How Fast Can I Delete a Negative Collection Item From Credit Report

A negative collection item can seriously damage your credit score, but the good news is that it may not have to stay there for years. If you are wondering how fast you can delete a negative collection item from your credit report, the answer often depends on accuracy, verification, and how the account is reported.

In many cases, collections that contain errors or cannot be properly verified can be removed within 30 to 45 days through the dispute process.

Understanding your rights and taking the right steps early can significantly speed up credit report cleanup and help you move toward better credit faster.

How To Remove Negative Collection Items

Here are four ways to remove collections faster and what actually determines your timeline.

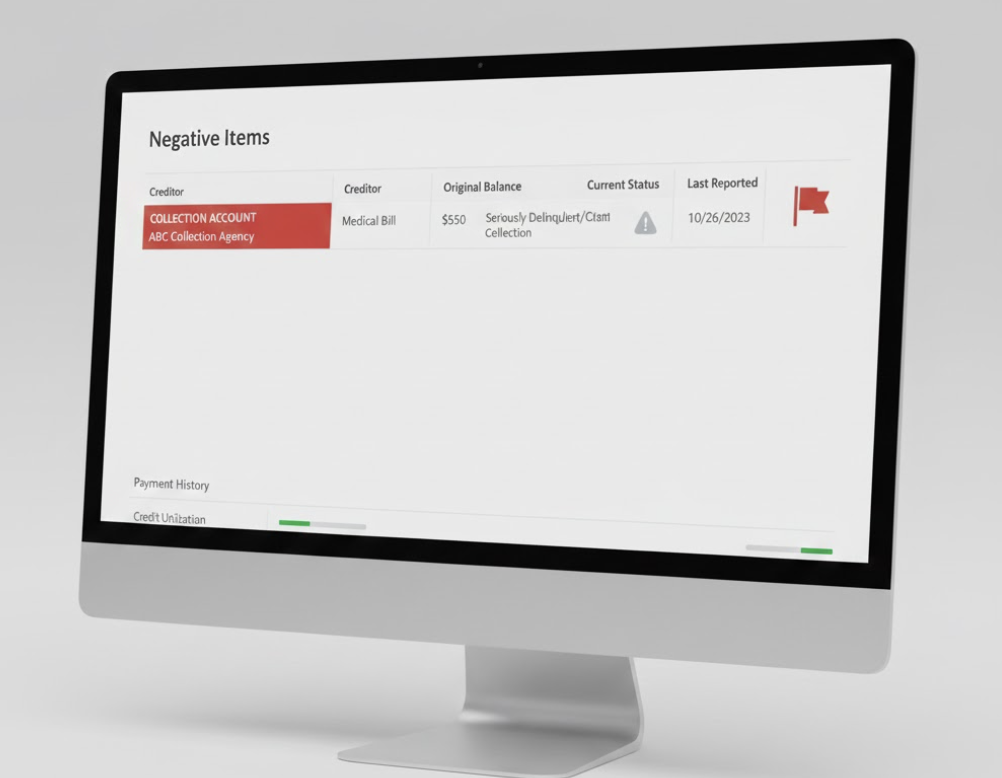

Does it feel like that negative collection item is never going away? You aren't imagining it. Collections can stay on your credit report for seven years, dragging down your score and blocking approvals.

To remove them faster, you need to act strategically – not desperately.

The good news: you don't need to wait seven years or hire expensive credit repair companies. With the right approach, you can challenge inaccurate collections, negotiate deletions, or wait out removals in months instead of years.

A negative collection item hurts your credit because it signals unpaid debt to lenders. That means missed payments, ignored accounts, and financial instability. By addressing these marks directly, you increase the chances your score improves, your report cleans up, and your creditworthiness recovers.

This shift from hoping collections disappear to actively removing them matters because credit bureaus and collection agencies operate on timelines you can influence. Instead of passively waiting, you can dispute errors, negotiate pay-for-delete agreements, and force verification that many collectors can't provide.

Credit repair isn't magic, but action is faster than inaction. As reporting cycles continue, taking control of collection removal becomes more critical than simply ignoring the problem.

