If you’ve spotted "Criterion Collection" on your credit report, you're probably confused — and maybe a little worried. Criterion Collection is not a scam or a mistake. It's a debt collection agency that often works on behalf of original creditors in sectors like healthcare, utilities, or unpaid service bills.

They buy or are assigned your debt and then report it to the major credit bureaus — Experian, Equifax, and TransUnion — to pressure you into paying.

But here’s the problem: even if the debt is legit, collection accounts can tank your credit score, especially if they’re recent or unpaid.

Let’s understand more about this debt collection item on your credit report.

Disclaimer: This article provides general information and should not be construed as legal advice. For guidance specific to your situation, consult with a qualified attorney or financial advisor. Any mention of companies or organizations, including debt collectors, is based on publicly available information and does not imply misconduct or wrongdoing on their part. Our intention is not to discredit any entity, but to provide readers with helpful guidance on navigating common credit reporting issues in a responsible and informed way.

What is Criterion Collection?

Criterion Collection is a debt collection agency that purchases unpaid debts from original creditors like banks, credit card companies, and loan providers. When you see Criterion Collection on your credit report, it means they've acquired the rights to collect on a debt you allegedly owe. While the name might sound like a film distributor (don’t worry — it’s a different company), this Criterion Collection is focused entirely on debt recovery.

Headquarters: Often listed in various states, depending on operational branches. Common filings are seen in California and Illinois.

Founded in 1983, Criterion Collection operates nationwide and specializes in collecting various types of consumer debt, Specializes In:

- Consumer loans

- Healthcare or medical debt

- Credit cards

- Auto loan deficiencies

- Utility and telecom bills

They often buy debt portfolios from banks and service providers for a fraction of the balance — sometimes as low as 3 to 10 cents on the dollar. That’s why they’re often willing to settle for less than the full amount if it means closing the account.

Is Criterion Collection legitimate?

Yup, you bet they are!

While Criterion Collection is a real debt collection agency, their Better Business Bureau (BBB) rating typically sits at a B- or lower. This rating often reflects the volume of complaints received and the number of unresolved issues. Notably, Criterion Collection is not BBB accredited.

Common consumer complaints reported about Criterion Collection include:

- Attempting to collect on debts that consumers believe have already been paid.

- Reporting inaccurate information about accounts to credit bureaus.

- Failure to provide proper debt validation when requested by consumers.

- Employing aggressive or excessively persistent phone calls.

- Ignoring consumer disputes or taking an extended period to respond to them.

Why Does Criterion Collection Appear on Your Credit Report?

Criterion Collection will appear on your credit report when:

📍You have an unpaid debt: An original creditor has given up trying to collect payment from you and sold your account to Criterion Collection.

📍They've reported the debt: After acquiring your debt, Criterion Collection has reported the collection account to one or more credit bureaus (Experian, Equifax, and TransUnion).

📍The debt is being pursued: Criterion Collection believes you owe money and has initiated collection activities against you.

It's important to note that Criterion Collection's appearance on your credit report creates what's known as a "collection account," which is considered a negative item that can significantly damage your credit score.

Recommended Article: Capio Partners on Credit Report: 5 Proven Ways To Delete it

Why Is It Important to Remove Criterion Collection Accounts?

Even one collection account can drop your score by 50–100 points or more. And it doesn't stop there:

- It lowers your chances of getting approved for a mortgage or auto loan.

- It can cause you to pay higher interest rates on everything from credit cards to insurance.

- It stays on your credit report for up to 7 years, even if you pay it.

- Employment and housing challenges: Since many employers and landlords check credit reports, collection accounts could impact job and housing opportunities.

So, whether the debt is valid or not, you have options — and I’ll walk you through them.

7 Effective Ways to Remove Criterion Collection from Your Credit Report

1. Verify the Debt is Yours

Before taking any action, confirm that the debt legitimately belongs to you:

