I’m sure you heard about a FICO® 9 Score, but do you know the meaning of it? If you have been following my blogs, you know that I have a deep passion for everything that impacts your finances.

Is FICO® Score 9 being less popular than FICO® Score 8 a problem? If you're trying to understand credit scores, you've probably heard about both FICO® Score 9 and FICO® Score 8. FICO® Score 9 was supposed to be better, but it's still not as popular as FICO® Score 8. Why? Well, lenders mostly still use FICO® Score 8.

It doesn’t make sense, right? It actually does! and you’ll learn about it as we go along.

So, what's the deal with these scores, and why does it matter? We'll look into both and what they mean for your finances.

![]()

In this article, we’ll learn:

FICO® Score 9 was supposed to be better than FICO® Score 8.

But lenders still prefer FICO® Score 8.

Understanding these scores is important for managing your money.

By knowing how they affect your credit, you can make better financial decisions.

Let's figure out why FICO® Score 9 isn't as popular and what it means for you. Time to understand credit scores and take control of your finances!

Recommended: FICO Score vs Credit Score: Understanding the Key Differences for Financial Success

![]()

What are FICO® scores?

Your credit score is pretty important, right? A FICO® score is a specific type of credit score designed to assess your creditworthiness. It's a number that ranges from 300 (not great) to 850 (excellent), and it's based on stuff like your payment history, how much debt you have, and how long you've been using credit. Credit scores are numerical representations of your likelihood to repay a loan as agreed. Companies use these scores to determine your eligibility for various financial products, like mortgages or credit cards.

So how is it calculated?

FICO® Scores are calculated based on various factors from your credit report, grouped into five categories: payment history, amounts owed, length of credit history, new credit, and credit mix. While payment history carries the most weight (35%), amounts owed, length of credit history, credit mix, and new credit also contribute to your score. However, the importance of these categories can vary depending on individual credit profiles. FICO® Scores only consider information from your credit report, not other factors like income or employment history.

Payment history, amounts owed, length of credit history, credit mix, and new credit are all key components in determining your FICO® Score.

Why does this matter?

Because when you're applying for a loan or a credit card, lenders take a peek at your FICO® score to decide if you're a good risk. The higher your score, the better your chances of getting approved for that loan or card you're after.

But here's the thing, there are different versions of FICO® Scores. There are FICO® Score 9 and FICO® Score 8, each with its own way of crunching the numbers. So, if you want to understand how your credit score works and how to make it work for you, you've got to get to know FICO® scores.

![]()

Why only focus on the FICO® Score 9? Isn't more data better?

Unfortunately, there are a lot of outdated credit scoring models out there that can often lead you astray.

For example, FICO® Score 8 has been the go-to model for lenders for a while now. But just because it's familiar doesn't mean it's the best option. That’s why newer, updated and more reliable data is produced. FICO® Score 9 is designed to be more accurate and fairer than its predecessor. It's like giving your credit score a much-needed upgrade.

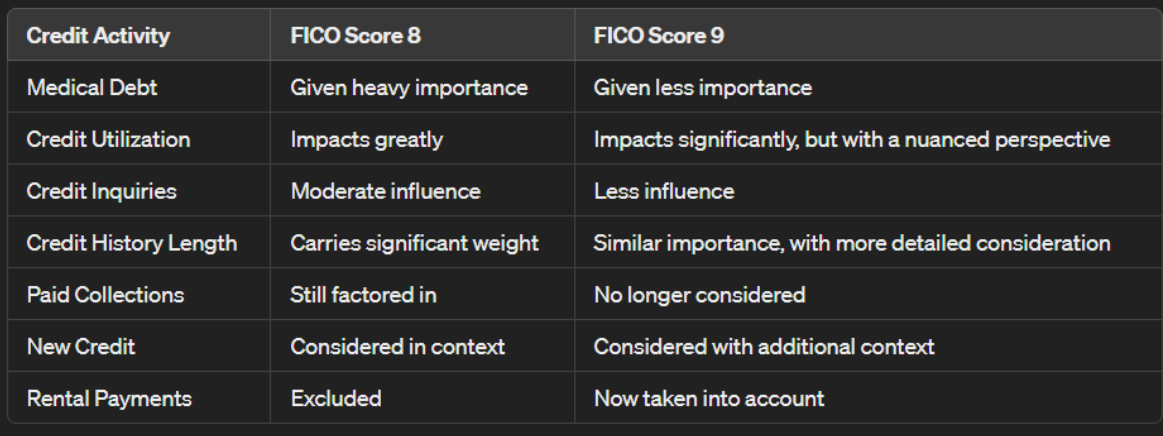

So, what's changed? Well, for starters, FICO® Score 9 takes a closer look at your medical debts and rental history. It's like shining a spotlight on areas that were previously overlooked. And when you dive into the specifics of FICO® Score 9, you'll see why it's gaining traction:

- Evaluating Collection Accounts: It disregards paid collections, reducing the negative impact on scores for those who’ve settled their debts.

- Treatment of Medical Collections: Medical debt is given less weight, acknowledging that such financial burdens might not reflect true creditworthiness.

