Grant and Weber is a debt collection agency that collects unpaid debts for original creditors. If their name appears on your credit report, it usually means an account has gone to collections. This guide explains exactly who they are, what they can do, and how to remove them.

Grant and Weber · Debt Collection · Credit Report · Consumer Rights

Grant and Weber on your credit report means a debt has been sent to collections. Before you call them back or pay anything, here is exactly who they are, what they can do, and how to get them removed.

Updated March 2026 · 9 min read · Sources: CFPB Complaint Database, BBB, FDCPA, FCRA

Grant and Weber on Your Credit Report: Grant and Weber is a debt collection agency that collects unpaid debts for original creditors. If they appear on your credit report, it usually means an account has been sent to collections. Grant and Weber is headquartered in Calabasas, California and has been in business since 1977. They specialize primarily in healthcare debt and report collection accounts to all three major credit bureaus.

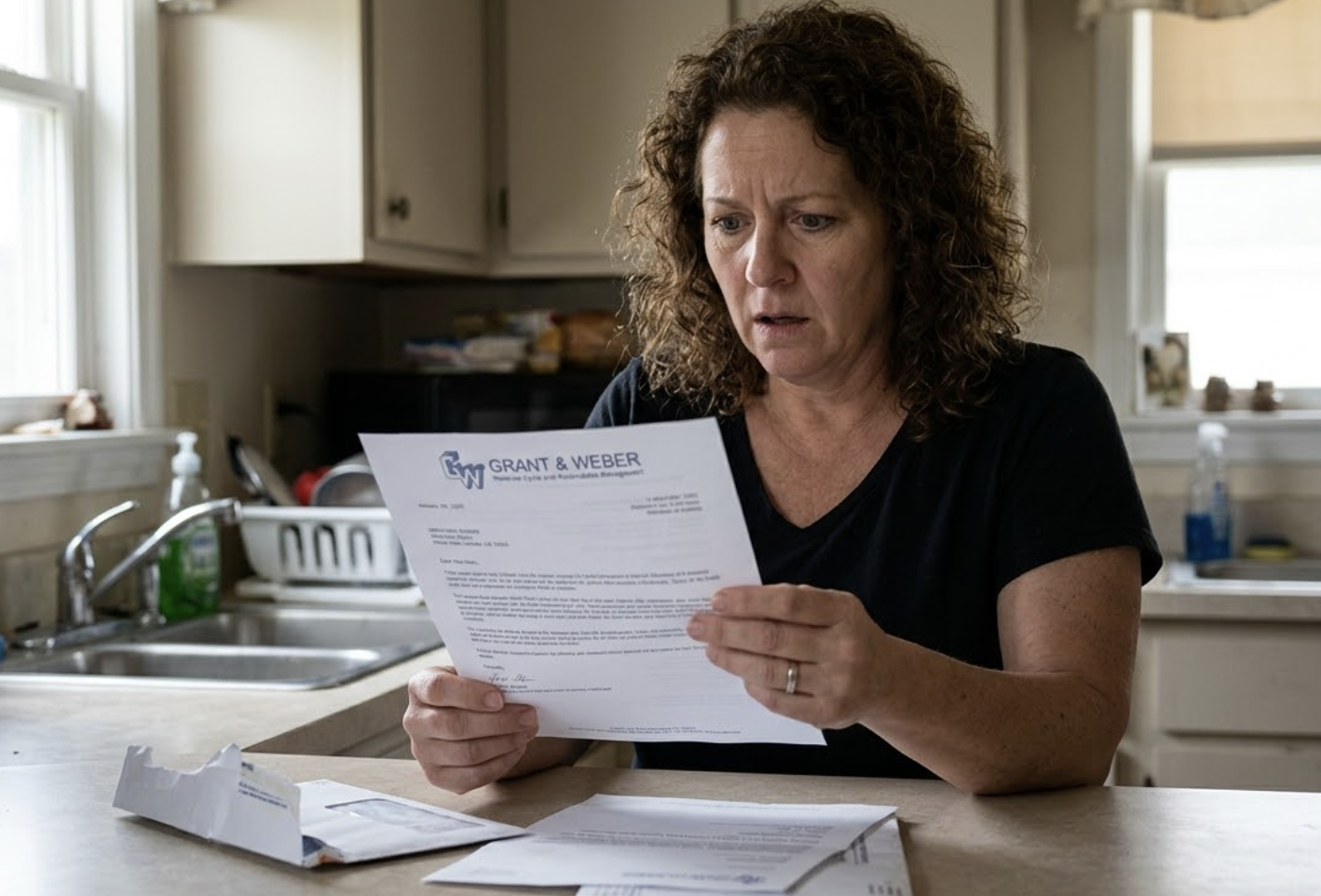

A client came to us frustrated. Grant and Weber had appeared on his credit report for a $618 hospital bill from over three years earlier. The hospital had been paid by his insurance. But a balance dispute between the provider and insurer had quietly sent a residual amount to collections without anyone notifying him. Grant and Weber reported it. His score dropped 71 points.