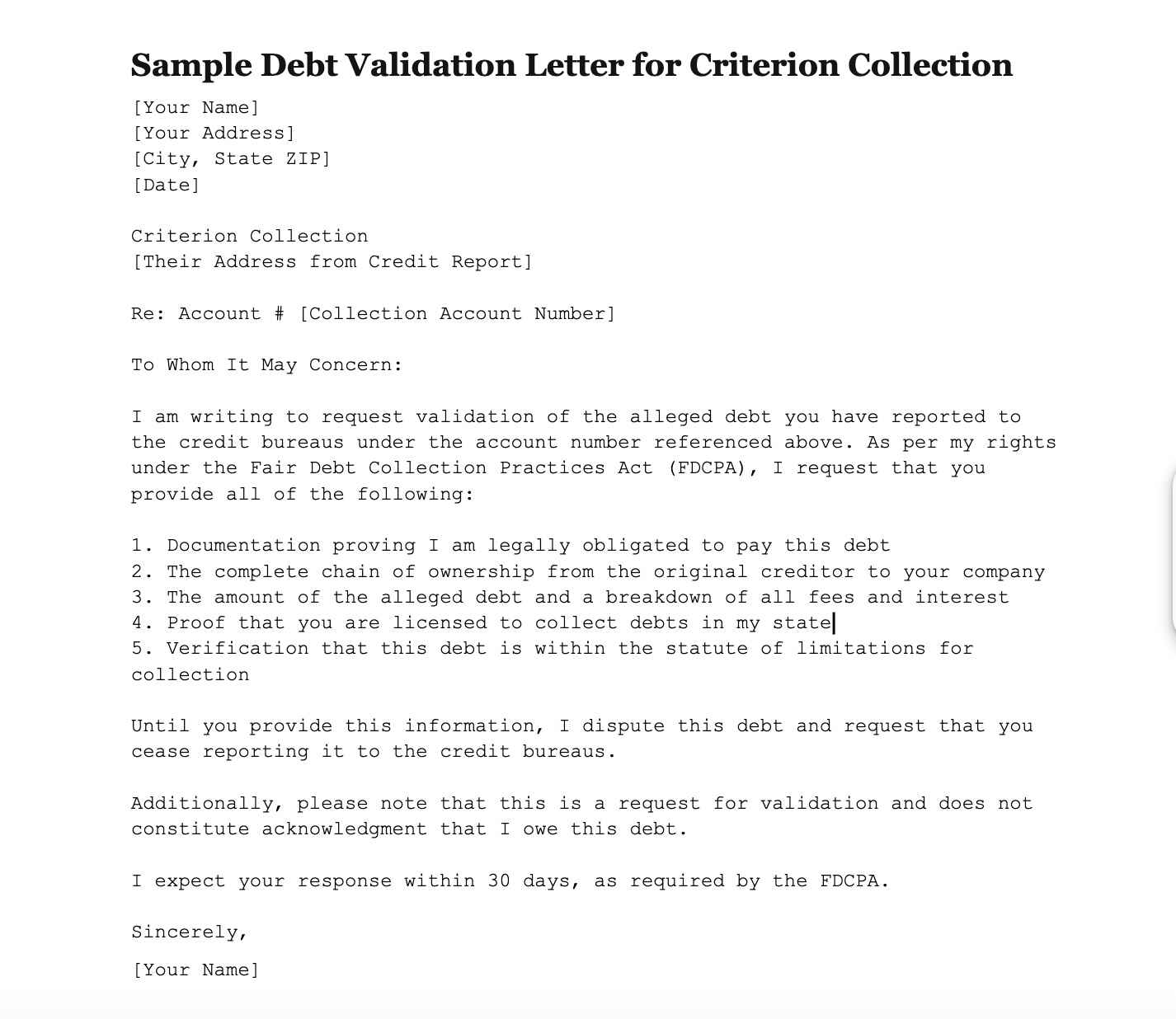

- Request debt validation: Within 30 days of Criterion Collection's first contact, send a debt validation letter asking them to prove you owe the debt.

- Check for errors: Verify all details including the amount, dates, and account information. Collection agencies frequently make mistakes.

- Look for time-barred debts: Each state has a statute of limitations on debt collection. If your debt is older than this limit, Criterion Collection may not be able to legally sue you for payment.

2. Dispute Inaccurate Information

If you find errors in Criterion Collection's reporting:

- File disputes with all credit bureaus: Submit detailed disputes to each bureau showing the Criterion Collection entry, explaining specifically what information is incorrect.

- Provide supporting documentation: Include any evidence that supports your claim, such as payment records or identity theft reports.

- Follow up consistently: Credit bureaus must investigate disputes within 30 days. If they don't respond or fail to correct legitimate errors, follow up with additional correspondence.

Related Story: Lakeside Collections: Why Is It on My Credit Report?

