Debt consolidation can cause a small, temporary drop in your credit score. But does debt consolidation hurt your credit score in the long run? No. When done right, consolidation improves your score over time by lowering your credit utilization and building a clean payment history.

Running a credit repair company, I see this fear hold people back all the time. One case that stands out: a client with $24,000 in credit card debt across six cards refused to consolidate for eight months because he was afraid of hurting his 612 score. He finally moved forward. His score dipped 4 points after the hard inquiry. Twelve months later, it was at 684. The temporary hit cost him almost nothing. The delay cost him thousands in interest.

According to the Federal Reserve Bank of New York, Americans now carry over $1.25 trillion in total credit card debt. The average cardholder with an unpaid balance owes $7,321. At the current average APR of 21.2%, that balance costs more than $1,500 per year in interest alone. Debt consolidation exists to solve exactly that problem.

Does Debt Consolidation Hurt Your Credit Score?

The short answer is: temporarily, yes. Permanently, no.

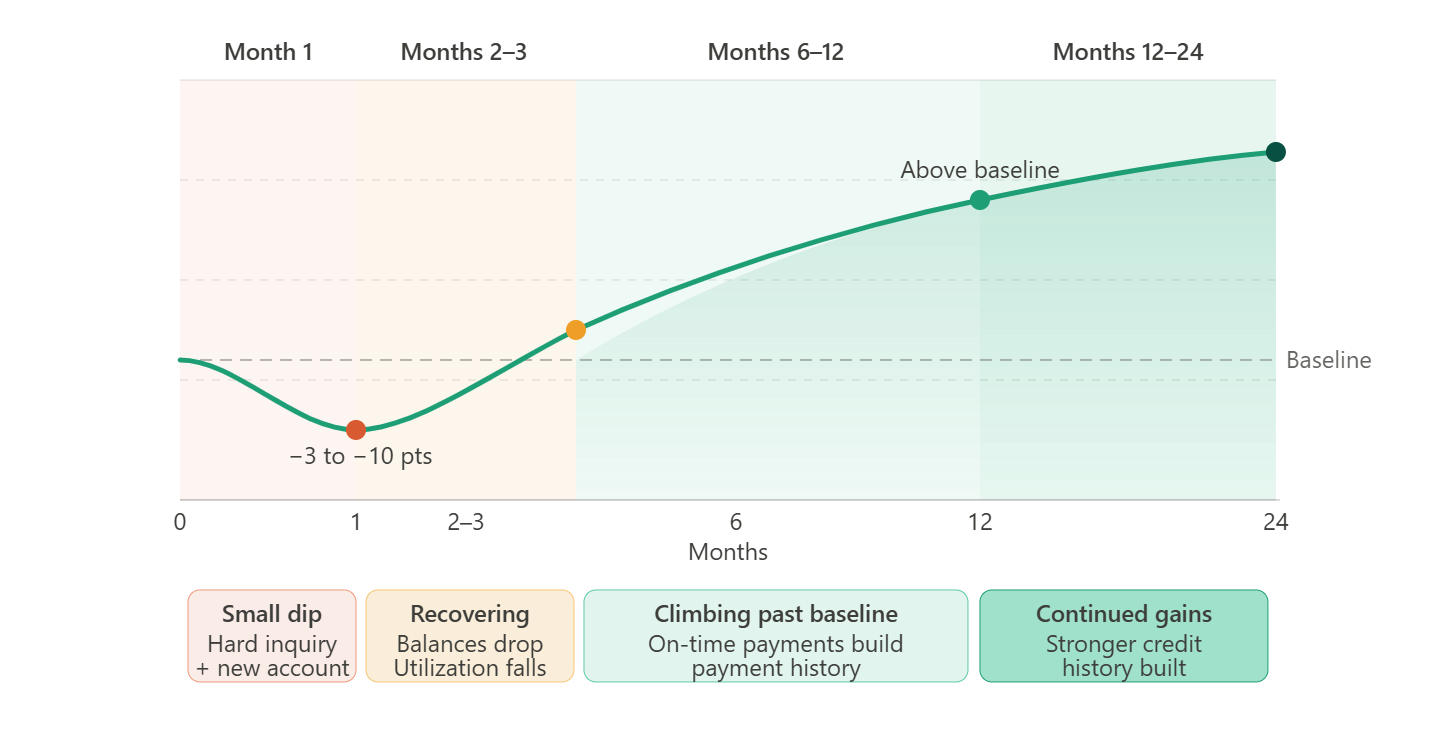

Debt consolidation causes a small dip right after you apply. That dip comes from a hard inquiry. A hard inquiry is what happens when a lender checks your credit to approve your loan. According to Experian, a single hard inquiry typically drops your score by fewer than 5 points. That impact fades within 12 months and falls off your report entirely after two years.

After the short-term dip, consolidation starts working in your favor. You lower your credit card balances. Your credit utilization drops. You make one payment on time every month. Those three things together push your score up over the following months.

The key rule: consolidation helps your score if you stop adding new debt. It hurts your score if you pay off your cards and then run them back up.

How Much Does Debt Consolidation Drop Your Credit Score?

Most borrowers see a drop of 3 to 10 points right after applying. Here is what drives that number:

Hard inquiry — drops your score by 1 to 5 points. This happens the moment a lender pulls your credit.