What you need to do now

You don't need to hire a credit repair service to remove a negative collection item. Collection removal relies on verification rules, dispute rights, and negotiation tactics you can execute yourself.

1. Dispute inaccurate or unverifiable collections immediately

Credit bureaus are required to investigate disputes within 30 days. When you dispute a negative collection item, the bureau contacts the collection agency to verify the debt. If the collector can't provide adequate proof – wrong dates, incorrect amounts, or missing documentation – the bureau must remove it.

Many collection agencies, especially those that purchased old debt, lack complete records. Disputing forces them to prove accuracy. If they can't, the collection disappears from your report within 30-45 days.

How to dispute effectively:

- File disputes directly with all three credit bureaus (Equifax, Experian, TransUnion).

- Be specific about what's wrong: incorrect balance, wrong date of delinquency, not your account.

- Include supporting documentation if you have it.

- Follow up if the dispute drags past 30 days.

This method works fastest when the negative collection item contains errors or the agency can't validate their claim.

2. Negotiate pay-for-delete agreements in writing

If the collection is accurate, disputing won't work. But you still have leverage: collectors want to get paid.

A pay-for-delete agreement means you pay the debt (often for less than the full amount) in exchange for the collector removing the negative item from your credit report. Not all agencies agree to this, but many will – especially if the debt is old or they bought it for pennies on the dollar.

How to negotiate pay-for-delete:

- Contact the collection agency and ask if they'll remove the item in exchange for payment.

- Get the agreement in writing before you pay anything.

- Negotiate the amount down if possible – start at 30-40% of the balance.

- Pay only after you have written confirmation they'll delete the tradeline.

- Keep all documentation in case they don't follow through.

Pay-for-delete can remove a negative collection item within 30-60 days after payment, depending on when the agency reports the deletion to the bureaus.

Important: paying a collection without negotiating deletion usually won't improve your score if you're using older FICO models, which still count paid collections as negative. Always get deletion in writing first.

3. Wait for automatic removal at seven years

Collections fall off your credit report automatically after seven years from the date of first delinquency – not from when the collection agency took over the account.

If a negative collection item is already five or six years old, waiting might be faster than disputing or negotiating. The impact on your score also decreases as the item ages, especially if you've built positive credit history since then.

How to track automatic removal:

- Check the "date of first delinquency" on your credit report.

- Calculate seven years from that date.

- Monitor your report around the removal date to confirm it drops off.

- Dispute if the item remains past seven years.

This timeline is fixed. Collections can't legally stay on your report beyond seven years, even if the debt is unpaid. If you're close to that mark, patience might be the fastest path.

4. Use the right-to-deletion for newer FCRA rules

Under the Fair Credit Reporting Act, you have the right to dispute inaccurate information. Recent updates to reporting standards also mean that medical collections under $500 no longer appear on credit reports, and paid medical collections are removed immediately.

If your negative collection item is medical debt, check whether it qualifies for automatic removal under these rules. Even non-medical collections may be removable if they violate reporting accuracy standards.

What qualifies for faster removal:

- Medical collections under $500.

- Paid medical collections of any amount.

- Collections with incorrect information (wrong amount, wrong creditor, identity errors).

- Collections that appear on your report but not in the collector's records.

These removals can happen within 30 days if you dispute properly and the collection meets removal criteria.

How fast is realistic?

The speed of negative collection item removal depends entirely on your situation:

Inaccurate collections disputed successfully: 30-45 days.

Pay-for-delete negotiated and executed: 30-60 days after payment and deletion reporting.

Automatic seven-year removal: Instant once the timeline expires.

Medical debt under new rules: Immediate to 30 days.

You can't force instant removal of accurate collections unless you negotiate deletion. But you can push timelines to their fastest possible resolution by disputing aggressively, negotiating smartly, and understanding which rules work in your favor.

Want to go deeper?

If you're ready to tackle negative collection items with a clear plan, track your disputes systematically, and monitor your credit report for changes, start by pulling your reports from all three bureaus. Identify every collection, verify accuracy, and decide whether to dispute or negotiate.

It's your credit report. Taking control of what's on it is faster than waiting and hoping.