3. Negotiate a Pay-for-Delete Agreement

One of the most effective strategies is negotiating a pay-for-delete arrangement:

- Offer a partial payment: Contact Criterion Collection and propose paying a portion of the debt in exchange for complete removal from your credit report.

- Get the agreement in writing: Never rely on verbal promises. Insist on a written agreement that clearly states they will remove the collection from all credit bureaus upon receiving your payment.

- Use certified mail: Send your payment with return receipt requested so you have proof of delivery.

- Verify removal: Check your credit reports 30 days after payment to ensure the item has been removed.

4. Request Goodwill Deletion

If you've already paid the debt but the collection remains on your report:

- Write a goodwill letter: Explain any extenuating circumstances that led to the debt (job loss, medical emergency, etc.) and request removal as a gesture of goodwill.

- Emphasize your positive payment history: Highlight your otherwise good credit history and commitment to financial responsibility.

- Be polite and respectful: A courteous approach is more likely to yield positive results than confrontational language.

5. Wait Out the Reporting Period

If other methods fail:

- Monitor your credit: The Criterion Collection entry should automatically fall off your credit report after 7 years.

- Build positive credit: Focus on establishing positive credit entries to offset the negative impact of the collection account.

6. Seek Professional Help

Consider professional assistance if you're struggling:

- Credit repair companies: These organizations specialize in challenging negative items on credit reports (though be cautious of scams).

- Consumer law attorneys: Lawyers specializing in Fair Debt Collection Practices Act (FDCPA) violations can help if Criterion Collection has engaged in illegal collection practices.

Need expert help removing Criterion Collection from your credit report?

ASAP Credit Repair specializes in helping consumers dispute collection accounts and improve their credit scores quickly. Our team has successfully removed thousands of Criterion Collection entries and can guide you through the entire process. Contact ASAP Credit Repair today for a free consultation and take the first step toward financial freedom!

7. Submit a Complaint to Regulatory Agencies

If Criterion Collection violates your rights:

- File with the CFPB: The Consumer Financial Protection Bureau accepts complaints about debt collectors and can help mediate solutions.

- Contact your state's attorney general: Many states have additional protections for consumers against aggressive collection practices.

Legal Rights When Dealing with Criterion Collection

When interacting with Criterion Collection, remember that you're protected by federal law:

- Fair Debt Collection Practices Act (FDCPA): Prohibits debt collectors from using abusive, deceptive, or unfair practices.

- Fair Credit Reporting Act (FCRA): Gives you the right to dispute inaccurate information on your credit report.

- Telephone Consumer Protection Act (TCPA): Restricts how and when debt collectors can contact you by phone.

Learn more about these rights here.

Criterion Collection must respect these laws, including limitations on:

- Calling before 8 AM or after 9 PM

- Contacting you at work if you've told them not to

- Discussing your debt with unauthorized third parties

- Using threatening or abusive language

- Making false statements about consequences of non-payment

Prevention Tips: Avoid Future Collection Accounts

To prevent Criterion Collection or other debt collectors from appearing on your credit report in the future:

- Set up payment reminders: Use calendar alerts or banking apps to notify you when bills are due.

- Establish automatic payments: For fixed expenses, automatic payments ensure you never miss a due date.

- Create an emergency fund: Having 3-6 months of expenses saved can help you weather financial hardships without falling behind on bills.

- Address financial problems early: If you're struggling to make payments, contact original creditors immediately to discuss hardship programs or payment plans.

- Check credit reports regularly: Monitor your credit reports to catch issues early, before they're sent to collections.

Being proactive about your financial health is the best defense against collection accounts. Even small steps toward better financial management can make a significant difference in preventing future issues with companies like Criterion Collection.

Removing Criterion Collection on Credit Report is Possible!

Having Criterion Collection on your credit report can be stressful and damaging to your financial health, but you have multiple strategies to address the situation. By understanding your rights and following the steps outlined above, you can work toward removing this negative item and restoring your credit.

Remember that persistence is key when dealing with collection agencies. Document all communications, follow up consistently, and don't hesitate to escalate matters to regulatory agencies if necessary. With diligence and the right approach, you can successfully remove Criterion Collection from your credit report and move forward with improved financial standing.

Why tackle this challenge alone? If you're facing difficulties with Criterion Collection on your credit report, ASAP Credit Repair has the expertise and resources to help. Contact us today to schedule your complimentary credit assessment and discover how we can help restore your financial reputation.