquent accounts in bulk, sometimes paying less than a penny on the dollar for them.

Think about that for a second. A company like BC Services pays $0.008 for a claim that says you owe $800. They now "own" your debt. They didn't lend you money. They've never had a relationship with you. They bought a spreadsheet entry and are now trying to collect the face value of it. So that’s pure profit if they succeed.

Here's the problem with that model: documentation gets lost.

Account records get separated from the debt when it's sold. By the time a junk debt buyer contacts you, they may not have the original contract, the complete payment history, or even proof that the amount they're claiming is accurate.

That's exactly why debt validation exists. It forces collectors to show their work.

Your Rights Under the FDCPA: What the Law Actually Says

The Fair Debt Collection Practices Act gives you specific, enforceable rights when a debt collector contacts you.

Here's what matters most:

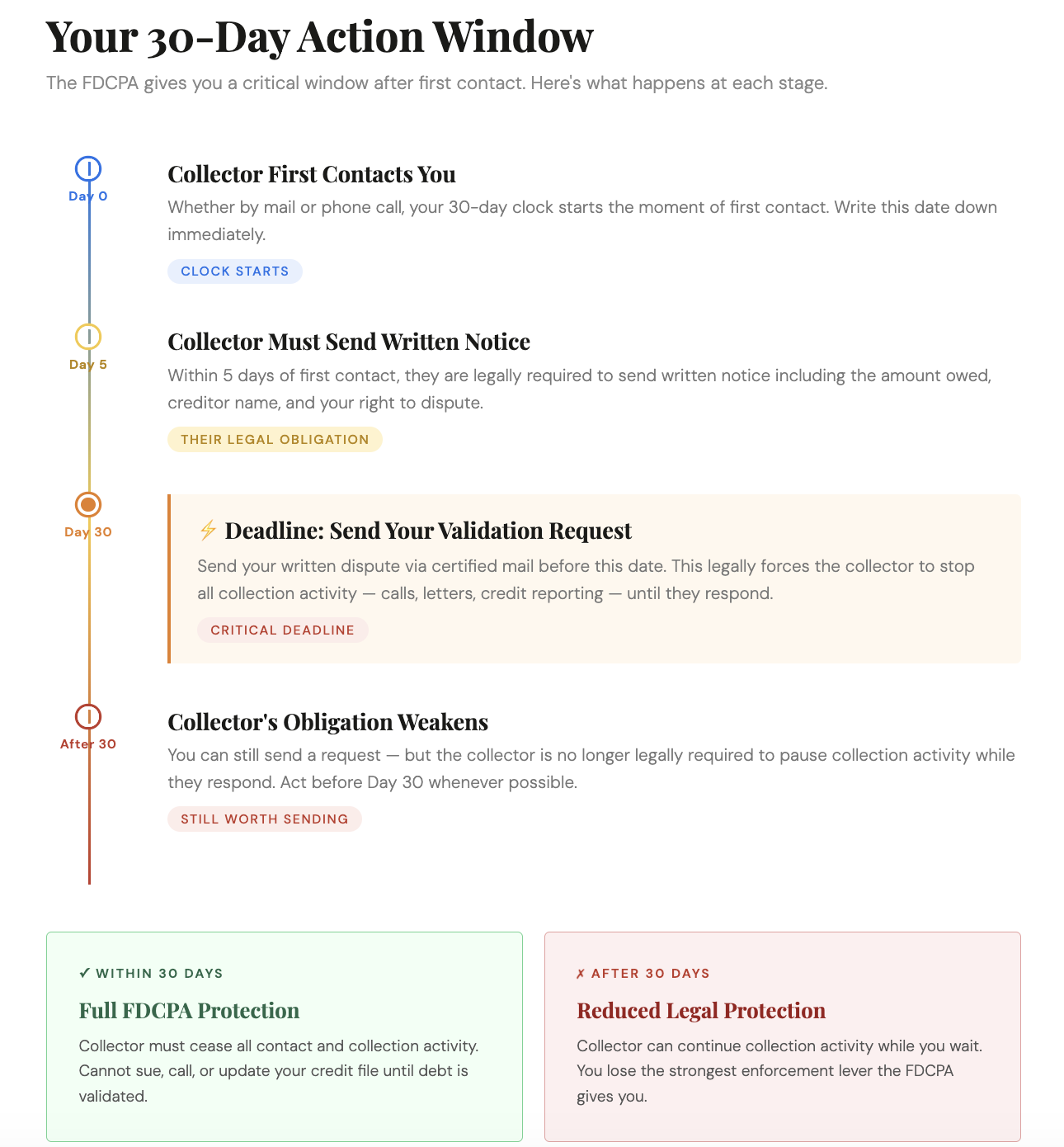

When a debt collector first contacts you, in whatever way (usually by letter or by phone), they are required to send you a written notice within five days. That notice must include the amount of the debt, the name of the creditor, and a statement that you have 30 days to dispute the debt in writing.

If you send a written dispute within that 30-day window, the collector must stop all collection activity until they provide you with verification of the debt. They cannot call you, send more letters, or report the debt to the credit bureaus as valid until they respond to your validation request.

This 30-day window is important. Mark it on your calendar the moment you receive any collection notice. If you miss it, you don't lose your right to dispute, but the collector's obligation to pause collection activity weakens significantly.

Even outside that window, you can still send a debt validation request.

Collectors aren't required to respond after 30 days, but many will. Especially if they're considering legal action, because they know that producing inadequate documentation exposes them to legal risk under the FDCPA.