- Updated Scoring Model: The model has been refined, especially benefiting individuals with limited credit history, thereby enabling lenders to make more informed decisions.

However, it’s worth noting that not all lenders have jumped on the FICO® Score 9 bandwagon yet. Some are still sticking with FICO® Score 8, even though it might not give you the full picture of your creditworthiness.

So, do you still want to focus on FICO® Score 9? Absolutely, since it's the future of credit scoring. But always remember that it's not the only metric that matters. It's just one piece of the puzzle regarding understanding your credit health.

Great Read: does transworld systems report to credit bureaus

![]()

How do FICO® Score 9 changes affect you?

FICO® Score 9 got some upgrades to make it better at judging how trustworthy you are with credit.

The updates to FICO® Score 9 are meant to help you with your score. One big change is that it's not as harsh on your credit if you've had medical bills you couldn't pay. This could be good news if you've struggled with medical debts.

These updates aren't just about being fair—they're also about giving you a better chance at improving your credit score. So, if you're aiming for a higher score or just want a fairer shake in the credit game, these changes could be good news for you.

But there are some things to think about. While it's nice that medical bills won't hurt your credit as much, some people worry that it might make lenders think you're less risky than you actually are. This could cause problems down the line if you cannot pay back what you owe.

Also, while FICO® Score 9 is supposed to be fairer, it might not make a big difference for people who already manage their credit well. On the other hand, it could help people who haven't been as good with their credit in the past.

So, while the changes to FICO® Score 9 sound good, it's important to think about both the good and the bad before you count on them to improve your credit.

![]()

Why does FICO® score 8 stay on top?

Even with the improvements of FICO® Score 9, FICO® Score 8 remains king, being used in over 90% of lending decisions in the U.S. This loyalty to FICO® Score 8 highlights the importance of understanding its impact on credit decisions and why lenders stick with it.

Below is a detailed comparison of FICO® Score 8 and FICO® Score 9 and how it impact your creditworthiness:

Understanding why lenders prefer FICO® Score 8 comes down to its proven track record in assessing credit risk and the industry's familiarity with it. We’ll go into detail about this topic in the next section.

![]()

A closer look at why lenders prefer FICO® 8 scoring models.

Lenders prefer FICO® Score 8 mainly because of its proven track record in assessing credit risk and the industry's familiarity with its system. Its consistent performance and reliability across different evaluations have built a strong level of trust that's not easily shaken. Despite the improvements brought by FICO® Score 9, the inertia within the industry and the challenges of transitioning to a new model keep FICO® Score 8 as the top choice for lenders.

Let’s break down why FICO® Score 8 is still the favorite among lenders, even though FICO® Score 9 exists:

Everyone's Used to It: FICO® Score 8 has been around for a while, so lenders are familiar with how it works. They trust it because it's been proven over time.

It Works Well: FICO® Score 8 has a good track record of predicting whether someone will pay back a loan on time. Lenders like that kind of reliability.

Switching is a Hassle: Changing to a new scoring system like FICO® Score 9 can be a pain for lenders. It means updating their systems and training their staff. Many prefer to stick with what they know.

It's Accurate Enough: FICO® Score 8 might not be perfect, but it's good enough for most lenders. They don't see a big enough benefit in switching to FICO® Score 9.

It Meets the Rules: Lenders have to follow certain rules when they decide who to lend money to. FICO® Score 8 meets those rules, so lenders are happy to keep using it.

In a nutshell, FICO® Score 8 is like the old, reliable car that everyone's used to driving. Even though there are newer models out there, sometimes sticking with the familiar just makes sense.

It's worth noting, however, that FICO® Score 10, the latest version, promises even better predictive accuracy than its predecessors.

![]()

FICO® Score 9: The Future Ahead

While FICO® Score 9 is gaining traction, it's still a slow journey to replace FICO® Score 8. Its new approach, especially with medical collections, is a positive step. However, challenges like logistics and costs slow down the transition. The credit industry's willingness to embrace this model and how well it works will determine its success.

![]()

Medical collections and rent payments: FICO® Score 9's changes

FICO® Score 9 is unique because it looks at things like medical bills in collections and whether you pay your rent on time when calculating your credit score. So, if you've been responsible with your rent payments, your score might get a boost. Another important change is how it handles paid-off collection accounts. With FICO® Score 9, if you've settled a debt that was in collections, it won't drag down your score as heavily. These updates paint a clearer picture of how trustworthy you are with credit.

![]()

Enhancing your FICO® score 9

Improving your FICO® Score 9 doesn't have to be complicated. It's all about making wise financial decisions, such as paying your bills promptly and not using up all your available credit. Your rental payment history also matters, so ensuring you have a solid record there can positively impact your score. Additionally, regularly checking your credit report for any inaccuracies is crucial. By staying vigilant, you can prevent errors from lowering your score and take steps toward enhancing your creditworthiness.

![]()

Understanding the loyalty of lenders towards FICO® Score 8

So Joe, the FICO® Score 9 looks more fair to me, why do lenders love FICO® Score 8 so much?