At ASAP Credit Repair USA, we see Grant and Weber on client reports regularly. They are one of the more aggressive medical debt collectors. Their CFPB complaint volume is significant and their BBB rating is an F. That does not make them a scam. It does mean you need to be careful about what you say to them, what you pay them, and when.

This guide covers everything about Grant and Weber: who they are, what they collect, whether you have to pay, and exactly how to remove them from your credit report.

What Is Grant and Weber?

Grant and Weber is a debt collection agency that collects unpaid debts for original creditors. If they appear on your credit report, it usually means an account has been sent to collections. Grant and Weber is headquartered in Calabasas, California and has been operating since 1977, making it one of the longer-standing debt collection agencies in the United States.

What Are Grant and Weber Known For?

Grant and Weber is known for collecting consumer debts, including healthcare and service-related accounts, and reporting collection accounts to credit bureaus. They are also known for aggressive collection tactics. The CFPB has received over 248 complaints against them, many alleging threatening or intimidating language during collection attempts and refusal to provide debt validation information when requested.

What consumers report about Grant and Weber

What real consumers say about Grant and Weber

How Long Has Grant and Weber Been in Business?

Grant and Weber has been operating since 1977, giving them nearly 50 years in the debt collection industry. They are one of the longer-established collection agencies in the United States, based in Calabasas, California. Their tenure makes them a known name in healthcare and medical debt collection, particularly across the Western United States.

Grant and Weber Has a BBB Rating of F. Their Records Are Not Always Accurate.

Nearly a third of all complaints against Grant and Weber allege they tried to collect a debt the consumer did not owe. Before you respond to their calls or pay anything, find out exactly what their entry says on your report and whether it is disputable. A free 3-bureau audit takes 2 minutes.

Can Grant and Weber Sue You for Debt?

Yes. Grant and Weber has an in-house legal team and has been a party to over 130 federal court cases. They can sue, but suing is not their standard practice and is unlikely for smaller balances. If you receive court papers from Grant and Weber, you must respond before the stated deadline or the court may issue a default judgment, giving them the authority to garnish wages or levy your bank account.

Unlike many smaller collection agencies that outsource all legal action, Grant and Weber has in-house attorneys. This means they can pursue litigation more efficiently than agencies that must hire outside counsel for every case. That said, multiple consumer law sources describe lawsuits as uncommon for average consumer balances. The risk increases significantly for balances over $1,000 and for consumers who ignore all contact entirely.

How Do I Remove Grant and Weber From My Credit Report?

To remove Grant and Weber from your credit report: send a written debt validation letter by certified mail requesting proof the debt is valid and theirs to collect. File FCRA disputes with all three bureaus if any error exists. If the debt is valid, negotiate a pay-for-delete agreement before paying. Note that Grant and Weber typically does not accept goodwill letters, so disputes and validation are the primary removal strategies.

Do I Have to Pay Grant and Weber?

You do not have to pay Grant and Weber until you have verified the debt is yours, the amount is correct, and it is within the statute of limitations. If the debt contains errors, you can dispute it without paying. If it is past the statute of limitations in your state, it may not be legally enforceable. If the debt is valid, always negotiate a written pay-for-delete agreement before making any payment.

There are three scenarios worth knowing before you make any decision about paying Grant and Weber:

- The debt is not yours or has errors: Do not pay. File validation and FCRA disputes first. Nearly a third of Grant and Weber complaints involve debts that were not owed. Confirm the debt is accurately yours before anything else.

- The debt is past the statute of limitations: Each state has a different window during which a creditor can sue to collect. In California, where Grant and Weber is based, the statute of limitations on medical debt is generally 4 years. If your debt is older than your state's limit, it is time-barred and you may not be legally required to pay it. Consult a consumer attorney before deciding.

- The debt is valid and within the statute of limitations: If you decide to pay, negotiate a written pay-for-delete agreement first. Paying without this agreement leaves the collection on your report as "paid" for up to 7 years. The payment alone does not remove the damage.