What a Debt Collector Actually Has to Provide

When you request debt validation, the law sets a relatively low bar for what a collector must produce. Under current FDCPA guidelines, a debt collector can satisfy their validation obligation with:

- A statement showing the account balance that matches what they're claiming

- A list of charges that add up to the total amount demanded

- Basic information identifying the original creditor

What they do not have to provide (and this is important) is a signed contract between you and them. In most cases, no contract between you and the collection agency exists. The debt was either assigned to them by the original creditor or purchased from them outright.

Here's where assigned debt and purchased debt differ in a meaningful way:

Assigned debt means the collection agency is working on behalf of the original creditor. They don't own the debt. They're just tasked with collecting it. Legally, you don't owe the collection agency any money directly. The original creditor is still the one you'd technically owe.

Purchased debt means the collection agency bought the account from the original creditor and now owns it. They've paid for the right to collect from you. If they can produce documentation of that purchase and the original account details, they have a stronger legal standing.

The practical implication: when you request debt validation from an agency working on an assigned debt, they often struggle to produce documentation that would hold up if challenged. Because no direct contract between you and the agency has ever existed.

One exception worth knowing: some original credit agreements contain language that reads "debtor agrees to be responsible for payment of this debt to creditor or its assigns."

If a collection agency can produce a contract with that specific wording, it strengthens their legal standing to collect. But they still need to produce it, and many can't.

How to Request Debt Validation: What to Do Step by Step

Requesting debt validation isn't complicated. You don't need a lawyer. You don't need to reference specific legal statutes in your letter. Simply disputing and requesting validation is enough to demonstrate that you know your rights. However, we recommend experts to help you with this.

Here's exactly what to do:

Step 1: Don't pay and don't ignore.

The moment you receive a collection notice, resist the pressure to pay immediately. Also, resist the urge to ignore it. Ignoring a collection notice doesn't make it go away. It just limits your options.

Step 2: Note the date of first contact.

You have 30 days from the date of first written contact to send a validation request that triggers the collector's legal obligation to pause collection activity. Write that date down immediately.

Step 3: Send a written validation request by certified mail.

Your request doesn't need to be elaborate. A simple letter stating that you dispute the debt and are requesting validation is sufficient. Send it via certified mail with a return receipt requested. This creates a paper trail that proves when the request was sent and received. Keep a copy for your records.

Step 4: Wait for their response.

If they respond with adequate documentation, review it carefully. Verify that the account is yours, that the balance is accurate, and that the collector has legal standing to collect. If anything looks off, like a balance higher than you remember, an account you don't recognize, or charges that don't add up. Then you have grounds to continue disputing.

Step 5: Check your credit reports.

Pull your credit reports from Equifax, Experian, and TransUnion at AnnualCreditReport.com. If the collection account appears and the information is inaccurate (Check items about wrong balance, wrong date, wrong creditor name), you have the right to dispute the entry directly with the bureau under the Fair Credit Reporting Act (FCRA). Bureaus must investigate within 30 days.

Successfully disputed inaccuracies can be removed, which can meaningfully improve your credit score.

What Happens If the Collector Can't Validate the Debt?

If a debt collector cannot provide adequate validation, or simply doesn't respond, they are legally required to stop collection activity on that account. They cannot continue contacting you. They cannot sue you to collect. And if the account is being reported on your credit file, you have grounds to dispute the reporting as unverified.

This is not a loophole. This is the system working as intended. The FDCPA exists precisely because debt collection is an industry with a documented history of errors. Issues about wrong amounts, wrong consumers, zombie debts that have already been paid or discharged, and accounts sold so many times that the documentation trail is completely broken.

Not every collection account is legitimate. Not every balance is accurate. And not every collector who contacts you has the legal standing or documentation to actually collect what they're claiming.

Requesting validation is how you find out which situation you're in.

Recommended Read: Who Is Allied Interstate and Why Are They Calling Me?

One Thing You Don't Need to Do (That Most People Think You Do)

You do not need to cite the FDCPA or the FCRA by name in your validation request letter.

A lot of people search for dispute letter templates and assume they need to fill them with legal citations to be taken seriously. You don't. Simply requesting validation in writing, clearly identifying the debt in question, and stating that you dispute it is sufficient. Your awareness of the process itself signals to the collector that you know your rights.

It's also not your job to educate the debt collector about their own legal responsibilities. If they're unfamiliar with what the FDCPA requires of them, that's their problem.

What Debt Validation Won't Do

Debt validation is a powerful tool, but it's not magic. It's worth being direct about what it can and can't accomplish.

If the debt is valid, like the amount is accurate, the account is yours, and the collector has proper documentation, validation won't make it disappear. What it does is ensure that you only pay what you actually owe to an entity that has the legal right to collect it, with an accurate accounting of the balance.

Validation also doesn't stop the clock on the statute of limitations for debt collection lawsuits. Each state sets its own time limit on how long a creditor or collector has to sue you to collect a debt. In many states, that window is 3 to 6 years from the date of last activity. Knowing where a debt stands relative to your state's statute of limitations is important context before you decide whether to pay, negotiate, or simply wait for it to age off your credit report.

The Bottom Line on Debt Validation

You don't owe a debt collector anything. Not a payment, not a conversation, not even a response, until you've confirmed that the debt is real, the amount is accurate, and they have the right to collect it.

Debt validation is how you do that. It's free. It's legal. And it levels the playing field between you and an industry that profits from consumers who don't know their rights.

The next time Chad comes knocking, you'll know exactly what to ask.

This article provides general financial information and does not constitute professional financial or legal advice. For personalized guidance on debt collection situations, consult a licensed credit counselor or consumer law attorney.