Well, it's been around the block and has a solid track record of predicting credit risk. Lenders know what to expect with FICO® Score 8, which is why it's still the go-to for many of them. Even though FICO® Score 9 offers some cool updates, like being more forgiving with medical debts, it's taking time for lenders to warm up to it. Plus, switching over to a new scoring model is no small feat for the industry.

![]()

Potential pros and cons if FICO® Score 9 is widely adopted

If FICO® Score 9 becomes the new norm, it could shake up the credit game in some interesting ways. For one, it might make it easier for folks with medical debts to get approved for credit. But there are also some hurdles to clear, like making sure lenders are on board and ironing out any kinks in the scoring model. Here’s my personal take on looking at the issue:

Pros:

Medical Bills Easier to Manage: FICO® Score 9 might make it easier for people with medical bills to get credit.

Fairer Decisions: FICO® Score 9 could make credit decisions fairer for everyone.

More Access to Loans: People who had money troubles before might find it easier to get loans.

Quicker Approvals: Lenders might approve loans faster because they understand credit better.

Paid Debts Matter Less: If you paid off a debt, it might not hurt your score as much with FICO® Score 9.

Cons:

Lenders Might Wait: Some lenders might take a while to use FICO® Score 9, so you might have to wait.

Setting It Up is Hard: It's not easy for all banks to use the new score, so it could take time.

Some Lenders Might Stick to Old Ways: Some banks might not want to change how they do things.

It Can Be Confusing: FICO® Score 9 might be hard to understand for some people.

We Might Not Know Everything: There could be unexpected problems with the new score that we don't know about yet.

![]()

Frequently Asked Questions

Still have questions about FICO® Score 9? You're not alone. Here are some answers to common questions:

Is FICO® 8 or FICO® 9 better?

Both have their pros and cons. FICO® Score 9 is more forgiving with medical debts, but FICO® Score 8 is still the gold standard for many lenders.

Where can I get a FICO® Score 9?

You can usually find it through major credit bureaus or some financial institutions. Just keep in mind that not all lenders use this model for credit decisions.

FICO® 8 vs. FICO® 9: Which is usually higher?

It depends on your credit history and financial situation. FICO® Score 9 might be higher for some people, while others might see a higher score with FICO® Score 8.

Are lenders using FICO® Score 9 now or older versions?

Many lenders still rely on FICO® Score 8, but FICO® Score 9 is gaining traction. Always check with lenders to see which model they use.

![]()

Ways To Boost Your Credit Score, No Matter What Scoring Model You Use

Your credit score is an important number that lenders use to determine your creditworthiness. A higher credit score can lead to better interest rates and more favorable loan terms, while a lower score can limit your borrowing options and cost you more in interest charges. Whether your credit score is calculated by FICO Score 8, FICO Score 9, or any other scoring model, there are universal strategies you can employ to improve it.

Here are some tips to get started:

- Make Payments on Time: Late payments can have a significant negative impact on your credit score. Set up automatic payments or reminders to ensure you never miss a due date.

- Keep Credit Utilization Low: Your credit utilization ratio is the amount of credit you use compared to your credit limit. Aim to keep your utilization ratio below 30% to improve your score.

- Check Your Credit Report: Errors on your credit report can drag down your score. Check your report regularly to ensure all the information is accurate and up-to-date.

- Don't Close Old Accounts: Closing old credit card accounts can hurt your score by reducing your available credit and shortening your credit history. Instead, use them occasionally and pay them off in full.

- Limit New Credit Inquiries: Every time you apply for credit, a hard inquiry is added to your credit report, which can lower your score. Try to limit your applications for new credit to avoid too many inquiries.

By following these tips, you can improve your credit score and increase your chances of getting approved for loans and credit cards with better terms and rates. Remember, building good credit takes time, but the benefits are worth the effort.

If you are interested in learning more tips, read here.

![]()

Understanding these scores is important for managing your money.

In summary, knowing how credit scores like FICO® Score 9 and FICO® Score 8 work is essential for managing your money wisely. Although FICO® Score 9 was meant to be better, most lenders still stick with FICO® Score 8 because they trust it more. Understanding these differences can help you make smarter financial decisions.

Despite the differences between these scoring models, the underlying principle remains the same: your credit score impacts your financial opportunities and significantly affects your ability to access credit on favorable terms. By comprehending how these scores are calculated and the factors that influence them, you can make informed decisions to improve your creditworthiness and secure better financial outcomes.

Whether you're aiming to boost your credit score, navigate the complexities of credit decisions, or understand the potential implications of changes in credit scoring models, staying informed and proactive is key. By implementing sound financial habits and utilizing strategies to enhance your credit profile, you can pave the way towards a more secure financial future.

Ready to take control of your credit score and unlock better financial opportunities? Contact ASAP Credit Repair today to discover how our expert team can help you navigate the complexities of credit scoring models like FICO® Score 9 and FICO® Score 8. With personalized strategies and dedicated support, we'll work together to improve your credit profile and achieve your financial goals.

Don't let credit challenges hold you back – reach out to ASAP Credit Repair and start your journey towards a brighter financial future today!