How to Dispute Grant and Weber on Your Credit Report

To dispute Grant and Weber on your credit report, file a written dispute with Equifax, Experian, and TransUnion identifying the specific error: wrong balance, wrong date, wrong creditor, already paid, or not your account. Attach any supporting documentation. The bureaus have 30 days to investigate. If Grant and Weber cannot verify the specific information you are disputing, the account must be removed from your report.

The most common disputable errors in Grant and Weber entries based on BBB and CFPB complaint records include:

- Original creditor listed incorrectly or not at all

- Balance that does not match the original provider's records after insurance adjustments

- Date of first delinquency that appears to be restarted rather than reflecting the original account date

- Account reporting after the 7-year FCRA removal period has passed

- Medical collection under $500 that should no longer appear per 2023 bureau policy

- Paid collection still showing as unpaid

As the CFPB explains, you have the right to dispute any item you believe is inaccurate. You do not need to prove the error is wrong. The burden falls on Grant and Weber to verify the information. If they fail to verify within the 30-day investigation window, the credit bureaus must remove the item.

Grant and Weber Does Not Make This Easy. We Handle Every Step.

Debt validation letters, FCRA disputes across three bureaus, pay-for-delete negotiations, and ongoing monitoring require time and documentation. Our team manages all of it simultaneously and tracks confirmed removals.

Full 3-bureau audit of every Grant and Weber entry and error

Certified debt validation letters sent to Grant and Weber

FCRA disputes filed with all three bureaus simultaneously

Pay-for-delete negotiation and bureau deletion confirmation

Most clients see the first confirmed bureau updates within 30 to 45 days.

Start My Free Credit Review → No obligation · Secure · Results within 30 to 45 days in most casesFrequently Asked Questions

What is Grant and Weber?

Grant and Weber is a debt collection agency that collects unpaid debts for original creditors. If they appear on your credit report, it usually means an account has been sent to collections. They are headquartered in Calabasas, California, have been in business since 1977, and specialize primarily in healthcare and medical debt collection.

What are Grant and Weber known for?

Grant and Weber is known for collecting consumer debts, including financial and service-related accounts, and reporting those accounts to the credit bureaus. They are also known for aggressive collection practices. The CFPB has received over 248 complaints against them, many alleging threatening language and refusal to provide debt validation when consumers request it.

How long has Grant and Weber been in business?

Grant and Weber has been operating since 1977, giving them nearly 50 years in the debt collection industry. They are one of the more established collection agencies in the United States, based in Calabasas, California and known primarily for healthcare and medical debt collection.

Is Grant and Weber legit or a scam?

Grant and Weber is a legitimate, licensed debt collection agency, not a scam. However, they carry a BBB rating of F, over 248 CFPB complaints, and a WalletHub score of 2.5 out of 5. Legitimate does not mean every debt they report is accurate. Nearly a third of complaints against them allege they attempted to collect a debt not owed. Always request written validation before paying.

Can Grant and Weber sue you for debt?

Yes. Grant and Weber has an in-house legal team and has been involved in over 130 federal court cases. They can sue for unpaid debt, though suing is not their standard approach for smaller balances. If you receive court papers, respond before the stated deadline or risk a default judgment that can lead to wage garnishment.

How do I remove Grant and Weber from my credit report?

Send a written debt validation letter by certified mail. File FCRA disputes with all three bureaus if errors exist. Negotiate a written pay-for-delete agreement if the debt is valid before making any payment. Grant and Weber typically does not accept goodwill letters, so formal disputes and validation are the primary removal strategies.

How do I stop Grant and Weber from calling me?

Send a written cease-and-desist letter by certified mail to Grant and Weber at 26650 Agoura Road, Suite 102, Calabasas, CA 91302. Under the FDCPA, they must stop all collection contact after receiving your letter. The only permitted follow-up is a single written notice confirming receipt or notifying you of a specific legal action. Any continued calls after confirmed delivery are FDCPA violations.

Related Reads and Additional Resources

- Capio Partners on Your Credit Report: How to Remove It — The largest medical debt buyer in the U.S. If both Capio Partners and Grant and Weber appear on your report, the same validation and dispute process applies to both simultaneously.

- How to Handle Debt Collection Calls, Validation Letters, and Negotiations — Phone scripts, letter templates, and pay-for-delete negotiation strategies that work for Grant and Weber too.

- National Enterprise Systems: Who They Are and How to Handle Them — Another established debt collector with a similar complaint profile and removal process.

- CFPB: How to Dispute an Error on Your Credit Report — Official federal guide to your FCRA dispute rights, bureau contact information, and what to include in your dispute.

- FTC: Debt Collection FAQs — Your full rights under the FDCPA including validation, cease-and-desist, and complaint filing procedures.