New account age — opening a new loan lowers the average age of your accounts. A shorter credit history slightly reduces your score.

Closed accounts — if you close old credit cards after paying them off, you lose available credit. That raises your utilization ratio and can lower your score.

The drop is usually small. Borrowers with longer credit histories feel it less. Borrowers with thin credit files or histories under two years may feel it more.

The good news: hard inquiries only count toward your FICO score for 12 months. After that, they stop affecting the calculation entirely, even though they stay visible on your report for two years.

What Types of Debt Consolidation Affect Your Credit Score?

Not all consolidation methods work the same way. Each one touches your credit differently.

Personal Loan

A personal loan replaces multiple debts with one fixed monthly payment. The lender does a hard inquiry when you apply. Opening the loan adds a new account and lowers your average account age. But paying off your credit cards drops your utilization, which helps your score quickly.

This is the most common method for borrowers with good credit. It works well when your loan rate is lower than your current card rates.

Balance Transfer Credit Card

A balance transfer card moves your credit card debt to a new card with a low or 0% intro APR. The new card requires a hard inquiry. It also adds a new account.

Watch out for one risk: if you transfer a large balance to a single card, the utilization on that one card can spike. High utilization on any single card hurts your score, even if your total utilization is low.

Debt Management Plan

A debt management plan (DMP) works through a nonprofit credit counseling agency. The agency negotiates lower interest rates with your creditors. You make one payment to the agency each month.

A DMP does not require a new loan, so there is no hard inquiry. But most DMPs ask you to stop using your credit cards. If you close those cards, your available credit drops. That raises your utilization and can lower your score.

In our office last year, we reviewed 35 clients who used DMPs. The average score dip in the first three months was 18 points. But by month 12, those same clients had scores averaging 44 points higher than when they started the plan.

At this point, you know what each method does to your score in the short term. Now let's look at how consolidation helps your score over time.

Does Debt Consolidation Help Your Credit Score Long-Term?

Yes. Debt consolidation almost always improves your score over 12 to 24 months when you stick to the plan.

Credit utilization makes up 30% of your FICO score. It is the second-biggest factor after payment history. When you pay off five credit cards with a consolidation loan, your utilization on those cards drops to zero. That improvement shows up on your score within 30 to 60 days of the balances being reported.

Payment history makes up 35% of your FICO score. One on-time payment each month on your consolidation loan builds that history steadily. Twelve months of clean payments can add significant points, especially for borrowers who have had late payments in the past.

The timeline most clients follow:

The only way this timeline fails is if you charge the paid-off cards back up. That is the most common mistake we see. The card balances go to zero, the score goes up, and then the client starts spending again. Within six months, they will have both the consolidation loan and the credit card debt.

Does Closing Credit Cards After Consolidation Hurt Your Score?

Yes. Closing credit cards after paying them off is one of the biggest mistakes in the consolidation process.

When you close a card, two things happen. First, you lose the available credit on that card. Your total available credit goes down. That raises your utilization ratio on the cards you still have open. Second, if the closed card was one of your oldest accounts, closing it can shorten your average credit history.

The better move: pay off the cards, keep them open, and stop using them. Set up a small recurring charge on each card, like a streaming subscription. Pay it off in full every month. This keeps the account active, maintains your available credit, and builds payment history.

How Long Does Debt Consolidation Affect Your Credit Score?

The negative effects are short-term. The positive effects last as long as you manage the account well.

Hard inquiry impact: up to 12 months on your score, visible on your report for 24 months.

New account impact: 3 to 6 months, as the account ages and the newness penalty fades.

Utilization improvement: immediate, usually appearing within one billing cycle after balances are paid.

Payment history improvement: ongoing, building with each on-time payment you make.

For most borrowers, the total net effect of debt consolidation on their credit score is positive within 6 to 12 months of starting the plan.

What Is the Best Way to Consolidate Debt Without Hurting Your Credit?

Follow these steps to reduce the impact on your score:

Check your credit before applying. Know your score before any lender pulls it. Use a free soft inquiry through your bank or a credit monitoring service.

Apply to one lender at a time. Multiple hard inquiries within 14 to 45 days count as one inquiry for rate-shopping purposes on mortgage and auto loans. For personal loans, the rules vary by lender. To be safe, apply to one lender first.

Do not close paid-off cards. Keep them open and use them lightly. Your available credit helps your utilization ratio.

Set up autopay immediately. One missed payment erases months of progress. Autopay removes that risk entirely.

Do not take on new debt. The consolidation plan only works if the total debt goes down each month.

According to a CFPB report on debt management, consumers who complete a debt management plan see both their debt and their interest costs fall significantly over the life of the plan. Completion rates rise when borrowers automate their payments and avoid new credit card use during the repayment period.

Frequently Asked Questions

Does debt consolidation show up on your credit report? Yes. A consolidation loan appears as a new installment account. A balance transfer appears as a new credit card. Both show the balance and payment history going forward.

Can you consolidate debt with bad credit? Yes, but your options are narrower. Secured loans, credit unions, and nonprofit DMPs are the most accessible paths for borrowers with scores below 620. Interest rates will be higher on any personal loan you qualify for.

Is debt settlement the same as debt consolidation? No. Debt settlement negotiates to pay less than you owe. It severely damages your credit score and stays on your report for seven years. Debt consolidation pays your debts in full and protects your credit history.